Tunisia Grain Market Analysis by Mordor Intelligence

The Tunisia Grain Market size is expected to grow from USD 1.5 billion in 2025 to USD 1.56 billion in 2026 and is forecast to reach USD 1.87 billion by 2031 at 3.78% CAGR over 2026-2031. The market expansion is driven by increased demand for food staples, feed grains, and vegetable oils, combined with policy reforms focusing on domestic production, import diversification, and storage capacity enhancement. Infrastructure improvements, including new coastal silos and port handling systems, reduced delivery time and post-harvest losses. The market has also benefited from a revised tender strategy emphasizing bilateral agreements, which has reduced procurement risks. Government interventions have protected against climate-related challenges, particularly in the cereals segment. According to the USDA Grain and Feed Annual Report 2025, the Cereal Board of Tunisia maintains exclusive control over wheat and wheat product imports and exports. The board directs all wheat tenders for domestic consumption, with the government subsidizing imported wheat prices and covering price differentials. Despite its impact on Tunisia's budget, the wheat subsidy program is anticipated to continue without changes or import reductions.

Key Report Takeaways

- Cereals accounted for 87.65% of Tunisia's grain market production. The oilseeds segment is anticipated to grow at a CAGR of 6.52% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Tunisia Grain Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Investments in Infrastructure and Modernization | +1.2% | Rades, Sousse, Sfax | Medium term (2-4 years) |

| Rising Barley Demand for Animal Feed and Beer Production | +0.8% | Livestock clusters nationwide | Short term (≤2 years) |

| Favoring Government Policies Supporting the Market | +0.9% | National | Medium term (2-4 years) |

| Adoption of salt-tolerant durum wheat cultivars | +1.1% | Southern Coast of the Mediterranean Sea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Investments in Infrastructure and Modernization

The Tunisian Cereals Office plans to expand grain storage capacity by 120,000 metric tons in 2025, distributed across Rades (40,000 metric tons), Sousse (58,000 metric tons), and Sfax (38,000 metric tons). The office will simultaneously renovate existing silos to maintain a stable grain supply. The new storage facilities require TND 205 million (USD 66.6 million), while silo renovations will cost TND 143 million (USD 44.5 million). The construction contracts specify modular steel designs for rapid assembly and reduced maintenance in port areas with high salinity. These infrastructure improvements enhance Tunisia's food security and increase the grain sector's resilience to climate and economic challenges.

Rising Barley Demand for Animal Feed and Beer Production

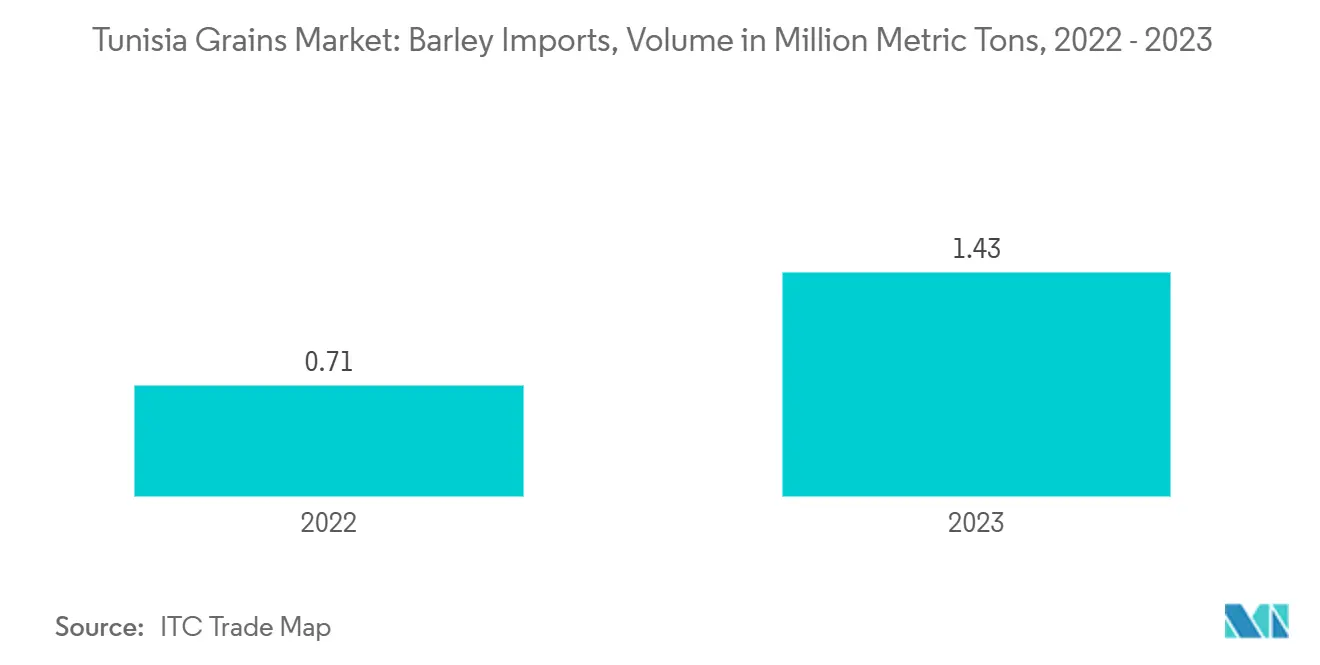

Barley serves as a secondary cereal crop in Tunisia, primarily supporting the livestock feed sector. While produced in lower volumes than wheat, it mainly serves as a feed grain for ruminants and livestock, with a small portion used in malt production for brewing. Tunisia's barley seeded area increased to 412,000 ha from 395,000 ha in Marketing Year 2024-2025[1]Ministry of Agriculture and Farmer Associations, while the USDA report 2025 forecasts consumption in MY 2025-2026 at 940,000 metric tons, maintaining an average growth rate of approximately two percent. The grain is predominantly used in feedlots and as supplemental feed, particularly in areas with stressed rangelands. The brewing industry's demand has contributed to increased barley imports, with ITC Trade Map data showing import volume reaching 1.43 million metric tons in 2023, a 99% increase from the previous year's 0.71 million. Tunisia has implemented import liberalization following a successful trial period in the market year 2023-2024, reducing state budget expenditure and aligning with recommendations from international institutions and donors, marking a transition from the Office des Céréales (Cereal Board) monopoly to private sector participation in barley imports.

Favoring Government Policies Supporting the Market

The government of Tunisia is supporting the grains sector by collaborating with international organizations. The World Bank provided a USD 300 million loan for the Emergency Food Security Response Project to support certified seed distribution, input vouchers, and direct income transfers in place of blanket subsidies.[2]World Bank The Ministry of Agriculture allocated TND 2,400 million (USD 760 million) for grain purchases in 2024-2025, enabling cooperatives to offer competitive prices to farmers and encourage increased planting. The Office des Céréales implemented e-procurement systems to improve transparency and reduce administrative processing times. These combined measures have strengthened farmer confidence, leading to increased cultivation area despite weather uncertainties.

Adoption of Salt-tolerant Durum Wheat Cultivars

Tunisia's grain market is experiencing growth through the adoption of salt-tolerant durum wheat cultivars, which enable farmers to maintain stable yields in saline soil conditions. The National Agronomic Research Institute of Tunisia (INRAT) has identified high-performing Tunisian wheat varieties with enhanced salt tolerance through agro-physiological screening and genetic introgression. The incorporation of Nax genes has improved durum wheat grain yield in saline soils by reducing sodium accumulation in leaves. This development is essential for Tunisia, where soil salinity affects more than 10% of arable land and restricts conventional wheat cultivation. The implementation of salt-tolerant cultivars allows farmers to expand wheat production into previously unviable areas, reducing import dependency and enhancing food security. These improvements strengthen the sustainability and resilience of Tunisia's grain market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevelance of Drought Conditions | -0.7% | Central and southern regions | Long term (≥4 years) |

| Unavailability of proper Storage and Transportation Facilities | -0.5% | Rural interior | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prevalence of Drought Conditions

Tunisia's grain market faces significant constraints due to drought conditions that affect crop yields, water availability, and food security. The country has experienced three consecutive years of drought, causing reservoir levels to fall to 25% of capacity and requiring water rationing by authorities. Grain harvests have decreased by 60%, with domestic production falling to 250,000 metric tons. The combination of high input costs, crop failures, and limited irrigation has forced farmers to increase grain imports from Ukraine and Romania. Climate models project a long-term rainfall reduction of up to 15%, indicating a continued reliance on imports of approximately 30% even during favorable growing seasons. While the implementation of water-efficient drip irrigation systems and drought-tolerant seed multiplication programs is increasing, their adoption rate remains insufficient to address the current climate challenges.

Unavailability of Proper Storage and Transportation Facilities

Tunisia's grain market faces significant constraints due to inadequate storage and transportation infrastructure, resulting in post-harvest losses, supply chain inefficiencies, and increased import dependency. The market experiences post-harvest losses of 10-15%, which negatively impact farmer incomes and increase import costs. The current silo network capacity of 508,000 metric tons falls short by 300,000 metric tons, necessitating open-air storage that increases the risk of aflatoxin contamination. Small-scale farmers in interior regions must transport grain over 150 km on poor-quality roads to reach certified elevators, incurring additional transportation costs. While there are plans to expand storage capacity by 120,000 metric tons, this addresses only 40% of the current deficit. According to World Bank analysis, resolving these storage constraints could reduce annual wheat import volumes by 7-10%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Tunisia's grain market operates within its Mediterranean climate, which supports wheat, barley, and pulses production while facing challenges from frequent droughts and water scarcity. The country's primary grain-producing regions are in the north and coastal areas, particularly Bizerte, Beja, and Jendouba, which benefit from higher rainfall and fertile soils. The central and southern regions, including Sfax and Gabes, experience arid conditions that limit grain cultivation and necessitate increased imports from Ukraine, Romania, and Russia.

Imports constitute a fundamental component of Tunisia's grain market. In 2024, wheat and barley imports reached USD 1.1 billion, accounting for approximately 10% of total merchandise imports. The import composition has evolved, with Russian volumes increasing to 1.1 million metric tons in 2023, while French shipments decreased due to shifting price benchmarks. The Office des Céréales implements staggered cargo scheduling to prevent freight congestion and storage overflow at Rades port, Tunisia's main grain entry point. The 2024 bilateral protocols establish quality and phytosanitary standards, enhancing supply chain efficiency.

Tunisia’s port-logistics revamp aims to raise berth productivity from 12 to 18 ships per month, matching peers and safeguarding Tunisia's grain market share in regional trans-shipment. Knowledge-exchange missions to Italian and Spanish ports feed into master-plan updates that envisage bonded warehousing zones, potentially repositioning Tunisia as a value-added milling and re-export hub.

Regulatory Landscape

Tunisia's grain market operates under strong state oversight led by the Office des Cereales (Office des Céréales), which, per USDA reporting, maintains exclusive control over wheat and wheat product imports and exports and manages official tenders for domestic supply. Annual decrees set farm-gate prices and define payment, storage, and retrocession modalities for each campaign, including Decret n 2025-344 (July 11, 2025) for the 2025-2026 campaign and Decret n 2024-545 (November 7, 2024) for the 2024-2025 campaign, anchoring procurement, collection incentives, and regulated handling terms.

Processing and quality controls are reinforced through product and milling specifications set by government instruments. A joint ministerial order dated April 2, 2026, issued by the Ministry of Agriculture and the Ministry of Commerce, sets extraction rates for flour and semolina, affecting millers and durum and soft wheat value realization in regulated channels. On the trade side, wheat tenders remain channeled through the Office des Cereales with supplier approval and registration requirements, while barley import liberalization creates a parallel route for private-sector participation, distinguishing the regulatory path by commodity.

Value Chain Analysis

Tunisia's grain value chain starts with input supply (certified seed, fertilizers, and crop protection), followed by farm production concentrated in higher-rainfall northern and coastal zones, and then moves through regulated collection and storage before milling, feed manufacturing, crushing (oilseeds), and distribution into retail and institutional channels. The Office des Cereales plays a central role across wheat procurement and supply management, including import tendering, port logistics coordination, and distribution, while domestic collection is handled through a mix of official and private operators (including private collectors and Agricultural Services Mutual Societies across multiple governorates), linking farms to certified elevators and downstream users.

Imports remain a structural component of the chain, with ports, notably Rades, serving as key entry points for wheat and barley, supported by road and rail distribution to inland consumption centers. Storage and transport bottlenecks continue to affect quality and post-harvest losses, underpinning the focus on new coastal silo capacity at Rades, Sousse, and Sfax and the renovation of existing facilities. Policy-driven liberalization has also reshaped the chain in barley, where private importers complement the state channel, while wheat stays centralized through Office des Cereales tenders and regulated pricing mechanisms.

Market Opportunities and Future Outlook

Infrastructure and quality-assurance upgrades create near-term opportunity across storage, handling, and compliance, especially in light of the documented storage deficit and World Bank-cited loss reduction potential. The Office des Cereales investment program to add 120,000 metric tons of port-area storage at Rades, Sousse, and Sfax (TND 205 million) and renovate existing silos supports modular silo construction, port handling systems, and maintenance services in high-salinity coastal environments. These improvements also strengthen the ability to manage staggered cargo scheduling and reduce congestion. Alongside physical work, Office des Cereales efforts toward e-procurement and wider supply-chain digitalization increase demand for traceability, warehouse management, and data integration across collection centers and port-to-silo flows.

Regulatory and program activity also points to opportunity around standardized milling outputs and testing capacity. The April 2, 2026, joint ministerial order setting flour and semolina extraction rates increases the emphasis on process control and quality consistency for millers operating within regulated channels. In parallel, Office des Cereales workstreams to establish and control new laboratory capabilities, including missions tied to labs in Beja and Sfax and a central analysis lab in Tunis, support demand for grain testing equipment, aflatoxin and quality analytics, and certification services. On the supply side, adoption of salt-tolerant durum wheat cultivars developed by INRAT supports demand for certified seed multiplication and distribution programs that connect research outputs with commercial planting in saline-affected areas.

Recent Industry Developments

- June 2026: Bunge was reported to have secured an Office des Cereales contract to supply 75,000 metric tons of milling wheat via a tender. The purchase reinforced Tunisia's use of competitive international procurement to manage staple supply, while concentrating near-term volumes through approved suppliers that can meet quality and delivery requirements.

- March 2025: Tunisia confirmed an investment of TND 205 million to construct 120,000 metric tons of new grain silos across Rades, Sousse, and Sfax, with completion targeted by 2027. The project supports tighter port-to-storage integration and addresses structural storage gaps that contribute to losses and quality risks.

- March 2024: The World Bank approved a USD 300 million top-up for Tunisia's Emergency Food Security Response Project, supporting access to certified seed and inputs for the 2024-2025 season. The financing strengthened the policy shift toward targeted support tools and helped stabilize farmer participation in cereal planting amid drought-related stress.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Tunisia grain market is defined as the value of grains at the first commercial handoff within Tunisia, covering locally produced and imported volumes that go into food, feed, and industrial use.

Scope exclusions: Excludes ready-to-eat breakfast cereals, brewery malt extracts, and grain-based beverages.

Segmentation Overview

- Cereals

- Production Analysis (Volume)

- Consumption Analysis (Volume and Value)

- Import Market Analysis (Volume and Value)

- Export Market Analysis (Volume and Value)

- Price Trend Analysis

- Pulses

- Production Analysis (Volume)

- Consumption Analysis (Volume and Value)

- Import Market Analysis (Volume and Value)

- Export Market Analysis (Volume and Value)

- Price Trend Analysis

- Oilseeds

- Production Analysis (Volume)

- Consumption Analysis (Volume and Value)

- Import Market Analysis (Volume and Value)

- Export Market Analysis (Volume and Value)

- Price Trend Analysis

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a fact base for Tunisia grain supply, demand, and trade, and then aligning definitions so the model stays consistent year to year. Public sources helped us map production, harvested area, yields, and official procurement signals, which are the practical anchors for a grains market.

Sources used include official and non-paywalled references such as FAOSTAT for crop production series, USDA FAS Grain and Feed updates for marketing-year balance sheets, UN Comtrade for import and export flows, and Tunisia government statistics and agriculture ministry releases for local crop outlooks and policy actions. We also reviewed customs and port related press releases, company filings and investor presentations where available, and reputable news for shipment timing and price direction. In parallel, we used approved paid subscriptions for company financials and intelligence, news and financials, import and export shipment-level checks, and patent databases to sense storage, handling, and processing investments. These examples are indicative, and many other sources were also consulted to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on validating how volumes move through state procurement, private trade, and milling channels, and on stress-testing the price and margin assumptions that link tons to USD. We spoke with a mix of importers, grain handlers, millers, distributors, and sector advisors, and the discussions were used to reconcile desk-based signals with on-the-ground seasonality, quality specs, and tender behavior inside Tunisia.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 16% | APAC: 40% |

| Mid tier: 49% | Functional/Unit leaders: 29% | EMEA: 33% |

| Smaller Players: 22% | Managers: 55% | Americas: 27% |

Market-Sizing & Forecasting

Sizing follows a top-down build that reconstructs the demand pool from Tunisia-specific production and trade data, and then converts it into market value using observed price and mix patterns across key grains. Where it helped, the totals were corroborated using selective bottom-up approximations, such as sampled importer and miller volume checks and an average price per ton applied to validated tonnage bands.

Inputs used in the model include domestic production volumes by crop, harvested area and yield trends, import volumes and origin mix, tender and procurement cadence, and local price movements for key grains (all of which influence the USD conversion and year-to-year variance). We also tracked the share of imported supply in total availability, because Tunisia can swing between seasons depending on rainfall and policy actions. For forecasting, scenario analysis was used so that yield outcomes, import needs, and price paths can be flexed in a transparent way, and then aligned with what interviewees saw as the most likely planning case. When data gaps appeared in smaller crop lines, proxying was done through trade-based volumes and conservative pricing rules, followed by a reasonableness check against total grain availability.

Data Validation & Update Cycle

Outputs are checked through triangulation across production, trade, and consumption signals, and then reviewed for spikes that do not match known harvest or import events. Variance checks are run at the grain-type level before totals are finalized, and any large mismatches trigger a re-check of units, marketing-year timing, and currency assumptions.

Before sign-off, the full model and its assumptions go through multi-step analyst reviews so calculation logic stays repeatable and traceable. The report is refreshed annually, and interim updates are made when material events occur, such as major tender shifts, policy changes, or abnormal harvest outcomes. Right before delivery, a final review pass is completed so clients receive the most current view supported by the latest available indicators.

Mordor Intelligence's Tunisia Grain Market Estimate Compared With Other Published Estimates

Different published estimates for Tunisia grains can look far apart because they may not count the same product forms, they may use different price timing, or they may build value from retail prices instead of first-sale values. Year selection also matters, since harvest variability and import dependence can shift volumes and prices noticeably.

The main gap comes from whether processed grain foods and retail markups are included, where Mordor Intelligence counts unprocessed cereals, pulses, and oilseeds at the first commercial handoff and leaves out ready-to-eat breakfast cereals and grain-based beverages, which lowers the USD total versus broader food baskets.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.50 B (2025) | |

| Regional Consultancy A | USD 1.02 B (2025) | Uses a narrower basket and channel-led splits, and the revenue figure appears to lean toward packaged retail and distribution coverage rather than total grain availability linked to production and imports. |

| Trade Publisher B | USD 1.20 B (2024) | Base year differs and the value build can shift with currency timing and price references, and the scope emphasis appears closer to cereals and wheat-focused dynamics, which can undercount pulses and oilseeds included in the baseline. |

Taken together, the spread is mostly explained by what is counted as grain (unprocessed versus processed foods), which year is used, and how prices are applied to volumes. Using a clear first-sale valuation, then cross-checking volumes against production and import signals, keeps the estimate transparent and easier to replicate when new season data comes in.

Key Questions Answered in the Report

What is the current size of the Tunisia grain market?

The Tunisia grain market stands at USD 1.56 billion in 2026 and is projected to reach USD 1.87 billion by 2031 at a 3.78% CAGR.

Which grain segment dominates domestic consumption?

Cereals, especially wheat, represent 87–88% of total grain value, reflecting their staple role in household diets and bakery channels.

Why is barley becoming more important?

Accelerating feed demand and a growing beer industry have increased barley’s share, while policy liberalization now lets private firms handle imports.

How is Tunisia addressing storage shortfalls?

The government has committed TND 205 million (USD 66.6 million) to build coastal silos adding 120,000 metric tons by 2027 and rehabilitating existing inland facilities.

Page last updated on: