India Geospatial Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

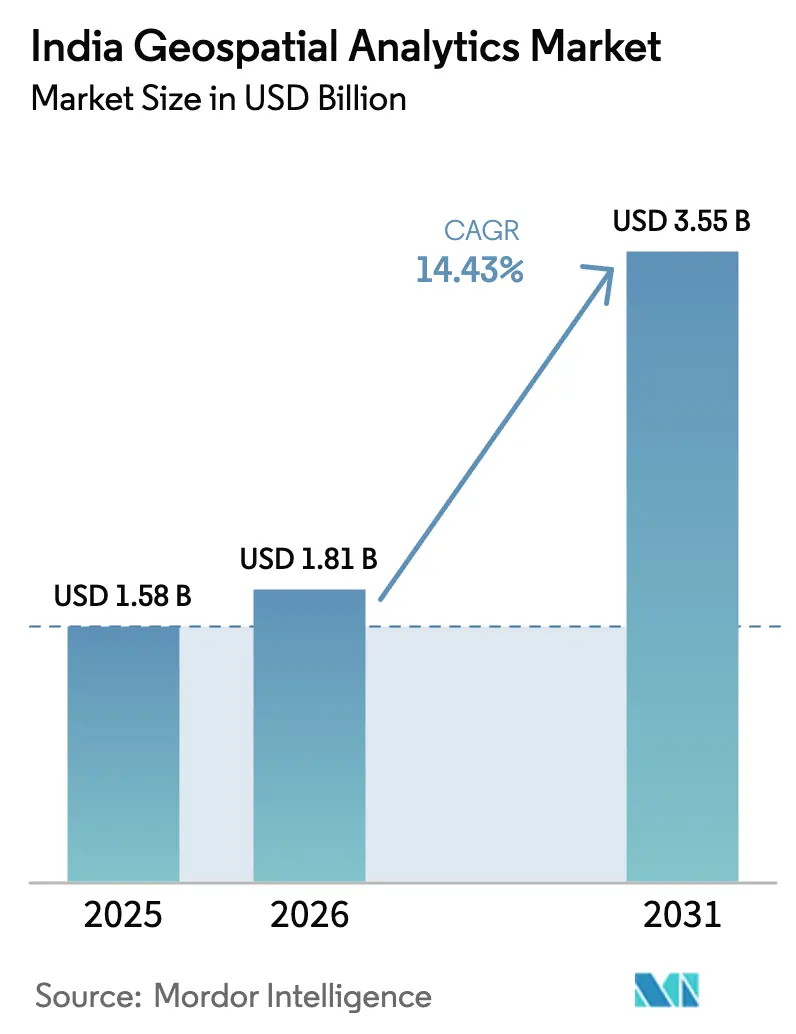

| Base Year Market Size (2025) | USD 1.58 Billion |

| Market Size (2026) | USD 1.81 Billion |

| Market Size (2031) | USD 3.55 Billion |

| Growth Rate (2026 - 2031) | 14.43% CAGR |

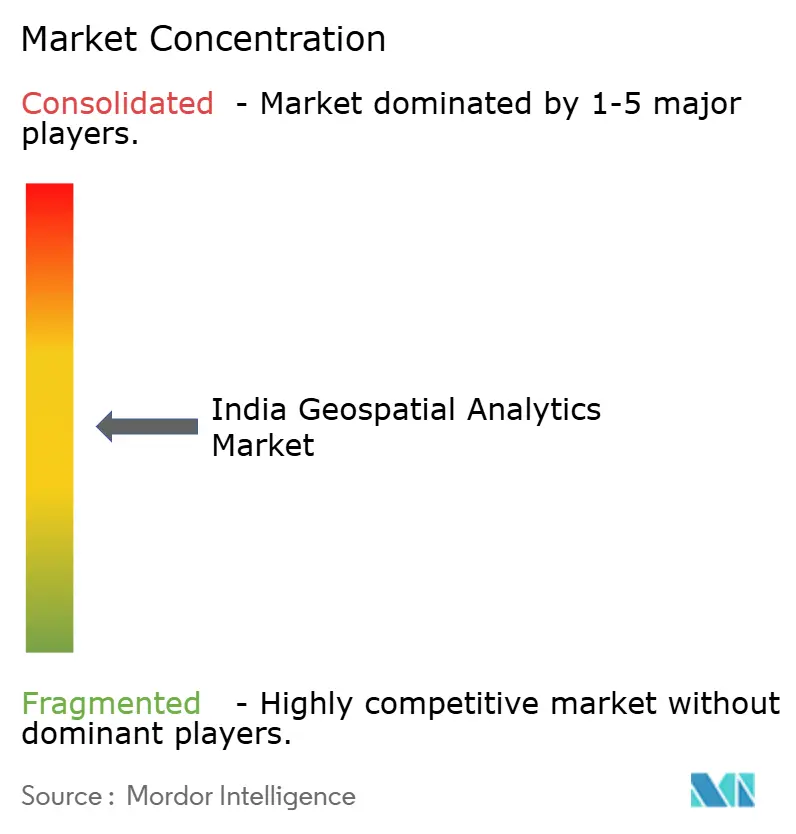

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Geospatial Analytics Market Analysis by Mordor Intelligence

The India Geospatial Analytics market size was valued at USD 1.58 billion in 2025 and estimated to grow from USD 1.81 billion in 2026 to reach USD 3.55 billion by 2031, at a CAGR of 14.43% during the forecast period (2026-2031). Increasing adoption of spatial technologies in 5G roll-outs, precision agriculture, and disaster management anchors demand, while the National Geospatial Policy 2022 strips away legacy approval barriers, fostering faster data access and domestic innovation. Public-sector projects such as PM Gati Shakti, SVAMITVA, and smart-city CAPEX expand the user base, and cloud-hosted analytics platforms lower the total cost of ownership for small and mid-sized enterprises. Competitive intensity heightens as local vendors leverage policy tailwinds to challenge global incumbents; partnerships with ISRO, cloud providers, and state GIS agencies underpin many go-to-market strategies. Services revenue rises sharply because agencies and enterprises require end-to-end implementation support, data fusion, and AI-enabled risk models built on domestic data stacks.

Key Report Takeaways

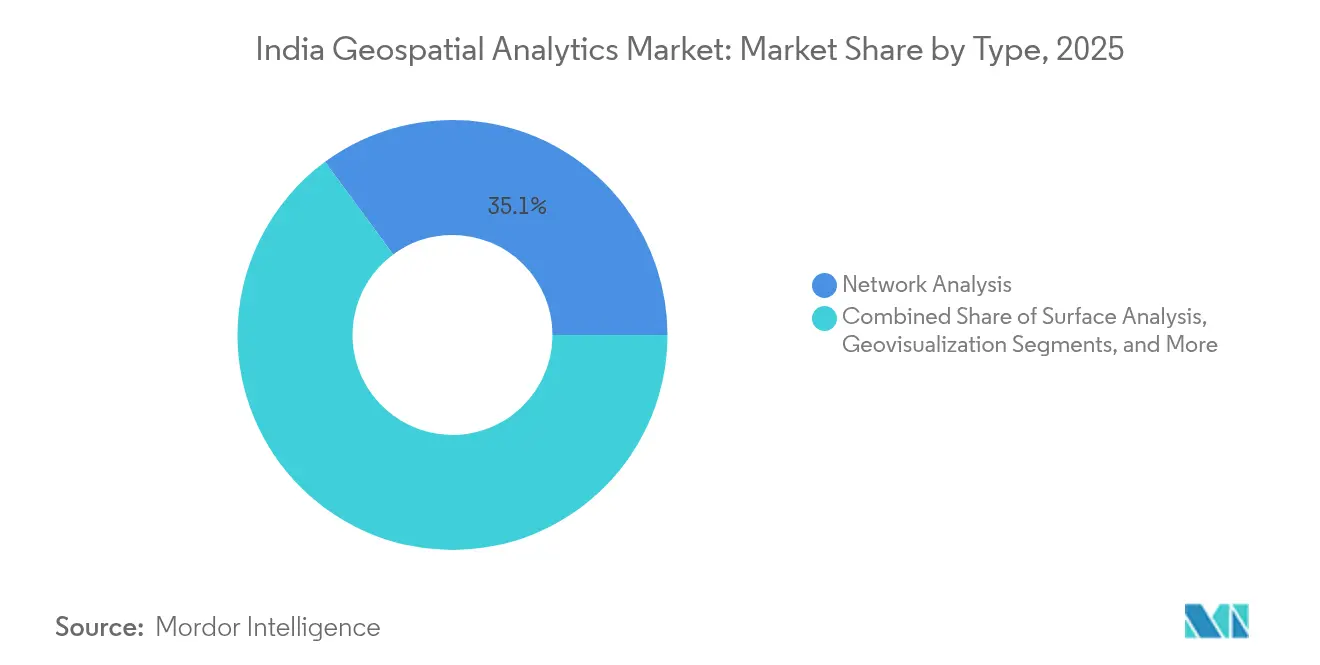

- By type, Network Analysis led with 35.10% of the India Geospatial Analytics market share in 2025, while Geovisualization is advancing at a 15.02% CAGR through 2031.

- By component, software platforms accounted for 60.78% of the India Geospatial Analytics market size in 2025; services are projected to expand at a 15.55% CAGR to 2031.

- By deployment, on-premises solutions held 53.85% share of the India Geospatial Analytics market size in 2025, whereas cloud deployments register the highest CAGR at 15.31% through 2031.

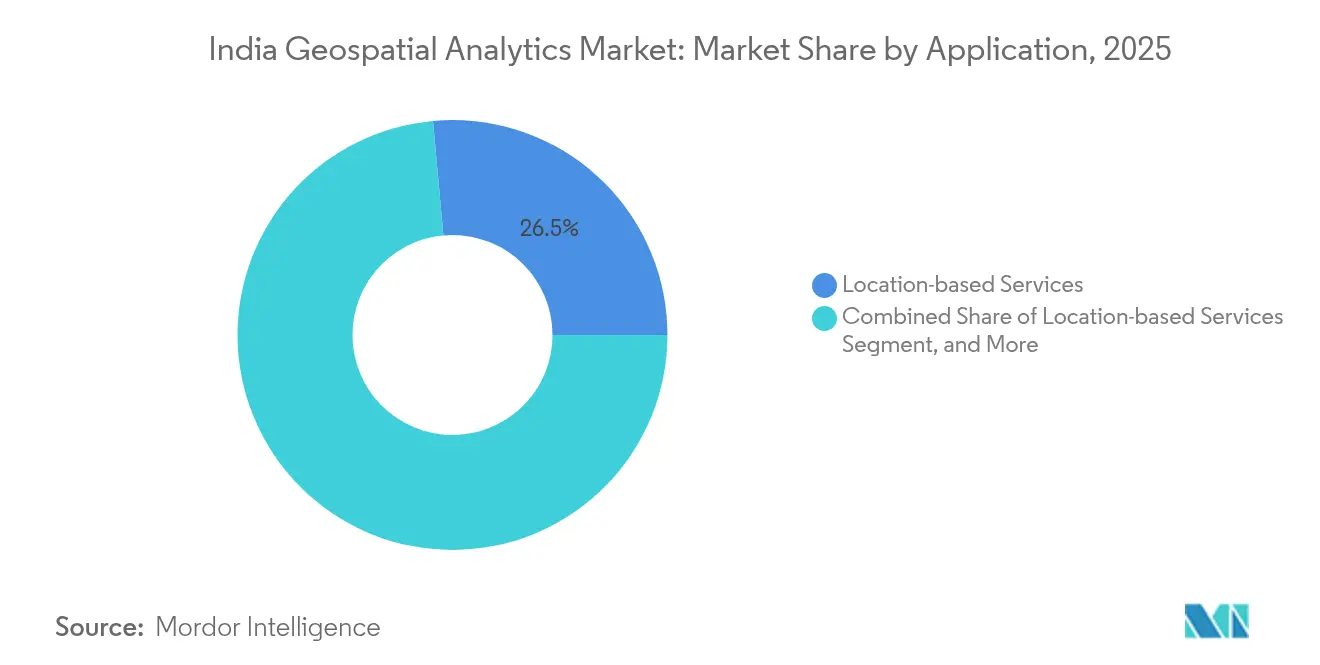

- By application, location-based services captured a 26.45% share of the India Geospatial Analytics market in 2025, and climate and environmental monitoring is climbing at a 14.96% CAGR to 2031.

- By end-user, agriculture accounted for a 29.10% share of the India Geospatial Analytics market size in 2025, whereas insurance and risk management is rising at a 15.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of India. The geospatial analytics market share in our global report expresses these relative weights.

India Geospatial Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Liberalized National Geospatial Policy 2022 | +2.8% | National, with early gains in Karnataka, Maharashtra, Gujarat | Medium term (2-4 years) |

| Rapid 5G and FTTH Roll-outs demanding GIS-based network design | +2.1% | Urban centers, expanding to Tier-2 cities | Short term (≤ 2 years) |

| Precision-agri adoption fuelled by satellite and drone imagery | +1.9% | Agricultural states: Punjab, Haryana, Uttar Pradesh, Karnataka | Medium term (2-4 years) |

| Smart-city CAPEX under Gati Shakti and AMRUT 2.0 | +1.7% | 100 Smart Cities, National Capital Region, major metros | Long term (≥ 4 years) |

| Demand for hyper-local location-intelligence in quick-commerce | +1.4% | Metropolitan areas, Tier-1 cities | Short term (≤ 2 years) |

| AI-driven risk-scoring for climate-linked insurance | +1.2% | Coastal states, flood-prone regions, agricultural zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Liberalized National Geospatial Policy 2022

The 2022 policy dismantled security-clearance bottlenecks and introduced self-certification, allowing Indian firms to create high-resolution maps once confined to government agencies.[1]Department of Science & Technology, “National Geospatial Policy meets Government commitment to inclusion & progress through access to locational data & related services,” dst.gov.in A nationwide CORS network now delivers centimeter-level accuracy to surveyors and the SVAMITVA program has digitized more than 2.8 lakh villages, producing granular land-records data that fuels diverse analytics use cases. Open-standards mandates invite private capital, pushing the India Geospatial Analytics market toward INR 52,000 crore valuation by 2025. Domestic providers gain a regulatory moat because foreign entities cannot conduct ground surveys without Indian partners, ensuring data sovereignty and boosting local employment.

Rapid 5G and FTTH Roll-outs demanding GIS-based network design

Telecom operators have installed 4.69 lakh 5G base transceiver stations covering 99.6% of districts, driving an urgent need for spatial planning tools that maximize coverage and minimize capital outlay.[2]Ministry of Communications, “Expansion of 5G network in the country,” pib.gov.in The GatiShakti Sanchar portal centralizes Right-of-Way approvals, cutting fiber deployment timelines and reducing duplication of civil works. Reliance Jio’s USD 75.44 million expansion across 17 cities underscores the financial scale of geospatial demand INVESTINDIAGRID. Future 6G research, 111 projects funded under Bharat 6G Vision, will require even denser cell geographies, amplifying demand for real-time location intelligence.

Precision-agri adoption fuelled by satellite and drone imagery

Agriculture supports 600 million livelihoods, and climate volatility intensifies the need for precision inputs. Kisan drones, satellite crop monitoring and AI-powered advisory services lift farmer incomes by up to 35% in pilot projects. Start-ups such as Cropin and SatSure integrate earth-observation data with credit scoring, while RMSI’s Cropalytics offers real-time crop maps to insurers. Vassar Labs’ fieldWISE platform marries IoT sensors with satellite feeds to advise on irrigation scheduling and pest alerts.

Smart-city CAPEX under Gati Shakti and AMRUT 2.0

PM Gati Shakti aggregates 1,600+ data layers from 44 central ministries and 36 states into a common geospatial portal, standardizing route alignment, land acquisition, and utility mapping at PIB.GOV.IN. Early evidence shows road and rail projects progress 25-30% faster when planned through the platform. Karnataka’s K-GIS mapped over 400,000 assets to improve municipal service delivery. As AMRUT 2.0 injects new CAPEX into water, sewerage, and public transit projects, geospatial workflows become standard practice for tendering and monitoring.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent shortage of certified GIS talent | -1.8% | National, acute in Tier-2 and Tier-3 cities | Long term (≥ 4 years) |

| Fragmented state-level procurement processes | -1.2% | State governments, varying by administrative efficiency | Medium term (2-4 years) |

| Legacy cadastral data accuracy issues | -0.9% | Rural areas, states with outdated land records | Long term (≥ 4 years) |

| High EO-satellite data costs for SMEs | -0.7% | Small enterprises, agricultural cooperatives | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent shortage of certified GIS talent

India needs 1.25 million AI professionals by 2027, yet geospatial modules remain peripheral in most engineering curricula. Water-resources agencies alone require 35,000 trained staff for GIS applications. Scarcity is acute outside major metros, limiting the diffusion of the India Geospatial Analytics market into rural development programs.

Fragmented state-level procurement processes

Karnataka and Odisha showcase mature GIS tenders, yet most states operate siloed procurement rules that inflate vendor compliance effort and time-to-award. Absence of common technical standards forces suppliers to customize proposals, raising total project costs and deterring startups from bidding. The National Informatics Centre’s State GIS Portal is a step toward harmonization but adoption remains uneven.[3]National Informatics Centre, “State GIS Portal,” nic.in

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Network Analysis Dominates Infrastructure Modernization

Network Analysis contributed 35.10% to the India Geospatial Analytics market in 2025. Telecom providers depend on RF propagation models and terrain analytics to design macro-cell and small-cell layers required for nationwide 5G. Utilities deploy similar toolsets to optimize fiber and power-grid routes, and transport planners rely on connectivity analytics to decongest corridors. The India Geospatial Analytics market size for Geovisualization is projected to expand at 15.02% CAGR, signaling a shift toward dashboard-based decision tools that simplify complex spatial datasets. Driven by citizen-centric governance, agencies demand interactive 3D city models and real-time mobility twins for scenario testing. Retailers and logistics firms embed map-centric BI layers to route fleets and place dark stores, indicating broad private-sector uptake.

Growing data complexity elevates Data Integration and Transformation, which fuses satellite imagery, cadastral maps and IoT feeds into unified schemas. The PM Gati Shakti platform exemplifies multi-layer fusion, integrating 1,600 datasets for infrastructure alignment. ISRO’s roadmap of 50 AI-enabled satellites will multiply data volumes, reinforcing demand for automated pipelines that clean, label and stream imagery to analytics engines.

By Component: Services Surge as Implementation Complexity Grows

Software held 60.78% India Geospatial Analytics market share in 2025 as public and private bodies licensed GIS suites, imagery servers and spatial SQL databases. Yet the services revenue pool grows at 15.55% CAGR because successful roll-outs require data migration, model customization and cloud orchestration. Esri India’s managed services on the Government e-Marketplace illustrate the shift toward outcome-based engagements that bundle software, hosting and SLAs. Insurance carriers outsource crop-yield validation algorithms that merge Sentinel imagery with actuarial tables, demanding cross-domain expertise that few in-house teams possess. For smaller municipalities, managed services circumvent hardware purchases, letting agencies access pay-per-use analytics on national sovereign clouds.

By Deployment Mode: Cloud Adoption Accelerates Despite On-Premises Legacy

On-premise still accounts for 53.85% of the India Geospatial Analytics market size in 2025, reflecting security mandates and sunk cost in government data centers. Nevertheless, cloud deployments post a 15.31% CAGR as organizations recognize elastic compute advantages for pixel-heavy workloads. The National Geospatial Policy’s self-certification model eases controlled data sharing in virtual private clouds. Hybrid architectures dominate in banking and insurance, where sensitive customer data remains on-premise while high-performance GPU clouds run AI classifiers. The sovereign GPU cloud initiative provides domestic compute at par with global hyperscalers, further reducing migration risk.

By Application: Location-Based Services Lead While Climate Monitoring Surges

Location-based services commanded 26.45% share in 2025 as ride-hailing, food delivery and mobility apps demanded accurate geocoding and routing APIs. Quick-commerce players use postal-code heat maps and last-meter network graphs to shrink delivery cycles to under 10 minutes. In parallel, climate and environmental monitoring outpaces overall growth at a 14.96% CAGR; high-resolution landslide atlases, flood-risk layers and air-quality indices feed emergency-response dashboards. The India Geospatial Analytics market size tied to disaster analytics is expanding as insurers adopt satellite-verified indices for parametric payouts and state relief funds trigger faster from objective loss maps.

By End-user Vertical: Agriculture Dominates While Insurance Accelerates

Agriculture’s 29.10% revenue share reflects sustained government subsidies for drone spraying, soil mapping, and yield forecasting tools. State procurement of crop-health analytics platforms under the Pradhan Mantri Fasal Bima Yojana further solidifies demand. Insurance and risk management grows at 15.06% CAGR as carriers deploy satellite big-data pipelines to settle crop and property claims within hours, reducing fraud and administrative overhead. Utilities, communication, and public-safety agencies follow closely, relying on geospatial twins for outage mapping, route optimization, and disaster readiness.

Geography Analysis

The India Geospatial Analytics market registers differentiated uptake across regions due to fiscal capacity, institutional readiness and hazard exposure. Karnataka spearheads adoption through the INR 100 crore K-GIS program, mapping 120+ thematic layers across 4 lakh assets for integrated governance. Bengaluru’s technology cluster supplies talent and venture funding, fostering a dense ecosystem of GIS start-ups. Maharashtra and Gujarat draw investment from industrial corridors and port logistics that require spatial asset management and multi-modal planning.

Northern grain-belt states, Punjab, Haryana, and Uttar Pradesh, prioritize precision agriculture. Satellite-driven irrigation scheduling, soil salinity detection and insurance indexing strengthen farmer resilience against erratic monsoons. Uttar Pradesh’s participation in SVAMITVA showcases growing state interest in land-record digitization despite administrative complexity.

Coastal states Tamil Nadu, Andhra Pradesh, and Kerala intensify disaster preparedness due to cyclone and flood exposure. ISRO’s rapid damage assessment after the Dharali flash flood demonstrated how timely ortho-rectified imagery informs search-and-rescue and relief logistics. Odisha’s GOPLUS portal integrates geospatial layers with industrial land banks, accelerating investment approvals and infrastructure readiness.

The National Capital Region benefits from proximity to federal ministries piloting smart-city dashboards and live traffic twins under PM Gati Shakti. The dense urban fabric drives demand for indoor mapping, drone-based asset inspection and AI-enabled congestion analytics, further expanding the India Geospatial Analytics market.

Mordor Intelligence examines the geospatial analytics market across diverse other regional markets as well, including Africa and Middle East, while also offering granular country-level perspectives for Japan, South Korea, Nigeria, Saudi Arabia, Israel, Russia, and Germany and more.

Competitive Landscape

The market remains moderately fragmented; the top five vendors account for roughly 32% revenue, leaving room for vertical specialists and regional system integrators. MapmyIndia leverages ISRO data to launch Mappls RealView, offering street-level imagery across 400,000 km to compete with foreign street imagery. RMSI develops high-resolution coastal-flood models predicting city submersion scenarios by 2050, serving banks and municipalities. Global incumbent Esri doubles down on managed services and lower-price bundles tailored to Indian state budgets.

Strategic alliances increase: domestic analytics firms pair with telcos for 5G rollout planning, satellite operators partner with agri-fintechs for crop-index insurance, and cloud providers host sovereign GPU clusters to meet localization norms. M&A activity accelerates as larger IT-services companies acquire niche drone-mapping startups to add field-data acquisition capabilities. Product roadmaps converge on AI-powered feature extraction, real-time video analytics, and API-first architectures that integrate seamlessly with ERP and CRM systems.

India Geospatial Analytics Industry Leaders

Google LLC

Esri India Technologies Private Limited

Precisely Holdings LLC

SAAR IT Resources Private Limited

General Electric Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: NRSC welcomed 460 delegates at the National User Interaction Meet 2025, highlighting Earth-observation pipeline upgrades for Indian Space Policy implementation.

- February 2025: Union Budget allocated INR 100 crore for the National Geospatial Mission and INR 13,416.2 crore to the Department of Space, reinforcing satellite-based data generation.

- February 2025: NAKSHA project launched with INR 194 crore to digitize urban land records across 152 ULBs, using aerial surveys by the Survey of India.

- January 2025: Ministry of Communications rolled out the Sanchar Saathi Mobile App and National Broadband Mission 2.0, targeting optical fiber in 270,000 villages by 2030.

India Geospatial Analytics Market Report Scope

Geospatial analytics is the process of acquiring, manipulating, and displaying imagery and data from the geographic information system (GIS), such as satellite photos and GPS data. The specific identifiers of a street address and a zip code are used in geospatial data analytics. They are used to create geographic models and data visualizations for more accurate trend modeling and forecasting.

The India geospatial analytics market is segmented by type (surface analysis, network analysis, geovisualization), end user vertical (agriculture, utility and communication, defence and intelligence, government, mining and natural resources, automotive and transportation, healthcare, real estate, and construction).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Surface Analysis |

| Network Analysis |

| Geovisualization |

| Geocoding and Reverse Geocoding |

| Data Integration and Transformation |

| Other Types |

| Software |

| Services |

| On-premises |

| Cloud-based |

| Hybrid |

| Location-based Services |

| Disaster Management and Emergency Response |

| Climate and Environmental Monitoring |

| Urban Planning and Smart Cities |

| Supply-Chain and Logistics Optimisation |

| Asset Tracking and Management |

| Insurance and Risk Management |

| Other Applications |

| Agriculture |

| Utilities and Communication |

| Defense and Intelligence |

| Government and Public Safety |

| Mining and Natural Resources |

| Automotive and Transportation |

| Healthcare and Life Sciences |

| Real Estate and Construction |

| Retail and E-commerce |

| Banking, Financial Services and Insurance |

| Other Verticals |

| By Type | Surface Analysis |

| Network Analysis | |

| Geovisualization | |

| Geocoding and Reverse Geocoding | |

| Data Integration and Transformation | |

| Other Types | |

| By Component | Software |

| Services | |

| By Deployment Mode | On-premises |

| Cloud-based | |

| Hybrid | |

| By Application | Location-based Services |

| Disaster Management and Emergency Response | |

| Climate and Environmental Monitoring | |

| Urban Planning and Smart Cities | |

| Supply-Chain and Logistics Optimisation | |

| Asset Tracking and Management | |

| Insurance and Risk Management | |

| Other Applications | |

| By End-user Vertical | Agriculture |

| Utilities and Communication | |

| Defense and Intelligence | |

| Government and Public Safety | |

| Mining and Natural Resources | |

| Automotive and Transportation | |

| Healthcare and Life Sciences | |

| Real Estate and Construction | |

| Retail and E-commerce | |

| Banking, Financial Services and Insurance | |

| Other Verticals |

Key Questions Answered in the Report

What is the current value of the India Geospatial Analytics market?

The market is worth USD 1.81 billion in 2026.

How fast will the sector grow through 2031?

It is forecast to expand at a 14.43% CAGR, reaching USD 3.55 billion by 2031.

Which segment holds the largest share by type?

Network Analysis leads with 35.10% share in 2025.

Why is cloud deployment gaining momentum?

Elastic compute, lower upfront costs and the National Geospatial Policy’s data-sharing provisions are driving a 15.31% CAGR for cloud deployments.

Which end-user vertical is growing fastest?

Insurance and risk management is advancing at a 15.06% CAGR as carriers adopt satellite-driven claim assessment.

Page last updated on: