Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

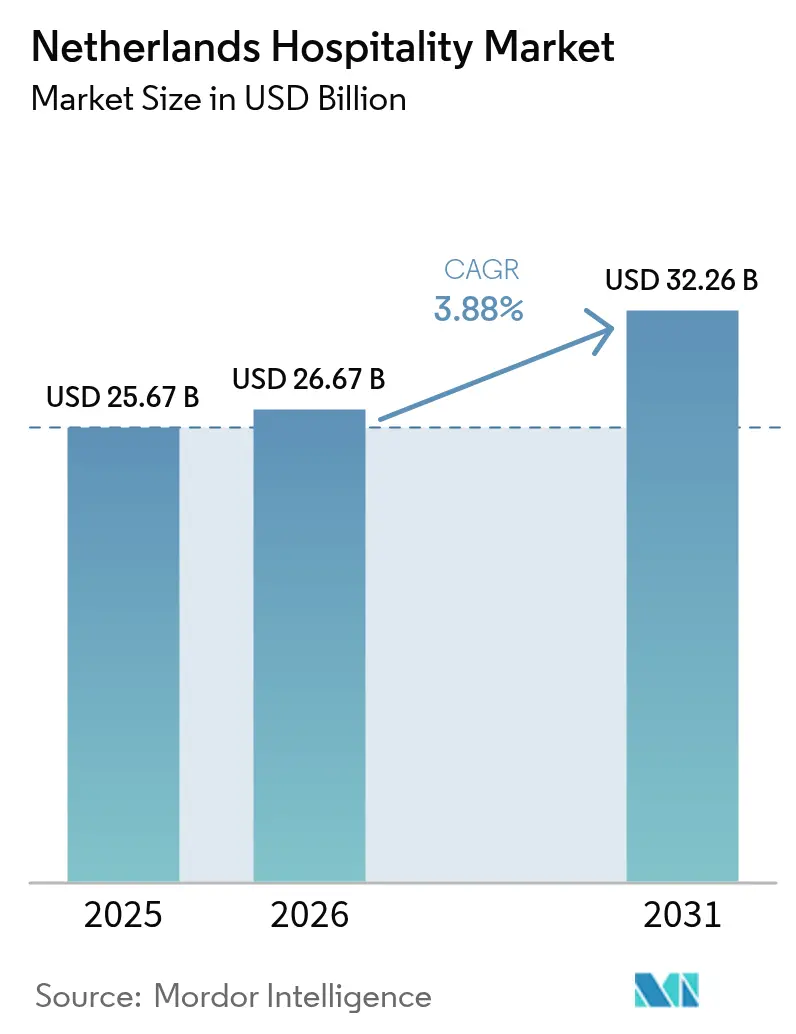

| Base Year Market Size (2025) | USD 25.67 Billion |

| Market Size (2026) | USD 26.67 Billion |

| Market Size (2031) | USD 32.26 Billion |

| Growth Rate (2026 - 2031) | 3.88% CAGR |

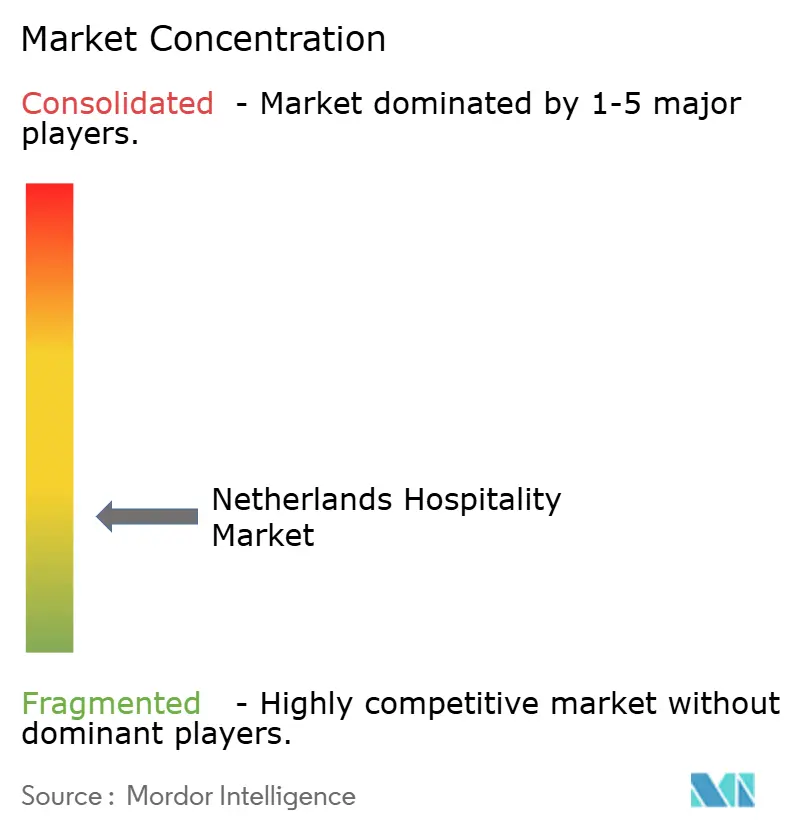

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Hospitality Market Analysis by Mordor Intelligence

The Netherlands hospitality market size is expected to grow from USD 25.67 billion in 2025 to USD 26.67 billion in 2026 and is forecast to reach USD 32.26 billion by 2031 at 3.88% CAGR over 2026-2031. Record tourism receipts of EUR 105 billion (USD 116.6 billion) in 2023 reflect a sharp 15% annual increase, while overnight stays topped 50 million guests in 2024, up 4% year on year[1]Statistics Netherlands, “Tourism Expenditure Rises to Nearly 105 Billion Euros in 2023,” cbs.nl. . International arrivals surpassed the 2019 baseline by 2% in 2024, encouraged by the removal of health-related travel barriers, Schiphol’s improving seat capacity, and active destination marketing that spotlights secondary provinces. Chain penetration reached 61%, well above the European mean of 35%, pointing to an operating landscape where scale-driven efficiencies, brand trust, and loyalty programs are pivotal. Budget and economy flags leverage standardized design, lean staffing models, and asset-light agreements to accelerate rollouts in university towns and logistics hubs, where cost-conscious leisure and business travelers converge. Simultaneously, robust direct-booking momentum, fueled by the EU Digital Markets Act (DMA), is shifting revenue away from high-commission online travel agencies (OTAs) toward proprietary channels that bolster net margins.

Key Report Takeaways

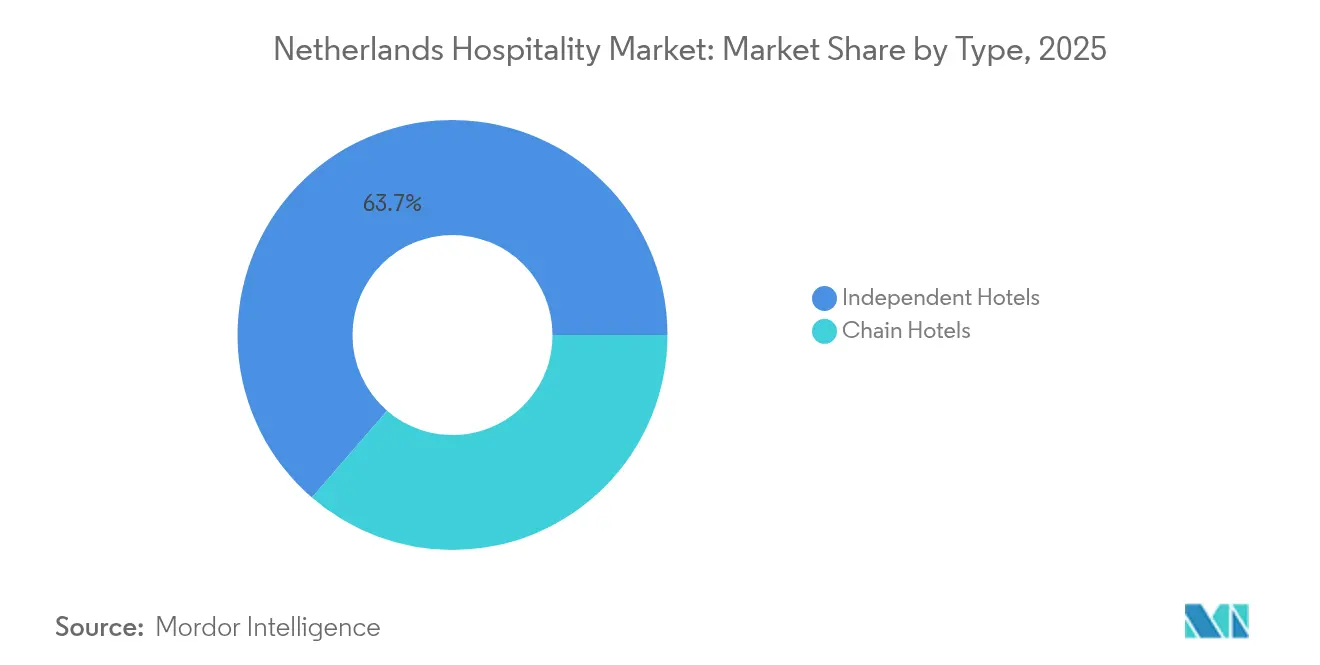

- By type, Independent Hotels captured 63.65% of the Netherlands hospitality market share in 2025, whereas Chain Hotels are advancing at a 4.64% CAGR through 2031.

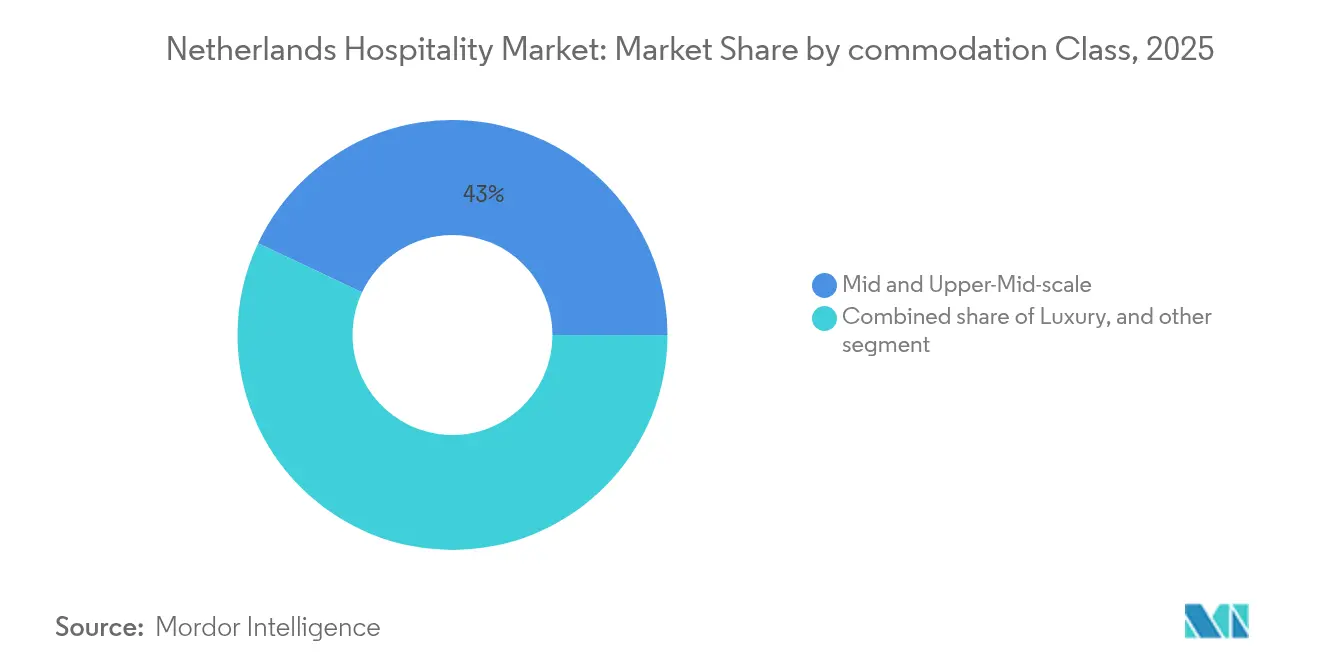

- By accommodation class, Mid & Upper-Mid-scale accounted for 42.98% of the Netherlands hospitality market size in 2025, while Service Apartments are forecast to post a 6.85% CAGR to 2031.

- By booking channel, Direct Digital controlled 56.51% of of the Netherlands hospitality market share in 2025 and is expected to expand at a 7.25% CAGR through 2031.

- By geography, North Holland led with 28.43% of the Netherlands hospitality industry share in 2025; Utrecht is projected to record the fastest provincial CAGR at 4.12% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Amsterdam’s Global Urban Tourism Ecosystem Supporting Hospitality Demand | +1.2% | Urban gateway Amsterdam, with spillover into Haarlem, Zaandam, and Almere as overflow accommodation corridors | Short term (≤ 2 years) |

| Growth of Flexible Stay Models Driven by Changing Workforce Mobility | +0.7% | Business and tech corridors in Amsterdam Zuidas, Rotterdam, Eindhoven, and Utrecht central district office clusters | Medium term (2–4 years) |

| Expansion of Secondary City Tourism Across Dutch Regions | +0.6% | Emerging destination clusters in Utrecht, Leiden, Maastricht, Groningen, and Arnhem regional cultural and university cities | Medium term (2–4 years) |

| Digital-First Consumer Environment Accelerating Smart Hospitality Adoption | +0.5% | Tech-forward markets Amsterdam, Eindhoven, and Delft, with phased roll-out to secondary operators via cloud PMS platforms | Medium term (2–4 years) |

| Waterfront and Urban Regeneration Projects Creating New Hospitality Assets | +0.8% | Regeneration zones in Rotterdam Waterfront, Amsterdam Noord, The Hague Kust, and IJmeer waterfront corridors | Long term (≥ 4 years) |

| Strong Domestic Short-Break Culture Supporting Regional Accommodation | +0.4% | Leisure clusters in Veluwe, Zeeland coastal resorts, North Sea dune villages, and Limburg hill country retreats | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Amsterdam's Global Urban Tourism Ecosystem Supporting Hospitality Demand

Amsterdam remains the main demand engine of the Netherlands hospitality sector. The city is projected to record 23.7 million overnight stays by tourists in 2025 across hotels, campsites, bed-and-breakfasts, and privately rented dwellings, exceeding the municipality’s 20 million ceiling and marking another annual record. Guest volume is expected to reach 9.5 million in 2025, up 2% from 2024, supported by 544 hotels with about 41,000 rooms and 92,000 sleeping places. The Netherlands recorded 26 million international arrivals in 2024, with inbound spending of USD 23.1 billion, and Amsterdam accounted for the largest share. Key source markets included Germany, the United Kingdom, Belgium, and the United States. Cultural assets, business travel, and congress demand supported peak hotel occupancy above 85%. O&S projects business hotel overnight stays at 6.9-7.7 million annually by 2026, and total overnight stays at 25.0-29.4 million by 2028.[2]NL Times, “Amsterdam Tourism Hits Record 23.7 Million Overnight Stays Despite City Tourism Cap."

Growth of Flexible Stay Models Driven by Changing Workforce Mobility

The Netherlands is an active European market for flexible and extended-stay hospitality, supported by demand from corporate headquarters, project teams, expat workers, and mobile labor within the European Union. Savills reports rising 7–12-night stays and fewer sub-7-night stays as remote and hybrid work expands work-travel demand. The planned VAT increase on short-stay accommodation from 9% to 21%, effective January 1, 2026, is set to raise 30–90-day housing costs and support a shift toward serviced apartment contracts[3]Graebel, “Netherlands to Raise VAT on Short-Stay Accommodation: Why This Matters.” . Operators are expanding workforce-focused models, including Makerstoren in Amsterdam, The Stay near Eindhoven, and FlexStay/HomeFlex for groups of up to 200 workers. MDPI research notes municipal short-stay zones of 7 days to 6 months for logistics, agriculture, manufacturing, and technology workers, strengthening institutional demand beyond leisure tourism.

Expansion of Secondary City Tourism Across Dutch Regions

Secondary Dutch cities are gaining hospitality demand as visitor redistribution policies, better accessibility, and distinct urban identities draw travelers beyond Amsterdam. Rotterdam is expected to show the strongest structured growth, with hotel overnight stays reaching 3.2 million in 2025 (+5% year-on-year), overnight guests rising to 1.81 million (+2.4%), and MICE demand recovering to 1 million overnight stays (+25%). Eindhoven Airport is expected to handle nearly 7 million passengers in 2025, supporting business and leisure demand. Amsterdam’s 33.5% hotel tax, effective from January 2026, is expected to shift price-sensitive demand to Rotterdam, Utrecht, and The Hague. Flevoland, Groningen, and Friesland are expected to lead provincial international overnight-stay growth. [4]The Dutch Daily, “Amsterdam Accommodation Tax 2026: VAT Doubles to 21%.”

Digital-First Consumer Environment Accelerating Smart Hospitality Adoption

The Netherlands remains one of Europe’s most digitally advanced economies, and its hospitality market is adopting smart technology due to labor shortages, higher wages, and demand for app-based guest services. Hotelschool The Hague’s 2026 Outlook Paper notes that about one in ten Dutch hospitality firms uses AI structurally, compared with broader Dutch businesses, where AI users generate half of total turnover. In hospitality, AI users generate only a quarter of turnover, showing efficiency gaps and competitive risk from OTAs and booking platforms. Valk Exclusief selected Apaleo in September 2024 to replace legacy systems, went live with its first 10 champion hotels in October 2025, and plans to migrate all 43 properties by December 2025, reducing onboarding time for over 4,000 employees. Straiv’s April 2026 Dutch expansion may accelerate the adoption of the digital guest journey.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Restrictions on Tourism Growth in High-Density Cities | −0.9% | Overtourism-constrained zones in Amsterdam city centre, extending to Utrecht and Rotterdam historic districts | Short term (≤ 2 years) |

| High Real Estate Costs and Limited Availability of Development Sites | −0.7% | Premium land-constrained markets in Amsterdam, The Hague, and Rotterdam, spreading to Eindhoven and Utrecht | Medium term (2–4 years) |

| Labor Shortages Affecting Hospitality Service Quality and Operating Efficiency | −0.6% | Sector-wide in Amsterdam, Rotterdam, and Maastricht, with acute gaps in front-of-house and culinary roles | Medium term (2–4 years) |

| Exposure to International Travel and Economic Cycles | −0.5% | High-dependency international markets in Amsterdam Schiphol gateway, Rotterdam port tourism, and Maastricht corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Restrictions on Tourism Growth in High-Density Cities

Amsterdam’s regulatory framework restricts hospitality growth through overlapping rules that limit new supply, cap demand, and raise operator costs. The Hotelbeleid introduced a city-wide “hotel bed stops,” prohibiting new hotel construction and bed-count expansions across the municipality, except under a “new-for-old” rule requiring an equivalent hotel closure, a minimum four-star standard, and municipal approval. The Tourism in Balance ordinance caps tourists' overnight stays at 20 million, but stays exceeded that limit, triggering legal action and investor uncertainty. Fiscal pressure also increased as the national accommodation VAT rose from 9% to 21%, alongside Amsterdam’s 12.5% tourist tax, with planned increases to 16% and later 20%. HVS reported limited annual supply growth, while Cushman & Wakefield described the investment market as cautious.

High Real Estate Costs and Limited Availability of Development Sites

The Netherlands faces a structural mismatch between real estate demand and development supply. New-build properties account for only 10–15% of residential listings, as construction has lagged due to permit delays, land scarcity, and rising costs. This constraint affects hospitality development, where residential, commercial, office, and hotel use compete for urban sites. A boutique hotel in Rotterdam has an estimated 2026 startup cost of USD 855,570, driven by high land values, strict building codes, energy compliance, and labor costs. CBRE report says that room rates fell nearly 2%, while occupancy rose from 72.6% to 73.4%, compressing RevPAR and margins as personnel costs rose 11%. Planning delays and limited hotel sites continue to restrict new supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Chain Consolidation Accelerates Market Share Gains

Independent Hotels commanded 63.65% revenue in 2025, illustrating a still-fragmented heritage within the Netherlands hospitality market despite above-average chain penetration. Chain Hotels, however, are projected to expand at a 4.64% CAGR to 2031 as operators capitalize on central procurement, brand recognition, and sophisticated demand-forecasting systems. This consolidation trend lifted the Netherlands hospitality market size for chain properties, enabling better labor scheduling and multi-property cross-selling that cushions the impact of wage inflation. Asset-light management contracts remain the preferred growth vehicle, letting owners tap global distribution without relinquishing property ownership. Independent operators, particularly family-run inns and small boutique hotels, are increasingly pursuing soft-brand affiliations to access loyalty programs while preserving unique guest experiences. Transaction volume rose to EUR 931 million (USD 1.03 billion) in 2024, up from EUR 185 million (USD 201.65 million) in 2023, underscoring investor appetite for Dutch stock with stable cash flows and favorable exit scenarios.

The Netherlands hospitality market shows chains focusing expansion on secondary nodes such as Eindhoven, Arnhem, and Leeuwarden, where supply pipelines remain thin and land-use rules are less restrictive. Van der Valk’s purchase of the former NH Waalwijk and CitizenM’s exploration of a EUR 4 billion (USD 4.36 billion) equity event highlight how local and international investors perceive upside in scaling proven Dutch brands. Independent owners unable to finance energy-efficiency upgrades mandated by EU taxonomy are opting for strategic sales, joint ventures, or franchise conversions, likely pushing chain penetration further above 65% by decade-close. Greater consolidation also dilutes OTA bargaining power, as multi-property groups negotiate commission caps and preferential listing positions.

By Accommodation Class: Service Apartments Capitalize on Extended-Stay Demand

Mid & Upper-Mid-scale rooms captured 42.98% share of spending in 2025 thanks to a balanced value proposition appealing to both business and leisure segments. Luxury properties, although smaller in volume, enjoy strong pricing power as high-net-worth visitors resume long-haul trips and diplomatic missions convene in The Hague. The Netherlands hospitality market size for Service Apartments is set to expand at 6.85% CAGR, the highest among classes, driven by multinationals relocating talent into cities where housing shortages persist. Dublin-based Staycity and Dutch newcomer The Student Hotel are prototyping hybrid lodgings combining private studios with communal work lounges, thereby extracting higher revenue per square meter.

Service Apartments benefit from a longer average length of stay, often beyond 14 nights, smoothing revenue seasonality and lowering distribution costs. HVS forecasts more than 12,600 new extended-stay keys across Europe by 2028, with Amsterdam and Rotterdam ranking among the top targets Developers capitalize on office-to-hospitality conversions enabled by remote-work-driven vacancies, while institutional capital favors the predictable cash flows and reduced turnaround costs relative to transient-stay hotels.

By Booking Channel: Direct Digital Dominance Reshapes Distribution

Direct Digital streams held 56.51% of turnover in 2025 and remain the fastest-rising channel at 7.25% CAGR through 2031, reflecting a conscious effort by hoteliers to reclaim pricing autonomy. Rate-parity relaxation catalyzes meta-search advertising, loyalty-member pricing, and ancillary upselling that collectively widen contribution margins. The Netherlands hospitality market share held by OTAs is expected to erode incrementally as hotels reinvest commission savings into user-experience enhancements, such as instant messaging and embedded payment gateways.

Wholesale and traditional agents retain relevance for large tour groups and inbound markets with limited online penetration, while Corporate/MICE portals gain traction via consolidated travel-management platforms. Nonetheless, Booking Holdings’ EU gatekeeper status ensures it remains a dominant traffic generator, compelling hotels to pursue a balanced mix that hedges algorithmic risk. Properties lacking marketing analytics face higher customer-acquisition costs, reinforcing the advantage of chain affiliation or tech-savvy boutique clusters that share centralized e-commerce functions.

Geography Analysis

North Holland remains the epicenter of the Netherlands' hospitality market, generating 28.43% of 2025 market size. Amsterdam’s average daily rate reached EUR 205 (USD 227) per room despite tight supply growth arising from a municipal moratorium that demands a one-in, one-out approach to new hotel openings. Schiphol’s gradual capacity restoration, coupled with KLM’s resumed long-haul network, sustains robust international traffic even as the airport explores flight-cap caps to mitigate noise.

Utrecht’s strategic location between Amsterdam and the German border, combined with a 24.1% jump in B&B registrations, positions the province as the fastest-growing hospitality locale. The construction of 63,000-75,000 new homes by 2035 is projected to amplify business-related lodging demand, particularly for extended-stay formats that accommodate project teams during build-outs. South Holland leverages Rotterdam’s port activity, generating resilient weekday occupancy, while The Hague’s concentration of embassies and the International Court of Justice underpins a stable calendar of diplomatic events.

Peripheral provinces pursue distinctive value propositions: Groningen markets its Hanseatic heritage and university conferences, Friesland positions nautical tourism around the Wadden Sea, and Zeeland aligns with coastline wellness retreats. Provincial tourism boards coordinate multi-region itineraries to lengthen average trip duration, leveraging the nation’s high-speed rail to bundle Amsterdam city breaks with countryside experiences. Overijssel’s 3% dip in 2024 highlights uneven recovery, prompting targeted campaigns on cycling trails and rural gastronomy to revive visitation.

Competitive Landscape

The Netherlands hospitality market demonstrates moderate fragmentation, with the operators creating a competitive yet accessible landscape. While large chains benefit from scale advantages, operational efficiencies, and brand recognition, there is still space for niche-focused and entrepreneurial players to thrive. The market is led by a prominent family-owned chain with a widespread national footprint, while another key competitor has built a robust leisure-focused network across over 100 locations. These domestic leaders have established strong customer loyalty through consistent service delivery and strategic positioning. Their success underscores the viability of both scale and specialization in a market that rewards operational agility.

Leading operators are leveraging advanced technologies, including revenue management systems, contactless guest experiences, and predictive maintenance, to address labor shortages and enhance profitability. In contrast, independent hotels are carving out distinct identities through boutique design, locally sourced dining, and curated partnerships with regional artisans and businesses. These experiential strategies help maintain premium pricing in a market increasingly drawn to authentic, personalized stays. In 2024, the hotel investment pipeline reached approximately USD 1 billion, reflecting sustained investor confidence. The year’s largest portfolio deal was marked by a USD 392 million transaction involving a major urban hotel group, reinforcing appetite for Dutch hospitality assets.

New market entrants are introducing fresh models, such as tech-enabled operators offering AI-powered dynamic pricing for small hotel clusters, and hybrid serviced-apartment brands that integrate co-living and coworking amenities. These disruptors are redefining traditional hospitality formats and responding to evolving guest expectations around flexibility and community. Meanwhile, tightening environmental regulations particularly nitrogen emissions and energy efficiency standards are reshaping development and renovation priorities. Well-capitalized operators with the means to invest in sustainable retrofits are gaining an advantage, while green-focused investors are actively targeting underperforming assets for redevelopment. As the regulatory and consumer landscape evolves, the Dutch hospitality sector is positioned for innovation-led growth, where sustainability, technology, and guest experience will define competitive advantage.

Netherlands Hospitality Industry Leaders

Van der Valk Hotels & Restaurants

NH Hotel Group

Accor SA

Marriott International Inc.

Hilton Worldwide Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Fattal Hotel Group completed a EUR 360 million (USD 392.4 million) purchase of 12 Eden Hotels, cementing Leonardo Hotels as a major domestic player.

- February 2025: Wyndham partnered with HR Group to open 25 Trademark Collection and Vienna House Easy hotels across the Netherlands, Germany, and Austria.

- November 2024: The Digital Markets Act (DMA) designation for Booking Holdings, specifically concerning its online travel service, became enforceable, requiring Booking.com to comply with the DMA's regulations, including the prohibition of rate-parity clauses.

- July 2024: Minor Hotels debuted the 163-room Avani Museum Quarter Amsterdam, expanding its European footprint.

Netherlands Hospitality Market Report Scope

The hospitality industry is a broad category of fields within the service industry that includes lodging, food and beverage service, event planning, theme parks, travel agencies, tourism, hotels, restaurants, and bars. A complete background analysis of the hospitality industry in the Netherlands, which includes an assessment of the industry associations, overall economy, emerging market trends by segments, significant changes in the market dynamics, and market overview, is covered in the report.

The hospitality industry in the Netherlands is segmented by type (chain hotels, independent hotels) and by segment (service apartments, budget, and economy hotels, mid and upper mid scale hotels, and luxury hotels).

The report offers market size and forecasts for the hospitality industry in the Netherlands in value (USD) for all the above segments.

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| North Holland |

| South Holland |

| Utrecht |

| North Brabant |

| Rest of Netherlands |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | North Holland |

| South Holland | |

| Utrecht | |

| North Brabant | |

| Rest of Netherlands |

Key Questions Answered in the Report

What is the projected value of the Netherlands hospitality market in 2031?

It is expected to reach USD 32.26 billion, reflecting a 3.88% CAGR from 2026.

Which accommodation class is growing fastest?

Service Apartments lead with a 6.85% CAGR forecast through 2031, driven by extended-stay demand

How will the 2026 VAT increase impact Dutch hotels?

The hike from 9% to 21% may pull bookings forward into 2025 and could depress demand once implemented.

Why are direct digital bookings rising?

The EU Digital Markets Act removed rate-parity clauses, allowing hotels to offer better prices on their own channels.

Which province is forecast to grow the quickest in hotel revenue?

Utrecht, at an expected 4.12% CAGR through 2031, benefits from infrastructure expansion and central positioning.

How concentrated is ownership within Dutch hospitality?

Five leading chains control about 45% of rooms, yielding a market concentration score of 6 on a 10-point scale.

Page last updated on: