Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

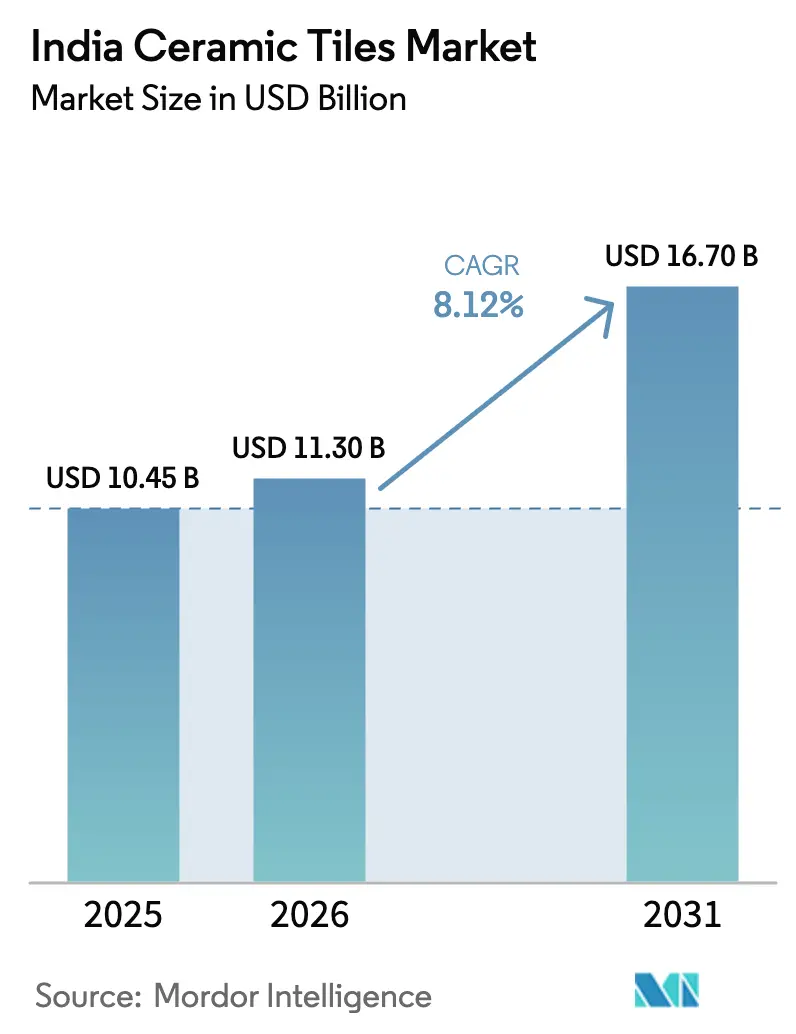

| Base Year Market Size (2025) | USD 10.45 Billion |

| Market Size (2026) | USD 11.30 Billion |

| Market Size (2031) | USD 16.70 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Ceramic Tiles Market Analysis by Mordor Intelligence

The India ceramic tiles market size is expected to increase from USD 10.45 billion in 2025 to USD 11.30 billion in 2026 and reach USD 16.70 billion by 2031, growing at a CAGR of 8.12% over 2026-2031. Manufacturers are increasingly focusing their production on housing and infrastructure projects, as exports face challenges due to anti-dumping duties in markets such as Saudi Arabia, Qatar, and Taiwan. West India continues to dominate, with Morbi's 800-plus manufacturing units contributing approximately 70% of the nation's output. Meanwhile, South India is experiencing the fastest growth, supported by IT-driven residential and industrial corridors. The market is shifting towards large-format porcelain slabs, while the adoption of hydrogen-ready kilns is helping reduce energy costs. The growth of online retail channels is enabling direct-to-consumer sales, compressing distributor margins.

Key Report Takeaways

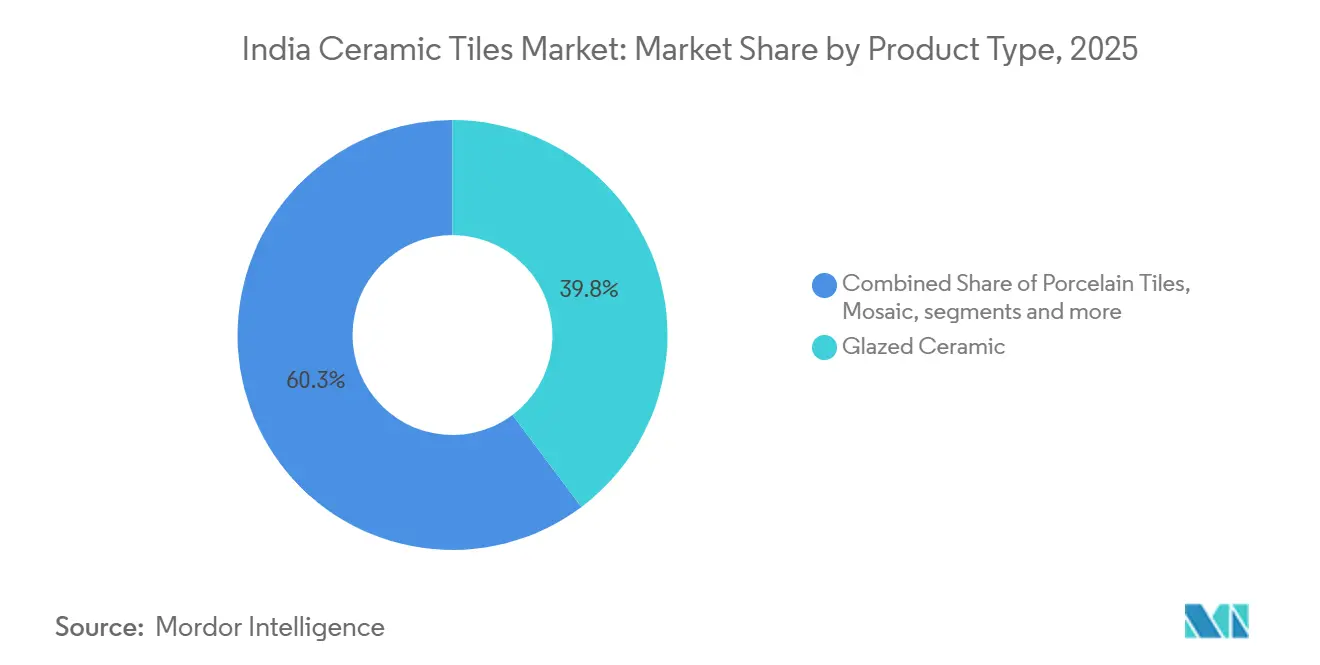

- By product type, glazed ceramic tiles led with 39.75% of the India ceramic tiles market size in 2025, whereas porcelain tiles are forecast to post the quickest rise at an 11.33% CAGR through 2031.

- By application, floor tiles accounted for a dominant 62.26% of the India ceramic tiles market share in 2025, while wall tiles are advancing at a 9.37% CAGR to 2031.

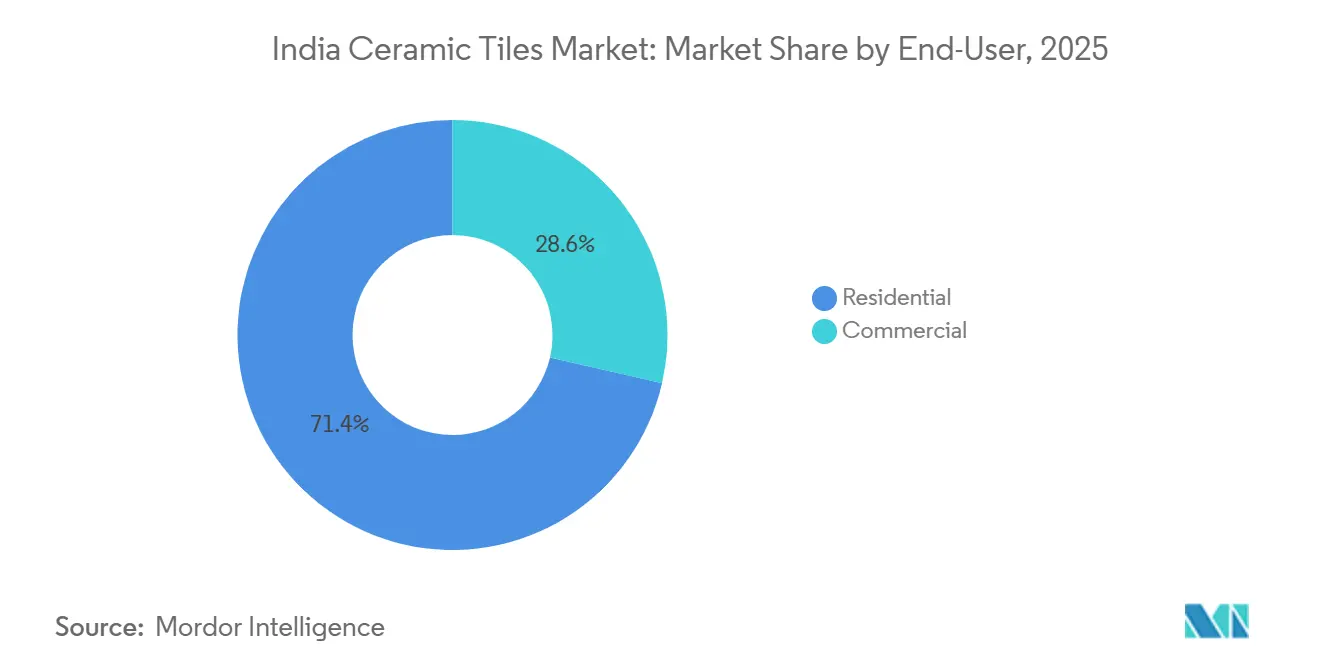

- By end-user segment, residential projects commanded 71.35% of the India ceramic tiles market size in 2025, but hospitality premises are projected to climb at a 10.87% CAGR to 2031.

- By construction type, new construction retained 55.78% of the India ceramic tiles market size in 2025, yet renovation work is expected to record a 10.82% CAGR through 2031.

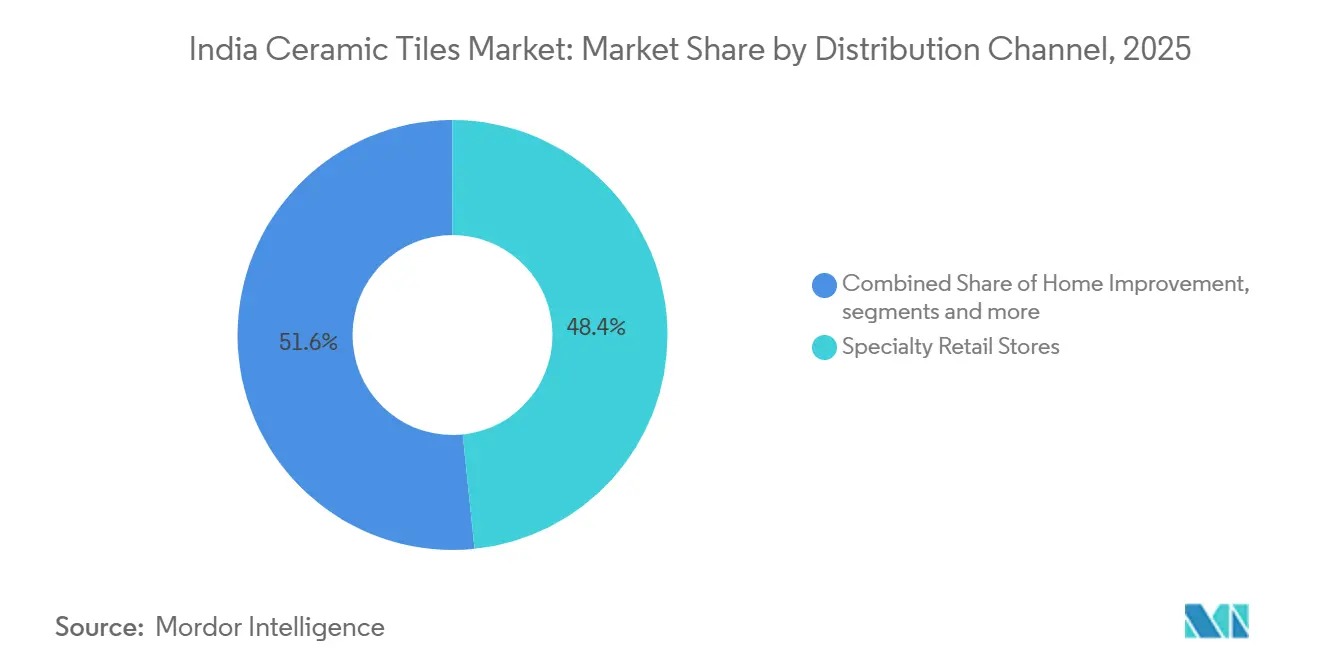

- By distribution channel, specialty retail stores led with 48.36% of the India ceramic tiles market size in 2025, whereas online retail is expected to record a 14.49% CAGR up to 2031.

- By Region, West India seized 35.37% of the India ceramic tiles market size in 2025, and South India is projected to register the quickest 10.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Affordable Housing and Smart City Projects | +2.1% | National: highest in Uttar Pradesh, Maharashtra, Gujarat, Rajasthan | Medium term (2–4 years) |

| Renovation Boom Among Urban Middle-Class | +1.4% | Delhi NCR, Mumbai, Bengaluru, Hyderabad, Pune | Short term (≤ 2 years) |

| Large-Format Slab Tiles Gain Popularity | +1.2% | South and West India, with spillover to North India metros | Medium term (2–4 years) |

| Morbi Clusters' Hydrogen-Ready Kilns Slash Energy Costs | +0.9% | Gujarat with diffusion to Rajasthan | Long term (≥ 4 years) |

| Small Builders Embrace Digital-Inkjet Mass Customization | +0.8% | National; early uptake in South and West India | Short term (≤ 2 years) |

| Thin-Set Overlay Systems See Rising Adoption | +0.6% | Tier-1 and tier-2 urban renovation markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growth in Affordable Housing and Smart City Projects

As of June 2024, the Pradhan Mantri Awas Yojana–Urban (PMAY-U) has made substantial progress toward its objective of delivering affordable housing, with several million homes sanctioned and delivered nationwide, reflecting steady advancement in urban housing supply[1]Source: Press Information Bureau, “PMAY Progress Update,” pib.gov.in. Builders working on these time-sensitive projects prefer suppliers that can deliver just-in-time, giving larger, organized players an edge. In smart-city public spaces, slip-resistant porcelain tiles rated R10–R13 comply with Bureau of Indian Standards norms. Product mixes are therefore tilting to premium slabs because safety and longevity outweigh upfront cost. Ongoing government investment in affordable housing and smart-city infrastructure ensures a steady pipeline of large-scale, high-value projects, supporting consistent demand for ceramic tiles. Coupled with increasing urbanization and rising consumer awareness of quality and safety standards, manufacturers are positioned to benefit from sustained growth in both residential and commercial segments.

Renovation Boom Among Urban Middle-Class

Demand from architects and project specifiers in India is increasingly moving away from conventional 600 mm × 600 mm tiles toward large-format slab tiles measuring up to 1,600 mm × 3,200 mm, driven by preferences for seamless aesthetics in luxury residential developments and premium commercial spaces such as hotel lobbies. To meet this demand, domestic manufacturers have invested in advanced Italian pressing technology that minimizes warpage and enables consistent quality at larger sizes. These technological upgrades allow producers to command price premiums of approximately 15%–25% over standard tiles, while incremental labor costs remain relatively contained[2]Source: Kajaria Ceramics, “Annual Report FY24,” kajariaceramics.com. Large slabs are becoming a meaningful contributor to premium revenue streams, reinforcing their strategic importance within the higher-value segment of the market. Additionally, large-format tiles support green-building objectives by reducing grout usage, which in turn lowers volatile organic compound emissions and aligns with India’s Energy Conservation Building Code. Manufacturers that fail to upgrade production capabilities risk losing share in the premium segment of the Indian ceramic tiles market.

Small Builders Embrace Digital-Inkjet Mass Customization

The technology allows manufacturers to produce short runs of approximately 500–1,000 square meters with distinct patterns, textures, and color variations, removing the high setup costs and minimum order requirements associated with traditional screen printing[3]Source: System Ceramics, “Digital Inkjet Lines in India,” systemceramics.com. This has expanded design access for small and mid-sized residential developers, allowing projects in tier-2 and tier-3 cities to specify tiles inspired by regional stone, cultural motifs, or bespoke aesthetics without incurring the significant cost premiums previously associated with low-volume customization. The growing installation of high-speed, high-resolution inkjet lines by Indian tile manufacturers has further improved operational efficiency, enabling faster order fulfillment and shorter production lead times. In addition to design flexibility, digital inkjet technology supports sustainability goals by reducing water usage compared to conventional wet processes, aligning with water-conservation regulations in drought-affected states.

Thin-Set Overlay Systems See Rising Adoption

The growing use of thin-set overlay systems is emerging as an important driver in the Indian ceramic tiles market, particularly within the renovation and replacement segment. These advanced adhesive systems allow 6–8 mm thin tiles to be installed directly over existing flooring, eliminating the need for tile removal, heavy demolition, and dust-intensive processes. As a result, homeowners can complete kitchen and bathroom renovations within a few days instead of several weeks, significantly reducing disruption to daily living. The ability to avoid demolition also delivers cost savings of nearly 60%–70% on floor removal expenses, making renovation projects financially viable for middle-income households. Builders and contractors are increasingly adopting overlay systems in tier-2 cities, where improving interior finishes is closely linked to higher resale values. Manufacturers that offer thinner, high-strength tiles compatible with overlay applications are therefore well positioned to benefit from the growing replacement and refurbishment demand across India.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Natural Gas Prices Experience Significant Fluctuations | -1.3% | Gujarat, Rajasthan, with spillover to national pricing | Short term (≤ 2 years) | |

| Key Export Destinations Impose Anti-Dumping Duties | -0.9% | National; sharper in Gujarat and Tamil Nadu export-oriented plants | Medium term (2–4 years) | |

| Mundra Port Faces Logistics Bottlenecks | -0.4% | Gujarat affects container supply and freight rates | Short term (≤ 2 years) | |

| Commercial Shift Towards LVT/SPC Flooring | -1.1% | Metro office and retail projects | Medium term (2–4 years) | |

| Source: Mordor Intelligence | ||||

Natural Gas Prices Experience Significant Fluctuations

Volatility in natural-gas prices poses a significant challenge for ceramic tile manufacturers in India, particularly those in energy-intensive regions like Morbi, Gujarat. Unpredictable fuel costs make it difficult for producers to offer fixed-price contracts to builders, forcing the inclusion of quarterly price-revision clauses that can alienate cost-sensitive customers in the affordable-housing segment. For instance, in July 2024, Gujarat Gas raised industrial gas prices by INR2–INR2.48 (USD 0.023–USD 0.029) per SCM, increasing energy bills for local manufacturers by 8% to 12% depending on kiln efficiency. Since gas accounts for 30%–35% of variable costs, a 10% price change can erode 3%–3.5% of gross margins, while legacy contracts expiring in 2025 face immediate margin pressure[4]Source: Gujarat Gas, “Industrial Natural Gas Price Notice,” gujaratgas.com. Price volatility also discourages investment in new kiln capacity, as lenders require higher debt-service coverage and payback assumptions become uncertain. While some producers have mitigated risk by diversifying into coal-fired kilns or installing solar thermal pre-heaters, achieving 5%–8% lower cost variability, these retrofits demand INR15–25 crore (USD 1.8–3 million) per line and take 18–24 months to commission, limiting their short-term feasibility.

Commercial Shift Towards LVT/SPC Flooring

In India, the rising popularity of luxury vinyl tile (LVT) and stone-plastic composite (SPC) flooring in offices, retail spaces, and hospitality sectors is intensifying competition for ceramic tile manufacturers. LVT and SPC flooring boast advantages over traditional ceramic tiles: they install more swiftly, are lighter, and manage moisture better. Their click-lock installation system, which forgoes adhesives, slashes labor costs by 40%–50% and trims project timelines by 30%. This efficiency makes them particularly appealing for co-working spaces and tech campuses in cities like Bengaluru and Hyderabad. The Indian vinyl flooring market, buoyed by imports from China, South Korea, and Vietnam, as well as domestic production from firms like Greenlam Industries and Action Tesa, is on a trajectory of double-digit growth through 2030. Yet, LVT’s unmatched acoustic performance and its comforting warmth underfoot pose challenges for replication. This has led ceramic producers to channel investments into R&D for composite-backed tiles, aiming to stay relevant in the competitive commercial renovation arena.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Gains on Premium Projects

In 2025, glazed ceramic tiles held a 39.75% market share, solidifying their dominance in mid-range residential projects where builders prioritize cost over aesthetics. However, porcelain tiles are set to grow at 11.33% CAGR through 2031. This surge is fueled by architects' preference for low-porosity, high-strength materials in luxury apartments, hotel lobbies, and airport terminals. With a water absorption rate below 0.5%, porcelain is ideal for exterior facades and wet areas. Manufacturers like Somany Ceramics and H&R Johnson have adopted Italian dry-pressing technology, enabling them to produce porcelain slabs measuring up to 1,600 mm × 3,200 mm with minimal warpage. Unglazed ceramic tiles find their niche in industrial and outdoor settings, prioritizing slip resistance over aesthetics. In contrast, mosaic tiles are favored by boutique interior designers and for heritage restoration.

Porcelain tiles boast an attractive margin profile: they achieve average selling prices 20% to 30% higher than glazed ceramics. Meanwhile, the rise in raw material costs for feldspar, kaolin, and quartz hovers between 12% to 15%. This dynamic results in an impressive 500 to 700 basis points of incremental gross margin. Such economics shed light on Kajaria Ceramics' decision to invest INR200 crore (USD 24 million) in fiscal 2024, aiming to boost porcelain capacity at its Gailpur and Maloot plants. The company targets a 25% contribution from porcelain to its total volumes by fiscal 2027. While glazed ceramics continue to dominate affordable housing and demand in tier-2 cities, their market share is poised to decline. This shift is attributed to builders elevating specifications, influenced by buyer expectations shaped by social media and home-improvement shows.

By Application: Wall Tiles Ride Design Premiumization

In 2025, floor tiles accounted for 62.26% of the total market size, primarily driven by their use in residential living rooms, kitchens, and bathrooms, where durability and ease of cleaning are paramount. Wall tiles, however, are set to experience a robust growth rate of 9.37% CAGR through 2031. This surge is attributed to urban homeowners and commercial developers increasingly opting for digital-inkjet patterns. These patterns mimic the aesthetics of marble, wood, and fabric textures, all at a fraction of the cost of their natural counterparts. This shift towards wall tiles underscores a broader trend of premiumization in the market. Buyers are now willing to allocate larger budgets for feature walls, especially in master bedrooms and reception areas. Government mandates in hill stations and coastal zones specify clay or concrete roofing tiles, emphasizing their cyclone resistance and thermal insulation properties.

The growth of wall tiles is closely linked to an uptick in per-capita spending on home interiors. This spending rose from INR18,000 (USD 216) in fiscal 2020 to INR26,000 (USD 312) in fiscal 2024, as reported by ICRA, and is particularly notable among urban households earning above INR10 lakh (USD 12,000) annually. Builders, keenly attuned to millennial preferences, are now installing wall tiles in spaces like open kitchens and home offices. These areas, once dominated by paint or wallpaper, have seen an 8% to 10% increase in wall-tile volumes per project due to this expanded usage. While floor tiles are riding the wave of renovations, homeowners are swapping 10- to 15-year-old vitrified tiles for anti-skid porcelain; the replacement cycle for floors is notably longer. On the other hand, roofing tiles are facing competition from metal sheets and polycarbonate panels, especially in industrial sheds.

By End-User: Hospitality Leads Growth Amid Tourism Surges

In 2025, residential applications commanded a dominant 71.35% market share, buoyed by India's vast population of 1.4 billion and a relentless urbanization trend that annually adds 10 to 12 million households. Meanwhile, the hospitality sector, encompassing hotels, resorts, and transport hubs, foresees an expansion at a robust 10.87% CAGR through 2031. This growth is fueled by India's ambitious target of drawing 30 million international tourists by 2028, coupled with a rebound in domestic travel post-pandemic. Notably, the hospitality segment opts for high-traffic-rated tiles (PEI 4 and PEI 5) boasting slip-resistance coefficients exceeding R10. Landmark projects, such as the Statue of Unity complex in Gujarat and the redevelopment of Ayodhya's temple precinct, are consuming millions of square meters of these custom-designed tiles, as highlighted by the Press Information Bureau.

Educational institutions and transport hubs, including airports, metro stations, and bus terminals, account for a significant share of commercial demand. These entities show a preference for large-format tiles, which reduce grout lines and streamline cleaning processes. Residential demand remains a core segment of the Indian ceramic tiles market, but its growth is relatively moderate compared with the faster expansions in the hospitality and commercial sectors. In contrast, the healthcare segment is witnessing increasing adoption of antimicrobial-glazed tiles, which help inhibit bacterial growth and support enhanced infection-control measures. Consequently, while residential demand continues to provide steady market support, the commercial, hospitality, and healthcare segments are emerging as key drivers of overall market growth.

By Construction Type: Renovation Accelerates Amid Urban Upgrades

New construction accounted for 55.78% of the total market size in 2025, highlighting India's significant housing deficit. The Ministry of Housing and Urban Affairs estimates a shortage of 10 million units in urban areas and 40 million units in rural regions. Renovation and replacement activities are projected to grow at a CAGR of 10.82% through 2031, driven by urban households earning over INR 8 lakh (USD 9,600) annually, who are upgrading kitchens, bathrooms, and living rooms with open layouts, modular storage, and designer finishes. The typical renovation cycle for ceramic tiles spans 12 to 15 years. Homes built between 2008 and 2015, during India's pre-financial-crisis construction boom, are now entering the replacement phase. These advancements make renovations more accessible for middle-class households, who previously delayed upgrades due to concerns about disruption, as noted in an ICRA Report on Building Materials.

New construction is supported by extensive government infrastructure initiatives, including the 100 smart cities project, PMAY's goal of 11.8 million housing units, and the National Infrastructure Pipeline's INR 111 lakh crore (USD 1.3 trillion) investment through 2030. On average, each new residential unit requires 50 to 70 square meters of tiles, while commercial projects demand 80 to 120 square meters per 1,000 square feet of built-up area. Renovation demand is concentrated in metro cities such as Delhi NCR, Mumbai, Bengaluru, and Hyderabad, where rising property values justify interior upgrades. Builders targeting the renovation segment are introducing tile collections with click-lock backing and self-adhesive layers, enabling DIY installations. These innovations appeal to consumers who prioritize convenience and cost control over contractor-led projects.

By Distribution Channel: Online Retail Disrupts Traditional Networks

In 2025, specialty tile and stone stores commanded a dominant 48.36% market share, capitalizing on their unique offerings: full-size tile displays, on-site design consultations, and bundled installation services. Meanwhile, online retail is set to surge at a robust 14.49% CAGR through 2031. This growth is largely fueled by direct-to-consumer (D2C) brands, including Orientbell, Somany, and Kajaria. These brands have rolled out e-commerce platforms equipped with augmented-reality room visualizers, allowing buyers to preview tile patterns in their own spaces before making a purchase. Home improvement and DIY stores, like Home Centre and Urban Ladder, account for 12% to 15% of the market. They do this by stocking mid-range tiles alongside sanitaryware and hardware, catering to homeowners undertaking small-scale renovations without the help of contractors.

Online retail allure is rooted in its transparency and convenience. Buyers can effortlessly compare prices across brands, peruse user reviews, and schedule home delivery within 48 to 72 hours, all without the hassle of visiting multiple showrooms. Kajaria Ceramics highlighted the growing significance of e-commerce in its operations, noting that the channel contributed 4% to its fiscal 2024 revenues, a significant jump from 1.5% in fiscal 2022. The company has set its sights on achieving a 10% contribution by fiscal 2027, bolstered by partnerships with giants like Amazon and Flipkart, in addition to its own website. To counter the encroachment of online platforms, specialty stores are doubling down on value-added services. They offer free design consultations, installation training for contractors, and loyalty programs that online platforms find challenging to emulate.

Geography Analysis

In 2025, West India commanded a 35.37% market share of India's ceramic tiles market, largely due to the Morbi cluster in Gujarat. This region enjoys advantages like proximity to raw materials, well-established supply chains, and a robust manufacturing ecosystem, all of which streamline production and cut costs. While smaller clusters in Maharashtra and Rajasthan cater to local residential and commercial projects bolstered by infrastructure investments such as high-speed rail and renewable energy, West India grapples with export challenges, notably anti-dumping duties in key markets. Nevertheless, the region stands strong as a production hub, serving both domestic needs and selective export demands.

South India, spearheaded by Telangana, Karnataka, Tamil Nadu, and Kerala, is on track to expand at a 10.24% CAGR through 2031. This growth is fueled by the IT sector's expansion, the development of industrial corridors, and bolstered tourism infrastructure, all driving a heightened demand for premium and custom-designed tiles. In major cities, landlords are increasingly choosing durable porcelain tiles for commercial spaces, aiming to minimize maintenance costs over extended leases. To differentiate in competitive projects, local manufacturers are pouring investments into digital inkjet technology, catering to specialized design needs. Additionally, rising incomes and urbanization trends are propelling the adoption of higher-value tiles in both residential and hospitality sectors.

North and East India, while holding a smaller slice of the market, see growth bolstered by urban residential construction and affordable housing initiatives. East India, hindered by lower urbanization rates and per-capita incomes, is nonetheless witnessing a surge in demand for commercial-grade tiles, due to industrial growth in states like Odisha. Moreover, strategic logistics hubs in East India are streamlining distribution to adjacent areas, including Northeast India and Bangladesh. Meanwhile, North India maintains a preference for mid-range offerings in both residential and commercial sectors, striking a balance between cost and quality. Though their growth lags South India's, both regions consistently contribute to the nation's overall demand.

Competitive Landscape

The Indian ceramic tiles market is moderately fragmented, with leading organized players Kajaria Ceramics, Somany Ceramics, H&R Johnson, Asian Granito, and Nitco capturing a significant share of branded-sector revenues. Smaller regional and unorganized producers continue to dominate tier-2 and tier-3 cities, leaving ample white space for new entrants. Energy efficiency and technology adoption are emerging as key differentiators, with hydrogen-ready kilns, solar thermal preheaters, and digital inkjet printers providing low-cost producers a margin advantage. Kajaria’s patented nano-coating enhances scratch and stain resistance, while Somany leverages AI-driven quality control to reduce defects below 1%, bolstering reliability. Competitive intensity revolves around fuel efficiency, design refresh cycles, and distribution reach, influencing profitability across the sector.

Strategic initiatives by organized players focus on capacity expansions, product innovation, and backward integration. BIS certification, mandatory for organized players, ensures quality and creates barriers for unorganized operators, with costs per SKU ranging from USD 2,400 to USD 6,000. The technology adoption and compliance standards separate market leaders from laggards while sustaining consumer confidence.

The market is expected to consolidate gradually over the next decade as smaller producers face fuel-cost pressures, export challenges, and operational inefficiencies. White-space opportunities include antimicrobial-glazed tiles for healthcare facilities, ultra-thin porcelain for retrofits, and premium tiles with integrated heating, segments currently dominated by European imports. Organized players are also leveraging D2C e-commerce platforms to bypass traditional dealer networks and expand market reach. Regional diversity and price sensitivity ensure fragmentation persists at higher levels than in mature markets such as China or Europe. Firms that combine innovation, efficient production, and strong distribution are positioned to capture market share while sustaining long-term growth.

India Ceramic Tiles Industry Leaders

Kajaria Ceramics Limited

Somany Ceramics Limited

H&R Johnson (India)

Asian Granito India Ltd

Nitco Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Antica Ceramica launched a Kota stone‑inspired tile collection that modernizes the traditional material with large‑format, durable, stain‑resistant, and non‑slip tiles suitable for both residential and commercial wall and floor applications.

- June 2025: RAK Ceramics launched its Re‑Use tile collection, the world’s first porcelain tiles made entirely from 100 % pre‑consumer recycled materials, offering durable, stylish, and eco‑friendly flooring and wall options that reduce resource use and support sustainable building practices without compromising performance.

- February 2025: Simpolo Tiles & Bathware opened a new 7,000 sq ft display centre in Chennai’s T. Nagar, showcasing its latest premium tile ranges and surface technologies to architects, designers, and homeowners, reinforcing its regional market presence and expansion strategy.

India Ceramic Tiles Market Report Scope

India's ceramic tile market is segmented by product, application, construction type, and end-user. By product, the market is sub-segmented into glazed, porcelain, scratch-free, and other products. The market is sub-segmented by application into floor tiles, wall tiles, and other applications. The market is sub-segmented by construction type into new construction, replacement, and renovation. By end-user, the market is sub-segmented into residential and commercial. The report offers market size and forecasts for the Indian ceramic tiles market in value (USD ) for all the above segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| North India |

| South India |

| West India |

| East India |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | North India | |

| South India | ||

| West India | ||

| East India | ||

Key Questions Answered in the Report

How big is the India ceramic tiles market in 2026?

The India ceramic tiles market size is USD 11.30 billion in 2026 and is forecast to reach USD 16.70 billion by 2031.

Which region is growing fastest for ceramic tiles in India?

South India shows the quickest expansion at a 10.24% CAGR through 2031, helped by IT-driven housing and industrial corridors.

What is driving the switch to porcelain tiles?

Low porosity, larger slab formats, and 20%–30% price premiums with higher margins are shifting demand toward porcelain.

How are online channels changing tile sales?

Direct-to-consumer online platforms with AR room visualizers are expanding at a 14.49% CAGR, eroding traditional dealer share.

Why are energy costs critical for tile makers?

Fuel accounts for up to 35% of variable costs, and gas price swings can compress gross margins by more than three points.

Page last updated on: