Market Overview

| Study Period | 2020 - 2031 |

|---|---|

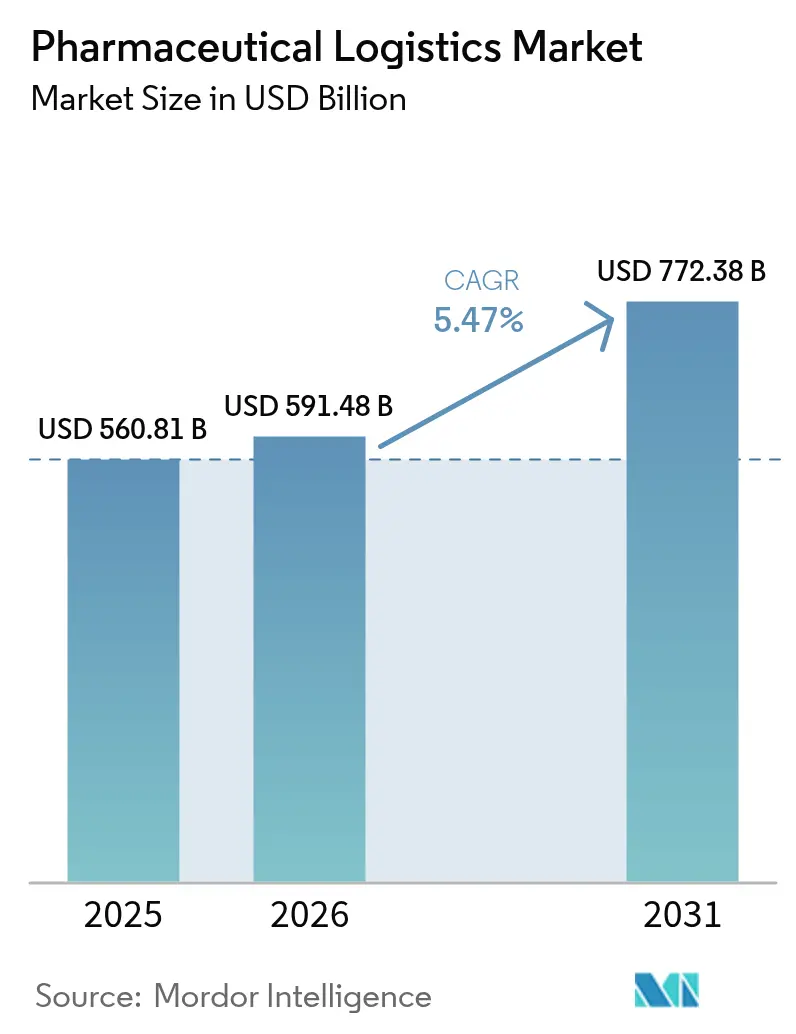

| Market Size (2026) | USD 591.48 Billion |

| Market Size (2031) | USD 772.38 Billion |

| Growth Rate (2026 - 2031) | 5.47% CAGR |

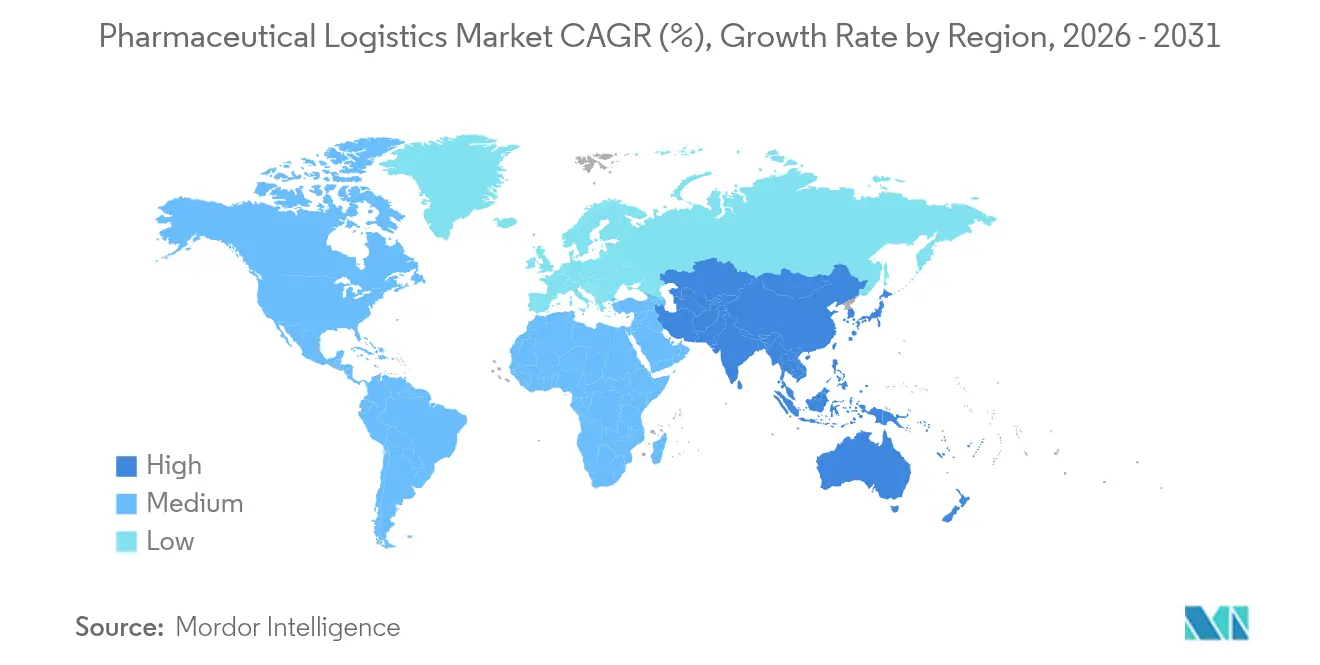

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Logistics Market Analysis by Mordor Intelligence

The Pharmaceutical Logistics Market size was valued at USD 560.81 billion in 2025 and estimated to grow from USD 591.48 billion in 2026 to reach USD 772.38 billion by 2031, at a CAGR of 5.47% during the forecast period (2026-2031).

Robust growth stems from biologics proliferation, rigorous serialization mandates, and the pivot toward direct-to-patient delivery models that require precision distribution capacities. Strong capital spending by global integrators, sustained e-pharmacy adoption, and expanding temperature-controlled infrastructure continue to intensify competition while enlarging addressable demand for end-to-end, compliant supply-chain solutions. Technology deployment—particularly IoT sensors, blockchain traceability, and AI-driven network optimization—has accelerated as stakeholders guard against temperature excursions and counterfeit risk. At the same time, sustainability commitments are redirecting capacity toward intermodal and ocean transportation to curb emissions, opening new service niches for specialty providers. Price pressures linked to cold-chain energy costs and multi-jurisdictional compliance remain headwinds, yet they also spur investment in low-carbon packaging, regionalized inventories, and alternative fuels that ultimately expand the pharmaceutical logistics market.

Key Report Takeaways

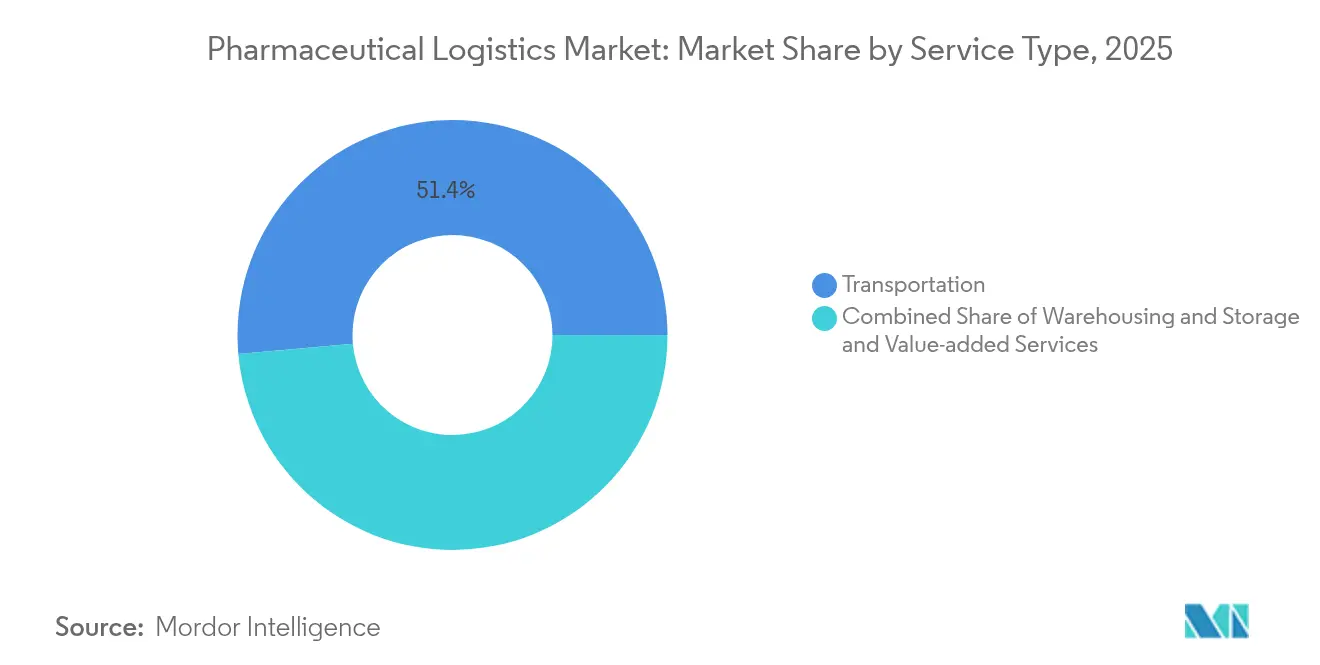

- By service type, transportation services held 51.40% of the pharmaceutical logistics market share in 2025, while value-added services are forecast to grow at a 4.42% CAGR to 2031.

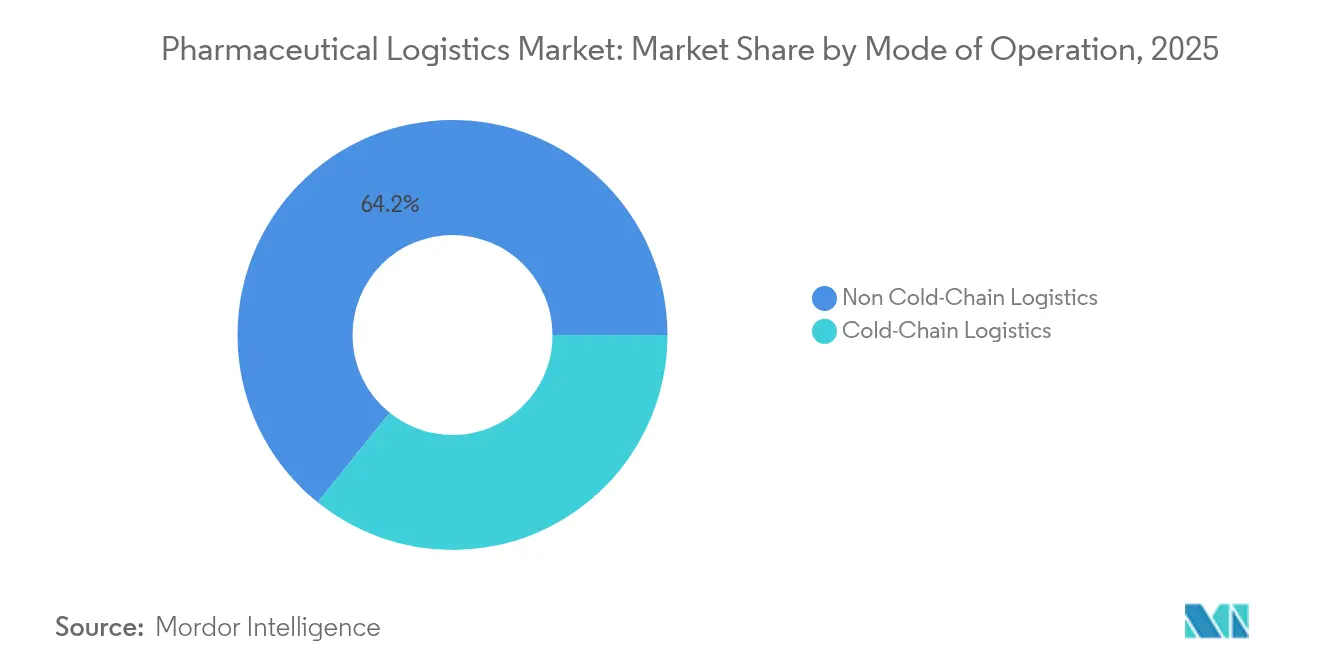

- By mode of operation, non-cold-chain logistics accounted for 64.20% of the pharmaceutical logistics market size in 2025, whereas cold-chain logistics is poised to advance at a 5.57% CAGR through 2031.

- By product type, prescription drugs secured a 30.60% revenue share of the pharmaceutical logistics market size in 2025; cell & gene therapies are projected to expand at a 6.12% CAGR to 2031.

- By geography, Europe led with 31.70% of the pharmaceutical logistics market share in 2025, while Asia-Pacific is expanding at a 5.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmaceutical Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of online pharmacies | +0.8% | Global, with early gains in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising OTC-medicine demand & chronic-disease burden | +0.6% | Global, concentrated in aging populations across developed markets | Long term (≥ 4 years) |

| Acceleration of biologics & vaccine cold-chain needs | +1.2% | Global, with emphasis on North America, Europe manufacturing hubs | Short term (≤ 2 years) |

| Outsourcing surge to 3PL/4PL specialists | +0.9% | Global, particularly strong in Asia-Pacific and North America | Medium term (2-4 years) |

| Mandatory end-to-end IoT / blockchain track-and-trace | +0.7% | North America & EU regulatory leadership, spillover to APAC | Medium term (2-4 years) |

| Net-zero logistics investments driving infrastructure renewal | +0.5% | Global, with EU and North America leading sustainability mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Online Pharmacies

Nearly half of consumers now prefer ordering medicines online, compelling carriers to engineer door-step delivery networks that secure 2 °C–8 °C conditions for sensitive products. Providers in Asia-Pacific leverage digital payments and telehealth platforms to scale ambient and refrigerated parcel services, while U.S. integrators enhance last-mile visibility through IoT-enabled pack-out solutions. Regulators have responded by extending serialization and track-and-trace to the single-unit level, raising compliance hurdles but also differentiating operators that offer real-time temperature and location data. As e-pharmacy volumes climb, network redesign toward micro-fulfillment hubs tightens lead-times, improving medication adherence and fueling incremental demand across the pharmaceutical logistics market.

Rising OTC-Medicine Demand & Chronic-Disease Burden

OTC formulations carry less-stringent handling rules than prescription drugs, enabling blended transport lanes that cut storage costs for integrated distributors. However, the rising prevalence of diabetes and cardiovascular disease forces continual replenishment cycles that intensify throughput requirements for time-critical inventory. Logistics partners exploit automation, such as robotic pick-and-pack and smart blister packaging, to combine OTC and chronic-care medications within unified flows that reduce dwell time. Hybrid models improve asset utilization and sustain profitability within the pharmaceutical logistics market while enhancing service quality for pharmacies and clinics.

Acceleration of Biologics & Vaccine Cold-Chain Needs

Sixty percent of new drug approvals anticipated by 2030 involve biologics or gene therapies that require 2 °C–8 °C or even −196 °C cryogenic preservation. DHL earmarked EUR 2 billion (USD 2.08 billion) to enlarge GDP-certified hubs and liquid-nitrogen capabilities, underscoring investment urgency. Advanced therapy medicinal products also demand synchronized pickup and patient infusion, driving real-time control-tower solutions that triangulate manufacturing slots, flight availability, and clinical appointments. These rigorously timed moves create premium-yield lanes that reinforce overall expansion of the pharmaceutical logistics market.

Outsourcing Surge to 3PL/4PL Specialists

Temperature-controlled warehousing, global trade compliance, and specialty packaging now require expertise beyond the scope of most drug manufacturers. Pharmaceutical firms, therefore, award multi-year contracts to integrators and specialty forwarders that bundle regulatory know-how with worldwide infrastructure. Fourth-party logistics orchestrators aggregate multiple providers and furnish a single visibility layer, lowering complexity for brand owners and strengthening market stickiness for service partners[1]“Direct To Patient, Clinical Trial Supply Chain,” World Courier, worldcourier.com. The shift elevates recurring revenues and supports sustained capital deployment across the pharmaceutical logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of temperature-controlled distribution | -0.9% | Global, with acute impact in emerging markets lacking infrastructure | Short term (≤ 2 years) |

| Complex & divergent global compliance standards | -0.6% | Global, with particular complexity in cross-border operations | Medium term (2-4 years) |

| Shortage of advanced phase-change packaging materials | -0.4% | Global, with supply constraints affecting specialized cold-chain applications | Short term (≤ 2 years) |

| Last-mile biologic delivery bottlenecks in emerging markets | -0.3% | APAC, MEA, Latin America with infrastructure limitations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Temperature-Controlled Distribution

Cold-chain failures cost drug makers an estimated USD 35 billion each year, reflecting write-offs, repackaging, and penalty shipments. Passive packaging with phase-change materials can extend protection to 96 hours but often doubles per-parcel expenses, placing strain on emerging-market programs where funding is scarce. The need for redundant monitoring equipment and qualified staff compounds overhead, limiting profit margins for smaller carriers within the pharmaceutical logistics market. Innovation in low-carbon refrigerants and reusable totes aims to reduce cost per shipment, yet wide deployment remains constrained by initial capital outlay.

Complex & Divergent Global Compliance Standards

EU GDP, U.S. DSCSA, and a patchwork of Asia-Pacific rules force operators to maintain multiple label formats, validation documents, and data-exchange protocols. Serialization interoperability challenges persist, especially when blockchain pilots operate alongside linear barcode systems, creating duplication and risk of data mismatch[2]“GMP Update 2024/2025,” ECA Academy, gmp-journal.com. Brexit-driven license splitting and new Latin American import rules further strain resources, leading some mid-sized forwarders to exit certain corridors. Harmonization efforts progress slowly, keeping compliance costs elevated across the pharmaceutical logistics market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominates While Value-Added Services Accelerate

Transportation generated 51.40% of 2025 revenue, illustrating that physical movement remains the backbone of the pharmaceutical logistics market. Road freight captures regional flows, particularly across Europe and North America, while air freight underpins long-haul biologics replenishment with next-day service guarantees. Ocean lanes gain relevance as shippers pursue sustainable options, leveraging GDP-compliant reefer containers to curb emissions.

Value-added services, growing at a 4.42% CAGR, include labeling, secondary packaging, order kitting, and serialization consulting that relieve manufacturers of non-core tasks. Demand rises fastest in Asia-Pacific, where contract manufacturers seek single-source partners to handle regulatory printing in multiple languages. As data integrity rules tighten, certified relabeling and tamper-evident pack-outs transform from optional extras into procurement prerequisites, driving incremental margin across the pharmaceutical logistics market.

Note: Segment shares of all individual segments available upon report purchase

By Mode of Operation: Cold-Chain Expansion Redefines Asset Allocation

Non-cold-chain flows still comprise 64.20% of 2025 throughput, yet cold-chain volumes expand faster as biologics, vaccines, and specialty injectables proliferate. Dedicated 2 °C-8 °C cross-dock corridors integrate real-time telemetry, allowing proactive intervention before excursions occur. Hybrid DCs equipped with multi-zone chambers optimize footprint, enabling operators to toggle between ambient and refrigerated storage within the same building to protect the pharmaceutical logistics market size.

Ultra-low and cryogenic services form a high-margin micro-segment. UPS’s acquisition of Frigo-Trans and BPL adds bulk liquid-nitrogen capacity and 24/7 command centers. Passive packaging innovations, vacuum-insulated panels, PCM bricks, and nitrogen-charged dewars, extend lane coverage in regions where active containers are unavailable, enhancing service density and supporting broader pharmaceutical logistics market growth.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Cell & Gene Therapies Trigger Premium Service Demand

Prescription drugs represented 30.60% of the 2025 value and continue to leverage mature distribution protocols that balance cost and quality. However, precision-medicine launches complicate ambient routing as a rising share of prescription items requires refrigerated handling.

Cell & gene therapies, forecast to rise at a 6.12% CAGR, demand cryogenic preservation, chain-of-identity safeguards, and synchronized pick-up at manufacturing suites minutes after release. Providers that embed validated −196 °C holding rooms and GPS-enabled dry shippers command premium rates, reinforcing differentiation within the pharmaceutical logistics market. Broader biologics and biosimilar portfolios further enlarge cold-chain lane density, permitting economies of scale in dry-ice replenishment, PCM pooling, and validated lane certification.

Geography Analysis

Europe maintained a 31.70% revenue share in 2025, underpinned by harmonized GDP enforcement, dense road networks, and large-scale manufacturing clusters in Germany, Switzerland, and Ireland. Investment in cross-border rail-air corridors supports modal shifts that lower emissions without compromising lead times. The pharmaceutical logistics market size in Europe benefits from continual capacity additions such as Cold Chain Technologies’ new Netherlands hub, which augments regional PCM production and reduces transit risk.

North America remains a powerhouse thanks to DSCSA-driven serialization maturity and sustained public-sector funding for pandemic preparedness. DHL allocated 50% of its EUR 2 billion (USD 2.08 billion) plan to U.S. and Canadian facilities, integrating solar-powered warehouses and LNG trucks that curb emissions while preserving service standards. Combined with FedEx’s USD 440 million expansion of healthcare distribution centers, the region continues to redefine best practices around data visibility and sustainability.

Asia-Pacific is expected to post the fastest growth at 5.02% CAGR from 2026 to 2031, buoyed by increased production out of China and India, widening insurance coverage, and e-pharmacy proliferation. Governments incentivize cold-chain upgrades, as evidenced by India’s 2025 tax rebates on GDP-compliant warehousing equipment. Regional carriers deploy rail-truck sea-air solutions along the China-Europe corridor, trimming cost and cutting transit emissions. Middle East & Africa trail in infrastructure, yet Gulf Cooperation Council localization programs spur warehouse investment, securing future pharmaceutical logistics market expansion.

Competitive Landscape

Consolidation accelerates as capital-intensive temperature-controlled assets raise barriers to entry. DHL’s EUR 2 billion (USD 2.08 billion) pledge through 2030 spans new GDP hubs in Chicago, São Paulo, and Singapore, while UPS’s USD 1.6 billion purchase of Andlauer Healthcare Group widens Canadian cryogenic reach. FedEx counters with expansions that add redundant power and automated picking tailored to clinical-trial returns.

Niche specialists such as Cryoport anchor the ultra-cold segment by combining validated dewars with 24/7 control towers, often partnering with integrators for first-mile collection. IoT start-ups like Controlant supply disposable trackers that feed real-time data into cloud dashboards, enabling predictive interventions that reduce excursion risk. Blockchain pilots led by TraceLink and IBM receive FDA endorsement, positioning compliant platforms as key differentiators in upcoming DSCSA milestones.

Competitive intensity also rises among cold-storage REITs—Lineage, Americold, and Nichirei—as they purchase regional facilities to embed pharmaceutical-grade chambers into wider food networks, boosting utilization and diversifying revenue. Overall, differentiation hinges on global reach, validated cold-chain capacity, and integrated digital visibility that collectively strengthen customer lock-in and expand the pharmaceutical logistics market.

Pharmaceutical Logistics Industry Leaders

Deutsche Post DHL

Kuehne + Nagel

UPS

FedEx

Nippon Express

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: FedEx reported securing nearly USD 400 million in new healthcare contracts, underscoring heightened demand for pharma-grade distribution.

- January 2025: UPS completed the Andlauer Healthcare Group acquisition for CAD 2.2 billion (USD 1.6 billion), enhancing its Canadian temperature-controlled logistics reach.

- January 2025: DHL Group announced a EUR 2 billion (USD 2.08 billion) investment in DHL Health Logistics to expand GDP-certified hubs, with 50% allocated to the Americas.

- April 2024: CEVA Logistics inaugurated an 18,000 m² Tarragona facility with 50 docks and BREEAM “Excellent” certification to bolster Iberian pharmaceutical capacity.

Global Pharmaceutical Logistics Market Report Scope

Pharmaceutical logistics involves manufacturing, processing, and shipping materials and resources. Pharmaceutical logistics companies also undertake activities related to handling finished products for customers.

Transporting healthcare products by different modes requires the establishment of complex logistical methods to maintain the integrity of a pharmaceutical shipment. It requires specific equipment, storage facilities, harmonized handling procedures, and strong cooperation among the cold chain partners. Logistics companies play a vital role in the functioning of pharmaceutical companies.

A complete background analysis of the global pharmaceutical logistics market, which includes an assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for critical segments, emerging trends in the market segments, market dynamics, and the impact of COVID-19, is covered in the report.

The report covers pharma logistics companies, and the market is segmented by product (generic drugs and branded drugs), mode of operation (cold chain transport and non-cold chain transport), application (biopharma, chemical pharma, and specialized pharma), mode of transport (air, rail, road, and sea), and geography (North America, Europe, Asia-Pacific, Latin America, and the Rest of the World). The report offers the market size in value terms in USD for all the segments mentioned above.

By Service Type

| Transportation | Road Freight |

| Air Freight | |

| Sea Freight | |

| Rail Freight | |

| Warehousing & Storage | |

| Value-added Services and Others |

By Mode of Operation

| Cold-Chain Logistics |

| Non-Cold-Chain Logistics |

By Product Type

| Prescription Drugs |

| OTC Drugs |

| Biologics & Biosimilars |

| Vaccines & Blood Products |

| Clinical Trail Materials |

| Cell & Gene Therapies |

| Medical Devices & Diagnostics |

| Veterinary Medicine |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Service Type | Transportation | Road Freight |

| Air Freight | ||

| Sea Freight | ||

| Rail Freight | ||

| Warehousing & Storage | ||

| Value-added Services and Others | ||

| By Mode of Operation | Cold-Chain Logistics | |

| Non-Cold-Chain Logistics | ||

| By Product Type | Prescription Drugs | |

| OTC Drugs | ||

| Biologics & Biosimilars | ||

| Vaccines & Blood Products | ||

| Clinical Trail Materials | ||

| Cell & Gene Therapies | ||

| Medical Devices & Diagnostics | ||

| Veterinary Medicine | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

How large is the pharmaceutical logistics market in 2026?

The pharmaceutical logistics market size is USD 591.48 billion in 2026 and is forecast to grow at a 5.47% CAGR to 2031.

Which service segment generates the most revenue?

Transportation services account for 51.40% of 2025 revenue, reflecting the sector’s core requirement for global product movement.

Why is cold-chain capacity expanding so rapidly?

Biologics, vaccines, and cell & gene therapies require temperatures from 2 °C to −196 °C, pushing carriers to add cryogenic storage, IoT monitoring, and GDP-certified hubs that drive 5.57% CAGR in cold-chain services.

Which region is growing fastest?

Asia-Pacific leads in growth at a 5.02% CAGR through 2031, supported by expanding drug manufacturing in China and India and broader healthcare access.

What is the key challenge to global pharmaceutical logistics compliance?

Divergent regulations, EU GDP, U.S. DSCSA, and varying Asia-Pacific rules, force operators to maintain multiple tracking standards and validation documents, elevating cost and complexity.

Page last updated on: