Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

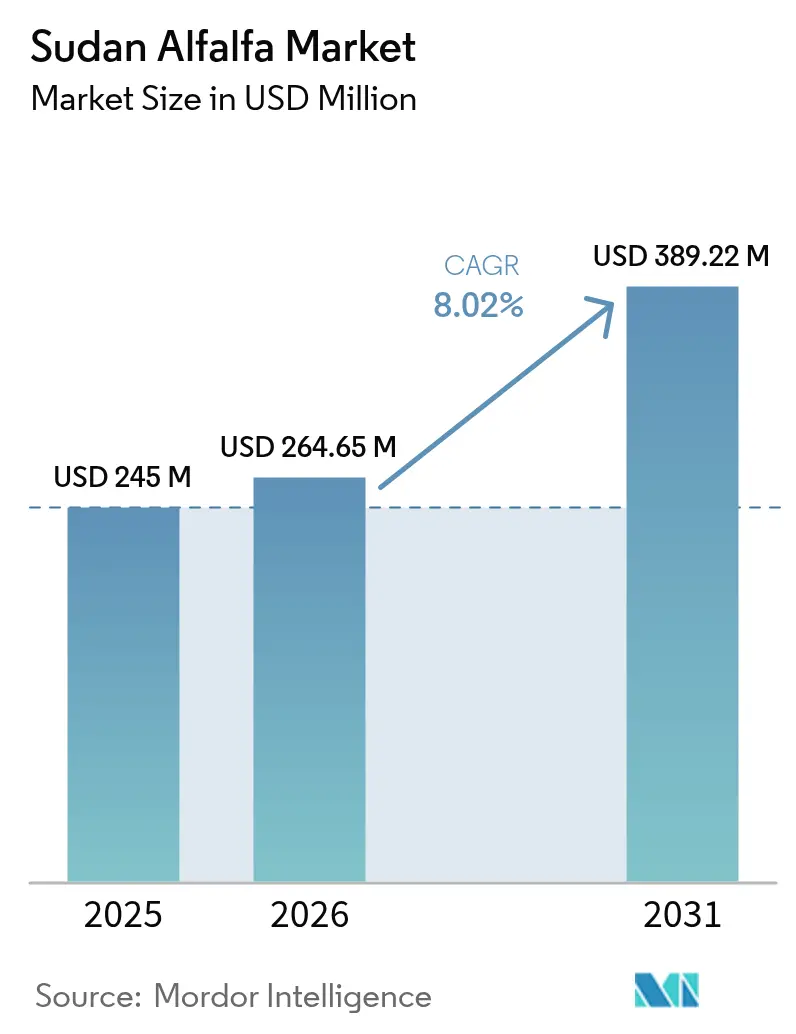

| Base Year Market Size (2025) | USD 245 Million |

| Market Size (2026) | USD 264.65 Million |

| Market Size (2031) | USD 389.22 Million |

| Growth Rate (2026 - 2031) | 8.02% CAGR |

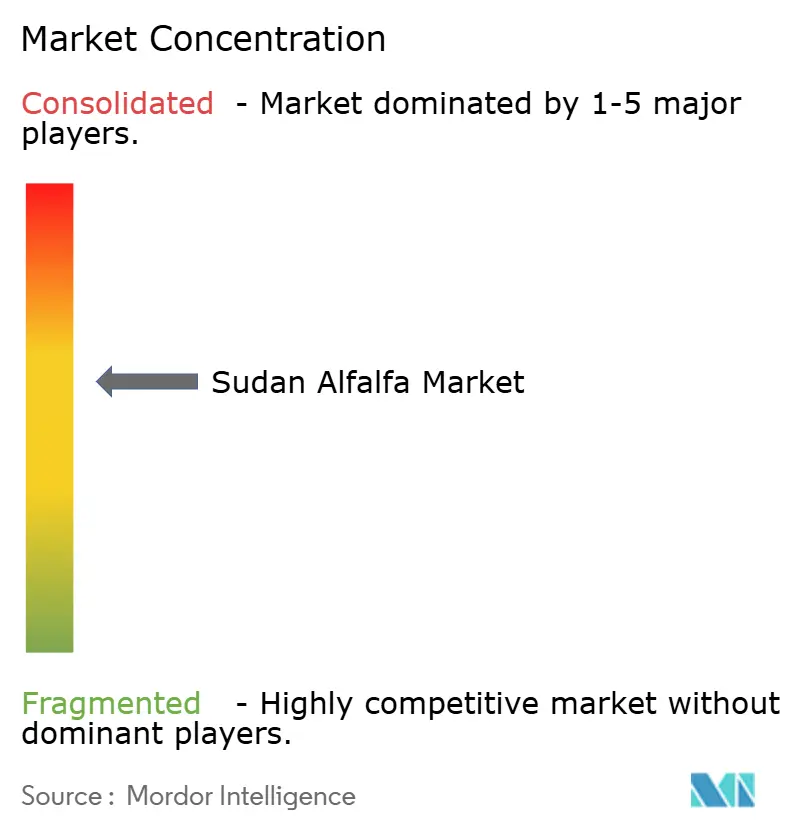

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sudan Alfalfa Market Analysis by Mordor Intelligence

Sudan Alfalfa market size in 2026 is estimated at USD 264.65 million, growing from 2025 value of USD 245 million with 2031 projections showing USD 389.22 million, growing at 8.02% CAGR over 2026-2031. This growth reflects intensifying feed-security initiatives across Gulf Cooperation Council dairy hubs, the gradual rehabilitation of Sudan’s Gezira irrigation network, and recovering container-shipping efficiencies that cut delivered costs to primary importers.[1]Source: Sudan Ministry of Irrigation and Water Resources, “Gezira Rehabilitation Project 2024,” irrigation.gov.sd The Sudan Alfalfa market benefits from government programs that allocate irrigated acreage to export-oriented forage clusters, from seed technology that raises tolerance to saline soils, and from large buyers replacing lower-protein grasses with alfalfa to improve milk yields. Processing investments that convert baled hay into pellets and cubes lift export margins while reducing quality-loss risks. Political instability, hard-currency shortages, and Red Sea freight premiums temper the near-term outlook yet leave the long-run demand trajectory intact as Middle East dairy modernization continues.

Key Report Takeaways

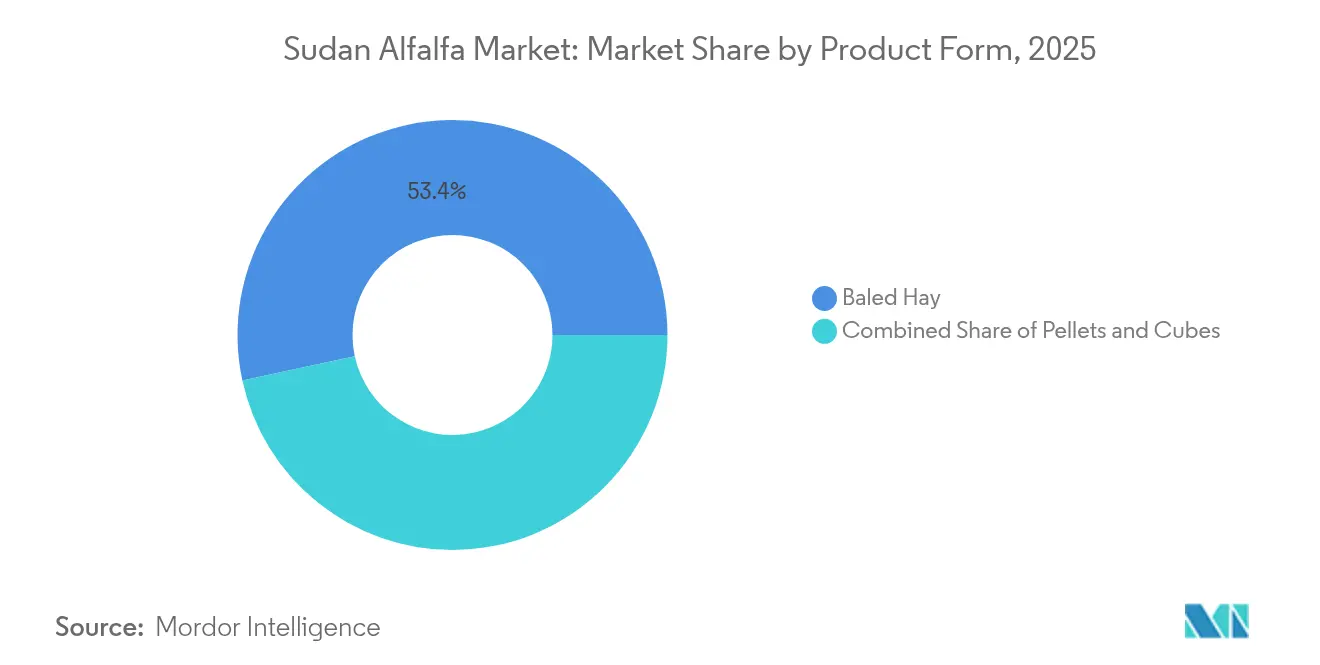

- By product form, baled hay held 53.40% of the Sudan Alfalfa market share in 2025, while pellets are projected to expand at an 11.18% CAGR through 2031.

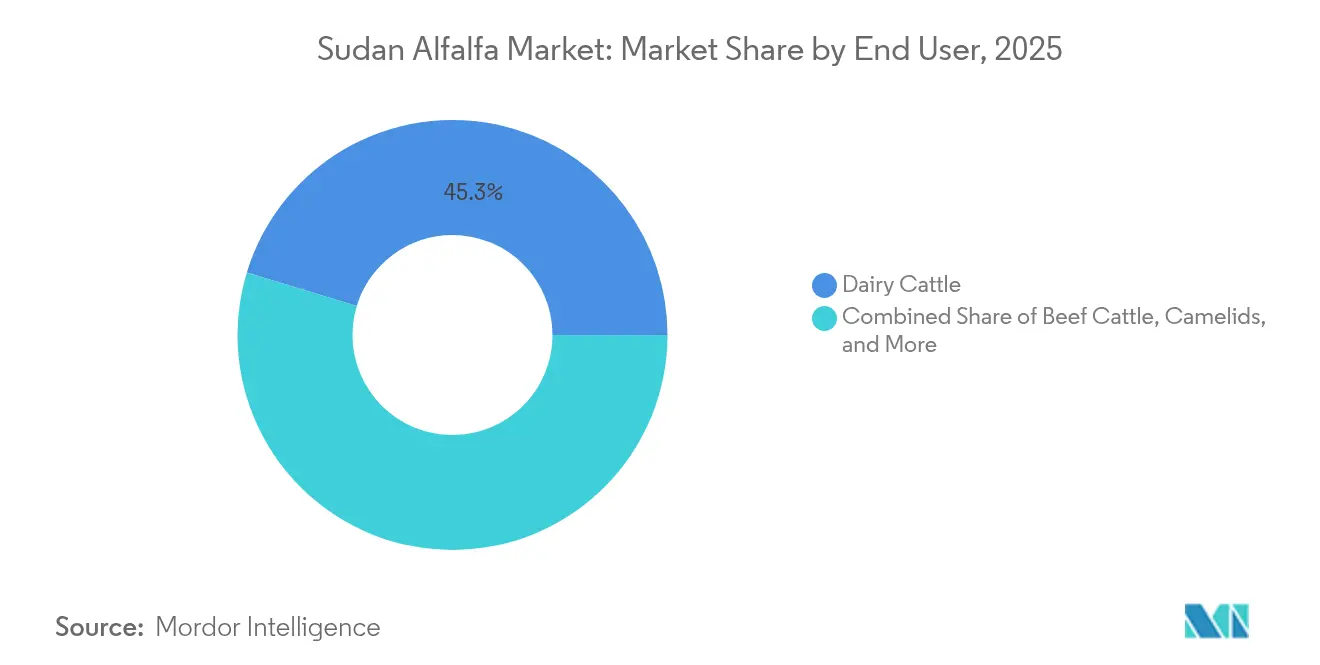

- By end user, dairy cattle commanded a 45.30% share of the Sudan Alfalfa market size in 2025, whereas camelids record the highest projected CAGR at 10.45% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sudan Alfalfa Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising dairy-herd modernization in Middle East markets | +2.1% | Middle East, North Africa | Medium term (2-4 years) |

| Government push for feed self-sufficiency in Sudan | +1.8% | Sudan, Regional spillover to Chad and South Sudan | Long term (≥ 4 years) |

| Recovery of Sudanese river-based irrigation capacity | +1.5% | Sudan (Gezira, White Nile, Blue Nile regions) | Medium term (2-4 years) |

| Containerized shipping cost decline for high-density forages | +1.2% | Global, with strongest impact on Middle East trade routes | Short term (≤ 2 years) |

| Advent of salt-tolerant alfalfa cultivars | +0.9% | Sudan, Egypt, Jordan, other arid regions | Long term (≥ 4 years) |

| Pivot toward climate-smart fodder crops by export buyers | +0.7% | Global, led by European and North American buyers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Dairy-Herd Modernization in Middle East Markets

Mega-dairy operators in Saudi Arabia and the United Arab Emirates increasingly replace Rhodes grass with Sudanese alfalfa to raise milk-solids output and feed efficiency. Contracts linked to Vision 2030 targets guarantee year-round offtake, stabilizing producer cash flow. Camel-milk farms mirror this trend, citing 15% yield gains when diets include high-protein alfalfa. Quality-assurance rules under the Gulf Standards Organization reinforce demand for traceable, pesticide-safe forage. Procurement switches from spot deals to multiyear supply agreements that reward reliable exporters. Forward pricing enables Sudanese processors to hedge freight volatility and plan capacity additions.

Government Push for Feed Self-Sufficiency in Sudan

The Ministry of Agriculture earmarked 150,000 hectares of Nile-irrigated land for forage export hubs, pairing subsidized seed and low-interest credit with streamlined export licensing.[2]Source: Ministry of Agriculture and Forests, “Sudan Forage Export Strategy,” agriculture.gov.sd Targets call for USD 180 million in annual alfalfa export receipts by 2027. Pilot plots show farmers moving acreage away from cotton toward alfalfa for faster cash cycles. Policy success hinges on extension-service reach, yet digital advisory tools lower the training gap. Sudan Alfalfa market participants gain from lower bureaucracy and a clearer investment outlook.

Recovery of Sudanese River-Based Irrigation Capacity

World Bank and African Development Bank funding of USD 400 million restores canal lining, automated gates, and drainage across Gezira, boosting water-delivery efficiency from 35% to 65%.[3]Source: World Bank, “Sudan Agricultural Recovery Project,” worldbank.org Farmers shift from two to four alfalfa cuts per season, raising unit output without extra land. Planned upgrades at Rahad and New Halfa schemes may add 75,000 hectares of reliable production by 2026, directly enlarging the Sudan Alfalfa market size. Training sessions on precision irrigation further lift water-use productivity.

Containerized Shipping Cost Decline For High-Density Forages

Post-pandemic freight rates fell by USD 30 per ton on key Port Sudan to Jebel Ali routes as container availability normalized. Pelletizing raises payload density 40% over baled hay, magnifying freight savings. Port Sudan’s new gantry cranes improve dwell times, though Red Sea insurance surcharges raise total cost by 12%. Exporters lock in rates six months ahead, cutting budget uncertainty. The freight relief accelerates processing investment as exporters chase the pellet premium.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic hard-currency shortages limiting input imports | -1.9% | Sudan, with spillover effects on regional trade | Short term (≤ 2 years) |

| High freight premiums on Red Sea routes | -1.4% | Middle East trade corridors, Red Sea shipping lanes | Medium term (2-4 years) |

| Salinity buildup in Gezira and White Nile irrigation schemes | -1.1% | Sudan (primary irrigation zones) | Long term (≥ 4 years) |

| Rising global interest rates squeezing working-capital access | -0.8% | Global, with acute impact on developing markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Hard-Currency Shortages Limiting Input Imports

Sudan’s parallel-market exchange rate trades at triple the official peg, slashing fertilizer imports by 40% in 2024. Producers pay cash up front in scarce foreign currency, delaying seed and machinery purchases. Lower-grade domestic fertilizer dampens alfalfa protein levels, triggering export-quality downgrades. Development-finance credit lines ease some pressure yet take months to disburse. The constraint stalls processing-plant commissioning as equipment suppliers demand advance dollars.

Salinity Buildup In Gezira And White Nile Irrigation Schemes

Continuous irrigation without adequate drainage raises soil salinity above optimal thresholds, slicing yields 10% in pockets of Gezira despite canal repairs. Subsurface drainage projects require heavy investment and temporarily idle land. Farmers adopt split-irrigation and gypsum amendment, yet long-term remediation is essential for the Sudan Alfalfa market to meet projected volume. Remediation requires significant investment in subsurface drainage systems and periodic flushing operations that temporarily remove land from production. The problem is most acute in the central Gezira region, which represents 35% of Sudan's total alfalfa production capacity. Farmers are adopting salt-tolerant varieties and modified irrigation scheduling to mitigate impacts, but these measures only partially offset yield losses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Processing Innovation Drives Value Addition

Baled hay held 53.40% of the Sudan Alfalfa market share in 2025 as exporters leveraged existing baling infrastructure and established logistics chains. Pellets are forecast to deliver an 11.18% CAGR through 2031, supported by dehydration investments that raise container load factors and extend shelf life. Cubes captured a modest share of the Sudan Alfalfa market size in 2025, appealing to buyers who seek a mid-priced processed option with lower dust levels.

Processors that shift from baling to pelletizing capture value lost to import-country feed mills. Automatic bale-breakers and hammer mills boost throughput and cut manual handling. Quality-assurance sensors verify protein content before compaction, satisfying Gulf regulatory checks. These investments align with buyer preferences for standardized feed that can be dosed in automated dairy mixers, reinforcing the appeal of processed formats.

By End User: Camelids Lead Specialized Feed Demand

Dairy cattle dominated demand with a 45.30% share of the Sudan Alfalfa market size in 2025 as mega-dairies in Saudi Arabia and the United Arab Emirates favored high-protein roughage. Camelids posted the fastest growth at 10.45% CAGR through 2031, driven by commercial camel-milk ventures scaling up across the Gulf.

Sudan Alfalfa market suppliers tailor protein and fiber profiles to exotic feed specifications in camelids, which display improved milk-solid yields on alfalfa-rich diets. Feed integrators incorporate pelleted alfalfa into total-mixed rations that require uniform particle size. Dairy-cattle demand remains resilient as regional herds expand under food-security mandates. In beef-cattle systems, alfalfa serves as a finishing feed that raises average daily gain, though price sensitivity keeps growth moderate. Small-ruminant uptake grows in North African meat chains that recognize alfalfa’s digestibility benefits for fast-turnover lamb.

Geography Analysis

Central Gezira accounts for the majority of the Sudan Alfalfa market share in 2025, due to canal-rehabilitation investments that raise cutting frequency to four harvests per year. The White Nile and Blue Nile schemes jointly contribute a modest share by leveraging gravity-fed channels that lower pumping costs. Remaining output comes from emerging clusters in Kassala and River Nile states, where salt-tolerant cultivars expand acreage on previously marginal soils. Across all zones, growers channel roughly two-thirds of production toward export contracts while local dairies absorb the balance through spot purchases.

Regional performance inside Sudan hinges on the pace of irrigation infrastructure upgrades. The World Bank and African Development Bank-financed Gezira overhaul lifts water-delivery efficiency from 35% to 65%, reducing yield gaps between head- and tail-end farms. Drainage in the White Nile scheme still lags, causing salinity levels that trim per-hectare output by 10% in affected blocks. Blue Nile gains from automated gate controls that stabilize flow rates during peak evapotranspiration months. Kassala relies on smallholder pump sets along seasonal wadis, making production more vulnerable to diesel-price spikes. Government extension officers promote laser-leveling and deficit-irrigation scheduling to harmonize productivity across states.

Logistics inside Sudan shape delivered costs as much as agronomy. A paved corridor from Gezira to Port Sudan allows baled hay to reach the terminal in under 36 hours, while pellets trucked from White Nile need an additional day because of weigh-station queues. Port Sudan’s new gantry cranes lift container throughput, trimming vessel-berth time during the October to March export rush. Continuous improvements in domestic transport and storage infrastructure underpin the country-specific growth outlook for the Sudan Alfalfa market.

Competitive Landscape

Competition in the Sudan Alfalfa market is moderately concentrated. Integrated groups pair cultivation, dehydration, and freight forwarding to capture economies of scale. Kenana Sugar Company leveraged irrigation canals and energy cogeneration to enter alfalfa, diversifying revenue beyond sugar. Blue Nile Seeds and Forage positions itself as a seed-to-feed specialist with proprietary salt-tolerant cultivars.

Technology adoption differentiates market leaders. Precision irrigation sensors lower water use by 20%, boosting sustainability credentials that resonate with climate-smart buyers. Pelletizing facilities rely on natural-gas dryers that curb energy costs and reduce greenhouse-gas emissions. Cold-chain logistics investment enables cubes and haylage to reach importers without mold risk. Smaller players carve niches in organic certified hay and specialty micronutrient-fortified pellets for camel dairies.

Strategic moves in 2024 and 2025 focused on vertical integration and market access. DAL Agriculture signed a three-year supply agreement with a Saudi mega-dairy for 120,000 metric tons annually, ensuring offtake for its new 30-ton-per-hour pellet mill. Kenana commissioned a USD 12 million cube line that targets premium equine feed in Qatar. Market entrants monitor the evolving export-license regime that rewards compliance with traceability and quality audits.

Sudan Alfalfa Industry Leaders

DAL Agriculture (DAL Group)

Arab Company for Livestock Development (ACOLID)

Kenana Forage Division (Kenana Sugar Company)

Al Dahra Holding

Hassad Food

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Arab Authority for Agricultural Investment and Development updated Kenana Sugar Company profile, highlighting the company's expanded forage division operations and processing capabilities for alfalfa export markets.

- April 2024: World Bank and African Development Bank committed USD 400 million for Gezira irrigation scheme rehabilitation, targeting restoration of 150,000 hectares of irrigated agricultural land including alfalfa production areas.

Sudan Alfalfa Market Report Scope

Alfalfa is cultivated as an important forage crop in Sudan. It is used for grazing, hay, silage, green manure, and cover crop.

Sudan alfalfa hay market reports provides a detailed analysis by extensively analyzing the production (volume), consumption (value and volume), import (value and volume), export (value and volume), and price trend within the country.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product/Form

| Baled Hay |

| Pellets |

| Cubes |

| Others |

By End User

| Dairy Cattle |

| Beef Cattle |

| Camelids |

| Small Ruminants (Goat, Sheep) |

| Others |

| By Product/Form | Baled Hay |

| Pellets | |

| Cubes | |

| Others | |

| By End User | Dairy Cattle |

| Beef Cattle | |

| Camelids | |

| Small Ruminants (Goat, Sheep) | |

| Others |

Key Questions Answered in the Report

How big is the Sudan Alfalfa market in 2026?

The Sudan Alfalfa market size stands at USD 264.65 million in 2026 and is projected to reach USD 389.22 million by 2031.

Which product form grows the fastest in Sudanese alfalfa trade?

Pellets record the highest growth at an 11.18% CAGR because dehydration raises container load factors and preserves quality.

Why is camel feed demand important for Sudanese alfalfa?

Commercial camel-milk farms in the Gulf prefer alfalfa for its amino-acid profile, pushing camelid feed demand at a 10.45% CAGR.

How does irrigation rehabilitation affect Sudanese alfalfa output?

Canal repairs in Gezira lift water-delivery efficiency to 65%, enabling four harvests per year and enlarging production capacity.

Page last updated on: