Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

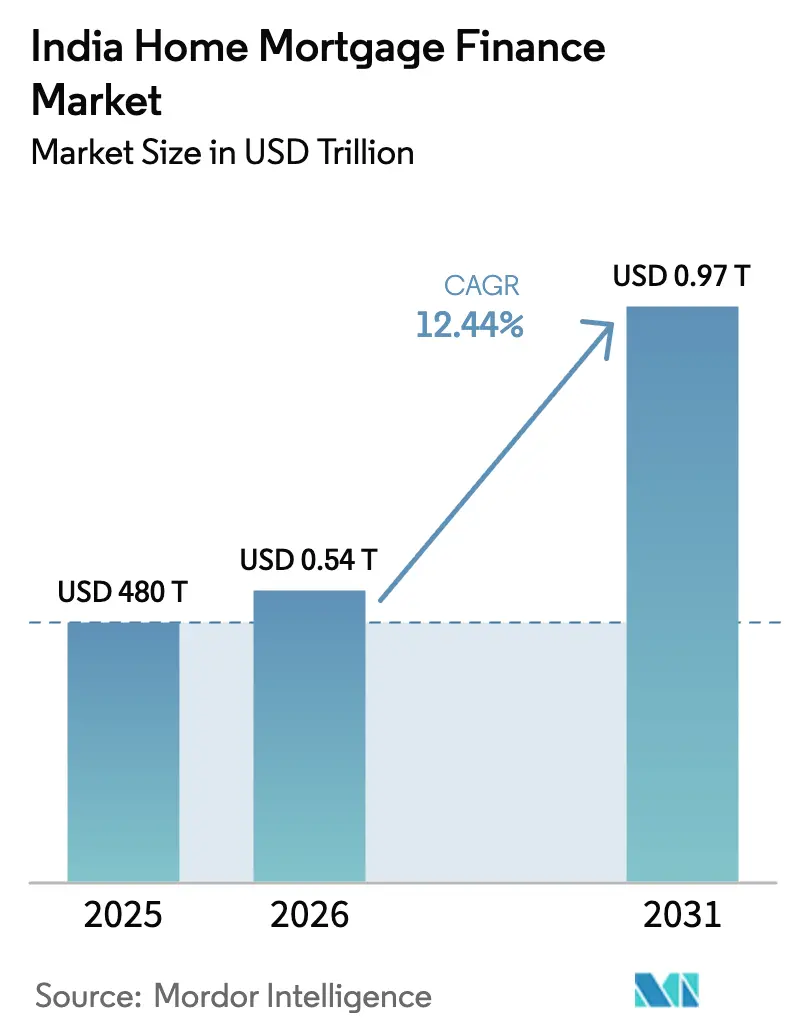

| Base Year Market Size (2025) | USD 480 Trillion |

| Market Size (2026) | USD 0.54 Trillion |

| Market Size (2031) | USD 0.97 Trillion |

| Growth Rate (2026 - 2031) | 12.44% CAGR |

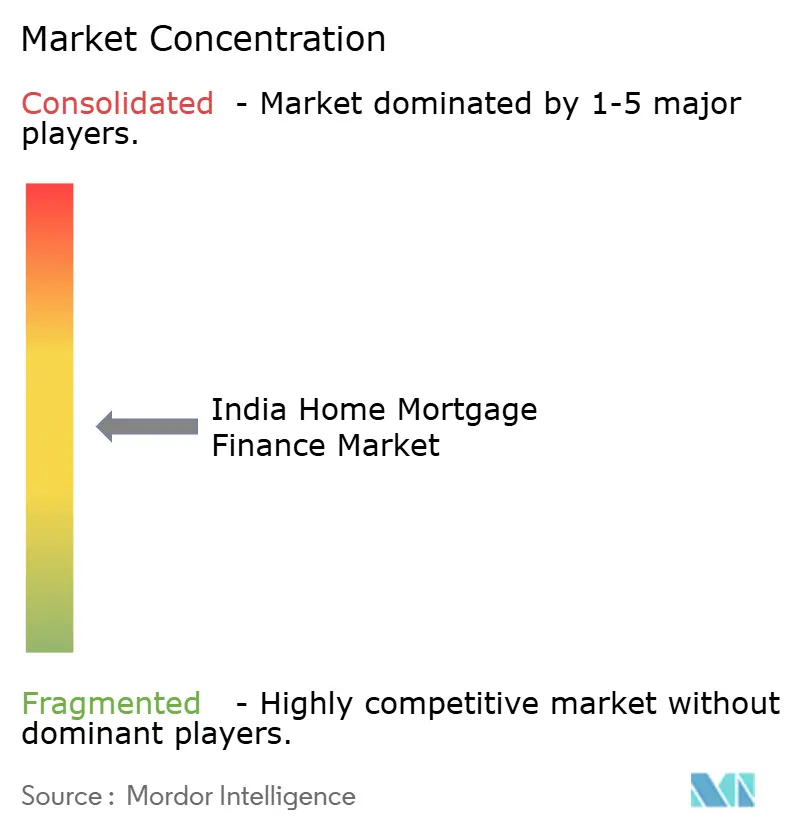

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Home Mortgage Finance Market Analysis by Mordor Intelligence

India home mortgage finance market size in 2026 is estimated at USD 539.71 billion, growing from 2025 value of USD 480 billion with 2031 projections showing USD 969.52 billion, growing at 12.44% CAGR over 2026-2031. The surge reflects a structural rather than cyclical shift, propelled by subsidy-backed demand, easier monetary conditions, institutional appetite for the country’s debut residential mortgage-backed securities (RMBS), and widespread digital-onboarding infrastructure. A 100 basis-point repo-rate cut has improved affordability, the expanded PMAY-Urban 2.0 budget has created predictable loan pipelines, and open-API lending rails have shortened approval times from weeks to days[1]Ministry of Housing & Urban Affairs, “PMAY-Urban Mission Guidelines,” mohua.gov.in. Further momentum arises from AI-driven underwriting that unlocks thin-file borrowers, while the first RMBS listing re-prices lender funding costs, allowing housing finance companies (HFCs) to challenge deposit-funded banks on price without compromising service agility. This convergence of policy and technology is tilting competitive boundaries and sustaining double-digit expansion across the Indian home mortgage finance market.

Key Report Takeaways

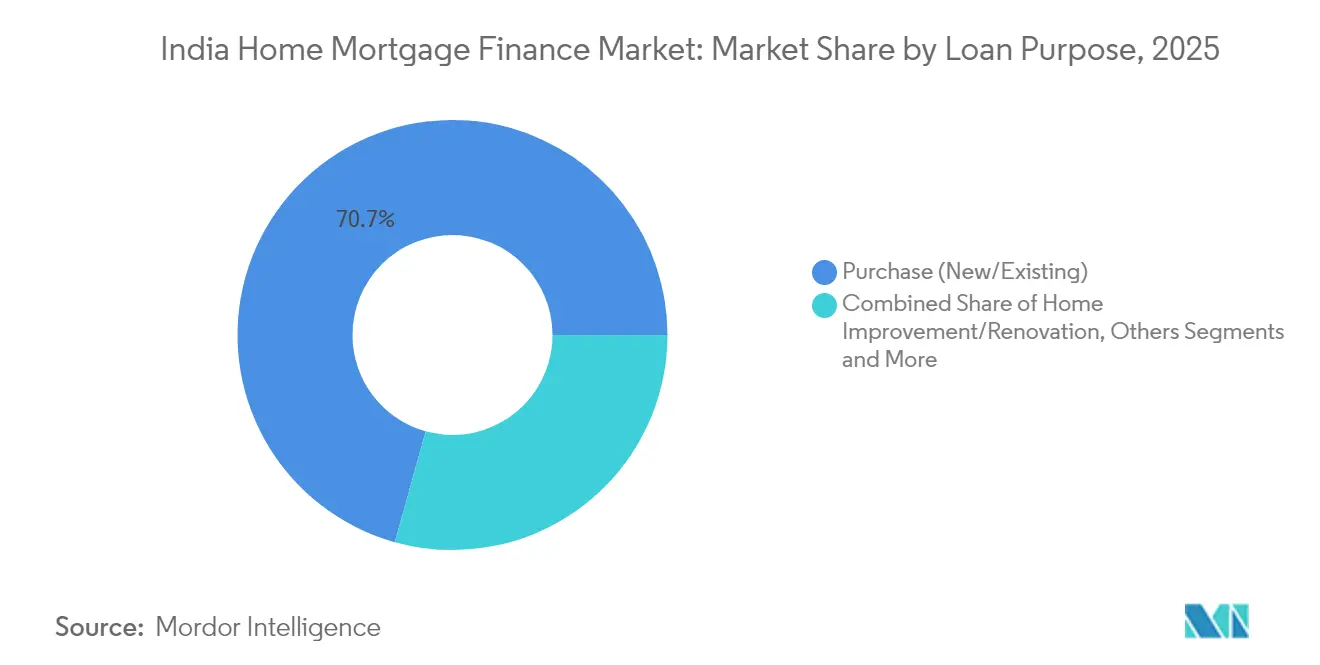

- By loan purpose, purchase loans controlled 70.68% of the Indian home mortgage finance market in 2025; loan against property is projected to grow at 15.02% CAGR through 2031.

- By provider, banks held 62.10% of the Indian home mortgage finance market share in 2025, whereas HFCs are expanding at 13.52% CAGR.

- By interest rate type, floating-rate loans represented 83.40% of the Indian home mortgage finance market size in 2025 and are advancing at 14.31% CAGR to 2031.

- By tenure, the 11–20 year bracket captured 56.05% of the Indian home mortgage finance market in 2025; loans above 20 years are rising at 13.22% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Home Mortgage Finance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Affordable-housing push (PMAY-Urban & Rural) | +2.8% | National; tier-2/3 focus | Long term (≥ 4 years) |

| Formal-sector wage growth in tier-2/3 cities | +2.1% | Tier-2/3 nationwide | Medium term (2-4 years) |

| Mutual-fund & insurer demand for RMBS | +1.4% | National | Medium term (2-4 years) |

| Open-banking APIs for digital KYC | +1.8% | Urban → rural | Short term (≤ 2 years) |

| EWS/LIG mortgage-guarantee schemes | +1.6% | National | Medium term (2-4 years) |

| AI-credit scoring for thin-file borrowers | +1.9% | Rural & semi-urban | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding Affordable-Housing Push (PMAY-Urban & Rural)

PMAY-Urban 2.0 earmarks USD 536 billion through 2029, embedding trunk infrastructure, transport links, and social amenities that lift end-user demand. The scheme’s Credit Risk Guarantee Fund lets lenders extend sub-8% rates to EWS and LIG borrowers by lowering capital charges and risk weights. Lenders equipped with rural sourcing networks benefit as the programme mandates 2 crore rural units, pressuring traditional banks to expand into smaller centers. HFCs such as Aadhar Housing Finance and Aavas Financiers gain competitive headroom because they already serve low-ticket borrowers with lean, tech-first operations. These reinforcing dynamics enlarge the India home mortgage finance market and foster sustainable portfolio diversity.

Rapid Formal-Sector Wage Growth in Tier-2/3 Cities

Economic decentralization has moved 60% of GDP creation to smaller cities, where property remains more affordable relative to incomes. Industrial corridors under Gati Shakti cut transit times and raise land values, allowing lenders to underwrite on stronger collateral bases. Corporate relocations widen the salaried borrower pool, encouraging customized EMI-holiday and step-up repayment products that suit evolving income profiles. Manufacturing jobs created by Production-Linked Incentive schemes stabilize borrower cash flows, which improves risk metrics for lenders active in emerging clusters. Together, these shifts drive geographic rebalancing within the India home mortgage finance market and temper concentration risk.

Growing Securitization Appetite of Mutual Funds & Insurers

India’s inaugural RMBS placement in May 2025 marked a watershed, delivering a 50–75 bp funding cost advantage for originators and broadening investment options for asset managers overseeing USD 500 billion[2]Reuters Staff, “India’s First RMBS Debuts,” reuters.com. Revised RBI guidelines now mandate granular pool-level disclosure, boosting transparency and institutional confidence. Secondary-market liquidity is rising, enabling smaller HFCs to recycle capital faster and scale loan books beyond balance-sheet limits. Competitive pricing pressure forces banks to revamp rate strategies, sharpening consumer options across the credit spectrum. This securitization flywheel expands the India home mortgage finance market by unlocking fresh capital flows.

Open-Banking APIs Accelerating Digital KYC & Disbursal

The Reserve Bank’s Unified Lending Interface merges Aadhaar, UPI, and banking data, slashing average approval times from 21 days to 3 days for early adopters[3]Reserve Bank of India, “Master Direction on Digital Lending,” rbi.org.in. Lenders cite 40% cuts in acquisition costs and 60% faster sanction volumes, translating into keener pricing and broader reach. Standardized APIs encourage fintech-bank partnerships, allowing origination scale without heavy branch investments. Rural borrowers benefit from vernacular-language onboarding and reduced documentation friction, shifting previously informal credit demand into formal channels. These improvements broaden the addressable borrower base and intensify competition inside the India home mortgage finance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NPA overhang in PSU-bank mortgage books | -1.8% | National; rural-skewed | Medium term (2-4 years) |

| Substitution by BNPL & unsecured personal credit | -1.2% | Urban → tier-2 | Short term (≤ 2 years) |

| Climate-risk premiums in coastal districts | -0.9% | Coastal & flood zones | Long term (≥ 4 years) |

| Land-title fragmentation slows enforcement | -1.4% | National; peri-urban | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent NPA Overhang in PSU-Bank Mortgage Books

Public-sector banks report mortgage NPA ratios between 1.02% and 5.73%, far higher than private peers’ 0.20–0.64% bands, reflecting legacy risk-management gaps. Bureaucratic foreclosure procedures extend recovery cycles, compelling higher provisioning that constrains fresh affordable-housing lending. Risk-averse underwriting sidelines borderline borrowers who might otherwise qualify, siphoning market share toward agile HFCs. While capital infusions help shore up buffers, operating discipline still lags, limiting price competitiveness in the India home mortgage finance market. Until balance-sheet clean-ups accelerate, PSU banks will trail volume growth leaders.

Crowding-Out from Alternative Retail Credit (BNPL & Unsecured Personal)

Buy-now-pay-later and unsecured personal loans offer instant credit, fostering consumption-first behavior among millennials who delay home-purchase decisions. These products already account for 52% of fresh retail NPAs, threatening spill-over stress into secured portfolios if borrower leverage peaks. BNPL platforms build customer stickiness that competes with mortgage down-payment savings, reducing conversion pools. RBI’s higher risk weights on unsecured books can temper supply but may also raise cross-product pricing, nudging borrowers toward informal channels. This substitution effect marginally curtails growth avenues within the India home mortgage finance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Loan Purpose: Purchase Dominance Amid LAP Acceleration

Purchase mortgages retained a 70.68% share of the India home mortgage finance market in 2025, cementing home-ownership aspirations in a culture that views residential property as the premier wealth-building asset. Government subsidies, 90% loan-to-value (LTV) caps for sub-INR 30 lakh tickets, and improved job prospects fuel this preference. Developers in tier-2 hubs align new launches with 2- and 3-BHK formats, ensuring product-market fit for salaried buyers. Falling mortgage rates spur refinance demand, enlarging the pool of rate-switch transactions that pad fee income for lenders.

Loan against property (LAP) enjoys 15.02% CAGR, buoyed by MSME owners converting idle residential equity into working capital amid limited unsecured business‐credit channels. Digitized valuation platforms and desktop appraisals shrink turnaround to under 72 hours, differentiating LAP from traditional bank overdrafts. Home-improvement loans gain traction as rising disposable incomes encourage aesthetic upgrades, especially in growing tier-2 markets where property price appreciation unlocks usable equity. Construction loans scale cautiously under RERA-linked stage-disbursement models that improve consumer protection but elongate revenue recognition for developers. The “Others” bucket—refinance and top-up loans—expands as rate differentials encourage port-over activity, further enlarging the India home mortgage finance market size.

By Provider: Banks Leverage Cost Advantages Despite HFC Innovation

Banks commanded a 62.10% share of the India home mortgage finance market in 2025, exploiting low-cost CASA deposits, wide branch grids, and cross-sell capabilities. Integrated salary-account bundling lowers acquisition expenses, while treasury operations hedge interest risk through dynamic asset-liability management. Yet, balance-sheet optimization is evident: HDFC Bank sold USD 717 million mortgages to free capital for higher-yield assets.

Housing finance companies clock 13.52% growth by targeting underserved borrowers with lean cost structures and swift sanction cycles. Their gross-NPA ratios below 1.5% underscore disciplined underwriting, even as they penetrate deeper into semi-urban geographies. Co-lending models pair bank liquidity with HFC origination prowess, blending cost and reach advantages. Fintech-enabled HFCs mine alternate data—utility payments, GST returns—to widen credit funnels, challenge incumbents, and diversify the India home mortgage finance market share distribution.

By Interest Rates: Floating Rate Preference Amid Declining Cycle

Floating-rate loans dominate with 83.40% share of the India home mortgage finance market in 2025, as borrowers expect accommodative policy continuity; June 2025’s 50 bp repo cut to 5.5% immediately fed through 10–15 bp MCLR reductions. Lenders now price floating mortgages with fortnightly repo resets, offering transparency to rate-sensitive customers.

Fixed-rate products attract risk-averse profiles anticipating bottom-of-the-cycle lows, but penalty-free prepayments on floating loans tilt value perception. Hybrid structures—two-year fixed transitioning to floating—address rate-cycle uncertainties for sophisticated borrowers who benchmark against inflation expectations. Competition prompts granular pricing bands linked to credit scores, enhancing customer choice and sustaining breadth in the India home mortgage finance market.

By Loan Tenure: Extended Terms Reflect Affordability Pressures

The 11–20 year bracket captured 56.05% share of the India home mortgage finance market in 2025, balancing EMI affordability with manageable total interest outgo. This tenure benefits from historically lower delinquencies, prompting lenders to price it most aggressively.

Loans beyond 20 years grow 13.22% as rising metropolitan real-estate costs stretch debt-service ratios; extended amortization keeps EMIs within 35% of monthly income caps. Banks experiment with step-up EMIs synced to anticipated salary growth for IT and manufacturing professionals. Sub-10-year contracts remain niche, appealing to high-income borrowers prioritizing rapid equity build-up and tax-dedication optimization. These diverse tenure structures enrich the Indian home mortgage finance market and enhance portfolio risk dispersion.

Geography Analysis

Southern and western states dominate credit penetration: Maharashtra and Telangana record housing-loan-to-GSDP ratios of 18.49% and 18.44% respectively, driven by IT clusters, established banking infrastructure, and higher formal-sector employment. Robust demographic inflows of young professionals secure demand pipelines, while state-level stamp-duty rebates spur first-time purchases.

Northern India’s National Capital Region benefits from proximity to federal administration and consistent infrastructure capex; satellite towns such as Noida Extension and Sohna Road draw developers focused on mid-income buyers. PMAY-Urban 2.0 allocations prioritize Delhi’s peri-urban belts, ensuring supply alignment with subsidy-eligible borrowers. Industrial corridors connecting Lucknow and Kanpur stimulate salaried employment, fueling mortgage uptake.

Eastern corridors still trail national averages in mortgage penetration due to lower per-capita incomes, but connectivity upgrades under the Gati Shakti program reduce logistics costs and entice manufacturing investments. Gradual formalization of wages promises future demand uplift. Tier-2 and tier-3 cities across all regions account for 44% of developer land acquisitions, supported by 20% year-on-year housing-sales growth and property price jumps of up to 65% in 2024. Rural potential expands as the Registration Bill 2025 digitizes land records, reducing title risk and paving the way for collateral-secure lending. These evolving patterns ensure the India home mortgage finance market remains geographically diversified.

Competitive Landscape

The India home mortgage finance market is moderately fragmented, with the top lenders controlling most of the annual disbursals and a long tail of agile specialists vying for share. Banks leverage low-cost funding, but their processing times and legacy IT stacks create service gaps that HFCs exploit through rapid digital onboarding. Bajaj Housing Finance’s USD 16 billion valuation illustrates investor confidence in mono-line mortgage platforms that prioritize speed and customer experience.

Technology adoption is the decisive differentiator. Early users of the Unified Lending Interface report cost-to-income ratio reductions of 200 basis points and sanction-cycle compression to 72 hours, positioning them for aggressive growth. AI-driven scoring engines help lenders penetrate thin-file segments without compromising portfolio quality. Fintech-bank co-lending partnerships pool strengths: low-cost liquidity meets granular origination, broadening risk distribution, and lowering customer rates.

Strategic M&A adds momentum. February 2025 saw Aquilo House Pte. Ltd.’s 52.68% stake acquisition in Aavas Financiers, injecting foreign capital and best-practice governance into the affordable-housing niche. HUDCO’s INR 1 trillion memorandum with Rajasthan expands public-sector reach into urban infrastructure, potentially feeding mortgage demand. HDFC Bank’s periodic loan securitization exemplifies balance-sheet optimization in response to tighter capital norms. Collectively, these moves reinforce a competitive yet opportunity-rich environment where nimble players can scale quickly, keeping the India home mortgage finance market vibrant.

India Home Mortgage Finance Industry Leaders

HDFC Bank

State Bank of India

LIC Housing Finance

ICICI Bank

PNB Housing Finance

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: India listed its first RMBS, creating new investment channels and lowering originator funding costs.

- April 2025: RBI raised priority-sector housing loan limits to INR 50 lakh for large cities and INR 35 lakh for smaller centres, broadening eligibility.

- February 2025: Union Budget hiked PMAY-Urban 2.0 allocation 133% to INR 3,500 crore, reinforcing subsidy pipelines.

- February 2025: Aquilo House gained approval to acquire 52.68% of Aavas Financiers, signalling foreign confidence in affordable-housing finance.

India Home Mortgage Finance Market Report Scope

Home mortgage finance secures a loan for purchasing a house by using an asset as collateral. Mortgages can be utilized to buy a new home or to borrow against the equity of an existing one. Banks, mortgage companies, and financial institutions provide these loans, catering to primary residences, secondary homes, or investment properties. The Indian home mortgage finance market is segmented by source, interest rate, tenure, and type. By source, the market is segmented into bank and housing finance companies. By interest rate, the market is segmented into fixed rate and floating rate. By tenure, the market is segmented into up to 5 years, 6 - 10 years, 11 - 24 years, and 25 - 30 years. By type, the market is segmented into home purchase, land/ plot purchase, home construction, home improvement, and home extension. The report offers market size and forecasts for India's Home Mortgage Finance Market in value (USD) for all the above segments.

By Loan Purpose

| Purchase (New/Existing) |

| Home Improvement/Renovation |

| Loan Against Property |

| Others (Construction, Refinance, etc.) |

By Provider

| Banks |

| Housing Finance Companies |

| Others |

By Interest Rates

| Fixed Interest Rates |

| Floating Interest Rates |

By Loan Tenure

| ≤ 10 Years |

| 11 – 20 Years |

| More than 20 Years |

| By Loan Purpose | Purchase (New/Existing) |

| Home Improvement/Renovation | |

| Loan Against Property | |

| Others (Construction, Refinance, etc.) | |

| By Provider | Banks |

| Housing Finance Companies | |

| Others | |

| By Interest Rates | Fixed Interest Rates |

| Floating Interest Rates | |

| By Loan Tenure | ≤ 10 Years |

| 11 – 20 Years | |

| More than 20 Years |

Key Questions Answered in the Report

What is the current size of the India home mortgage finance market?

The India home mortgage finance market is valued at USD 0.54 trillion in 2026 and is projected to rise to USD 0.97 trillion by 2031.

Which loan purpose category dominates the market?

Purchase mortgages dominate, holding a 70.68% share of the India home mortgage finance market in 2025.

How fast is the loan against property segment expanding?

Loan against property is the fastest-growing segment, advancing at a 15.02% CAGR through 2031.

Why are floating-rate mortgages preferred by most borrowers?

Borrowers favor floating rates because the 5.5% repo rate and recent policy cuts pass through quickly, lowering EMIs when rates decline.

Which geographies are leading growth?

Tier-2 and tier-3 cities lead current expansion, accounting for 44% of new land deals and up to 65% annual price appreciation.

Is the market fragmented or consolidated?

With the top five lenders controlling a significant share of the market, the India home mortgage finance market is considered moderately fragmented, allowing new entrants to scale rapidly through technology and niche focus.

Page last updated on: