Waterproofing Solutions Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 32.83 Billion |

| Market Size (2031) | USD 42.77 Billion |

| Growth Rate (2026 - 2031) | 5.43% CAGR |

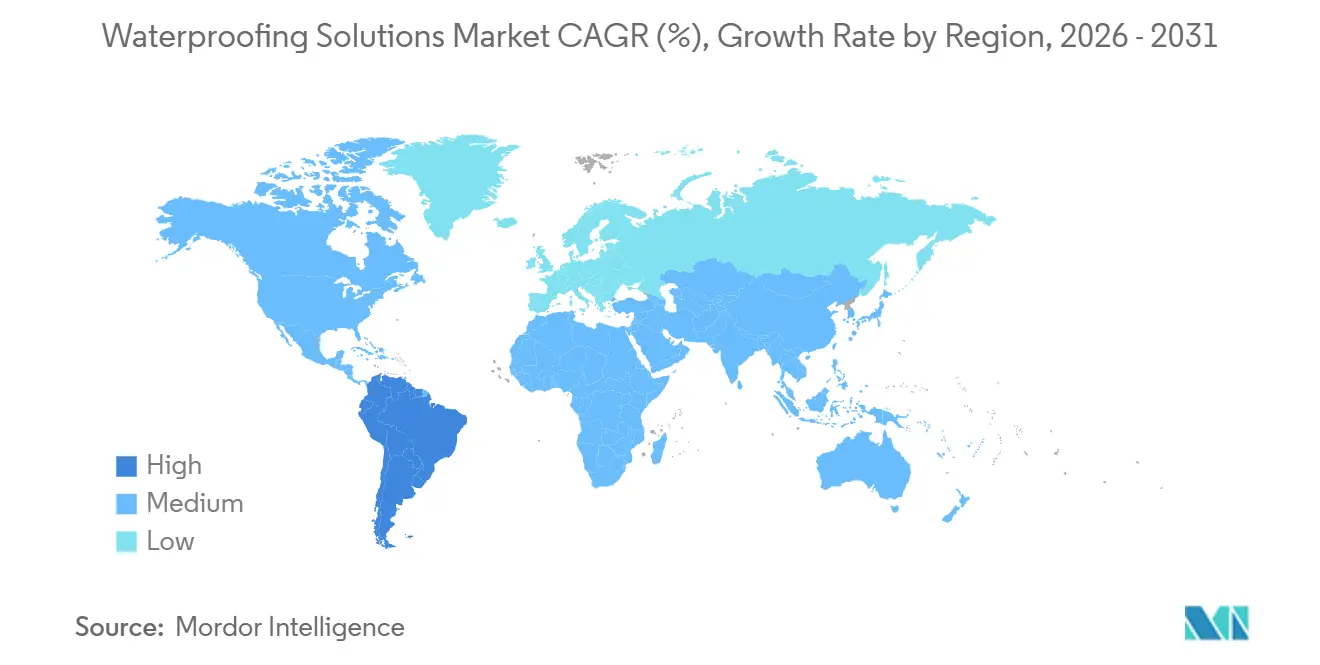

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

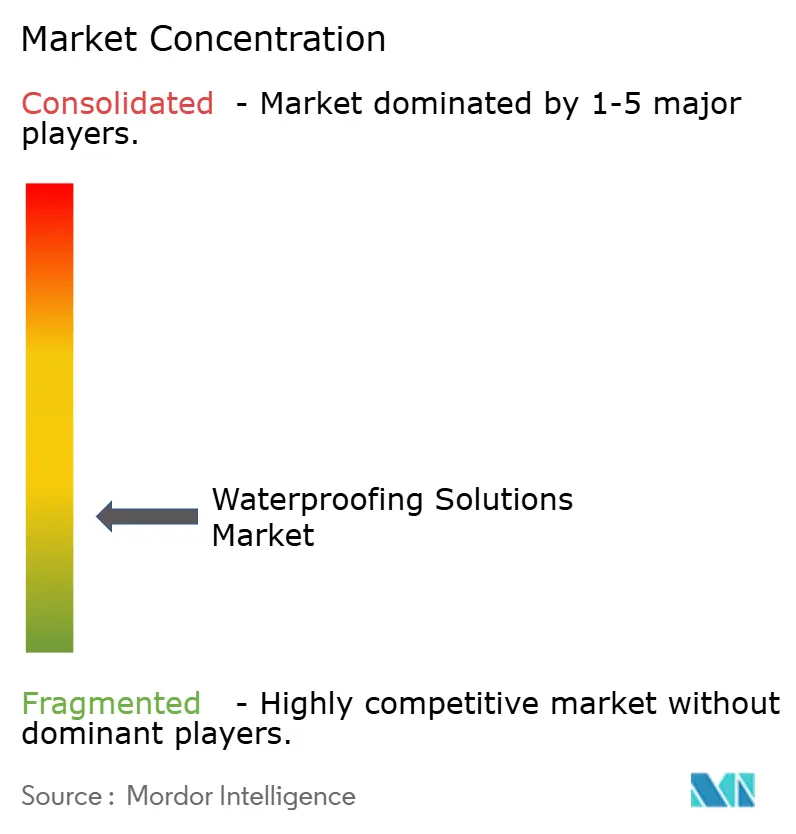

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Waterproofing Solutions Market Analysis by Mordor Intelligence

The Waterproofing Solutions Market size is expected to grow from USD 31.14 billion in 2025 to USD 32.83 billion in 2026 and is forecast to reach USD 42.77 billion by 2031 at 5.43% CAGR over 2026-2031. Heightened fire-performance codes, global low-VOC mandates, and accelerating public-infrastructure spending are reshaping competitive dynamics and fueling a structural pivot toward sheet and water-borne liquid membranes. Suppliers are back-integrating into raw materials to hedge against polyurethane feedstock volatility, while simultaneously moving downstream into installation services to ease the certified-labor bottleneck. Asia-Pacific remains the volume engine as urban migration tightens housing supply, yet North American and European buyers are pulling demand toward integral-crystalline admixtures that self-heal micro-cracks in concrete, a technology now endorsed by ACI 212.3R-24. The waterproofing solutions market is further buoyed by hyperscale data-center builds that require advanced roofing assemblies capable of supporting liquid-cooling systems and withstanding extreme thermal cycling.

Key Report Takeaways

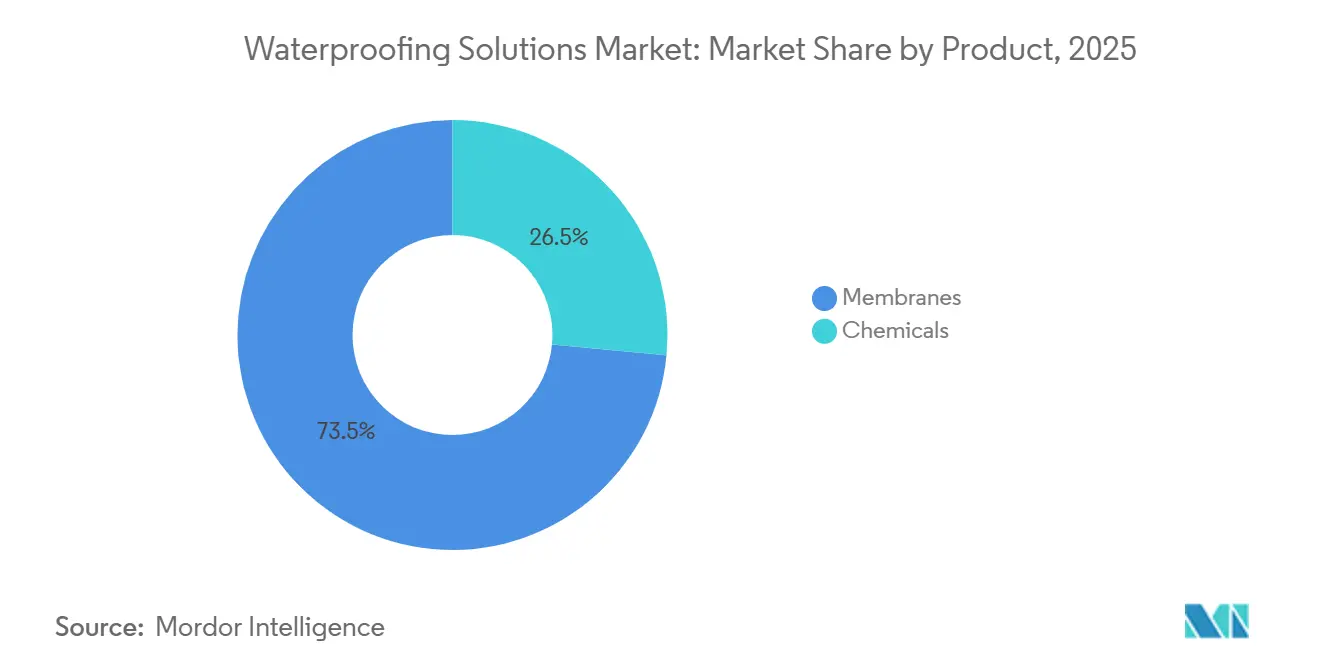

- By product, membranes held 73.49% of the waterproofing solutions market share in 2025 and are projected to expand at a 5.72% CAGR through 2031.

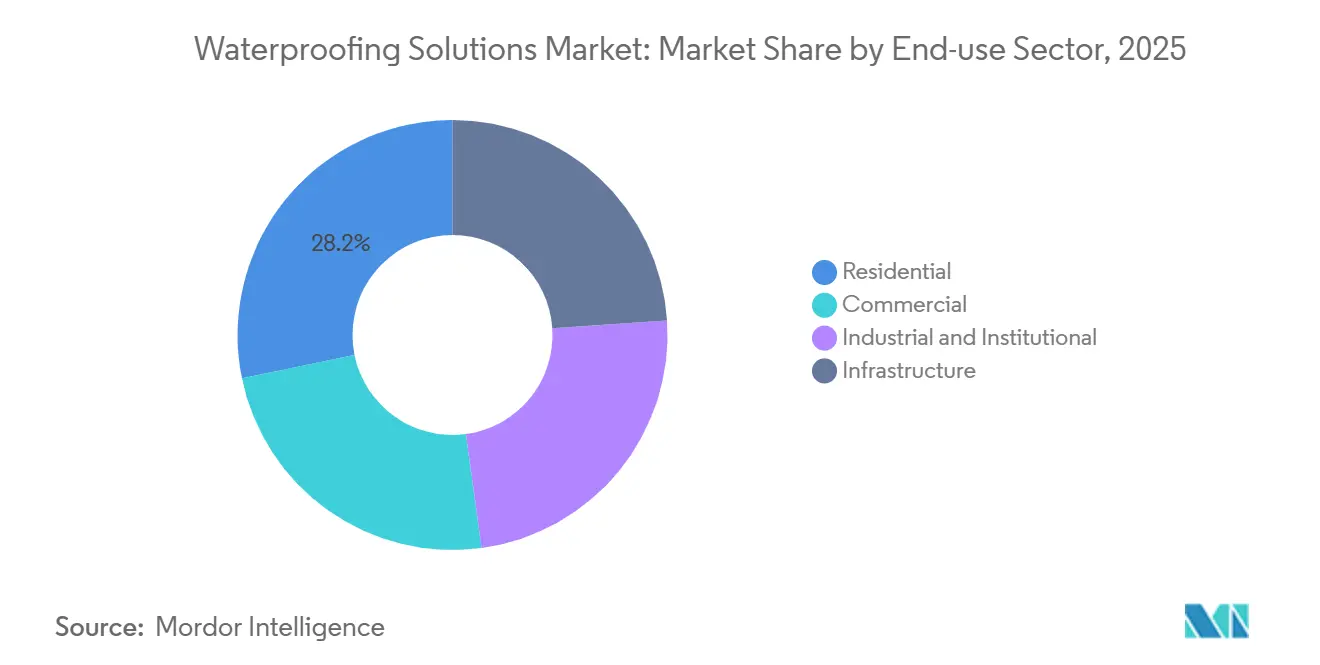

- By end-use sector, residential held 28.22% of the waterproofing solutions market share in 2025, while infrastructure is projected to expand at a 5.93% CAGR through 2031.

- By geography, Asia-Pacific captured 36.88% of the waterproofing solutions market share in 2025, while South America is poised to expand at a 6.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Waterproofing Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in green-building low-VOC mandates | +0.8% | North America and EU, spillover to APAC | Medium term (2-4 years) |

| Rapid urbanization and infrastructure build-out | +1.2% | APAC core (China, India, Indonesia), MEA | Long term (≥ 4 years) |

| Rapid growth in public infrastructure projects | +1.0% | Global, concentrated in APAC and South America | Medium term (2-4 years) |

| Expansion of hyperscale data-centers requiring advanced roofing solutions | +0.6% | North America, EU, Singapore, Australia | Short term (≤ 2 years) |

| Climate-resilience retrofits driving integral-crystalline admixture uptake | +0.7% | Coastal regions globally, APAC typhoon belt, North America hurricane zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Green-Building Low-VOC Mandates

California capped VOC content in waterproofing membranes at 100 grams per liter in 2022, and the European Union’s Construction Products Regulation (EU) 2024/3110 will require digital product passports from January 2026[1]California Air Resources Board, “Architectural and Industrial Coatings Rule,” arb.ca.gov . These rules are forcing a transition from solvent-based polyurethanes to water-borne dispersions, inflating raw-material costs by 10-15% but opening access to LEED v4.1 and BREEAM Excellent projects. Hybrid silane-terminated polymers that cure at ambient humidity without isocyanate catalysts are gaining share in curtain-wall, plaza-deck, and façade applications. ISO 14025 environmental product declarations have become de-facto gatekeepers for public tenders in Germany and the Nordic countries, locking out suppliers unable to fund third-party verification.

Rapid Urbanization and Infrastructure Build-Out

Asia-Pacific added 60 million urban residents in 2024, lifting China’s urbanization rate to 66.2% and creating demand for 1.5 billion m² of new floor space. India’s National Infrastructure Pipeline has allocated USD 1.4 trillion through 2025, yet municipal funding gaps favor cost-effective bituminous membranes in Tier-2 and Tier-3 cities. Multinationals like Sika and BASF pursue metro-rail and high-rise projects with cold liquid-applied membranes, while domestic champions dominate affordable-housing schemes with hot-applied rolls priced 30-40% lower. Crystalline admixtures are accelerating in Indonesia, Vietnam, and the Philippines where flood-control investments lag and lifecycle savings reach 25% versus surface coatings.

Rapid Growth in Public Infrastructure Projects

The United States Infrastructure Investment and Jobs Act earmarked USD 110 billion for roads and bridges that require bridge-deck and tunnel waterproofing. Brazil’s PAC committed BRL 1.7 trillion (USD 340 billion) through 2026 to sanitation and flood-mitigation works. Agencies favor fully adhered sheet membranes that bond mechanically to concrete and endure freeze-thaw cycles better than loose-laid alternatives. Saudi Arabia’s Vision 2030 megaprojects deploy reflective liquid-applied membranes that cut roof temperatures by 20-30 °C, extending service life in desert climates.

Expansion of Hyperscale Data-Centers Requiring Advanced Roofing Solutions

North American hyperscale capacity rose 18% in 2025 as Microsoft, AWS, and Google added 1,200 MW of IT load that demands roofs capable of supporting 50-80 kg/m² mechanical equipment. Fully adhered TPO and PVC membranes rated for ponding water now dominate data-center specifications. Direct-to-chip liquid cooling introduces condensation risks, prompting dual-layer assemblies pairing vapor-permeable air barriers with impermeable liquid membranes, adding USD 15-20 per m² but eliminating interstitial moisture. Singapore’s Green Mark scheme awards points for membranes with SRI more than 78, effectively mandating white or light-gray systems and accelerating adoption in Southeast Asia.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Specialist-installer labor shortage | -0.5% | Global, acute in North America and Western Europe | Short term (≤ 2 years) |

| Microplastic compliance burden | -0.3% | EU, potential spillover to North America and APAC | Medium term (2-4 years) |

| Fire-performance code revisions limiting combustible liquid membranes | -0.4% | North America, EU, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Specialist-Installer Labor Shortage

The United States recorded 400,000 unfilled construction jobs in 2025, with roofing and waterproofing trades facing turnover above 30%[2]U.S. Bureau of Labor Statistics, “Job Openings and Labor Turnover Survey,” bls.gov . Cold liquid-applied membranes demand multistep application within narrow climatic windows, a skill set that takes up to three years to master and commands 20-25% wage premiums. Project durations have stretched from six to nine weeks for a 50,000 ft² roof, inflating labor costs by 35-40%. Manufacturers such as Sika and RPM International have launched installer academies, but meaningful capacity increases will take three to five years to materialize.

Microplastic Compliance Burden

The European Chemicals Agency added styrene-butadiene latex and acrylic copolymers to its restricted list in 2024, citing runoff concentrations above 100 mg/L on high-traffic plaza decks. Reformulating with bio-based binders adds 15-20% to raw-material costs and forces retooling of production lines. Multinationals can amortize expenses across global volumes, but small regional players risk exit or acquisition. Investment decisions are frozen until Brussels clarifies whether roofing membranes, 60% of the waterproofing solutions market, fall under the next phase of restrictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Membranes Dominate Amid Fire-Code Tailwinds

Membranes captured 73.49% of the waterproofing solutions market share in 2025 and are projected to grow at a 5.72% CAGR through 2031 as NFPA 285 and Approved Document B elevate demand for sheet and cold liquid-applied systems. Fully adhered sheets bond mechanically to damp concrete and now dominate bridge-deck specifications, while cold liquid-applied membranes are displacing hot-applied systems on commercial roofs as insurers surcharge projects using open-flame equipment. Loose-laid sheets remain cost-effective on low-slope industrial roofs but are losing share as owners add rooftop solar and HVAC units that require puncture resistance.

Chemical formulations, such as epoxy, polyurethane, and water-based coatings, address niches where thin-film protection or chemical resistance is paramount. Epoxy dominates secondary containment and industrial flooring but suffers from UV sensitivity. Polyurethane offers superior abrasion resistance for parking decks, yet its isocyanate content triggers low-VOC rules in California and Europe. Water-based acrylics and silicones appeal to do-it-yourself residential users but lack the crack-bridging capacity demanded by structural waterproofing. Emerging bio-based epoxies command a 25-30% premium but are gaining traction in LEED Platinum projects that prioritize embodied-carbon reduction.

By End-use Sector: Infrastructure Accelerates as Residential Matures

The residential sector accounted for 28.22% of the waterproofing solutions market share in 2025, but infrastructure is forecast to expand at a 5.93% CAGR through 2031, supported by record public-works budgets. Single-family homes in North America and Europe are adopting integral-crystalline admixtures for below-grade walls, while Asia-Pacific affordable-housing schemes continue to rely on bituminous rolls to meet cost targets. Commercial developers are layering waterproofing beneath green roofs that reduce stormwater runoff by 50-70%, adding USD 40-60 per m² yet unlocking LEED credits.

Industrial and institutional buyers specify epoxy and polyurethane systems for chemical resistance in food processing, pharmaceuticals, and wastewater facilities. Infrastructure projects, such as bridges, tunnels, metros, and airports, demand membranes that withstand de-icing salts and heavy loads. The U.S. Federal Highway Administration estimates 40% of bridges need deck rehabilitation, fueling demand for rapid-curing polyurea that reopens traffic within six hours. Coastal cities retrofit seawalls and subway tunnels with crystalline admixtures to prevent flood damage that can cost USD 5-10 million per incident.

Geography Analysis

Asia-Pacific generated 36.88% of the waterproofing solutions market share in 2025, driven by China’s 66% urbanization rate and India’s USD 1.4 trillion infrastructure pipeline, yet growth is moderating as Beijing’s property deleveraging shifts demand from speculative condos to government-backed affordable housing. Japan’s condominium retrofit wave is replacing aged balcony membranes, where Nippon Paint and Sika enjoy 60% combined share through exclusive deals with property managers. Southeast Asia is emerging as a manufacturing hub; Beijing Oriental Yuhong and Keshun have formed joint ventures in Indonesia and Malaysia to sidestep anti-dumping duties and serve ASEAN transport projects. Australia’s National Construction Code 2025 now mandates independent wet-area inspections, professionalizing installers and reducing warranty claims.

North America posts steady gains under the USD 1.2 trillion Infrastructure Investment and Jobs Act, though residential construction lags pre-2008 peaks due to high mortgage rates. Canadian green-roof bylaws in Toronto and Vancouver accelerate adoption of vegetated assemblies that require robust waterproofing. Mexico’s nearshoring wave boosts industrial builds with polyurethane roofs that satisfy multinational sustainability standards. Europe splits between retrofit-heavy Western markets and new-build-focused Eastern members tapping cohesion funds for transport and energy projects.

South America is projected to grow at a 6.26% CAGR through 2031, led by Brazil’s BRL 1.7 trillion infrastructure drive and Argentina’s lithium-mining expansion, both requiring epoxy linings and crystalline admixtures resilient to chemical attack. Middle-East and Africa gain momentum from Saudi Arabia’s Vision 2030 and UAE Expo legacy builds specifying reflective membranes, yet reliance on imported materials exposes the region to currency and supply-chain risks.

Competitive Landscape

The waterproofing solutions market exhibits low concentration, with Sika AG, RPM International, Saint-Gobain, Beijing Oriental Yuhong Waterproof Technology Co., Ltd., and Soprema controlling 28% of global revenue. Backward integration into polyol and isocyanate feedstocks, forward integration into installation services, and rapid portfolio pivoting toward low-VOC, fire-compliant systems define today’s playbook. Sika’s 2023 purchase of MBCC injects concrete admixtures and tunneling chemicals, allowing single-source bids on metro and bridge projects. RPM International’s acquisitions of regional applicators grant 450 installers to its Tremco division, capturing installation margins that exceed manufacturing return.

Technology is a differentiator. Soprema embeds IoT moisture sensors in membranes, extending warranties from 10 to 20 years in data-center and pharma builds. Arkema filed 12 patents on lignin-derived epoxies in 2024-2025, while BASF commercializes microencapsulated self-healing agents. Regional champions carve niches: Pidilite Industries dominates India’s do-it-yourself segment through a network of 8,000 retailers, and Beijing Oriental Yuhong secures multi-year supply contracts for China’s affordable-housing program. Regulatory costs around microplastics and fire codes are expected to trigger further consolidation as smaller firms lack resources to reformulate and certify new chemistries.

Waterproofing Solutions Industry Leaders

Sika AG

Saint-Gobain

Beijing Oriental Yuhong Waterproof Technology Co., Ltd.

RPM International Inc.

Soprema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Bigbloc Building Elements Private Limited, a subsidiary of Bigbloc Construction Limited, commenced trial production of construction chemicals at its Umargaon facility. The product range included waterproofing solutions, block jointing mortar, ready-mix plaster, and tile adhesives.

- November 2025: Sika AG acquired Awazil Al Khaleej Industrial Co. (“Gulf Seal”), a Saudi-based manufacturer of bituminous waterproofing membranes, strengthening its presence in Saudi Arabia and the Gulf Cooperation Council (GCC) region. Established over 20 years ago, Gulf Seal supplied membranes for significant construction projects in Saudi Arabia and other GCC countries.

Global Waterproofing Solutions Market Report Scope

Waterproofing solutions consist of materials, techniques, and systems designed to form an impermeable barrier, preventing water from penetrating surfaces or structural elements. These solutions safeguard buildings and objects from damage caused by moisture, hydrostatic pressure, and water vapor.

The waterproofing solutions market is segmented by product, end-use sector, and geography. By product, the market is segmented into chemicals and membranes. By chemicals, the market is sub-segmented into epoxy-based, polyurethane-based, water-based, and other technologies. By membranes, the market is sub-segmented into cold liquid applied, hot liquid applied, fully adhered sheet, and loose-laid sheet. By end-use sector, the market is segmented into residential, commercial, industrial and institutional, and infrastructure. The report also covers the market size and forecasts for waterproofing solutions in 22 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Membranes | Cold Liquid Applied |

| Hot Liquid Applied | |

| Fully Adhered Sheet | |

| Loose-Laid Sheet | |

| Chemicals | Epoxy-based |

| Polyurethane-based | |

| Water-based | |

| Other Technologies |

| Residential |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacific | |

| North America | Canada |

| Mexico | |

| United States | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle-East and Africa |

| By Product | Membranes | Cold Liquid Applied |

| Hot Liquid Applied | ||

| Fully Adhered Sheet | ||

| Loose-Laid Sheet | ||

| Chemicals | Epoxy-based | |

| Polyurethane-based | ||

| Water-based | ||

| Other Technologies | ||

| By End-use Sector | Residential | |

| Commercial | ||

| Industrial and Institutional | ||

| Infrastructure | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Malaysia | ||

| Thailand | ||

| Vietnam | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| North America | Canada | |

| Mexico | ||

| United States | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle-East and Africa | ||

Market Definition

- END-USE SECTOR - Waterproofing solutions consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of waterproofing solutions such as membranes, coatings, and chemicals are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms