India EV Battery Pack Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

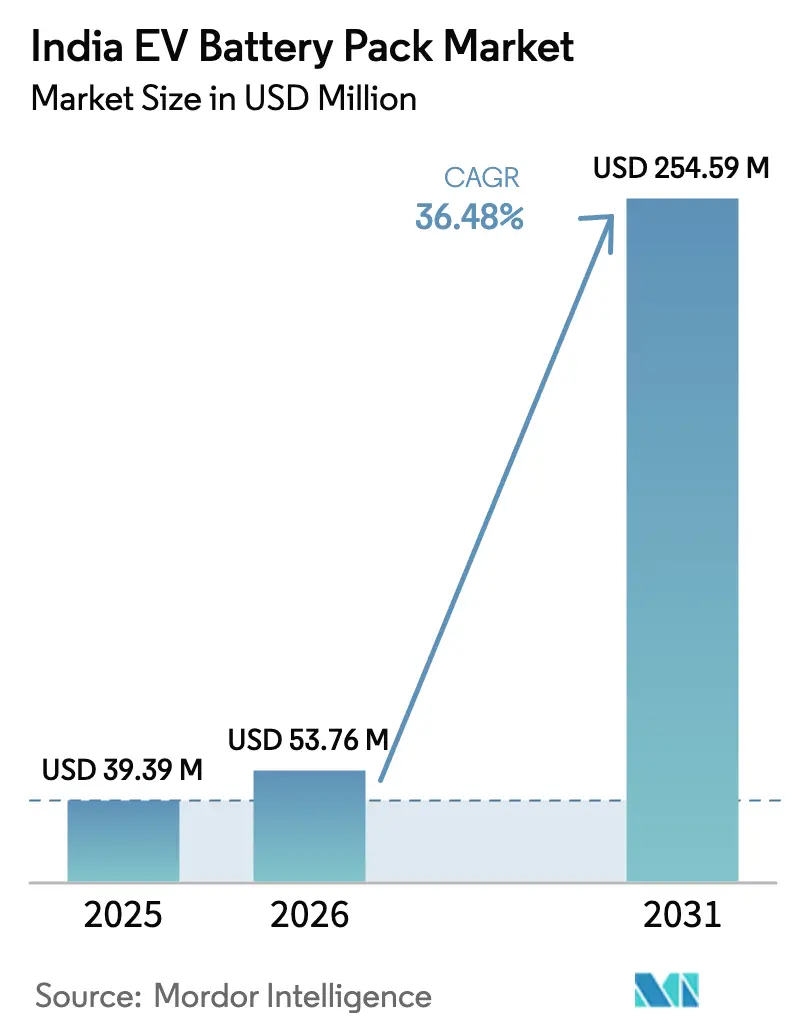

| Base Year Market Size (2025) | USD 39.39 Million |

| Market Size (2026) | USD 53.76 Million |

| Market Size (2031) | USD 254.59 Million |

| Growth Rate (2026 - 2031) | 36.48% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India EV Battery Pack Market Analysis by Mordor Intelligence

The India EV battery pack market size is expected to grow from USD 39.39 million in 2025 to USD 53.76 million in 2026 and is forecast to reach USD 254.59 million by 2031 at a 36.48% CAGR over 2026–2031. Declining cell costs, dual‐layer FAME-II and PLI-ACC incentives, and global gigafactory inflows position the India EV battery pack market as a strategic node in Asia’s electrification supply chain. Passenger cars continue to anchor pack demand, but accelerating bus and fleet orders are reshaping volume mix. Manufacturers are shifting toward LFP and emerging LMFP chemistries to balance safety, energy density, and raw-material security. New entrants are adopting cell-to-pack integration and 800 V architectures to shorten charging time, while incumbents invest in backward integration to safeguard margins.

Key Report Takeaways

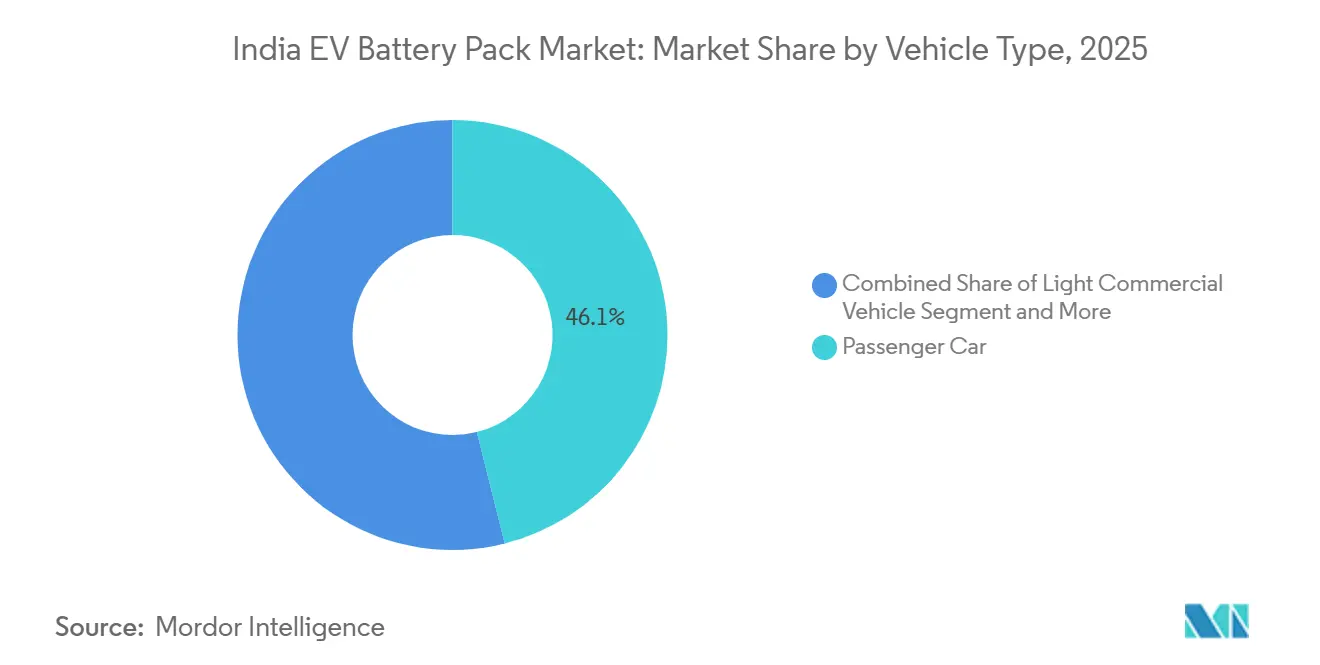

- By vehicle type, passenger cars led with 46.12% of the India EV battery pack market share in 2025, whereas buses are projected to post the fastest 46.45% CAGR through 2031.

- By propulsion, BEV solutions commanded 81.87% of volume in 2025 and are set to advance at a 34.92% CAGR through 2031 as charging density rises.

- By battery chemistry, LFP held 38.27% share in 2025, while LMFP is on track for the highest 49.18% CAGR owing to its superior energy density trajectory.

- By capacity, 40–60 kWh packs accounted for 41.35% share in 2025; the 80–100 kWh bracket is forecast to expand at a 38.62% CAGR on premium-EV adoption.

- By battery form, prismatic cells captured 43.67% of shipments in 2025 and are expected to grow at 28.91% CAGR due to manufacturing efficiency gains.

- By voltage class, 400–600 V systems commanded 56.82% share in 2025, whereas 600–800 V designs will deliver a 41.12% CAGR as OEMs chase ultrafast charging.

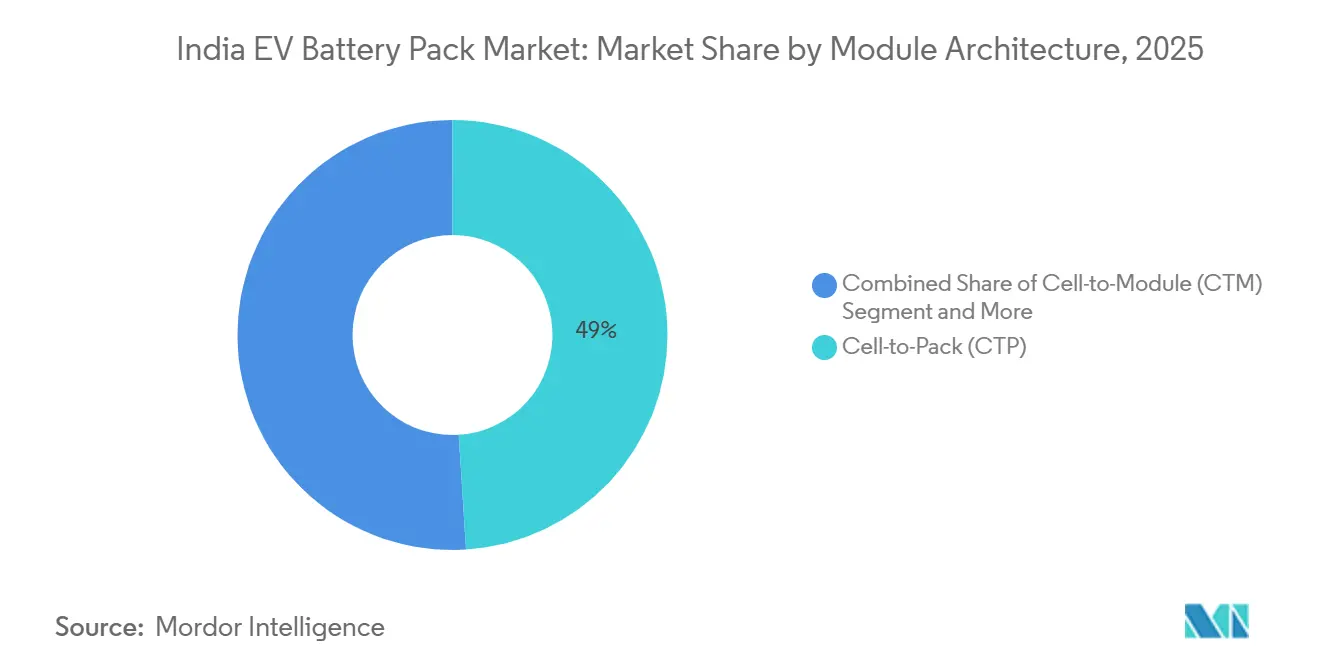

- By module architecture, cell-to-pack platforms led with 48.95% share in 2025 and will accelerate at a 43.87% CAGR on cost and density benefits.

- By component, cathode materials contributed 33.21% of pack value in 2025, while separators are poised for a 27.88% CAGR on stricter safety norms.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India EV Battery Pack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid fall in LFP and LMFP chemistries’ cost curve below USD 70/kWh | +9.1% | National, export oriented | Medium term (2-4 years) |

| FAME-II and Production-Linked Incentive schemes accelerate domestic demand | +8.2% | Gujarat, Tamil Nadu, Karnataka | Medium term (2-4 years) |

| Entry of global gigafactories bringing advanced cell formats | +7.3% | Western & Southern corridors | Long term (≥ 4 years) |

| Corporate-fleet electrification mandates | +6.8% | Delhi NCR, Mumbai, Bangalore | Short term (≤ 2 years) |

| Swappable-battery business models unlocking two- and three-wheeler volumes | +6.0% | Rajasthan, Andhra Pradesh pilot sites | Long term (≥ 4 years) |

| Domestic mineral refining (lithium, nickel) projects reduce import reliance | +5.6% | Tamil Nadu, Karnataka, Maharashtra | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

LFP and LMFP cost fall below USD 70/kWh

Cell costs crossed below USD 80/kWh in late 2025 at Chinese fabs; localized production and duty exemptions are projected to pull India's pack costs toward USD 70/kWh by 2027 [1]“Battery Technology Roadmap 2025,” BloombergNEF Research, about.bnef.com . LMFP promises higher energy density than LFP while retaining thermal tolerance, opening mid-segment car and light truck possibilities. Lower cobalt and nickel exposure hedges against commodity volatility and strengthens supply security. Pack makers are retooling for higher-nickel cathode severities to cover premium models while scaling LMFP lines for volume segments. Cost breakthroughs align with the removal of upfront FAME subsidies, sustaining affordability.

FAME-II and PLI-ACC incentives

FAME-II demand subsidies and the INR 18100 crore PLI-ACC program jointly cover vehicle buyers and cell makers, creating a closed-loop stimulus that cuts payback periods for investors. The first 30 GWh allocation already spans 16 approved bidders, equal to three-fifths of the projected domestic cell need by 2030 [2]“Corporate fleet mandates under NEMMP,” Economic Times Bureau, economictimes.indiatimes.com . Upfront subsidies for the first five production years shield gigafactories from scale-up losses. Delayed commissioning deadlines were extended in 2025, underscoring policy commitment despite start-up hurdles. State-level top-ups in Gujarat and Tamil Nadu further sweeten land and power costs for greenfield projects. Collectively, these measures lower delivered pack prices and quicken OEM model launches.

Global gigafactory entries

LG Energy Solution’s Gujarat JV, CATL’s disclosed Tamil Nadu roadmap, and Samsung SDI scouting reflect rising confidence in India’s battery value chain [3]“LGES-JSW joint venture details,” Business Standard Staff, business-standard.com . These investors introduce 4680 cylindrical and blade-style prismatic formats, cutting weight and boosting volumetric density. Technology transfer extends to advanced slurry mixing, dry-electrode coating, and automated formation cycling, which shorten the learning curves for local firms. Co-located supply agreements anchor OEM production, reducing logistics friction. Knowledge spillovers lift ecosystem productivity and set benchmarks for quality and safety.

Corporate fleet electrification mandates

From 2026, state notifications require a slight shift of urban commercial fleets to be electric, locking in predictable multi-year pack demand. Delhi’s aggregation portals and Karnataka’s green-cab scheme already guarantee fleet purchase volumes, giving pack assemblers stable order books. High daily utilization pushes total cost-of-ownership breakeven below three years for 15-40 kWh packs. National government agencies mirror these targets, spurring demand for standardized packs that ease maintenance. Leasing platforms and battery-as-a-service models leverage fleet regulations, further expanding the addressable market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slow roll-out of high-power public DC charging | -4.2% | Tier-2 and Tier-3 corridors | Medium term (2-4 years) |

| Safety recalls linked to thermal-runaway incidents | -3.8% | Northern and Coastal hot zones | Short term (≤ 2 years) |

| Working-Capital Crunch for Tier-2/3 Pack Assemblers Amid GST Credit Delays | -3.2% | National, port clusters | Long term (≥ 4 years) |

| Volatility in INR-USD Exchange Rate Inflates Imported Cell Costs | -2.5% | Emerging gigafactory hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Slow roll-out of >150 kW DC chargers

By 2025, only a limited number of public chargers were operational, predominantly consisting of mid-range power units. These units struggle to replenish larger battery packs within typical driver break times. Highway corridors between major metros lack high-power charging hubs, which hampers the electrification of long-haul eLCVs and intercity buses. As a result, operators are delaying the launch of high-capacity models. Simultaneously, energy firms are holding back, seeking assurance on volume. This has led to a classic chicken-and-egg scenario. While the PM E-DRIVE scheme has allocated a significant amount of funding, the pace of approvals and necessary utility upgrades lags behind the surging demand. Without a significant increase in charger density, the adoption of fast-charging will remain sluggish, limiting the potential for larger battery packs.

Thermal-runaway safety incidents

High ambient temperatures above 45 °C hasten degradation in nickel-rich chemistries, leading to headline recalls that dent consumer confidence. The Tata Nexon EV compensation ruling in 2025 spotlighted liability risks and spurred a wave of BIS standard updates. OEMs pivoted to LFP, yet premium buyers still seek higher energy density, sustaining exposure. Pack integrators now over-specify thermal interfaces, adding cost and weight that erode range benefits. Insurers have raised premiums for NMC-based models, signaling market pricing of safety externalities until widespread liquid cooling adoption stabilizes failure rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial mandates lift buses and delivery fleets

Passenger cars controlled 46.12% of the India EV battery pack market in 2025, reflecting early-adopter retail demand in the 40–60 kWh class. The segment benefits from favorable GST and zero-registration duty in select states. Parallelly, bus contracts under state transport utilities are scaling 200–400 kWh pack demand, shifting share toward heavier vehicles. OEM roadmaps indicate more than 10,000 e-bus deliveries by 2026, accelerating learning-curve drops for high-voltage packs.

Fleet economics dominate growth narratives. Daily urban mileage near 250 km amplifies fuel savings for ride-hail cars and delivery vans, underpinning repeat orders. Subsidized depot chargers compress downtime, and standardized pack formats simplify maintenance across multi-OEM fleets. Consequently, the bus category is forecast to expand at 46.45% CAGR, lifting the India EV battery pack market’s revenue mix toward commercial vehicles.

By Propulsion Type: BEV supremacy aligns with policy focus

BEV options made up 81.87% of 2025 shipments as simpler drivetrains and larger subsidies outweighed range concerns, and are also growing at a robust CAGR of 34.92% till 2031. Home and workplace charging meet most urban use cases, reducing dependency on sparse highway infrastructure. TCO parity arrives earlier for BEV than PHEV due to lower maintenance and tax incidence.

PHEV adoption remains niche, confined to premium SUVs using imported propulsion kits. Limited domestic component localization keeps sticker prices high. Nevertheless, policy dialogue on future zero-emission mandates could tighten CO₂ fleet averages and open narrow PHEV windows. Until then, BEV models will maintain the lion’s share, ensuring that the India EV battery pack market remains anchored in fully electric architectures.

By Battery Chemistry: LFP consolidation with LMFP momentum

LFP secured 38.27% of pack chemistry in 2025 due to inherent thermal stability and cobalt-free cost advantages. Domestic cathode powder production plans could widen its cost lead. LMFP is on an aggressive 49.18% CAGR trajectory, marrying higher energy density with comparable safety, creating a sweet spot for mid-size SUVs aimed at 500 km range.

Nickel-rich NMC variants continue in premium brands that target quick acceleration and extended range. Yet high metal exposure and safety recall risk limit mass-market penetration. As OEM homologation cycles converge around LMFP, supply chains are reorienting anode and electrolyte formulations to match higher voltage thresholds, gradually reshaping chemistry splits inside the India EV battery pack market.

By Capacity: Mid-range dominance, premium expansion

The 40–60 kWh band, aligned with family hatchbacks and compact SUVs, captured 41.35% share in 2025, emphasizing balanced range and affordability. Subsidy design caps and weight norms further reinforce this sweet spot. Above-80 kWh packs, however, will post a 38.62% CAGR as luxury imports and intercity e-buses proliferate.

Battery swapping pilots in two- and three-wheelers accelerate cyclic demand for 2–4 kWh modules, but these remain small in value. Over the forecast, average pack capacity edges upward as cell-level densities rise, keeping curb-weight constant. That shift supports higher revenue intensity per vehicle in the India EV battery pack market size estimates.

By Battery Form: Prismatic leadership aids thermal routing

Prismatic cells comprised 43.67% of shipments in 2025, aided by pack design efficiency and structural rigidity and are growing at a robust CAGR of 28.91% through 2031. Manufacturers integrate cooling channels between elongated cells to counter tropical heat, lowering thermal gradient stress. Cylindrical 4680 formats follow in premium sedans where fast power pulses justify round-cell pack designs.

Pouch cells, though light, confront swelling and compression challenges under long heat cycles. Indian pack makers are redesigning module trays to stabilize pouch stacks but scaling remains slower. Consequently, prismatic dominance is expected to persist, shaping tooling investments and vendor qualification inside the India EV battery pack industry.

By Voltage Class: 400 V mainstream, 800 V transition

Platforms in the 400–600 V class held 56.82% share during 2025, reflecting global benchmarks for compact EVs. Yet, 600–800 V architectures enable 350 kW charging, slicing charge times to sub-20 minutes, critical for highway electrification. The segment’s 41.12% CAGR hinges on simultaneous rollout of high-power chargers.

Component suppliers are redesigning IGBTs, cabling, and safety disconnects to manage doubled voltage without weight penalties. Government draft norms now list 800 V upper limits, offering regulatory clarity for upcoming launches. Voltage upsizing feeds directly into higher ASPs, bolstering revenue streams for the India EV battery pack market.

By Module Architecture: Cell-to-Pack cuts parts count

Cell-to-pack lines reduce modules entirely, boosting volumetric efficiency by 15% and slashing welding operations by reducing weld count. Holding 48.95% share in 2025, CTP will remain the architecture of choice, growing at 43.87% CAGR. Tooling amortization drops as fewer SKUs cover multiple models, raising break-even volumes for greenfield plants.

Traditional CTM persists where serviceability outweighs density, such as light trucks on rough roads. Module-to-pack legacy formats will phase out as OEMs re-platform, aligning the India EV battery pack market with global best-practice layouts.

By Component: Cathode cost center, separator sprint

Cathode powders accounted for 33.21% of the pack bill-of-materials in 2025, dominated by imported LFP and NMC precursors. Domestic nickel and lithium refining pilots seek to trim import bills. Separators, posting a 27.88% CAGR, grow faster on upgrades to ceramic-coated membranes that withstand higher voltage and temperature ranges.

Anodes evolve toward silicon blends, promising minimal energy density gains with limited cost uplift. Electrolyte suppliers race to commercialize high-voltage formulations compatible with LMFP and 800 V systems. Component localization will dictate future margin capture across the India EV battery pack market value chain.

Geography Analysis

Gujarat leads capacity build-out, hosting LG Energy Solution’s 20 GWh JV and Tata’s forthcoming gigafactory, leveraging coastal logistics and pro-manufacturing policy. The state’s port network streamlines cathode and anode raw-material imports, while renewable-rich grids cut carbon intensity, appealing to export-market auditors.

Tamil Nadu ranks second, integrating battery pack assembly into its Chennai and Hosur auto clusters. Ather Energy, Ola Electric, and TVS Motor localize cell and BMS lines to shorten supply loops. Karnataka’s Bangalore corridor specializes in R&D and prototyping, incubating chemistry start-ups and software-led BMS specialists.

Maharashtra and Haryana furnish OEM adjacency advantages, though higher land costs temper gigafactory scale. Emerging southern states like Telangana incentivize with twenty-year power-tariff shields, attracting Amara Raja’s massive plant. Geographic concentration, while efficient, magnifies risk from natural disasters or logistics snags, pushing policymakers to encourage multi-cluster dispersion across the India EV battery pack market.

Competitive Landscape

In the Indian EV battery pack market, Amara Raja and Exide are making significant strides, allocating substantial investments to shift from lead-acid to lithium cell lines. Their well-established dealer networks enhance their service reach.

Global giants are making their mark through joint ventures, introducing advanced formats and stringent quality controls. Notably, LG Energy Solution leads the charge with expertise in cylindrical technology, while CATL is exploring avenues for scaling LMFP.

Start-ups such as Log9 Materials are bringing high-C-rate cells to the three-wheeler market, and Sun Mobility is at the forefront of pioneering pack swapping. Key technological advancements focus on thermal management, liquid immersion systems, and AI-driven health algorithms tailored for India's unique climate. As concerns over raw material security grow, vertical integration and recycling initiatives are emerging as the next competitive frontiers.

India EV Battery Pack Industry Leaders

Contemporary Amperex Technology Co. Ltd. (CATL)

Denso Corporation

LG Energy Solution Ltd.

Nexcharge

Tata Autocomp Systems Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Ashok Leyland forged a significant, long-term partnership with China's CALB Group (China Aviation Lithium Battery), committing over ₹5,000 crore. This collaboration aims to establish a localized EV battery supply chain in India, starting with battery pack assembly and progressively advancing to cell manufacturing, all in line with Ashok Leyland's electric vehicle ambitions.

- August 2025: Ola Electric unveiled a self-developed ferrite motor, designed without rare-earth magnets, underscoring its quest for supply chain autonomy. Concurrently, the company is swiftly boosting its gigafactory's cell production capacity.

India EV Battery Pack Market Report Scope

The scope of the report includes Vehicle Type (Passenger Car and More), Propulsion Type (BEV and PHEV), Battery Chemistry (LFP and More), Capacity (Less Than 15 KWh and More), Battery Form (Cylindrical and More), Voltage Class (Less Than 400V and More), Module Architecture (CTM, CTP, and MTP), and Component (Anode and More).

| Passenger Car |

| Light Commercial Vehicle |

| Medium and Heavy-Duty Vehicle |

| Bus |

| Battery Electric |

| Plug-in Hybrid |

| LFP |

| LMFP |

| NMC (111/523/622/712/811) |

| NCA |

| LTO |

| Others |

| Less than 15 kWh |

| 15 kWh – 40 kWh |

| 40 kWh – 60 kWh |

| 60 kWh – 80 kWh |

| 80 kWh – 100 kWh |

| 100 kWh – 150 kWh |

| Above 150 kWh |

| Cylindrical |

| Pouch |

| Prismatic |

| Less than 400 V |

| 400–600 V |

| 600–800 V |

| More than 800 V |

| Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) |

| Module-to-Pack (MTP) |

| Anode |

| Cathode |

| Electrolyte |

| Separator |

| By Vehicle Type | Passenger Car |

| Light Commercial Vehicle | |

| Medium and Heavy-Duty Vehicle | |

| Bus | |

| By Propulsion Type | Battery Electric |

| Plug-in Hybrid | |

| By Battery Chemistry | LFP |

| LMFP | |

| NMC (111/523/622/712/811) | |

| NCA | |

| LTO | |

| Others | |

| By Capacity | Less than 15 kWh |

| 15 kWh – 40 kWh | |

| 40 kWh – 60 kWh | |

| 60 kWh – 80 kWh | |

| 80 kWh – 100 kWh | |

| 100 kWh – 150 kWh | |

| Above 150 kWh | |

| By Battery Form | Cylindrical |

| Pouch | |

| Prismatic | |

| By Voltage Class | Less than 400 V |

| 400–600 V | |

| 600–800 V | |

| More than 800 V | |

| By Module Architecture | Cell-to-Module (CTM) |

| Cell-to-Pack (CTP) | |

| Module-to-Pack (MTP) | |

| By Component | Anode |

| Cathode | |

| Electrolyte | |

| Separator |

Market Definition

- Battery Chemistry - Various types of battery chemistry considred under this segment include LFP, NCA, NCM, NMC, Others.

- Battery Form - The types of battery forms offered under this segment include Cylindrical, Pouch and Prismatic.

- Body Type - Body types considered under this segment include, passenger cars, LCV (light commercial vehicle), M&HDT (medium & heavy duty trucks)and buses.

- Capacity - Various types of battery capacities inldude under theis segment are 15 kWH to 40 kWH, 40 kWh to 80 kWh, Above 80 kWh and Less than 15 kWh.

- Component - Various components covered under this segment include anode, cathode, electrolyte, separator.

- Material Type - Various material covered under this segment include cobalt, lithium, manganese, natural graphite, nickel, other material.

- Method - The types of method covered under this segment include laser and wire.

- Propulsion Type - Propulsion types considered under this segment include BEV (Battery electric vehicles), PHEV (plug-in hybrid electric vehicle).

- ToC Type - ToC 1

- Vehicle Type - Vehicle type considered under this segment include passenger vehicles, and commercial vehicles with various EV powertrains.

| Keyword | Definition |

|---|---|

| Electric vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all electric vehicles as well as plug-electric vehicles as well as plug-in hybrids. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Battery Cell | The basic unit of an electric vehicle's battery pack, typically a lithium-ion cell, that stores electrical energy. |

| Module | A subsection of an EV battery pack, consisting of several cells grouped together, often used to facilitate manufacturing and maintenance. |

| Battery Management System (BMS) | An electronic system that manages a rechargeable battery by protecting the battery from operating outside its safe operating area, monitoring its state, calculating secondary data, reporting data, controlling its environment, and balancing it. |

| Energy Density | A measure of how much energy a battery cell can store in a given volume, usually expressed in watt-hours per liter (Wh/L). |

| Power Density | The rate at which energy can be delivered by the battery, often measured in watts per kilogram (W/kg). |

| Cycle Life | The number of complete charge-discharge cycles a battery can perform before its capacity falls under a specified percentage of its original capacity. |

| State of Charge (SOC) | A measurement, expressed as a percentage, that represents the current level of charge in a battery compared to its capacity. |

| State of Health (SOH) | An indicator of the overall condition of a battery, reflecting its current performance compared to when it was new. |

| Thermal Management System | A system designed to maintain optimal operating temperatures for an EV's battery pack, often using cooling or heating methods. |

| Fast Charging | A method of charging an EV battery at a much faster rate than standard charging, typically requiring specialized charging equipment. |

| Regenerative Braking | A system in electric and hybrid vehicles that recovers energy normally lost during braking and stores it in the battery. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms