India Big Data Technology And Service Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

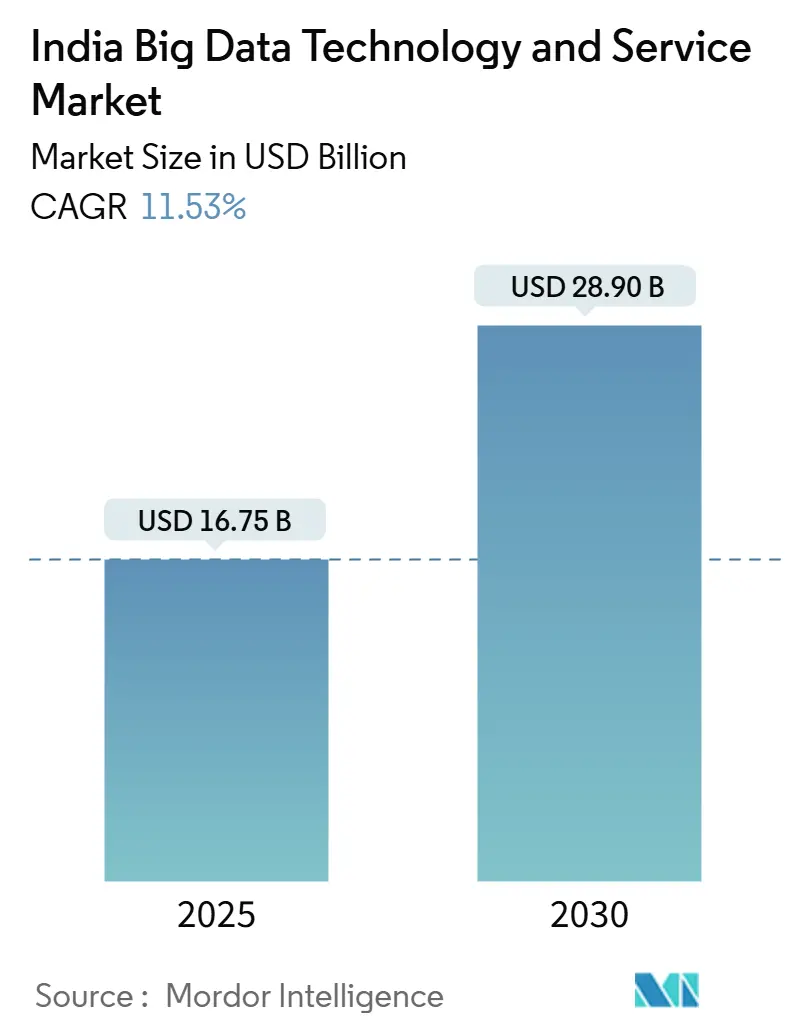

| Market Size (2025) | USD 16.75 Billion |

| Market Size (2030) | USD 28.90 Billion |

| Growth Rate (2025 - 2030) | 11.53% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Big Data Technology And Service Market Analysis by Mordor Intelligence

The India Big Data Technology and Service Market size is estimated at USD 16.75 billion in 2025, and is expected to reach USD 28.90 billion by 2030, at a CAGR of 11.53% during the forecast period (2025-2030). The market is driven by population-scale digital public goods that pump fresh transaction streams into enterprise data lakes, nationwide 5G coverage that shifts data architectures from batch to stream, hyperscale cloud economics that lower total cost of ownership for small firms, and regulatory mandates that compel data governance upgrades. Competitive intensity stays high as Indian IT services majors, global cloud vendors, and niche analytics boutiques scramble to secure vertical footholds. Government incentives, such as production-linked subsidies for datacenter hardware, widen the opportunity for localized infrastructure providers, while the persistent mid-senior talent shortage inflates delivery costs but also spurs investments in low-code automation.

Key Report Takeaways

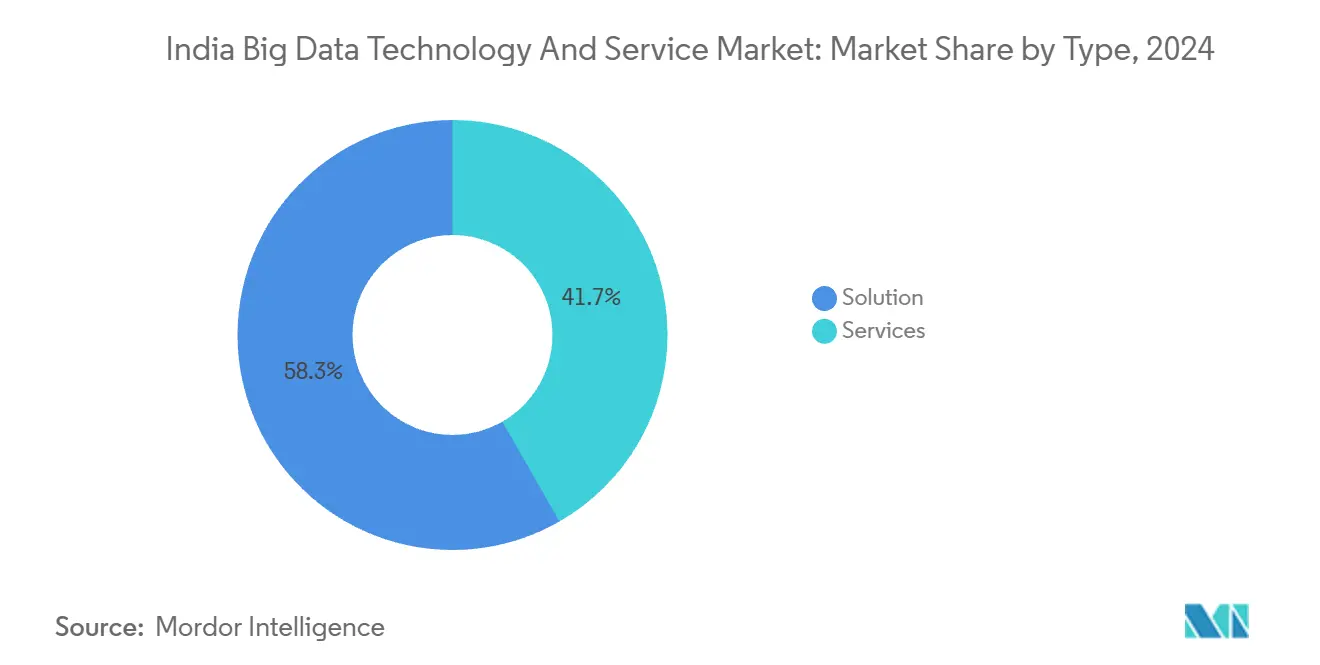

- By type, solutions constituted 58.3% of the India Big Data Technology and Service market share in 2024, and services are forecast to grow at a 12.6% CAGR to 2030.

- By deployment model, on-premise solutions captured 46.7% of the India Big Data Technology and Service market size in 2024, while cloud deployments are projected to advance at a 13.2% CAGR to 2030.

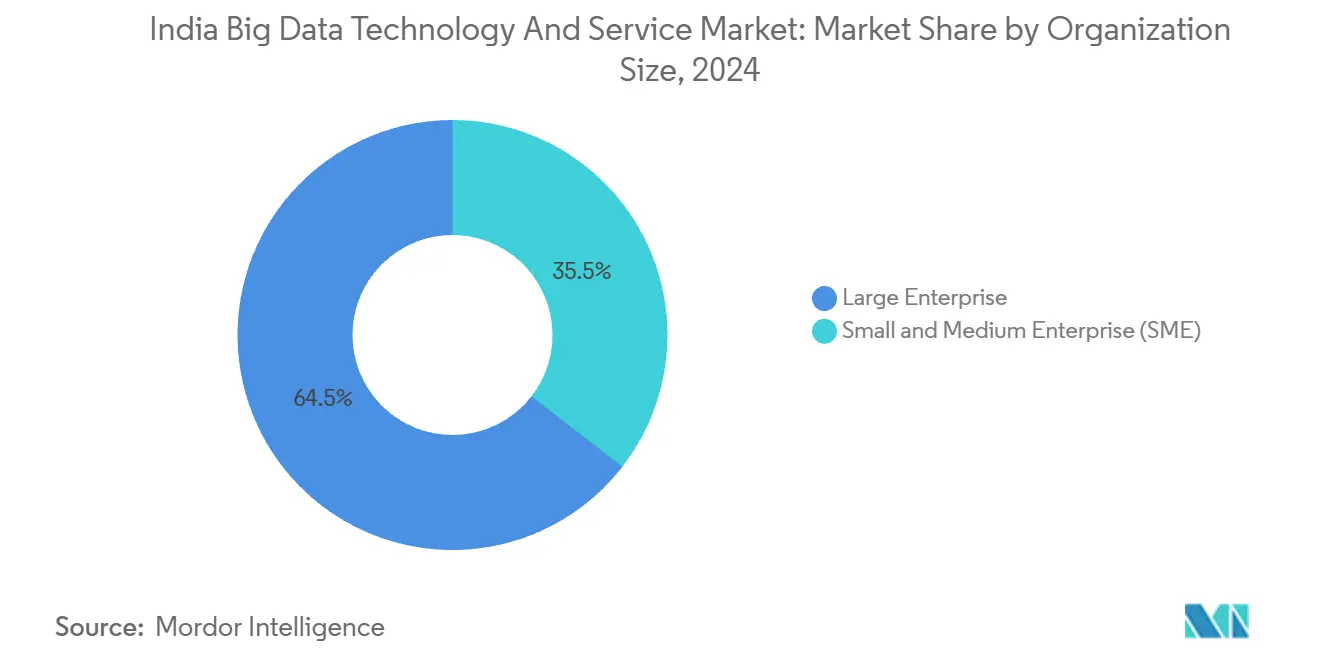

- By organization size, large enterprises commanded a 64.5% share of the India Big Data Technology and Service market size in 2024; SMEs record the highest projected CAGR at 12.78% through 2030.

- By end-user vertical, BFSI led with 22.6% of the India Big Data Technology and Service market share in 2024, whereas Healthcare and Life Sciences are expanding at a 13.9% CAGR through 2030.

India Big Data Technology And Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led open-data mandates accelerate enterprise analytics adoption | +2.1% | National; early gains in Delhi, Mumbai | Medium term (2-4 years) |

| 5G roll-out spurs real-time IoT data streams | +1.8% | Metro cities, expanding to Tier-2 centers | Short term (≤ 2 years) |

| Pay-per-use hyperscale cloud pricing lowers TCO | +1.5% | National; SME hubs in Gujarat, Tamil Nadu | Short term (≤ 2 years) |

| State-run digital-public-goods (Aadhaar, UPI) create new data lakes | +1.4% | National; rural focus | Long term (≥ 4 years) |

| Emergence of vernacular AI models boosts small-town datasets | +1.2% | Hindi, Tamil, Telugu regions | Medium term (2-4 years) |

| Energy-efficient ARM servers cut data-center OPEX | +0.9% | Maharashtra, Karnataka, Telangana hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-Led Open-Data Mandates Accelerate Enterprise Analytics Adoption

India’s Open Government Data Platform hosts more than 6,000 datasets from over 120 departments, obliging contractors on USD 45 billion of annual public procurement to demonstrate analytics competence.[1]Department of Administrative Reforms and Public Grievances, “Open Government Data Platform,” darpg.gov.inEnterprises integrate these external feeds to enrich risk scoring, fraud detection, and supply-chain visibility, thereby expanding spend on data ingestion tools and governance frameworks. Mid-tier analytics boutiques capitalize on the demand for public-sector data alignment that large system integrators often sidestep. The IndiaAI Mission’s allocation of 34,000 GPUs further removes compute barriers for advanced model training while keeping workloads within sovereign borders, stimulating hybrid cloud sales.[2]Ministry of Electronics and Information Technology, “IndiaAI Mission GPU Allocation,” meity.gov.in

5G Roll-Out Spurs Real-Time IoT Data Streams

Nationwide 5G coverage completed in October 2024 enables sub-20 millisecond latency, motivating manufacturing hubs in Gujarat and Tamil Nadu to boost sensor density by 40% since deployment.[3]Department of Telecommunications, “Nationwide 5G Coverage,” dot.gov.inEdge nodes within 50 kilometers of plants now process image and vibration data for predictive maintenance, expanding demand for stream-processing software that can ingest MQTT, OPC-UA, and proprietary protocols concurrently. Hyperscalers respond with micro-zone data centers, locking in new customers to integrated edge-cloud stacks that reduce capex for discrete manufacturers. Vendors skilled in event-driven analytics gain an early-mover advantage over legacy batch-oriented platforms.

Pay-Per-Use Hyperscale Cloud Pricing Lowers TCO

AWS, Microsoft, and Google now publicize consumption-based big-data tiers that trim total ownership costs for SMEs by 35-50% compared with perpetual licenses.[4]Amazon Web Services, “AWS Consumption-Based Pricing in India,” aws.amazon.com Textile clusters in Ahmedabad and automotive suppliers in Chennai deploy clickstream and quality-control analytics without buying servers, accelerating the Big Data Industry in India’s market footprint among the 63 million domestic SMEs. Traditional system integrators recalibrate revenue models toward managed services, while SaaS providers bundle analytics with domain apps to attract first-time data users.

State-Run Digital Public Goods Create New Data Lakes

Aadhaar’s 1.4 billion identities and UPI’s 131 billion annual transactions furnish structured population-scale data assets that enterprises remix for personalized offers and alternative credit scoring. The Account Aggregator framework widens consent-based sharing across 150 financial institutions, deepening insights into cash-flow volatility for small borrowers. Health records from the Ayushman Bharat Digital Mission enrich epidemiological dashboards that aid insurers in pricing preventive-care products. Together, these public utilities multiply data density and underpin triple-digit growth of governance-compliant analytics platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented data-sovereignty laws across states raise compliance cost | -1.6% | Multi-state BFSI, healthcare deployments | Short term (≤ 2 years) |

| Chronic shortage of mid-senior data engineers | -2.3% | National; acute in Bangalore, Hyderabad | Long term (≥ 4 years) |

| Legacy core-banking and telecom stacks resist integration | -1.1% | Metro BFSI, tier-1 telecom operators | Medium term (2-4 years) |

| Under-indexed cyber-insurance market limits risk-sharing | -1.4% | National; pronounced in export-oriented SMEs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Data-Sovereignty Laws Across States Raise Compliance Cost

Karnataka enforces data localization while Maharashtra allows cross-border transfers, forcing firms operating in both states to maintain parallel governance frameworks and increasing compliance spending by up to 40%. Sector-heavy BFSI and healthcare enterprises face the brunt, as patient and financial records traverse branch and telemedicine networks daily. Legal teams prolong contract negotiations, delaying analytics roll-outs that rely on multi-state data consolidation.

Chronic Shortage of Mid-Senior Data Engineers

India is short roughly 230,000 mid-senior data engineers, and salaries inflate 15-20% annually as global firms hire remotely at a 60% premium. Projects in stream-processing and MLOps stretch timelines, compelling enterprises to outsource or adopt low-code tooling. Extended delivery cycles erode projected ROI, especially in sectors where analytics payback depends on seasonal demand windows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Solutions Command the Foundation

Solutions owned 58.3% of the India Big Data technology and service market share in 2024, underscoring buyer preference for proven, compliance-ready platforms. Services, though smaller, are advancing at a 12.6% CAGR and are on track to lift their portion of India's Big Data technology and service market size as implementations grow more domain-specific. Indian buyers lean toward SAS, IBM, and Oracle packages for statutory comfort, then engage boutiques like Mu Sigma for vertical customization.

The enterprises shift from dashboarding to predictive and prescriptive routines that demand hands-on data engineering. Domestic consultancies leverage local regulatory fluency to price premium engagements, challenging global integrators whose playbooks remain technology-centric. This dynamic shifts revenue composition toward advisory and managed analytics over license resale.

By Deployment Model: Cloud Transformation Accelerates

On-premise installations retained 46.7% of India's Big Data technology and service market size in 2024, as regulators require in-house custody of sensitive BFSI and public-sector data. Cloud, however, is sprinting ahead at a 13.2% CAGR owing to USD 100-150 billion in hyperscale datacenter investments that remove sovereignty objections by keeping workloads within Indian borders. Hybrid configurations bridge core records on-premise with elastic compute in the cloud for fraud analytics and campaign management.

Local availability zones shrink latency and cut egress fees, tipping cost-benefit analyzes in favor of cloud-native stacks for new workloads. By 2028, cloud deployments are expected to overtake on-premise as the default for analytics pilots, compelling legacy BI vendors to refactor monoliths into micro-services to preserve relevance.

By Organization Size: SME Democratization Drives Growth

Large enterprises retained a 64.5% share of India's Big Data technology and service market size in 2024, but SMEs are racing ahead at a 12.78% CAGR as pay-as-you-go models erase upfront infrastructure hurdles. Export-oriented manufacturers in Gujarat and Karnataka deploy quality-inspection analytics to satisfy overseas certification, while e-commerce startups exploit clickstream intelligence to drive A/B testing velocity.

Although large enterprises still monopolize complex, multi-system projects, packaged vertical solutions are leveling the field. Vendors now market “one-click” analytics for invoice financing or telemedicine triage, reducing technical lift for SME buyers and threatening large-enterprise dominance over time.

By End-User Vertical: Healthcare Emerges as Growth Leader

The BFSI sector delivered 22.6% of India's Big Data technology and service market share in 2024, propelled by Basel III and RBI digital-lending compliance that makes analytics non-discretionary. Healthcare and Life Sciences, however, lead growth with a 13.9% CAGR as telemedicine and the Ayushman Bharat Digital Mission digitize patient records for population-health models.

BFSI remains resilient owing to risk and fraud mandates, yet healthcare’s pivot toward preventive analytics, genomics, and clinical decision support unlocks larger data bandwidth per capita.

Geography Analysis

Maharashtra, Karnataka, and Tamil Nadu jointly claimed roughly 60% of the India Big Data technology and services market in 2024 on the back of Mumbai’s financial hub, Bangalore’s tech cluster, and Chennai’s manufacturing strength. Karnataka’s Digital Economy Mission accelerates datacenter builds and talent skilling, buttressing vendor ecosystems.

Northern states led by Delhi-NCR and Uttar Pradesh are the fastest-growing territories as federal ministries digitize workflows and manufacturers set up cost-effective greenfield plants. Uttar Pradesh’s electronics policy ties capital subsidies to analytics adoption, fueling demand for factory intelligence suites.

Tier-2 cities such as Pune, Hyderabad, and Coimbatore register enterprises that tap lower-cost talent, and state governments dangle tax holidays for datacenters. Reliable broadband and edge cloud availability enable advanced workloads outside elite metros. Nonetheless, deep analytics talent remains scarce in smaller cities, making hybrid on-site and remote teams the norm.

Competitive Landscape

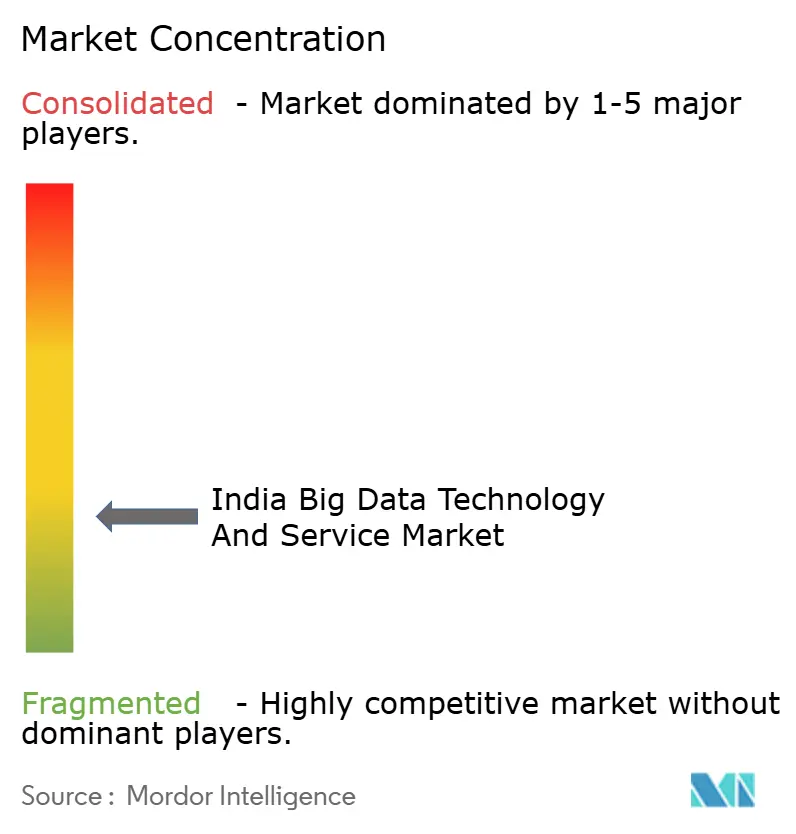

The India Big Data technology and service market is fragmented. Top Indian IT services firms such as TCS, Infosys, and Wipro expand analytics studios to preserve wallet share against cloud hyperscalers and platform specialists. Global vendors differentiate via technology depth, while local players leverage domain and regulatory fluency to win contracts requiring DPDP Act compliance.

TCS launches BFSI anti-fraud accelerators, AWS sells approved medical-data zones, and startups like Verloop.io build vernacular chat analytics for rural banking. Databricks works with state governments to train 10,000 engineers on Lakehouse architectures, and Cloudera teams with ride-sharing giant Ola for petabyte-scale data-lake workloads.

White-space opportunity persists in vernacular-language processing, rural credit scoring, and energy-efficient ARM-based analytics appliances. Players who align offers to these niches while assuring local data residency and auditability secure above-market margins despite intense price competition.

India Big Data Technology And Service Industry Leaders

Mu Sigma Business Solutions Private Limited

IBM Corporation

Capgemini SE

Fractal Analytics Limited

SAS Institute Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Cloudera disclosed a partnership with Krutrim to serve Ola and other enterprises with large-scale analytics on Krutrim Cloud.

- May 2025: Microsoft and Yotta Data Services partnered to deliver Azure AI services on Yotta’s sovereign Shakti Cloud for sectors such as agriculture, healthcare, and finance.

- April 2025: Databricks announced a USD 250 million investment over three years to expand R&D and headcount in India.

India Big Data Technology And Service Market Report Scope

The India big data technology and service market report is segmented by type (solution, and services), deployment model (on-premise, cloud, and hybrid), organization size (small and medium enterprise, and large enterprise), and end-user vertical (BFSI, retail and e-commerce, telecom and it, media and entertainment, healthcare and life-sciences, manufacturing, government and public sector). The market forecasts are provided in terms of value (USD).

| Solution |

| Services |

| On-premise |

| Cloud |

| Hybrid |

| Small and Medium Enterprise (SME) |

| Large Enterprise |

| BFSI |

| Retail and E-commerce |

| Telecom and IT |

| Media and Entertainment |

| Healthcare and Life-Sciences |

| Manufacturing |

| Government and Public Sector |

| By Type | Solution |

| Services | |

| By Deployment Model | On-premise |

| Cloud | |

| Hybrid | |

| By Organization Size | Small and Medium Enterprise (SME) |

| Large Enterprise | |

| By End-User Vertical | BFSI |

| Retail and E-commerce | |

| Telecom and IT | |

| Media and Entertainment | |

| Healthcare and Life-Sciences | |

| Manufacturing | |

| Government and Public Sector |

Key Questions Answered in the Report

What is the 2025 valuation of the Big Data Industry in India?

The market is valued at USD 16.75 billion in 2025.

How fast is cloud deployment growing?

Cloud deployments are expanding at a 13.2% CAGR through 2030.

Which sector currently leads spending?

BFSI leads, holding 22.6% share in 2024.

Which sector shows the fastest growth?

Healthcare and Life Sciences is forecast to grow at a 13.9% CAGR to 2030.

Are SMEs adopting big data analytics?

Yes, SMEs are the fastest-growing organization segment with a 12.78% CAGR, aided by pay-per-use cloud models.

What regions post the highest growth rates?

Delhi-NCR and Uttar Pradesh are pacing at 14-15% CAGR, while several Tier-2 cities exceed 16% growth.

Page last updated on: