North America Medium Voltage Switchgear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

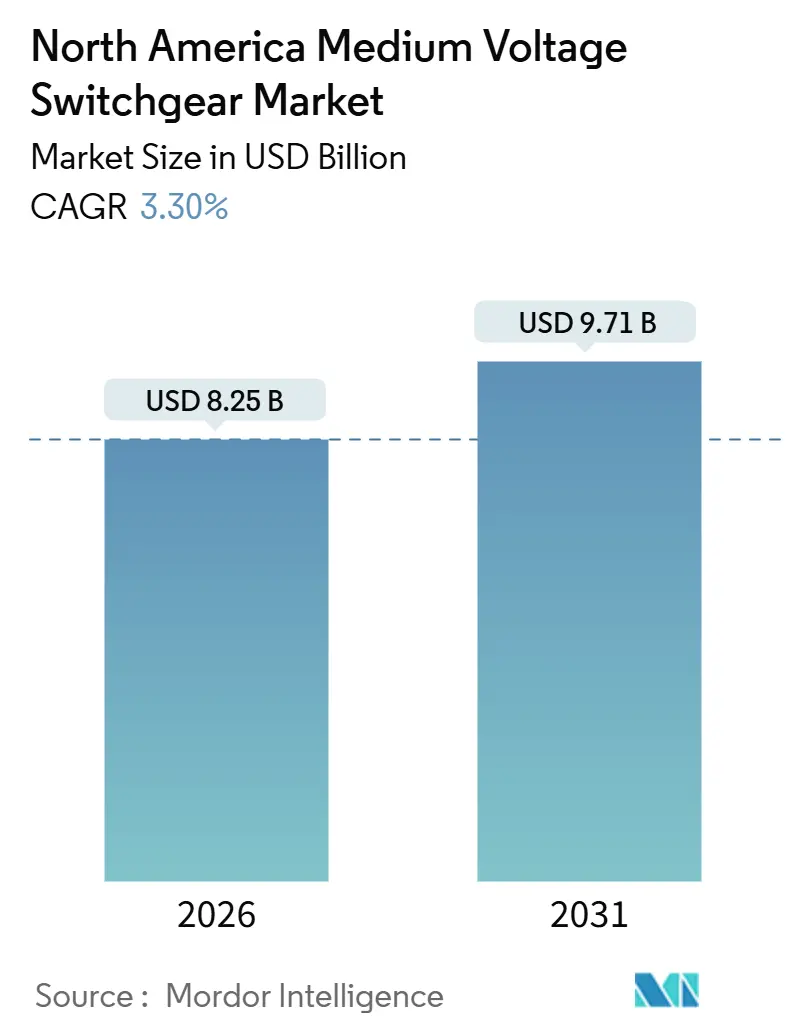

| Market Size (2026) | USD 8.25 Billion |

| Market Size (2031) | USD 9.71 Billion |

| Growth Rate (2026 - 2031) | 3.30% CAGR |

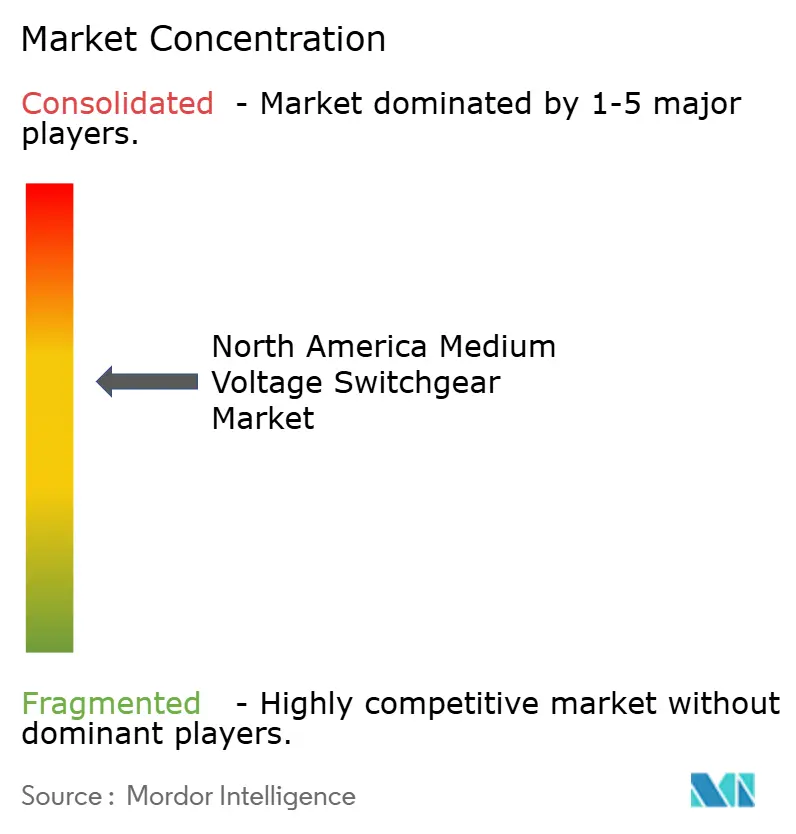

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Medium Voltage Switchgear Market Analysis by Mordor Intelligence

The North America Medium Voltage Switchgear Market size is estimated at USD 8.25 billion in 2026, and is expected to reach USD 9.71 billion by 2031, at a CAGR of 3.30% during the forecast period (2026-2031).

Grid-modernization grants under the Infrastructure Investment and Jobs Act (IIJA), rapid hyperscale data-center construction, and state-level bans on sulfur-hexafluoride (SF₆) are redefining procurement priorities across utilities and commercial buyers. Utilities are channeling IIJA funds toward SF₆-free gas-insulated switchgear (GIS) to meet California’s 2025 prohibition while safeguarding reliability in storm-prone regions.[1]U.S. Environmental Protection Agency, “Regulatory Impact Analysis for SF₆ Alternatives,” EPA.GOV Data-center operators, by contrast, are adopting 800-V direct-current (DC) architectures that sidestep conventional alternating-current (AC) switchgear in edge applications, compressing demand for traditional equipment in certain niches. Long manufacturing lead times for cast-resin components, together with a looming retirement wave that will remove half of the utility-electrician workforce by 2027, threaten to delay GIS projects and elevate labor premiums. Competitive pressure is intensifying as niche suppliers with North American factories win contracts on the strength of shorter cycle times and customized protection schemes.

Key Report Takeaways

- By insulation, Gas Insulated Switchgear captured 58.8% of the North America medium voltage switchgear market share in 2025, while the “Others” category is projected to advance at an 8.5% CAGR through 2031.

- By current type, AC switchgear led with 85.2% revenue share in 2025; the DC segment is forecast to expand at a 5.9% CAGR to 2031.

- By installation, indoor switchgear accounted for a 66.5% share of the North America medium voltage switchgear market size in 2025 and is set to grow at a 3.7% CAGR through 2031.

- By end-user, industrial facilities held a 57.7% share in 2025, while commercial users are advancing at a 6.6% CAGR to 2031.

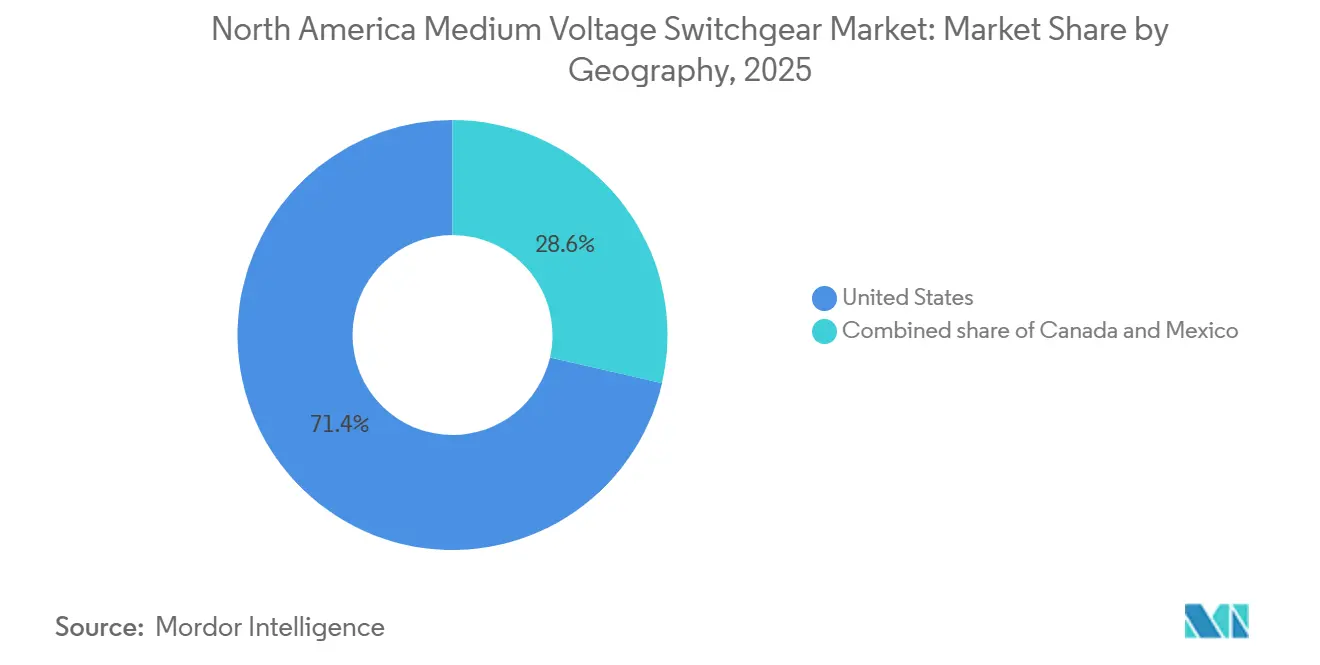

- By geography, the United States dominated with 71.4% revenue share in 2025; Canada records the fastest projected CAGR at 5.8% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global valuation is built by aggregating outputs from multiple regions, with North america forming one of the important contributors. Mordor Intelligence's global medium voltage switchgear market size report represents that cumulative total.

North America Medium Voltage Switchgear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-modernization investments under IIJA and provincial upgrade programs | +0.9% | United States, Canada | Medium term (2-4 years) |

| Rapid capacity build-out of hyperscale data centers | +1.1% | United States, Canada | Short term (≤ 2 years) |

| Utility commitments to SF₆-free switchgear | +0.6% | United States, Canada | Medium term (2-4 years) |

| Community-scale solar plus storage growth | +0.4% | United States, Mexico | Long term (≥ 4 years) |

| Electrification of commercial vehicle depots | +0.3% | United States, Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid-Modernization Investments Under IIJA and Provincial Upgrade Programs

Federal and provincial funding is accelerating substation upgrades that favor modular GIS over legacy air-insulated units. The IIJA’s USD 10.5 billion GRIP program steers utilities toward resilience rather than simple capacity expansion, and recipients such as the Tennessee Valley Authority have specified vacuum circuit breakers with remote-monitoring capability for extreme-weather hardening.[2]U.S. Department of Energy, “Grid Resilience and Innovation Partnerships Program,” ENERGY.GOV Ontario’s Grid Innovation Fund allocated CAD 400 million (USD 295 million) in 2025 for IEC 61850-ready switchgear to integrate distributed energy resources.[3]Ontario Government, “Grid Innovation Fund 2025,” ONTARIO.CA Southern utilities in hurricane zones are prioritizing outdoor-rated equipment with corrosion-resistant coatings, whereas northern operators prefer indoor GIS to avoid freeze–thaw stress. Compressed award timelines are shortening vendor selection windows, rewarding OEMs with U.S. or Canadian inventory. As grid-hardening mandates widen, the North America medium voltage switchgear market will increasingly pivot toward compact, digitally enabled platforms that comply with new interoperability standards.

Rapid Capacity Build-Out of Hyperscale Data Centers

Artificial-intelligence workloads are reshaping medium-voltage load profiles, with single racks now consuming up to 600 kW.[4]NVIDIA Corporation, “Powering AI at Scale,” NVIDIA.COM ABB and Eaton introduced 800 V DC switchgear in 2025 to serve edge data centers where real estate costs exceed USD 200 per square foot. U.S. data-center capacity is forecast to triple to 90 GW by 2030, yet interconnection queues in Virginia and Texas already exceed two years. Developers are responding by pairing on-site generation, often natural-gas peakers or battery storage, with dedicated medium-voltage switchgear. The result is a bifurcated demand curve: hyperscalers bypass utility substations with on-site 34.5 kV rings, while smaller colocation providers remain grid-connected and must satisfy NERC cybersecurity rules. This divergence supports sustained growth in the North America medium voltage switchgear market among vendors that can supply both AC and DC architectures with integrated protection and compliance features.

Utility Commitments to SF₆-Free Eco-Efficient Switchgear

California’s 2025 prohibition on new SF₆ installations is rippling across the region as Massachusetts and New York adopt similar deadlines. Hitachi Energy recorded 65 EconiQ orders in North America through 2025, primarily from investor-owned utilities pressured to cut Scope 1 emissions. Vacuum interrupters and fluoroketone insulation deliver equivalent dielectric performance with 99.9% lower global-warming potential, but they introduce higher maintenance frequency. Municipal utilities that operate on thin margins are delaying adoption until incentives materialize, producing a two-speed transition within the North America medium voltage switchgear market. Equipment makers are standardizing SF₆-free lines to serve both U.S. compliance markets and Canadian buyers that anticipate parallel regulations.

Community-Scale Solar Plus Storage Growth

Community solar projects ranging from 1 MW to 5 MW require medium-voltage interconnection at 12.47 kV to 34.5 kV. GE Vernova’s FLEXINVERTER integrates solar, battery storage, and switchgear onto a single skid, cutting commissioning time below two weeks and shrinking the substation footprint by 40%. In Mexico, distributed-generation reforms enable third-party ownership, and CFE mandates medium-voltage metering at the point of common coupling, stimulating switchgear orders in manufacturing hubs such as Nuevo León. Developers prize plug-and-play solutions, yet utility protection settings often necessitate custom relay programming, eroding cost advantages. Nonetheless, the solar-plus-storage wave broadens the customer base for the North America medium voltage switchgear market beyond traditional utility segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged GIS lead times from cast-resin shortages | -0.5% | United States, Canada | Short term (≤ 2 years) |

| Skilled-labor gaps in commissioning and maintenance | -0.4% | United States, Canada | Medium term (2-4 years) |

| Cybersecurity compliance costs | -0.2% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prolonged GIS Lead Times From Cast-Resin Shortages

Global epoxy feedstock disruptions continue to lengthen custom GIS lead times to 12–18 months, double the 6–9 months typical of air-insulated switchgear. ABB and Schneider Electric now pre-build GIS modules for common voltage classes, yet bespoke protection or bus configurations still require fresh casting, pushing delivery well into 2027 for projects ordered in 2025. Cast-resin prices rose 18% between 2024 and 2025, prompting surcharge pass-throughs that erode GIS’s total-cost-of-ownership edge in non-space-constrained sites. Some utilities pivot to outdoor AIS for greenfield builds, accepting larger land parcels to sidestep resin bottlenecks. Unless supply recovers, the North America medium voltage switchgear market faces a near-term cap on GIS volume growth.

Skilled-Labor Gaps in Commissioning and Maintenance

Half of North American utility electricians will be retirement-eligible by 2027, and apprenticeship pipelines lag replacement needs. Commissioning a 15 kV GIS now takes five weeks versus three weeks in 2020, adding 30%–40% labor cost. Rural cooperatives struggle most as technicians migrate to higher-paying data-center projects. Improper torque on bus joints or miscalibrated relays raises arc-flash risk, prompting insurers to tighten underwriting terms. Remote-assisted commissioning via augmented-reality headsets shows promise but is restricted by physical-security rules that limit off-site network access. Labor scarcity, therefore, constrains installation capacity across the North America medium voltage switchgear market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insulation: GIS Holds Pole Position While Hybrid Designs Scale

Gas-insulated switchgear secured 58.8% revenue share in 2025 within the North America medium voltage switchgear market, reflecting its 60%–70% footprint advantage in dense urban substations. The segment benefits further as utilities pursue SF₆-free replacements to meet state mandates. Air-insulated units retain cost leadership in rural builds where land is cheap. The “Others” category, covering solid-state and hybrid breakers, is projected to grow at an 8.5% CAGR through 2031, the industry’s fastest across insulation types, thanks to utilities piloting sub-cycle fault-current-limiting solutions.

Solid-state prototypes with silicon-carbide semiconductors from ABB and Eaton cut interruption time to microseconds, minimizing voltage sags for sensitive data-center loads. Hybrid platforms marry mechanical contacts for steady-state operation with electronic devices for fault clearing, enabling gradual migration toward solid-state architectures. In Canada, high wildlife-induced fault rates spur tests of hybrid reclosers designed for distribution grids. As a result, the North America medium voltage switchgear market will likely see GIS remain dominant in space-constrained settings, AIS rule in low-cost greenfield sites, and hybrid technologies blossom in reliability-critical nodes, the three designs coexisting rather than converging.

By Current Type: DC Footprint Expands From Niche to Visible Slice

AC equipment retained an 85.2% share of the North America medium voltage switchgear market size in 2025, underscoring the legacy AC grid architecture. Yet DC switchgear will record a 5.9% CAGR through 2031 on data-center, renewables, and battery-storage demand. ABB’s 800 V DC lineup trims cooling loads by 10%–15% in hyperscale facilities, a clear operating-expense benefit. Battery storage and solar plants that natively produce DC further reduce conversion losses when interconnected via medium-voltage DC switchgear.

Standards lag remains a hurdle, with IEEE and ANSI guidance trailing IEC 61660 for DC testing. Certification ambiguity slows U.S. utility adoption, although military and campus microgrids already specify DC loops to bolster resilience. Within the North America medium voltage switchgear industry, AC platforms will continue to dominate utility and industrial orders, but DC volumes will climb steadily where efficiency and space are premium concerns.

By Installation: Indoor Dominates Dense Metro Upgrades

Indoor units commanded 66.5% share of the North America medium voltage switchgear market in 2025 and will expand at a 3.7% CAGR through 2031 as city operators rebuild aging substations inside existing footprints. Gas-insulated designs allow placement beneath office towers or transport hubs, reducing land acquisition and improving protection from weather events.

Outdoor switchgear remains standard for greenfield utility substations and petrochemical complexes where space is ample. Powell Industries supplies outdoor metal-clad units with corrosion-resistant coatings for coastal utilities facing salt spray. Cost considerations still tilt some buyers toward outdoor air-insulated variants, but lifecycle analysis often favors indoor GIS when urban land exceeds USD 50 per square foot. Consequently, installation choice reflects a total-cost calculation rather than a one-time capital outlay, sustaining a mixed offering within the North America medium voltage switchgear market.

By End-User: Commercial Build-Out Overtakes Industrial Growth

Industrial plants held 57.7% revenue share in 2025, anchored by heavy manufacturing, mining, and petrochemical users with large-horsepower motor loads. Commercial customers, data centers, hospitals, and research campuses will expand at a 6.6% CAGR, nearly twice the market average, as AI clusters and high-acuity healthcare facilities demand resilient power.

Commercial buyers favor switchgear with sub-second protection clear times and N+1 redundancy. ABB’s HiPerGuard medium-voltage UPS exceeded 330 MW of global installs by 2025, with significant North American uptake in mission-critical facilities. Meanwhile, G&W Electric’s Viper-ST recloser appeals to commercial developers requiring automation without utility-grade complexity. Industrial buyers remain cost-sensitive, preferring standardized air-insulated units. This divergence means the North America medium voltage switchgear market must serve two distinct value propositions: customized reliability for commercial segments and rugged affordability for industrial users.

Geography Analysis

The United States held 71.4% of the North America medium voltage switchgear market share in 2025, lifted by IIJA funding and a pipeline exceeding 60 GW of announced data-center capacity. Federal grants flow through fiscal 2026, prompting utilities to compress procurement cycles for SF₆-free GIS.

Canada is projected to deliver the fastest regional CAGR at 5.8% through 2031, underpinned by Ontario and Québec grid-modernization mandates and hydro-powered data-center campuses. IEC 61850 interoperability requirements in provincial programs spur demand for digital switchgear.

Mexico remains the smallest market today, but is pivoting on nearshoring. CFE accelerates medium-voltage builds in Nuevo León and Coahuila, mandating metering at the point of common coupling for industrial solar sites. Mexican plants serve as low-cost assembly hubs for global OEMs shipping into the broader North America medium voltage switchgear market, tightening supply chains and shortening delivery timelines for U.S. buyers.

Coverage of the medium voltage switchgear market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, Middle East and Africa, and Asia.

Competitive Landscape

The top five suppliers, ABB, Siemens, Schneider Electric, Eaton, and GE Vernova, control roughly 55%–60% of the North America medium voltage switchgear market, yet regional specialists are eroding share by offering rapid customization and domestic production. Powell Industries leverages its Texas facility to deliver tailored switchgear in 10 weeks, winning multiple 2025 data-center awards. G&W Electric and S&C Electric dominate reclosers and sectionalizers for self-healing distribution grids, segments growing faster than base-substation gear.

Technology forms the new competitive battleground. Schneider’s EcoStruxure Grid bundles switchgear with cloud analytics, while Siemens integrates hardware with Xcelerator digital twins to offer asset-performance contracts. ABB and Eaton filed patents for fluoroketone insulation and solid-state breakers, signaling intent to lead the post-SF₆ era.

White-space opportunities arise in DC switchgear and solid-state designs where incumbents lack portfolio depth. NOJA Power entered North America in 2025, supplying rural cooperatives with auto-reclosing controllers that cut outage durations by up to 60%. Integration and cybersecurity expertise, more than hardware alone, will increasingly differentiate vendors as utilities embed switchgear in digital-substation ecosystems across the North America medium voltage switchgear market.

North America Medium Voltage Switchgear Industry Leaders

ABB Ltd

Eaton Corporation plc

Siemens AG

Schneider Electric SE

General Electric (GE Vernova)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Trystar, LLC has acquired Island Technical Installations Ltd (ITI) to strengthen its low and medium-voltage switchgear solutions, including installation, commissioning, testing, and field services. ITI, headquartered in Victoria, British Columbia, Canada, specializes in engineering, manufacturing, and servicing metal-clad and metal-enclosed switchgear.

- October 2025: Electro-Mechanical, LLC, a leading manufacturer of medium voltage switchgear, has acquired Powercon Corporation, a provider of custom medium voltage switchgear, e-houses, and modular substation power systems.

- August 2025: Oak Ridge National Laboratory researchers, under the Department of Energy, have developed faster, cost-effective medium-voltage circuit breakers to enhance the U.S. electric grid's capacity and reduce electricity costs.

- May 2025: GE Vernova Inc., a leading U.S. energy manufacturer, plans to invest nearly USD 600 million in its factories and facilities over the next two years to meet rising global electricity demands. The investment aims to enhance U.S. energy affordability, national security, competitiveness, and manufacturing capacity to support growing exports.

North America Medium Voltage Switchgear Market Report Scope

MV switchgear, or Medium Voltage Switchgear, serves as a centralized hub, housing essential electrical components such as circuit breakers, fuses, and switches within a protective metal enclosure. Its primary function is to control, protect, and isolate electrical circuits in power systems. This ensures safe and efficient power distribution across industries, commercial buildings, and utilities.

The North America medium voltage switchgear market is segmented by insulation, current type, installation, end-user, and geography. By insulation, the market is segmented into gas-insulated switchgear, air-insulated switchgear, and others. By current type, the market is segmented into AC switchgear and DC switchgear. By installation, the market is segmented into indoor and outdoor. By end-user, the market is segmented into utilities, residential, commercial, and industrial. The report also covers the market size and forecasts for the North America medium voltage switchgear market across the regions. For each segment, the market sizing and forecasts have been done based on revenue (USD billion).

| Gas Insulated Switchgear (GIS) |

| Air Insulated Switchgear (AIS) |

| Others |

| AC Switchgear |

| DC Switchgear |

| Indoor |

| Outdoor |

| Utilities |

| Residential |

| Commercial |

| Industrial |

| United States |

| Canada |

| Mexico |

| By Insulation | Gas Insulated Switchgear (GIS) |

| Air Insulated Switchgear (AIS) | |

| Others | |

| By Current Type | AC Switchgear |

| DC Switchgear | |

| By Installation | Indoor |

| Outdoor | |

| By End-User | Utilities |

| Residential | |

| Commercial | |

| Industrial | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America medium voltage switchgear market in 2026?

The market is valued at USD 8.25 billion in 2026, advancing toward USD 9.71 billion by 2031 at a 3.30% CAGR.

Which insulation type leads current revenue?

Gas-insulated switchgear leads with 58.8% share in 2025 and remains favored for space-constrained urban substations.

Where is growth fastest by geography?

Canada records the quickest pace with a projected 5.8% CAGR through 2031, propelled by provincial grid-modernization programs.

Why is DC switchgear gaining traction?

Data-center operators and renewable-energy developers adopt 800 V DC architectures to cut conversion losses and footprint, driving a 5.9% CAGR for DC equipment.

What is restraining GIS adoption?

Cast-resin shortages lengthen GIS lead times to up to 18 months and elevate costs, prompting some buyers to opt for air-insulated alternatives.

How will SF6 regulations influence demand?

How will SF₆ regulations influence demand?

Page last updated on: