Gyroscopes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.56 Billion |

| Market Size (2031) | USD 6.13 Billion |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

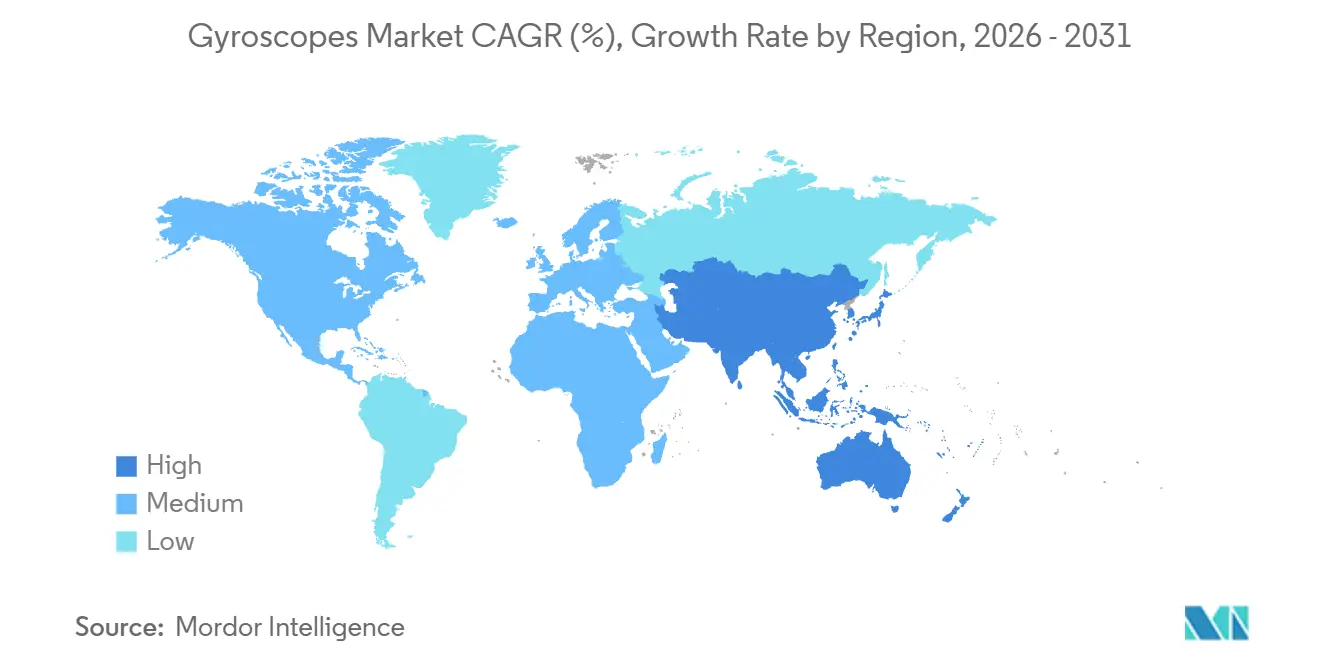

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

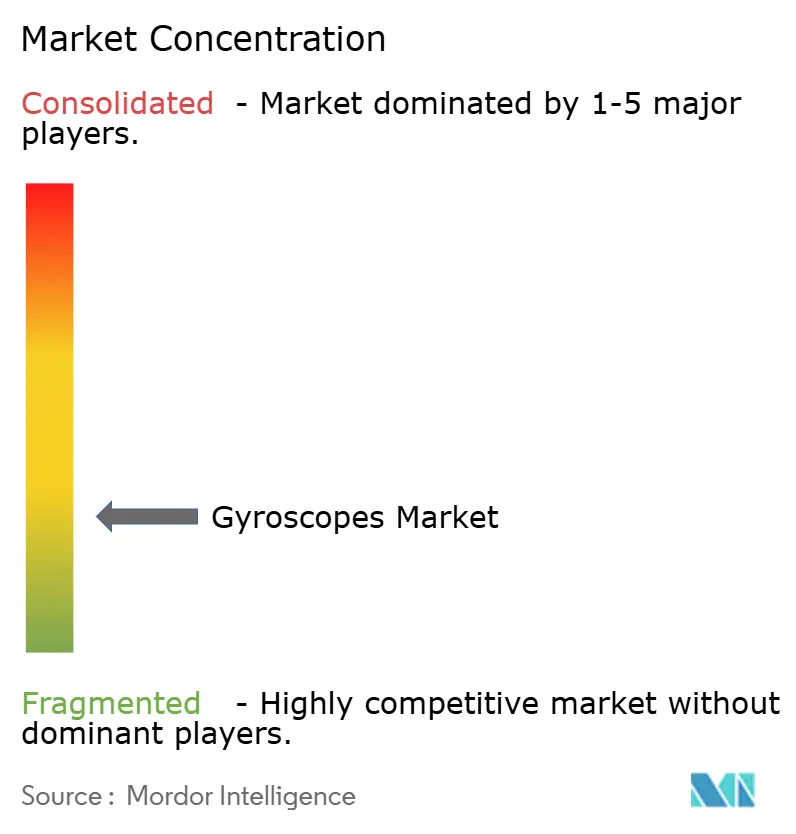

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gyroscopes Market Analysis by Mordor Intelligence

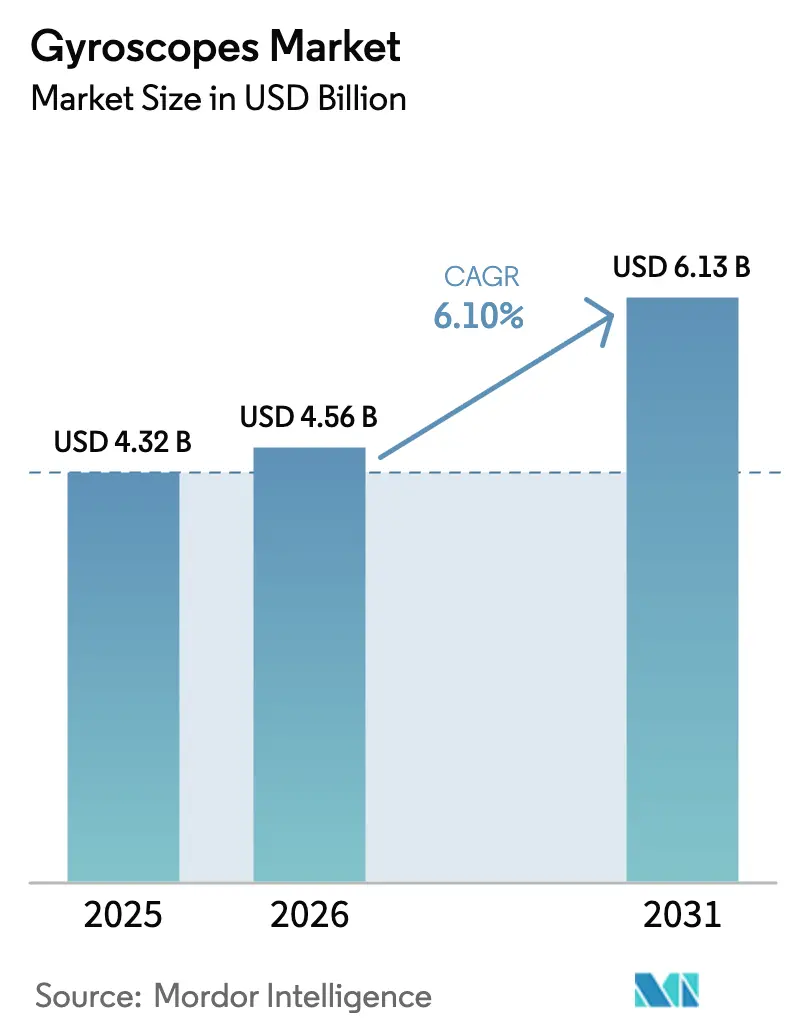

The gyroscopes market size is expected to increase from USD 4.32 billion in 2025 to USD 4.56 billion in 2026 and reach USD 6.13 billion by 2031, growing at a CAGR of 6.10% over 2026-2031. Demand is steadily shifting away from volume-driven consumer devices toward precision-oriented deployments in advanced driver assistance, defense navigation, and industrial automation, all of which demand tighter drift, higher bias stability, and multi-sensor fusion. MEMS miniaturization has advanced to the point where sub-degree accuracy is feasible in wafer-level chip-scale packages, opening doors that were once controlled by bulky ring-laser or fiber-optic platforms. Regional manufacturing synergies, particularly in Asia-Pacific, support high-volume output, while North American and European firms continue to set performance and certification benchmarks. Market concentration remains low, yet photonic integrated circuit start-ups are challenging incumbents on cost-to-precision ratios. Strategic bottlenecks in specialty optical fiber and high-Q resonator materials add supply risk but also encourage vertical integration.

Key Report Takeaways

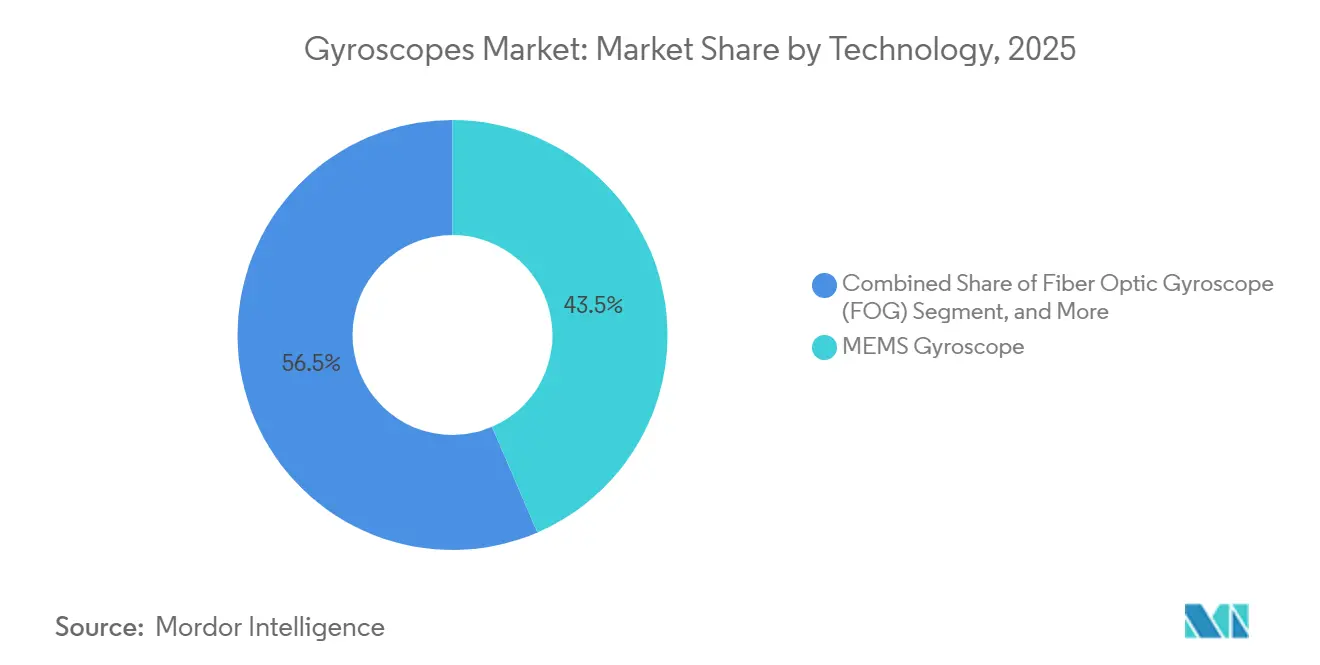

- By technology, MEMS held 43.53% of the gyroscopes market share in 2025, while fiber-optic devices are tracking a 7.85% CAGR through 2031.

- By axis configuration, 3-axis units led with 55.53% revenue in 2025; 2-axis devices are expanding at a 7.92% CAGR to 2031.

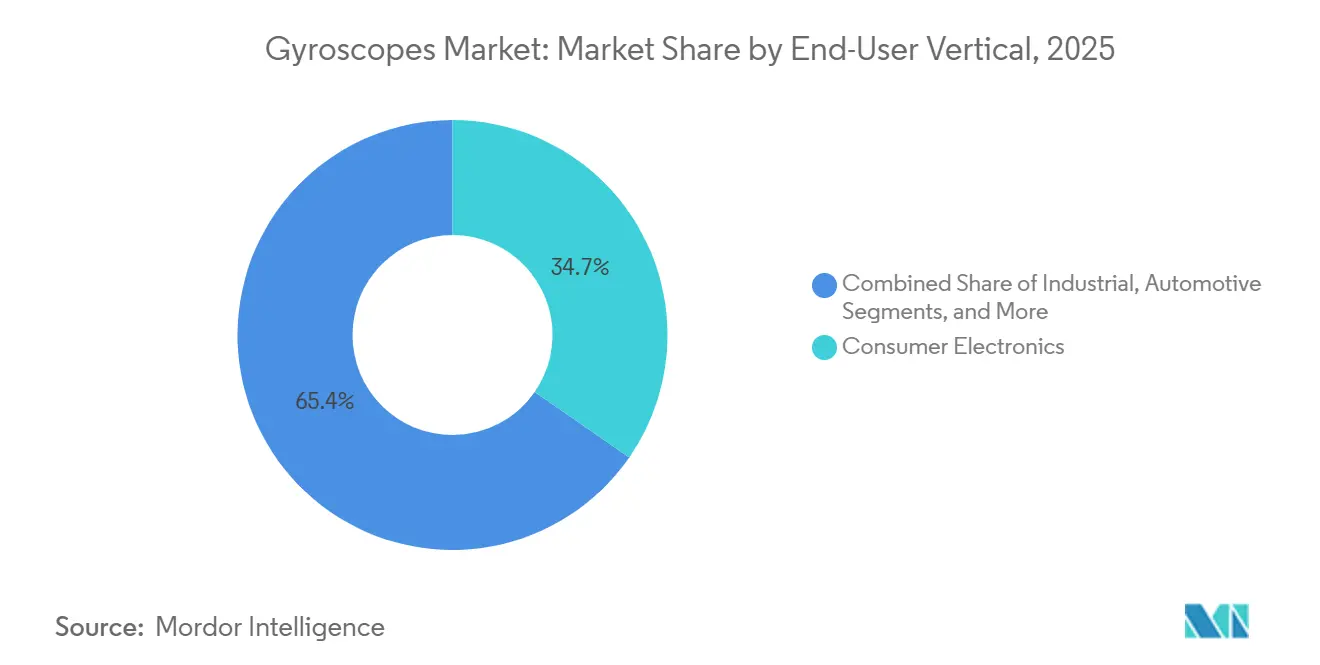

- By end-user, consumer electronics retained a 34.65% share in 2025, whereas industrial use is advancing at an 8.21% CAGR through 2031.

- By application, navigation systems captured 35.75% of the gyroscopes market in 2025, and gaming or virtual reality is growing at an 8.01% CAGR through 2031.

- By region, Asia-Pacific commanded a 40.42% share of the gyroscopes market in 2025 and is projected to grow at an 8.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gyroscopes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of MEMS Sensors in Smartphones and Wearables | +1.2% | Global, with APAC manufacturing concentration | Short term (≤ 2 years) |

| Automotive ADAS and Autonomous Driving Demand | +1.8% | North America and Europe leading, APAC following | Medium term (2-4 years) |

| Defense Modernization Programs in Emerging Economies | +1.0% | Middle East, Asia-Pacific, Eastern Europe | Long term (≥ 4 years) |

| Rapid Expansion of Commercial Drone Applications | +0.9% | Global, with regulatory leadership in North America and Europe | Medium term (2-4 years) |

| Cost Decline in Fiber-Optic and Ring-Laser Gyroscopes | +0.7% | Global, concentrated in defense and aerospace hubs | Long term (≥ 4 years) |

| Emergence of Quantum-Enhanced Inertial Navigation | +0.4% | North America, Europe, select APAC research centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of MEMS Sensors in Smartphones and Wearables

Six-axis MEMS hybrids are now shipping in flagship handsets and premium wearables, delivering sub-degree accuracy and a 40% reduction in footprint, which helps device makers maintain slim form factors without sacrificing motion fidelity.[1]STMicroelectronics, “ISM330BX Six-Axis IMU Datasheet,” st.com Closed-loop digital architectures reduce power draw while maintaining bias drift below 1°/h, enabling consumer suppliers to approach tactical-grade thresholds. Medical wearables add a new revenue tier that values low drift for FDA-approved patient monitoring. The result is a steady funnel of high-volume orders that anchors base demand, even as premium applications set loftier performance bars.

Automotive ADAS and Autonomous Driving Demand

Level 3 and Level 4 autonomy requires multi-sensor redundancy; thus, modern inertial modules must reach bias stability better than 10°/h, angular random walk below 0.1°-√h, and functional-safety diagnostics per ISO 26262.[2]Analog Devices, “High-Performance Inertial Sensors,” analog.com Electric vehicles further lean on precise rate feedback to optimize regenerative braking. Over-the-air calibration and self-test capabilities have become must-haves, giving suppliers that bundle MEMS gyros with on-board processors a competitive edge.

Defense Modernization Programs in Emerging Economies

New procurement cycles in India, Brazil, and Turkey are prioritizing indigenous inertial navigation systems for drones, guided munitions, and soldier systems. Specifications often require fiber-optic or ring-laser gyroscopes with bias instability of less than 1°/h and immunity to electromagnetic interference, favoring suppliers who can transfer technology without encountering export licensing hurdles. The appetite for local production creates joint-venture openings but also raises certification hurdles.

Rapid Expansion of Commercial Drone Applications

Precision agriculture, line inspection, and logistics drones now require gyros that maintain attitude accuracy through rapid altitude and temperature swings. ISO 24354-2023 mandates vibration tolerance and hot-swap capability, prompting MEMS manufacturers to ruggedize their designs.[3]ISO, “ISO 24354:2023 Payload Interface for Civil UAS,” iteh.ai Sensor-synchronized swarms benefit from built-in timing references, and urban air-mobility prototypes seek low-latency sensor fusion to navigate GPS-denied corridors, broadening the gyroscopes market footprint.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Manufacturing Complexity for High-Accuracy Gyroscopes | -1.4% | Global, concentrated in precision manufacturing hubs | Medium term (2-4 years) |

| Supply-Chain Volatility in Specialty Optical Fibers and ICs | -0.8% | Global, with acute impact in Asia-Pacific | Short term (≤ 2 years) |

| Certification Barriers in Aviation and Medical Markets | -0.6% | North America and Europe leading, global regulatory spillover | Long term (≥ 4 years) |

| Competition from Vision and GNSS-INS Hybrid Solutions | -0.5% | Global, with advanced markets leading adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Manufacturing Complexity for High-Accuracy Gyroscopes

Fiber-optic builds require optical fibers with a loss of ≤ 0.5 dB/m, while ring-laser cavities demand nanometer-grade machining, resulting in steep capital outlays and slow throughput. MEMS designs that aim for navigation-grade stability require vacuum wafer-level packaging and multi-point temperature compensation, lengthening production cycles and payback periods. Extended burn-in testing, which can sometimes last weeks, caps monthly volume and increases unit cost.

Supply-Chain Volatility in Specialty Optical Fibers and ICs

A handful of suppliers dominate the high-purity fiber and analog-to-digital converter markets. Telecom upswings or semiconductor shortages divert capacity, stretching lead times for gyroscope integrators. Rare-earth magnets and specialty glass compounds are geographically concentrated, so trade friction can cause material prices to spike suddenly, forcing OEMs to dual-source or near-shore at a higher cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: MEMS Dominance Faces Precision Challenge

MEMS devices accounted for 43.53% of the gyroscopes market share in 2025, a lead built on low cost and seamless SoC integration for phones, wearables, and cars. Fiber-optic designs, though pricier, are growing at a 7.85% CAGR as defense and aerospace buyers seek bias instability below 0.01°/h, a tolerance MEMS still rarely meet. Ring-laser and hemispherical resonator models protect smaller niches, such as high-g munitions and long-life satellites, where single-restart reliability outweighs bill-of-materials savings. Photonic integrated circuit prototypes have now logged less than 1°/h drift on footprints under 5 cm², hinting that chip-scale optics could soon bridge MEMS and fiber cost-to-precision gaps. MEMS engineers answer with cobweb-style disk resonators and multi-bit sigma-delta readouts, which have pushed bias noise toward navigation thresholds.

As hybrid stacks emerge, vendors that master both piezoelectric and photonic steps will control the most defensible intellectual property. Licensing paths are opening in the Asia-Pacific region, where fabs can co-package CMOS and optical waveguides, promising lower entry barriers for regional brands. Overall, the technology choice is shifting from a binary MEMS-versus-optics argument to a continuum of precision tiers that enable integrators to match cost, size, and environmental limits without switching suppliers mid-program.

By Axis: Multi-Axis Integration Drives Complexity

Three-axis chips captured 55.53% of 2025 revenue because phones, VR headsets, and full IMUs demand complete pitch-roll-yaw telemetry in a single die. Two-axis units nevertheless achieve the fastest 7.92% CAGR because automakers require only pitch and roll for electronic stability control and are cost-sensitive regarding yaw redundancy. Single-axis parts, once mainstream, now linger in high-speed spindles or scientific rigs where cross-axis coupling is unacceptable. Packaging advances enable a 3-axis MEMS to occupy the same board area as an older single-axis device, yet each axis still reacts differently to temperature. Therefore, vendors embed EEPROM calibration curves and on-die heaters to maintain drift parity. ISO 26262 diagnostics now monitor each axis separately, forcing firmware to flag latent faults before they trigger unstable vehicle dynamics.

In gaming, matched-axis latency tightens user comfort thresholds, pushing makers to align bandwidth and phase to the millisecond. Industrial buyers add vibration-hardening epoxy fill or ceramic carriers to stop resonance peaks that would otherwise amplify z-axis noise. As sensor-fusion processors mature, design wins increasingly hinge on how predictably each channel maintains linearity throughout the product’s life, rather than on the number of axes.

By End-User Vertical: Industrial Automation Accelerates

Consumer electronics dominated spending with 34.65% in 2025, but factory automation and robotics are pacing an 8.21% CAGR, a trend that widens the market size allocated to industrial OEMs. Collaborative robots weld, pick, and palletize with sub-degree orientation loops that tolerate eight-hour duty cycles, so buyers specify bias drift under 0.5°/h and vibration immunity past 2 kHz. Aerospace and defense continue to fund navigation-grade roadmaps, while marine surveyors demand hermetically sealed resonator units that survive salt fog and pressure cycling for years. Internet-of-Moving-Things trackers require less than 1 mW draw yet must hold heading in -40 °C to +85 °C swings, stretching process windows for temperature coefficient control.

Car OEMs are pushing over-the-air recalibration, allowing fleet software patches to realign IMUs without requiring dealer visits, thereby reinforcing the shift toward software-defined vehicles. Agricultural implement makers adopt tactical-grade gyros to level autonomous harvesters on uneven terrain, a frontier application that also values rugged IP-rated housings. Meanwhile, consumer brands continue to press for thinner, cheaper SKUs, driving wafer-level chip-scale packaging and 6-axis combinations that blend gyro and accelerometer dies. This demand dichotomy forces suppliers to fragment their product lines, pairing high-volume consumer fabs with smaller, tightly controlled tactical lines to maintain aerospace certifications.

By Application: Gaming Disrupts Navigation Dominance

Navigation systems retained 35.75% of 2025 revenue and anchor gyroscopes' market share across aircraft, ships, and strategic missiles; however, gaming and VR are growing at an 8.01% CAGR due to metaverse platform rollouts. Headset designers aim for latency under 1 ms and drift below 0.05°/min to maintain a stable virtual scene, thereby narrowing the performance gap with avionics. Drone gimbals utilize embedded IMUs to cancel vibration at up to 2 kHz, which is essential for 4K photogrammetry and LiDAR mapping. In contrast, inspection robots require repeatable heading in GPS-denied tunnels. Industrial automation lines rely on gyroscopes inside servo loops to stabilize robotic arms, thereby boosting first-pass yield in precision assembly.

Consumer smartphones, although flat in unit growth, still see volumes that amortize MEMS R&D across pricier niches. Autonomous delivery vehicles layer gyro data onto camera and radar feeds to keep parcels steady over potholes, a use case that favors 6-axis closed-loop MEMS. Finally, soldier-worn navigation kits blend gyros with magnetometers to track dismounted troops in urban canyons, underscoring how application diversity cushions the market from downturns in any single sector.

Geography Analysis

The Asia-Pacific region controlled 40.42% of the 2025 turnover, driven by semiconductor clustering in China, Japan, and South Korea, as well as India’s push for localized defense electronics. The region also posts the fastest 8.45% CAGR, a testament to domestic ecosystems that cover foundry services, packaging, and downstream system integration. Factory expansions in Taiwan and Malaysia promise additional MEMS capacity, but the same projects also increase local demand for high-purity precursor gases and lithography tooling, thereby gradually deepening the supply chain.

North America remains influential through its defense budgets, autonomous vehicle pilots, and a concentration of photonics start-ups. The Federal Aviation Administration’s TSO compliance templates elevate barrier costs, indirectly steering procurement toward incumbents familiar with paperwork. Parallel reshoring programs in New York and Arizona aim to rebuild the critical MEMS supply chain but face labor and utility-rate headwinds that may limit near-term throughput.

Europe emphasizes automotive ADAS and industrial cobots, benefitting from cohesive ISO and UNECE regulations that harmonize sensor testing. The Middle East and Africa, although small in volume, channel oil revenues into defense modernization and smart infrastructure projects that require precise inertial references for drones inspecting pipelines or bridges. Latin America, led by Brazil, eyes indigenous production in line with offsets tied to fighter and satellite contracts, spreading the gyroscopes market into fresh jurisdictions.

Competitive Landscape

Market concentration remains low. Honeywell and Bosch capitalize on certified manufacturing lines spanning MEMS and fiber-optic products, leveraging deep qualification data to secure multi-year defense and automotive contracts. STMicroelectronics and TDK InvenSense dominate consumer volumes by pairing MEMS gyroscopes with accelerometers on a single die, leveraging economies of scale.

Analog Devices combines delta-sigma converters and Kalman-filter DSP cores inside its iSensor modules, selling a drop-in path for industrial retrofits. New entrants, such as One Silicon Chip Photonics, focus on photonic integrated circuits that shrink optical interferometers onto silicon, enabling tactical accuracy without fiber spools. Venture capital is following quantum-enhanced concepts in cold-atom interferometry; however, those prototypes still require lab-grade conditions and high price points.

Supply risk in rare-earth magnets and fused-silica resonators encourages vertical integration. Several Tier 1 auto suppliers have co-investment deals with MEMS fabs to lock capacity and process recipes. Defense primes seek cyber-secure firmware images that resist over-the-air tampering, a niche where smaller vendors with encryption expertise can outmaneuver legacy firms. Overall, competition centers on hitting tighter drift at lower cost while navigating certification labyrinths across ISO 26262, FAA TSO and medical IEC 60601.

Gyroscopes Industry Leaders

Murata Manufacturing Co. Ltd

STMicroelectronics NV

Honeywell International Inc.

Analog Devices Inc.

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Tronics unveiled a north-seeking MEMS gyroscope targeting defense and industrial navigation deployments scheduled for H2 2025 readiness.

- January 2025: Murata released the SCH16T-K10 six-DOF inertial sensor with improved temperature stability and 30% lower power for automotive ADAS and robotics.

- December 2024: STMicroelectronics launched the ISM330BX six-axis IMU designed for vibration-heavy industrial automation usage.

- November 2024: Honeywell disclosed its HG3900 all-silicon MEMS IMU slated for 2026-2027 aerospace and defense qualification.

Global Gyroscopes Market Report Scope

Gyroscopes are sensors used to measure orientation in various devices. Since their inception, gyroscopes have undergone considerable evolution, primarily driven by incremental technological advancements. This has helped them emerge as a crucial component in any navigation system.

The Gyroscopes Market Report is Segmented by Technology (MEMS Gyroscope, Fiber Optic Gyroscope, Ring Laser Gyroscope, Hemispherical Resonating Gyroscope, Dynamically Tuned Gyroscope, and Other Technologies), Axis (1-Axis, 2-Axis, and 3-Axis), End-User Vertical (Consumer Electronics, Automotive, Aerospace and Defense, Industrial, Marine, and Other End-User Verticals), Application (Navigation Systems, Stabilization Platforms, Gaming and Virtual Reality, Robotics and Automation, and Other Applications), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| MEMS Gyroscope |

| Fiber Optic Gyroscope (FOG) |

| Ring Laser Gyroscope (RLG) |

| Hemispherical Resonating Gyroscope (HRG) |

| Dynamically Tuned Gyroscope (DTG) |

| Other Technologies |

| 1-Axis |

| 2-Axis |

| 3-Axis |

| Consumer Electronics |

| Automotive |

| Aerospace and Defense |

| Industrial |

| Marine |

| Other End-User Verticals |

| Navigation Systems |

| Stabilization Platforms |

| Gaming and Virtual Reality |

| Robotics and Automation |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Nigeria | ||

| Rest of Africa | ||

| By Technology | MEMS Gyroscope | ||

| Fiber Optic Gyroscope (FOG) | |||

| Ring Laser Gyroscope (RLG) | |||

| Hemispherical Resonating Gyroscope (HRG) | |||

| Dynamically Tuned Gyroscope (DTG) | |||

| Other Technologies | |||

| By Axis | 1-Axis | ||

| 2-Axis | |||

| 3-Axis | |||

| By End-User Vertical | Consumer Electronics | ||

| Automotive | |||

| Aerospace and Defense | |||

| Industrial | |||

| Marine | |||

| Other End-User Verticals | |||

| By Application | Navigation Systems | ||

| Stabilization Platforms | |||

| Gaming and Virtual Reality | |||

| Robotics and Automation | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the global gyroscopes market today?

The gyroscopes market size reached USD 4.56 billion in 2026 and is set to top USD 6.13 billion by 2031.

Which region generates the highest sales for gyroscopes?

Asia-Pacific accounts for 40.42% of 2025 revenue thanks to its semiconductor and consumer-electronics clusters.

What technology type is growing fastest?

Fiber-optic gyroscopes lead growth at a 7.85% CAGR due to defense and aerospace precision needs.

Which end-user segment is expanding most quickly?

Industrial automation is advancing at an 8.21% CAGR as factories deploy robots and asset-tracking systems.

How are automotive trends influencing gyro demand?

Level 3-4 ADAS and electric-vehicle platforms require low-drift MEMS gyros with ISO 26262 diagnostics, boosting automotive orders.

What are the key restraints limiting market growth?

High-accuracy manufacturing complexity and supply-chain volatility in specialty fibers and ICs are the main headwinds.

Page last updated on: