Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

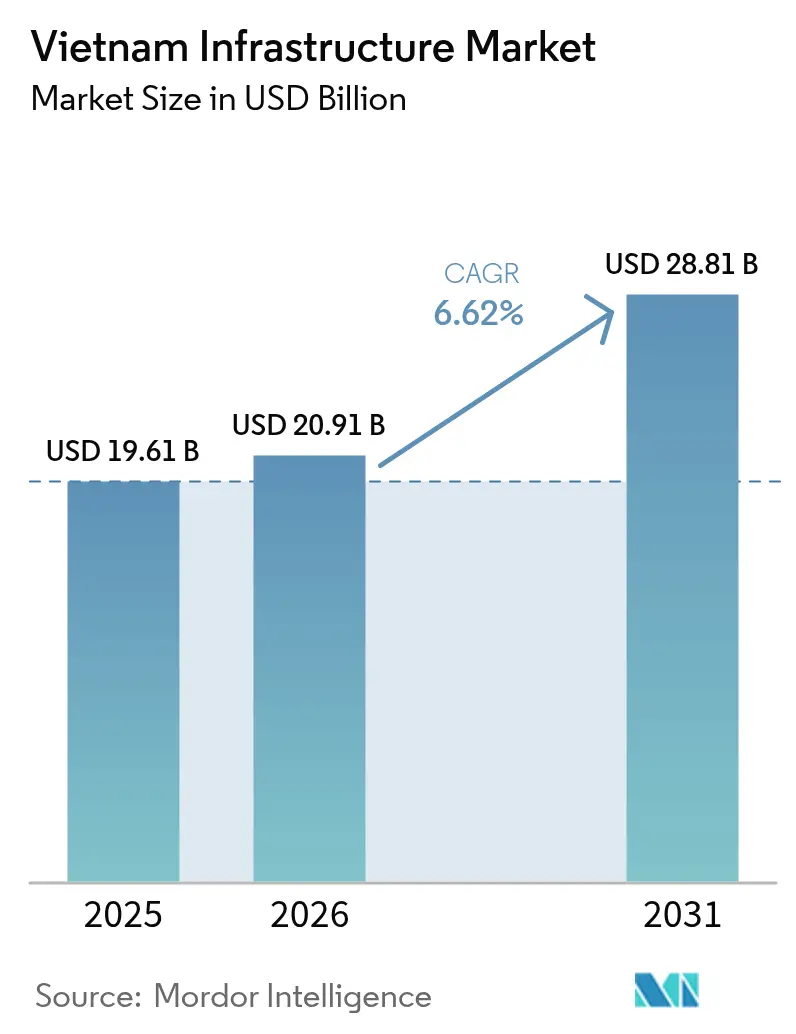

| Base Year Market Size (2025) | USD 19.61 Billion |

| Market Size (2026) | USD 20.91 Billion |

| Market Size (2031) | USD 28.81 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

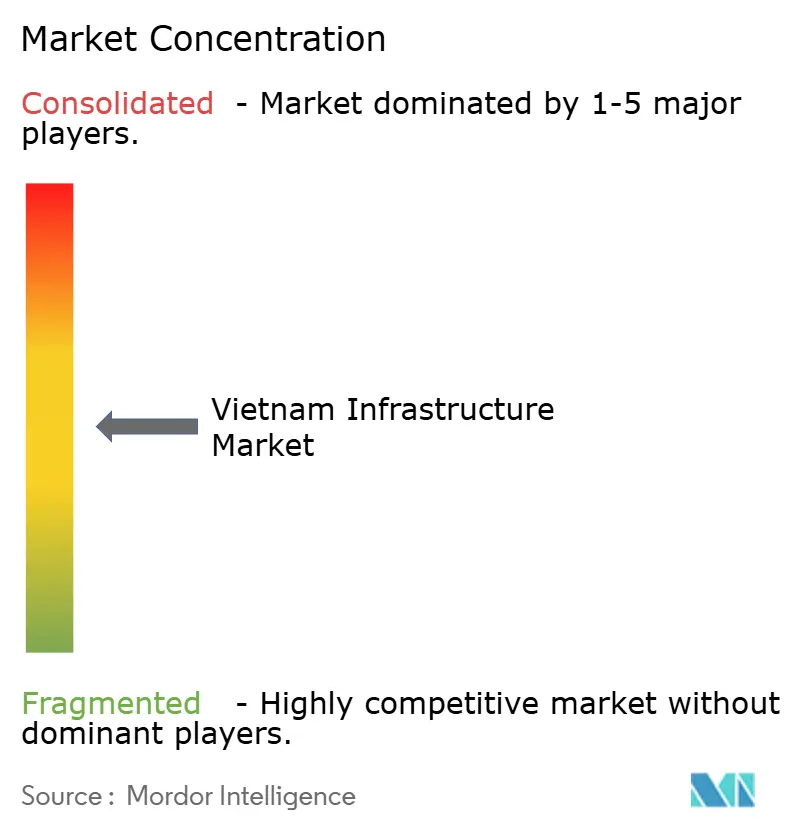

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Infrastructure Market Analysis by Mordor Intelligence

The Vietnam infrastructure market size was valued at USD 19.61 billion in 2025 and estimated to grow from USD 20.91 billion in 2026 to reach USD 28.81 billion by 2031, at a CAGR of 6.62% during the forecast period (2026-2031). Ongoing logistics bottlenecks, rising industrial relocation into Vietnam, and decisive government spending plans are combining to keep large projects moving through the approval pipeline, even as global capital costs remain elevated. Transportation continues to command investor attention because expressways, rail corridors, and airports unlock manufacturing exports, while utility assets are gaining momentum on the back of grid-ready renewable capacity targets. Policy reforms, from faster PPP approvals to risk-sharing mechanisms, are lowering entry barriers for private developers and diversifying funding sources. At the same time, severe contractor fragmentation, sand shortages, and delayed public disbursements highlight execution risks that can inflate budgets and elongate project timelines.

Key Report Takeaways

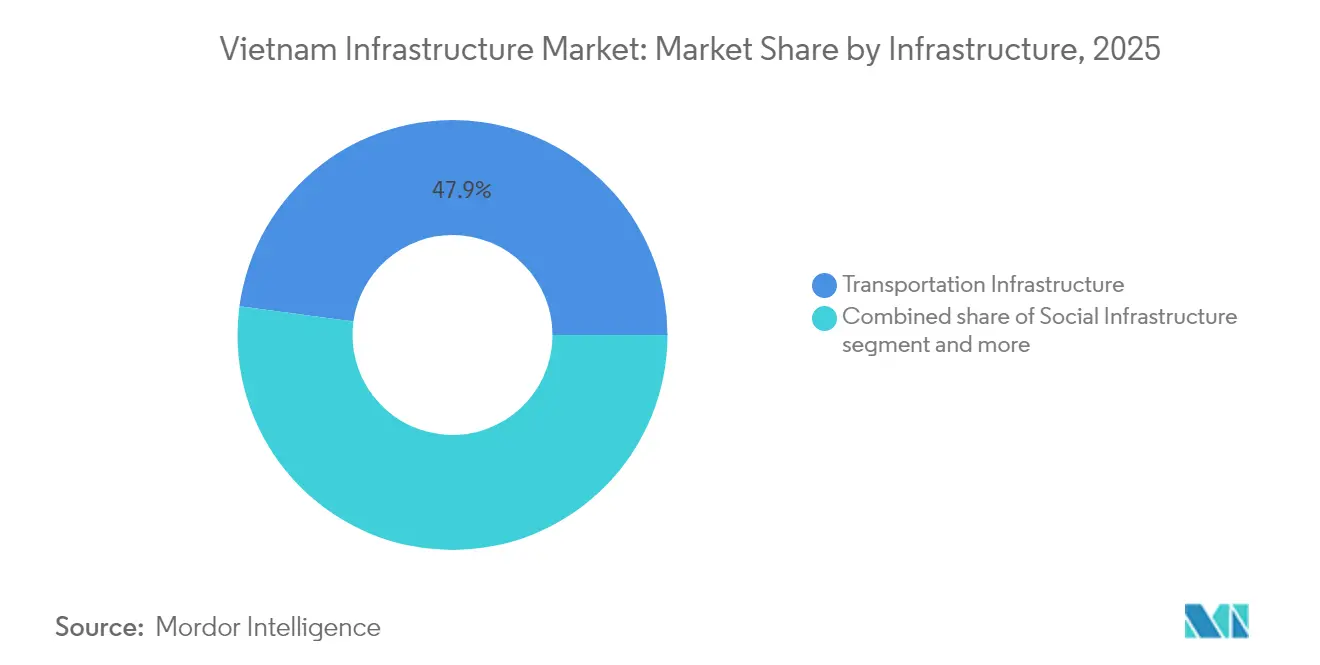

- By infrastructure type, transportation held 47.86% of Vietnam's infrastructure market share in 2025, while utilities are projected to expand at an 8.58% CAGR to 2031.

- By construction type, new construction accounted for 77.45% of the Vietnam infrastructure market size in 2025; renovation work is advancing at an 8.33% CAGR through 2031.

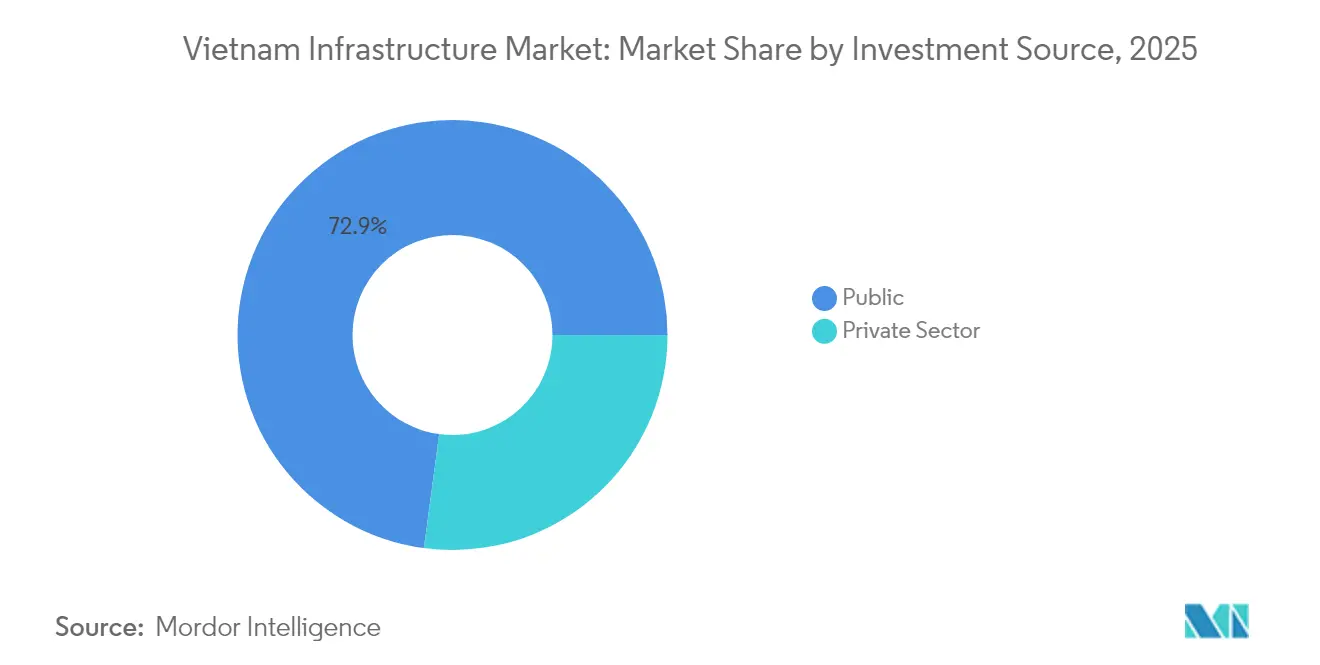

- By investment source, public funding captured a 72.88% share of the Vietnam infrastructure market in 2025, whereas private investment is forecast to rise at a 9.06% CAGR between 2026 and 2031.

- By geography, Ho Chi Minh City led with 41.72% of 2025 spending, while Da Nang is set to deliver the quickest gains at an 8.12% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Infrastructure Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of the public-sector CAPEX pipeline | +1.8% | National, with concentration in HCMC and Hanoi | Medium term (2-4 years) |

| Surge in foreign-funded mega-projects (ODA & FDI) | +1.5% | National, with emphasis on Northern and Southern economic corridors | Long term (≥ 4 years) |

| Accelerated PPP adoption under the 2024 amended PPP Law | +1.2% | National, with early gains in HCMC, Da Nang, Hanoi | Short term (≤ 2 years) |

| Electrification & grid-ready renewables build-out | +1.0% | National, with offshore wind focus in Southern provinces | Medium term (2-4 years) |

| Provincial sand-shortage resolution unlocking road/rail projects | +0.8% | Central and Southern Vietnam, particularly Da Nang and Khanh Hoa | Short term (≤ 2 years) |

| TOD zoning around new metro & HSR stations | +0.7% | HCMC, Hanoi, with spillover to Can Tho and Hai Phong | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of the Public-Sector CAPEX Pipeline

The government lifted its 2025 public investment allocation to USD 3.5 billion, 12% above 2024, and aims for full disbursement before year-end. Standardized construction cost norms under Decision 409/QĐ-BXD now guide spending and shrink approval backlogs. Eighty priority projects worth USD 18.4 billion were green-lit in April 2025, giving contractors forward visibility and boosting cement demand, which is expected to rise 15% annually through 2027. Higher public outlays stimulate jobs, materials, and equipment sales across the Vietnam infrastructure market. Continuous monitoring of disbursement progress is likely to keep pressure on ministries to maintain schedule discipline[1]Nguyen Thanh Lam, “Decision 409/QĐ-BXD on Construction Investment Rates,” Ministry of Construction, moc.gov.vn.

Surge in Foreign-Funded Mega-Projects (ODA & FDI)

FDI into Vietnamese infrastructure reached USD 38.23 billion in 2024, led by Singapore, South Korea, and Japan. Iconic examples include Huadian’s USD 2.4 billion green-hydrogen complex and the USD 14 billion Long Thanh International Airport. Foreign EPC firms bring advanced project-management practices, but their dominance also heightens competition for domestic builders. To preserve local capabilities, the government now reserves 30% of public contracts for Vietnamese bidders. A steady pipeline of ODA-backed highways and power plants should keep the Vietnam infrastructure market attractive to global investors well into the next decade[2]Pham Hong Son, “FDI Statistics 2024,” Foreign Investment Agency, fia.gov.vn.

Accelerated PPP Adoption Under the 2024 Amended PPP Law

Reforms cut approval cycles from 18 months to roughly 12 months, introduce revenue-risk-sharing, and mandate arbitration by the Vietnam International Arbitration Centre. VinGroup’s USD 4 billion Can Gio metro secured preliminary consent just eight months after filing, demonstrating early gains. Shorter timelines reduce interest-during-construction costs and lift project IRRs, encouraging private participation. Quicker closings also move the Vietnam infrastructure market toward regional best practice, outpacing Thailand and Indonesia on procedural efficiency. Consistent enforcement will determine whether investor optimism endures[3]Le Thi Thu Hang, “Amended PPP Law 2024—Key Provisions,” National Assembly of Vietnam, quochoi.vn.

Electrification & Grid-Ready Renewables Build-Out

Power Development Plan VIII targets 47% renewables by 2030, requiring USD 136 billion of new grid assets. Offshore wind clusters in Binh Thuan and Ca Mau, coupled with the USD 10 billion Cá Voi Xanh gas-to-power chain, balance intermittent supply. Electricity of Vietnam is rolling out 500 kV links and 15 million smart meters by 2027, while the national oil and gas group is planning 2 GW of battery storage. These upgrades create opportunities for equipment vendors and EPC contractors and add resilience to the Vietnam infrastructure market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented contractor landscape driving cost overruns | -1.5% | National, with acute impact in complex infrastructure projects | Medium term (2-4 years) |

| Weak absorptive capacity of public-investment disbursement | -1.2% | National, with 19 ministries and 28 localities showing poor performance | Short term (≤ 2 years) |

| Chronic scarcity of high-spec construction aggregates | -0.8% | Central and Northern Vietnam, particularly affecting highway projects | Medium term (2-4 years) |

| Volatile long-term VND bond yields curb domestic PPP financing | -0.5% | National, with particular impact on private infrastructure financing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Contractor Landscape Driving Cost Overruns

More than 50,000 registered builders share the market, and the top 10 hold only 15% of revenue. Coordination across dozens of subcontractors inflates costs by 20-35% and prolongs scheduling on mega-projects such as the North-South Expressway. International firms like Kajima and GS E&C fill capability gaps but charge premiums. The Ministry of Construction is promoting mergers and joint ventures to create 5-7 national champions by 2030, yet regional contractors often resist consolidation. Until scale improves, the Vietnam infrastructure market will continue to face budget volatility and quality risks.

Weak Absorptive Capacity of Public-Investment Disbursement

By July 2025, ministries had released only 43.9% of planned funds versus a 65% target. Deferred feasibility studies, thinly detailed environmental assessments, and additional three-to-six-month delays under Circular 08/2025/TT-BXD weigh on timelines. Suppliers such as Hoa Phat Steel reported 25% lower Q1 2025 sales because of slow site mobilization. Project cash-flow shortages ripple through subcontractor networks, creating claims and litigation. Unless administrative capacity rises, fresh allocations could translate slowly into on-ground progress, limiting the near-term upside for the Vietnam infrastructure market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infrastructure: Transportation Dominance Drives Mega-Project Pipeline

Transportation captured 47.86% of Vietnam's infrastructure market share in 2025, thanks to marquee assets such as the USD 67 billion North-South High-Speed Railway and the USD 59 billion expressway expansion. Utilities assets, though smaller, are projected to grow faster at an 8.58% CAGR.

The transportation build-out anchors supply-chain resilience for export-oriented manufacturers, reducing door-to-port times and lowering logistics charges. Conversely, grid expansion underpins Vietnam’s energy transition and supplies industrial parks with reliable power, making utilities the next magnet for private capital.

By Construction Type: New Construction Leads Amid Urban Renewal Acceleration

New construction accounted for 77.45% of the Vietnam infrastructure market size in 2025, lifted by 80 priority projects. Renovation, however, is gaining traction with an 8.33% CAGR, mirroring the shift toward asset optimization in dense urban zones.

Standardized cost norms are shortening approval cycles for greenfield sites, whereas aging districts in Ho Chi Minh City and Hanoi need systematic upgrades, from drainage to digital connectivity, to accommodate rising populations. The Vietnam infrastructure market share tied to renovation is poised to climb as transit-oriented redevelopment drives mixed-use projects and lifts land values. Both segments, therefore, coexist: greenfield build-out plugs infrastructure gaps, and brownfield renewal maximizes land efficiency in mature districts.

By Investment Source: Private Sector Momentum Builds Despite Public Dominance

In 2025, public funds supplied 72.88% of investment, reflecting Vietnam’s reliance on fiscal outlays to fix its infrastructure deficit. Yet private participation is forecast to expand at a 9.06% CAGR following the 2024 PPP reforms that compress approval timelines to roughly 12 months.

VinGroup’s USD 4 billion Can Gio metro and industrial-park pipeline illustrates newfound confidence among domestic conglomerates, while Singaporean and South Korean investors channel capital into logistics and power assets. Enhanced risk-sharing and streamlined arbitration attract insurers and pension funds seeking long-dated cash flows, smoothing funding diversity for the Vietnam infrastructure market.

Geography Analysis

Ho Chi Minh City retained 41.72% of the Vietnam infrastructure market share in 2025, owing to its USD 4 billion metro expansion and 535-project Thu Duc City blueprint. The metropolitan plan piles resources into roads, flood management, and digital utilities, complementing port and airport upgrades that will cement the city’s regional logistics role. Transit-oriented zoning lifts real-estate values around stations by up to 40%, mobilizing private co-investment and amplifying fiscal returns for local authorities.

Hanoi is advancing Metro Line 5 and supporting the USD 2.8 billion Dong Dang-Pingxiang economic corridor, strengthening its position as a trade conduit between China and ASEAN. Improvements to Noi Bai Airport access and ring-road capacity reduce congestion, while housing and social-service facilities keep pace with expanding administrative functions.

Da Nang, the fastest-growing region with an 8.12% CAGR through 2031, benefits from the VND 43.9 trillion (USD 1.8 billion) Lang Van tourism project and an airport expansion that will triple passenger handling. Its coastal setting and midway location between Hanoi and Ho Chi Minh City attract logistics and electronics manufacturers. Residual regions leverage the USD 59 billion expressway program, renewable-energy clusters, and 100 border-school upgrades to spur inclusive growth, broadening the reach of the Vietnam infrastructure market.

Regulatory Landscape

Vietnam’s infrastructure delivery is overseen through the construction management framework led by the Ministry of Construction (MoC), with conformity standards anchored in STAMEQ and referenced through the national construction standards portal. The Law on Construction 2025 (No. 135/2025/QH15), passed on December 10, 2025 and effective July 1, 2026, updates project management and compliance expectations for developers and contractors. This aligns with the Construction Industry Development Strategy to 2030 under Decision 179/QD-TTg (February 16, 2024), which prioritizes green materials, BIM-enabled delivery, and higher-complexity construction capabilities to support national infrastructure modernization.

Value Chain Analysis

Vietnam’s infrastructure value chain covers planning and capital allocation, design and engineering, procurement, construction, and asset commissioning and operations. Upstream, building materials and logistics remain key determinants of both cost and schedule. Midstream, the contractor base is highly fragmented, which raises coordination demands and increases the need for capable integrators and subcontractors for foundations, structures, and MEP packages. Downstream, owners and operators influence contractor selection and payment cycles, so digital compliance, transparent capacity disclosure, and stronger project controls become more relevant as firms broaden from pure contracting into PPP participation and specialized infrastructure packages.

Competitive Landscape

The sector remains moderately fragmented: over 50,000 contractors compete, and the top 10 collectively command only 15% of revenue. This structure hampers coordination on mega-projects and leads to cost overruns. Merger incentives seek to carve 5-7 national champions by 2030 that can bid head-to-head against global EPC heavyweights like GS E&C and Kajima.

Technology adoption is a critical differentiator. Hoa Binh Construction’s PRC V+ methodology lowers steel usage by 45% and concrete by 50%, cutting embodied carbon and appealing to ESG-minded financiers. Early movers in BIM and digital project controls report faster cycle times and fewer claims. Partnerships with state agencies remain decisive for public work, while specialized expertise, particularly in renewables and smart cities, creates defensible niches. As competition intensifies, firms able to combine cost discipline, technical depth, and regulatory fluency are positioned to gain share in the Vietnam infrastructure market.

Vietnam Infrastructure Industry Leaders

Vietnam Expressway Corporation (VEC)

Coteccons Construction JSC

Hoa Binh Construction Group JSC

Central Power Corporation (EVNCPC)

Song Da Corporation JSC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A broad project pipeline is forming as the government pushes large transport plans toward more bankable packages and tightens disbursement discipline. The Lao Cai-Hanoi-Hai Phong railway line investment guidelines, anchored by a total investment of 203.23 trillion VND, create demand across rail civil works, stations, bridges, and supporting utilities. In parallel, the 2026-2030 medium-term public investment plan (Resolution 27/2026/QH16) targets higher disbursement and fewer active projects, which tends to favor contractors and consultants able to run multi-site programs and standardized designs. Regulatory and digitalization measures also broaden demand for compliance tooling, green materials, and higher-productivity delivery methods. The Law on Construction 2025 taking effect July 1, 2026, along with the Construction Industry Development Strategy under Decision 179/QD-TTg, highlights green and smart standards and digital practices such as BIM, supporting needs for low-carbon materials, project controls, and engineering services that reduce rework and claims. Additional updates on unified electronic identification for residential properties (Decree 357/2025/ND-CP, effective January 3, 2026) and social housing rules (Decree 136/2026/ND-CP, effective April 7, 2026) further strengthen enabling infrastructure demand around large urban developments.

Recent Industry Developments

- July 2026: The Government directed that Long Thanh International Airport Phase 1 be brought into operation within 2026, reinforcing schedule pressure across airside works, landside connections, and supporting utilities. The instruction increases near-term procurement and commissioning readiness for contractors and suppliers tied to one of Vietnam’s flagship transport nodes.

- August 2025: Vietnam cleared a set of priority projects spanning highways, power plants, and urban schemes across 15 provinces. The approvals expanded the executable pipeline for EPCs and materials suppliers while increasing cross-regional delivery capacity.

- March 2024: Huadian began construction of a green-hydrogen facility in Tra Vinh, including electrolysis units and export terminals. The project strengthened demand for complex industrial civil works, port-adjacent enabling infrastructure, and power and utilities integration capabilities.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market is defined as the value of infrastructure development activity in Vietnam, counted across major asset types where spend can be tracked and forecast in USD.

Scope exclusions: It does not count routine operations and maintenance spending, pure land acquisition costs, or project financing fees that are not part of on-the-ground build activity.

Segmentation Overview

- By Infrastructure

- Transportation Infrastructure

- Utilities Infrastructure

- Social Infrastructure

- Extraction Infrastructure

- By Construction Type

- New Construction

- Renovation

- By Investment Source

- Public

- Private

- By Geography

- Ho Chi Minh City

- Hanoi

- Da Nang

- Rest of Vietnam

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping Vietnam infrastructure plans and budgets into a consistent spend view, then checking how that spend flows into actual project work. Public sources are used to anchor the model, including Vietnam government investment plans and ministry publications, General Statistics Office releases, World Bank and Asian Development Bank infrastructure notes, and customs or trade statistics for key construction-linked materials.

Alongside that, we review listed-company filings and investor presentations for construction and utility operators, plus project announcements and reputable press coverage, to understand timing shifts. When helpful, paid subscriptions for company financials and for shipment-level trade data are used to fill gaps in financial splits and to sanity-check import-driven demand signals. The desk sources listed here are illustrative, and many other public materials were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test desk assumptions on project execution, budget release timing, and how reported capex translates into real construction value during the year. We speak with a mix of EPC and contractor teams, public and private project owners, developers, and materials and logistics-linked participants, with coverage spread across Vietnam to avoid over-weighting one city or one funding source.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 14% | |

| Mid tier: 49% | Functional/Unit leaders: 27% | |

| Smaller Players: 21% | Managers: 59% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where public investment plans, sector capex signals, and project pipeline information are used to reconstruct annual infrastructure spend in Vietnam, then aligned to what gets executed within the year. Once that spend pool is formed, selective bottom-up checks are run to cross-check the totals, such as sampled project ticket sizes by asset type, basic contractor revenue mapping, and volume times ASP checks for major inputs where pricing is observable.

Key inputs vary by asset type, but they typically include public disbursement pace, private investment commitments, project start and completion timing, capacity additions (for utilities), and trade-linked indicators for critical materials. Where pricing is needed, we use clear USD conversion timing and simple inflation or contract-price progression assumptions, which are validated through interviews. Forecasting is mainly done through scenario analysis, where base, faster execution, and slower execution cases are created around budget release timing, approval pipeline movement, and the cost environment, and then consolidated into one central forecast.

Data Validation & Update Cycle

Validation is done in steps so obvious errors are caught early and judgment calls are documented. Model outputs are compared against independent signals, including budget utilization patterns, major project milestone news, and construction activity indicators, and then large variances are traced back to an input such as timing, pricing, or scope mapping.

Before sign-off, the numbers go through a second-analyst review, and follow-up calls are triggered when a key assumption moves or when a new project decision changes the yearly execution profile. Reports are refreshed annually, and interim updates are made when material events occur. Right before delivery, a final pass is completed so clients receive the latest updated view available at that time.

Mordor Intelligence's Vietnam Infrastructure Sector Market Size Versus Other Published Estimates

Published market sizes for Vietnam infrastructure can differ even when the topic name looks similar, because the year chosen, what gets counted as infrastructure, and how project timing is treated are not consistent across sources. Currency conversion timing, and whether values reflect planned budgets or executed work in-year, also create noticeable spread.

The benchmark table shows a higher 2025 figure than some other sources, and in Mordor Intelligence's model the scope includes social, transportation, utilities, extraction, and manufacturing-related infrastructure, then ties annual values to expected execution during the year rather than only listing planned allocations.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 19.61 B (2025) | |

| Industry Publisher A | USD 15.40 B (2025) | Uses a narrower inclusion set and tends to group infrastructure more like a standard segment list, which can leave out some manufacturing-linked infrastructure and can apply different execution timing when converting pipeline and budgets into annual market value. |

| Global Consultancy B | USD 18.33 B (2023) | Uses an earlier base year and a different forecast window, so the value reflects a different cost cycle and project mix. The scope write-up is also less clear on how planned spend is converted into delivered work, which can shift totals when large projects slip across years. |

Overall, the spread is mostly explained by scope boundaries, base year choice, and whether the estimate is anchored to executed activity versus broader planned investment. By keeping inputs tied to observable plan, pipeline, and execution signals, the final number stays easier to trace and repeat when assumptions are updated.

Key Questions Answered in the Report

How large is the Vietnam infrastructure market in 2026 and what is its growth outlook?

The market is valued at USD 20.91 billion in 2026 and is projected to reach USD 28.81 billion by 2031, reflecting a 6.62% CAGR.

Which infrastructure segment attracts the most spending?

Transportation leads with 47.86% of 2025 outlays, backed by expressway and high-speed rail megaprojects.

Which segment is growing the fastest?

Utilities infrastructure is expanding at an 8.58% CAGR through 2031, driven by renewable energy and grid investments.

What reforms are spurring private investment in Vietnamese infrastructure?

The 2024 amended PPP Law shortens approvals to 12 months and introduces risk-sharing, boosting investor confidence.

Page last updated on: