Low Voltage Electric Drives Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.13 Billion |

| Market Size (2031) | USD 21.54 Billion |

| Growth Rate (2026 - 2031) | 4.69% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Low Voltage Electric Drives Market Analysis by Mordor Intelligence

The low voltage electric drives market size is expected to increase from USD 16.35 billion in 2025 to USD 17.13 billion in 2026 and reach USD 21.54 billion by 2031, growing at a CAGR of 4.69% over 2026-2031. Regulatory mandates for motor-system efficiency are shortening replacement cycles, while discrete manufacturers are specifying servo architectures that traditional AC units cannot match for precision or response time. Silicon-carbide and gallium-nitride modules are shrinking cabinet footprints, yet premium pricing still limits penetration to high-power and high-accuracy segments. Rising cybersecurity compliance costs under IEC 62443 and the EU NIS2 Directive are adding non-trivial capital to connected-drive projects, nudging smaller operators toward pay-per-use models. Competitive pressure is intensifying as Chinese vendors undercut incumbents by 25% to 30%, prompting established suppliers to bundle drives with digital monitoring platforms that lock in service revenues.

Key Report Takeaways

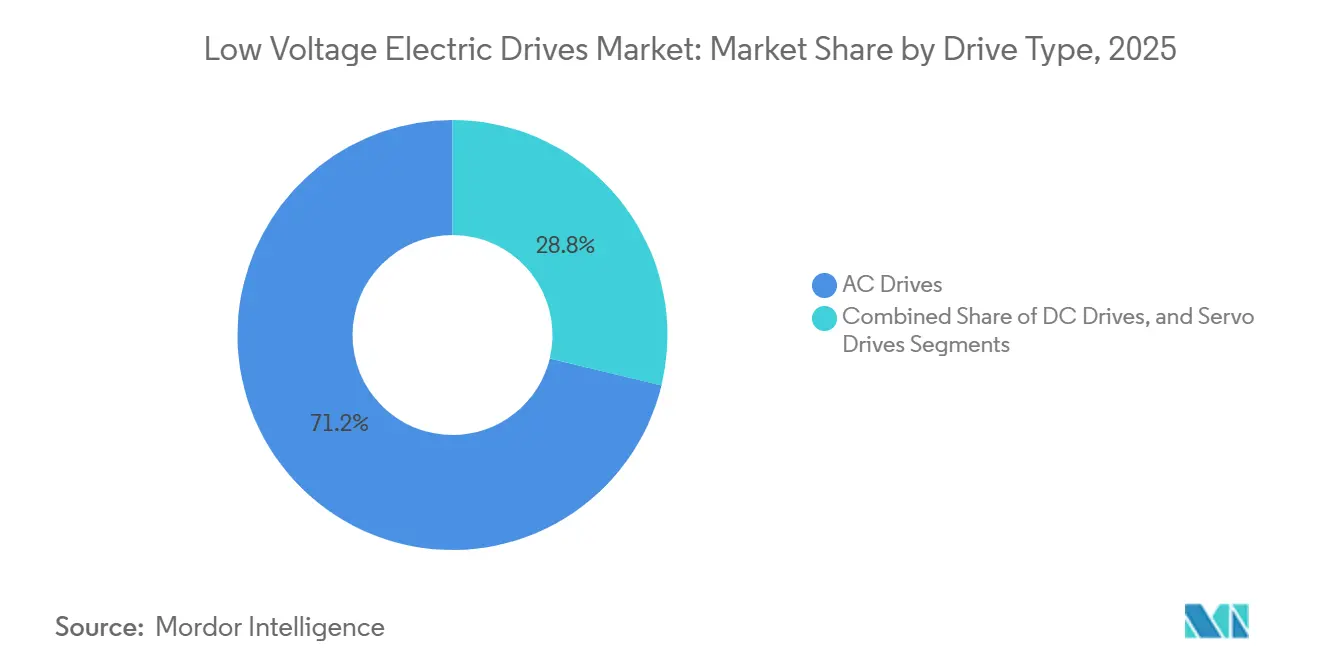

- By drive type, AC architectures led with 71.23% of the low voltage electric drives market share in 2025. Servo drives are projected to post the fastest growth at an 8.41% CAGR through 2031.

- By power rating, low-power units below 40 kW controlled 45.63% of the low voltage electric drives market size in 2025, whereas drives above 100 kW are on track to expand at 7.33% CAGR to 2031.

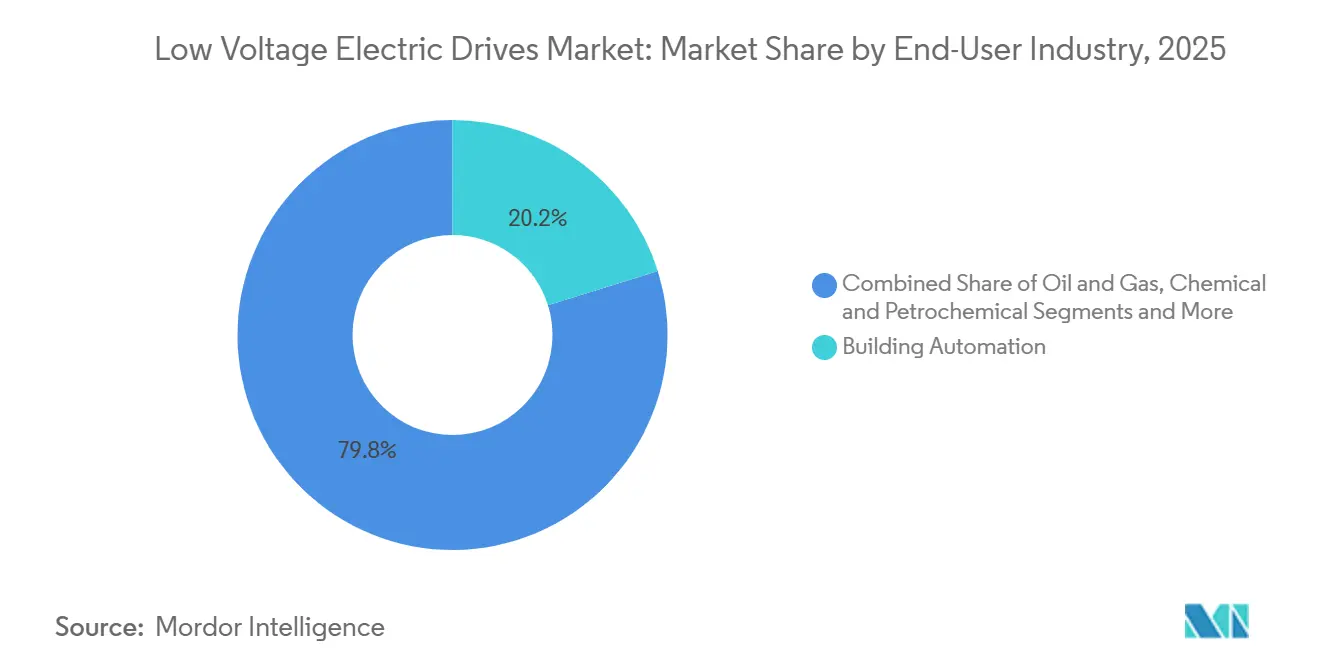

- By end-user industry, automotive and EV manufacturing accounted for the highest forecast CAGR at 8.98% from 2026-2031, while HVAC and building services contributed 20.18% of 2025 revenue.

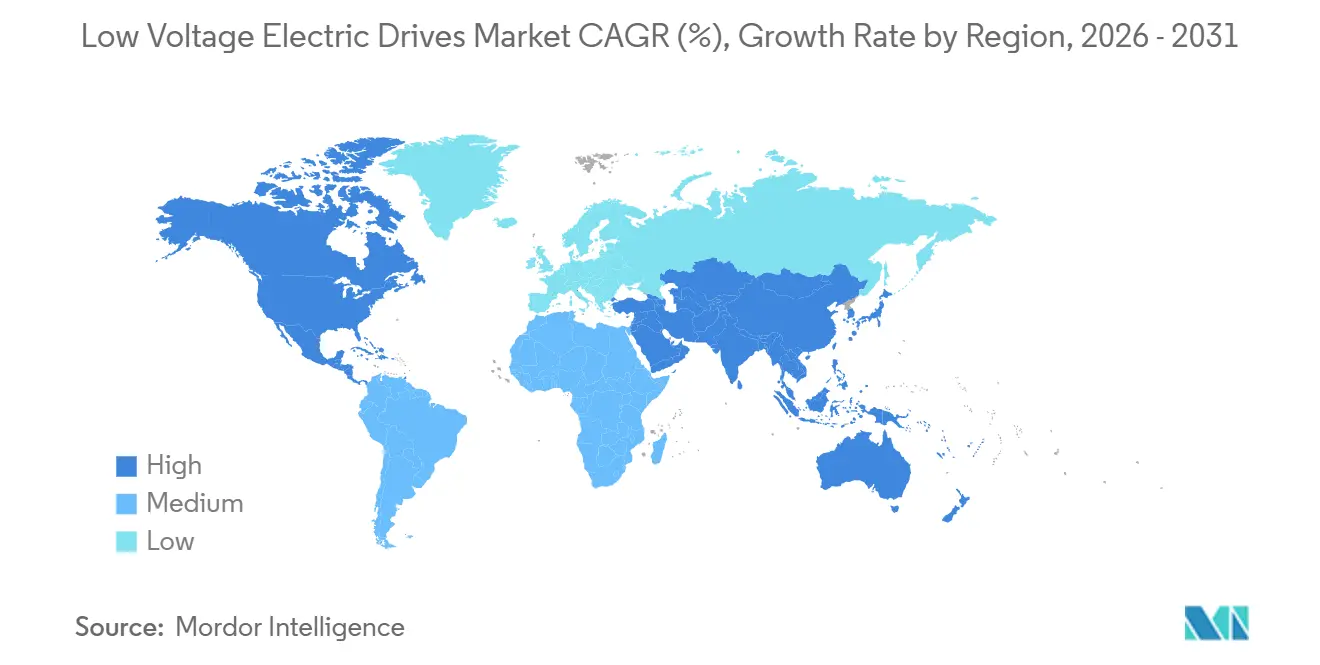

- By Geography, Asia-Pacific captured 47.41% of 2025 revenue and is estimated to grow at 7.11% CAGR, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Low Voltage Electric Drives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory Energy-Efficiency Regulations for Industrial Motors | 1.2% | Global, with EU and China leading enforcement | Medium term (2-4 years) |

| Rapid Automation in Discrete Manufacturing and Packaging Lines | 1.0% | Asia-Pacific core, spill-over to North America and EU | Short term (≤ 2 years) |

| Expansion of HVAC Retrofits for Building Decarbonisation | 0.8% | Europe and North America, emerging in Middle East | Medium term (2-4 years) |

| Rise of Compact Integrated-Motor-Drive Architectures | 0.6% | Global, concentrated in HVAC and pump applications | Long term (≥ 4 years) |

| Adoption of SiC/GaN Power Modules Enabling Smaller LV Drives | 0.5% | North America, Europe, Japan | Long term (≥ 4 years) |

| Emergence of Pay-per-Use Drive-as-a-Service Business Models | 0.3% | Europe and North America pilot markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Energy-Efficiency Regulations for Industrial Motors

New IE5 classifications in IEC 60034-30-1:2025 and system-level ratings in IEC 61800-9-2 are significantly driving the replacement of older IE2 motors. The EU's Ecodesign Regulation 2021/341 and China's GB 18613-2020 have effectively rendered inefficient motors obsolete, creating a surge in retrofit demand. These retrofits can result in substantial cost savings, with approximately USD 2,400 saved annually on a 100 kW machine operating for 6,000 hours. Additionally, sites certified under ISO 50001 are at risk of facing audit penalties if they continue to operate non-compliant assets. Furthermore, the EU Taxonomy directly links green-bond eligibility to documented energy savings achieved through drive systems, emphasizing the critical financial implications of adhering to these regulations and standards.[1]European Commission, “Ecodesign Regulation 2021/341,” europa.eu

Rapid Automation in Discrete Manufacturing and Packaging Lines

In the Asia-Pacific region, the demand for servo systems is experiencing significant growth, primarily driven by the increasing need for high precision and speed in various industries. Electronics, textiles, and food-packaging plants now require systems capable of achieving ±0.01 mm accuracy and sub-200 millisecond cycles, which has been a major factor contributing to the rising adoption of servo systems. Yaskawa, a prominent player in the servo market, reported a notable 23% year-on-year increase in servo shipments to China during fiscal 2025. A substantial portion of these shipments was utilized in applications such as smartphone manufacturing and battery-module assembly, highlighting the growing importance of servo systems in advanced production processes. The adoption of converging industrial-Ethernet protocols has further enhanced operational efficiency by significantly reducing commissioning time, achieving a 40% decrease. This technological advancement has streamlined processes and improved productivity across industries. Moreover, the introduction of outcome-based leasing models has provided smaller firms with an opportunity to adopt servo systems without the burden of high upfront capital investment. These models allow companies to pay based on output units, effectively lowering the financial barriers to entry and enabling broader adoption of advanced automation solutions.

Expansion of HVAC Retrofits for Building Decarbonisation

By 2030, all new constructions in the European Union must achieve near-zero-emission status, as mandated by the EU Energy Performance of Buildings Directive 2024/1275. This directive is significantly driving the adoption of variable-frequency drives (VFDs) in chillers and air handlers to meet stringent energy efficiency requirements. In the United States, the Infrastructure Investment and Jobs Act is allocating USD 3.5 billion towards efficiency upgrades in public buildings. A major focus of this initiative is on installing VFDs, which have the potential to deliver substantial energy savings of 40% on standard 50 kW fan motors, thereby reducing operational costs and environmental impact. Meanwhile, Saudi Arabia's Green Building Code is creating an additional demand for 120,000 units annually, further emphasizing the global momentum toward retrofitting and energy-efficient solutions in the construction sector.

Rise of Compact Integrated-Motor-Drive Architectures

By embedding inverters within motor housings, Danfoss and Nidec have significantly streamlined installation processes, achieving a 30% reduction in labor time while also eliminating the need for external cabling.[2]Danfoss A/S, “VLT Integrated Servo Drive Launch,” danfoss.com This innovative approach to design not only simplifies installation but also offers substantial space savings, making it particularly advantageous for applications in building basements and offshore rigs, where the cost of cabinets can be prohibitively high. However, this advancement comes with a notable drawback: if an inverter experiences a fault, the entire unit must be replaced, which can increase maintenance costs and downtime. Despite this limitation, Chinese manufacturers such as Inovance are enhancing the value proposition by offering comparable units at prices that are approximately 20% lower than those of Western counterparts, making them an attractive option in the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Low-Harmonic Premium Drives | -0.7% | Global, acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Global Semiconductor Shortages Constraining Drive Production | -0.5% | Global, concentrated in SiC/GaN module supply | Medium term (2-4 years) |

| Skill Gap in Tuning VFDs for Variable-Torque Applications | -0.4% | North America, Europe, Middle East | Medium term (2-4 years) |

| Escalating Cybersecurity-Compliance Costs for IIoT-Connected Drives | -0.3% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Low-Harmonic Premium Drives

Active-front-end or multi-level designs are highly effective in reducing total harmonic distortion to below 5%. However, these advanced designs come with a significantly higher price tag, costing 40%-60% more than their six-pulse counterparts. This substantial cost premium creates a notable challenge for utilities and municipal water plants, particularly those operating under constrained financial conditions and tight budgets. The high initial investment required for these designs often deters organizations from adopting them, despite their technical advantages. Although leasing programs are available to alleviate the upfront financial burden, their adoption has been relatively slow. This slow uptake is especially evident in regions where power-quality regulations and enforcement remain weak or inconsistent, further hindering the widespread implementation of these advanced designs. As a result, many organizations continue to rely on less expensive alternatives, even if they do not offer the same level of performance or efficiency.

Escalating Cybersecurity-Compliance Costs for IIoT-Connected Drives

Secure firmware is mandated by IEC 62443-4-2, which ensures the protection of industrial systems against cyber threats. Additionally, the EU NIS2 directive imposes strict requirements, including regular audits and mandatory breach reporting within 24 hours of detection. For mid-sized facilities, the integration of industrial firewalls and demilitarized zones incurs significant costs, ranging between USD 50,000 and 200,000. These expenses often pose a financial challenge for smaller manufacturers, leading to delays in their adoption of cloud migration strategies.[3]European Commission, “NIS2 Directive Overview,” europa.eu

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drive Type: Servo Precision Reshapes Automation Economics

Despite AC drives commanding a dominant 71.23% of the revenue in 2025, servo units emerged as the fastest-growing segment in the low voltage electric drives market, boasting a projected CAGR of 8.41% from 2026 to 2031. While AC architectures prove cost-effective for pumps and conveyors, servo platforms, with their 0.01-degree resolution and 1-millisecond settling times, cater to the precise demands of smartphone and wearable devices, as well as battery-module assembly lines. These features make servo units indispensable in industries requiring high precision and rapid response times, further driving their adoption across various applications.

Yaskawa's Sigma-7 series, now featuring AI-driven vibration suppression that reduces mechanical resonance by 50%, is making inroads into China's bustling electronics hubs. This innovation enhances operational efficiency and minimizes downtime, making it a preferred choice for manufacturers in competitive markets. The allure of the integrated-motor-drive concept is undeniable: Nidec's IMD servo, by cutting cabinet space requirements by 40%, has caught the attention of packaging and textile OEMs. This space-saving design not only optimizes factory layouts but also reduces installation costs, adding to its appeal. While Inovance exerts pricing pressure by slashing prices up to 30% compared to Japanese and European competitors, established players counterbalance this challenge, safeguarding their margins through enhanced software offerings and comprehensive lifecycle services. These strategies enable incumbents to maintain their competitive edge while addressing evolving customer needs in a dynamic market environment.

By Power Rating: High-Power Drives Gain as Heavy Industry Electrifies

High-power devices exceeding 100 kW are projected to grow at a 7.33% CAGR, significantly outpacing the average growth rate of the low voltage electric drives market. This notable growth is primarily driven by the increasing focus of miners, refiners, and LNG facilities on achieving Scope 2 decarbonization goals. For example, retrofitting a single 500 kW crusher can result in substantial annual savings of USD 80,000, assuming an energy cost of USD 0.10 per kWh. This retrofit not only delivers cost savings but also ensures a quick payback period of just three years, making it a highly attractive investment for industrial operators.

In 2025, Shell’s Prelude FLNG successfully reduced its auxiliary demand by 12 MW by installing 18 large drives, showcasing the potential of advanced drive technologies in optimizing energy consumption. SiC devices, which are at the forefront of innovation, offer an impressive efficiency of 98.5% and a smaller physical footprint, making them ideal for high-end applications. However, the higher cost of these devices has been a significant barrier to their full-scale adoption across industries. Mid-range units, typically ranging from 50-200 kW, are increasingly being deployed in extruders and blowers used in food, chemical, and plastics processing industries. These units deliver remarkable energy savings of 30%-50% when compared to traditional throttling control methods, providing both operational efficiency and cost benefits. Meanwhile, sub-5 kW drives are experiencing a resurgence in residential HVAC systems, where IMD solutions are proving to be highly effective. These solutions simplify installations in confined spaces, addressing a key challenge in residential applications and further driving the adoption of these compact drives.

By End-User Industry: Automotive and EV Manufacturing Accelerates Servo Adoption

With an 8.98% CAGR projected through 2031, automotive and EV manufacturing leads all user verticals, showcasing significant growth potential. At Tesla's Berlin facility, over 2,000 servo-driven robots operate, each requiring sub-millisecond synchronization to ensure optimal performance and efficiency. Meanwhile, BYD's ambitious goal of producing 3 million units by 2027 translates to a substantial demand for approximately 15,000 additional servo drives, highlighting the increasing reliance on advanced automation technologies in the automotive sector.

As retrofit mandates gain traction in the EU and the U.S., HVAC and building services captured 20.18% of the 2025 demand, underscoring their critical role in energy efficiency and sustainability initiatives. Oil and gas companies are actively transitioning to electrify their offshore platforms, aiming to reduce environmental impact and operational costs. Concurrently, under the updated Urban Wastewater Treatment Directive, water utilities are implementing VFDs, targeting a 30% reduction in energy intensity by 2030, which aligns with global sustainability goals. In Asia, discrete industries are witnessing a notable surge in servo adoption, driven by competitive demands for enhanced speed, precision, and accuracy, reflecting the region's growing focus on industrial automation and technological advancements.

Geography Analysis

Asia-Pacific owned 47.41% of the low voltage electric drives market in 2025 and is projected to expand at 7.11% CAGR through 2031. China’s dual-carbon policy enforces IE3 motor efficiency above 0.75 kW and targets a 13.5% energy-intensity cut by 2025, stimulating about 800,000 annual drive retrofits. India’s Production-Linked Incentive program funnels INR 738 billion (USD 8.9 billion) into electronics manufacturing, driving servo demand in surface-mount lines. Japan and South Korea supply high-precision servo exports, while Australia leans on VFDs for mining electrification.

Europe contributed 25% of 2025 revenue. The Ecodesign Regulation 2021/341 mandates VFD pairing with IE3 motors, and Directive 2024/1275 forces HVAC retrofits in buildings above 15 kW. Germany upgrades drives in automotive plants to meet Energiewende goals; the United Kingdom’s Ofwat links water-utility allowances to VFD-driven savings. Spain is emerging as an EV-component hub, drawing servo orders for new battery lines.

North America represented 22% in 2025. The U.S. IIJA funds HVAC and water VFD retrofits in federal buildings, while the CHIPS Act drives premium low-harmonic units for semiconductor fabs. Canada electrifies oil-sands operations, and Mexico benefits from nearshored EV capacity. The Middle East focuses on desalination and district cooling, whereas South Africa and Nigeria retrofit mining and cement plants with drives to curb diesel reliance.

Competitive Landscape

The low voltage electric drives market is moderately concentrated. The top five, ABB, Siemens, Schneider Electric, Danfoss and Rockwell Automation, held roughly 45%-50% combined revenue in 2025, but price aggression by Inovance and Hiconics is eroding share in Asia-Pacific and the Middle East. Incumbents differentiate via digital ecosystems such as ABB Ability, Siemens Xcelerator and Schneider EcoStruxure that bundle analytics, predictive maintenance and remote commissioning.

IMD solutions launched by Danfoss and Nidec have reduced installation labor by 30% and shrunk footprints by 40%, reshaping HVAC and pump value chains. Silicon-carbide modules serve as another wedge: ABB’s ACS880 reaches 98.5% efficiency, yet high device costs confine uptake to premium tiers. Japanese servo specialists, Yaskawa, Mitsubishi Electric, and Fuji Electric, maintain technical leadership yet face mid-tier pricing pressure.

Outcome-based pricing is emerging; Schneider’s Drive-as-a-Service spreads costs into operating budgets, potentially expanding penetration among cash-constrained users. Cybersecure-by-design credentials under IEC 62443 are becoming a buying criterion for water, energy and transport operators, favoring vendors that integrate encrypted boot and vulnerability disclosure. Indian producer CG Power is scaling under a domestic PLI scheme to address local infrastructure builds.

Low Voltage Electric Drives Industry Leaders

ABB Limited

Siemens AG

Schneider Electric SE

Danfoss A/S

Rockwell Automation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Siemens launched Sinamics G120X drives with AI-based predictive maintenance for HVAC and water clients.

- December 2025: ABB bought ASTI Mobile Robotics for USD 200 million to integrate AMR navigation with drive platforms.

- November 2025: Danfoss expanded its Tianjin plant, adding 500,000 units of annual capacity for Asia-Pacific HVAC markets.

- October 2025: Schneider Electric integrated EcoStruxure with Microsoft Azure for real-time multi-site drive optimization.

Global Low Voltage Electric Drives Market Report Scope

The study on the global low-voltage electric drive market contains a detailed segmentation by type, end-user, and geography. Several incentive programs in the United States and Europe to replace low-efficiency electric motors early will likely stimulate demand for low-voltage AC drives. Furthermore, due to the increasing implementation of Industry 4.0 policies, there is a significant demand for automation in the manufacturing, power generation, metal and mining, and discrete industry sectors.

The Global Low Voltage Electric Drives Market Report is Segmented by Drive Type (AC Drives, DC Drives, Servo Drives), Power Rating (Up to 5 kW, 5-50 kW, 50-200 kW, Above 200 kW), End-User Industry (Automotive and EV Manufacturing, Oil and Gas, Chemical and Petrochemical, Food and Beverage, Water and Wastewater, Power Generation, Metals and Mining, Pulp and Paper, HVAC and Building Services, Discrete Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| AC Drives |

| DC Drives |

| Servo Drives |

| Up to 5 kW |

| 5 – 50 kW |

| 50 – 200 kW |

| Above 200 kW |

| Automotive and EV Manufacturing |

| Oil and Gas |

| Chemical and Petrochemical |

| Food and Beverage |

| Water and Wastewater |

| Power Generation |

| Metals and Mining |

| Pulp and Paper |

| HVAC and Building Services |

| Discrete Industries (Electronics, Packaging, Textiles) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Drive Type | AC Drives | ||

| DC Drives | |||

| Servo Drives | |||

| By Power Rating | Up to 5 kW | ||

| 5 – 50 kW | |||

| 50 – 200 kW | |||

| Above 200 kW | |||

| By End-User Industry | Automotive and EV Manufacturing | ||

| Oil and Gas | |||

| Chemical and Petrochemical | |||

| Food and Beverage | |||

| Water and Wastewater | |||

| Power Generation | |||

| Metals and Mining | |||

| Pulp and Paper | |||

| HVAC and Building Services | |||

| Discrete Industries (Electronics, Packaging, Textiles) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What CAGR is projected for the low voltage electric drives market between 2026 and 2031?

A 4.69% CAGR is forecast for 2026-2031 based on Mordor Intelligence data.

Which region will add the most incremental revenue through 2031?

Asia-Pacific, expanding at a 7.11% CAGR on the back of China’s dual-carbon mandates and India’s PLI incentives.

Why are servo drives growing faster than traditional AC drives?

Servo platforms deliver sub-millisecond precision critical for electronics and EV battery lines, driving an 8.41% CAGR that outpaces AC units.

How do integrated-motor-drive systems benefit HVAC retrofits?

IMD units remove external cabling, cut installation labor by 30% and shrink cabinet space by 40%, easing upgrades in tight plant rooms.

Page last updated on: