Field Programmable Gate Array (FPGA) Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | 10.32 % |

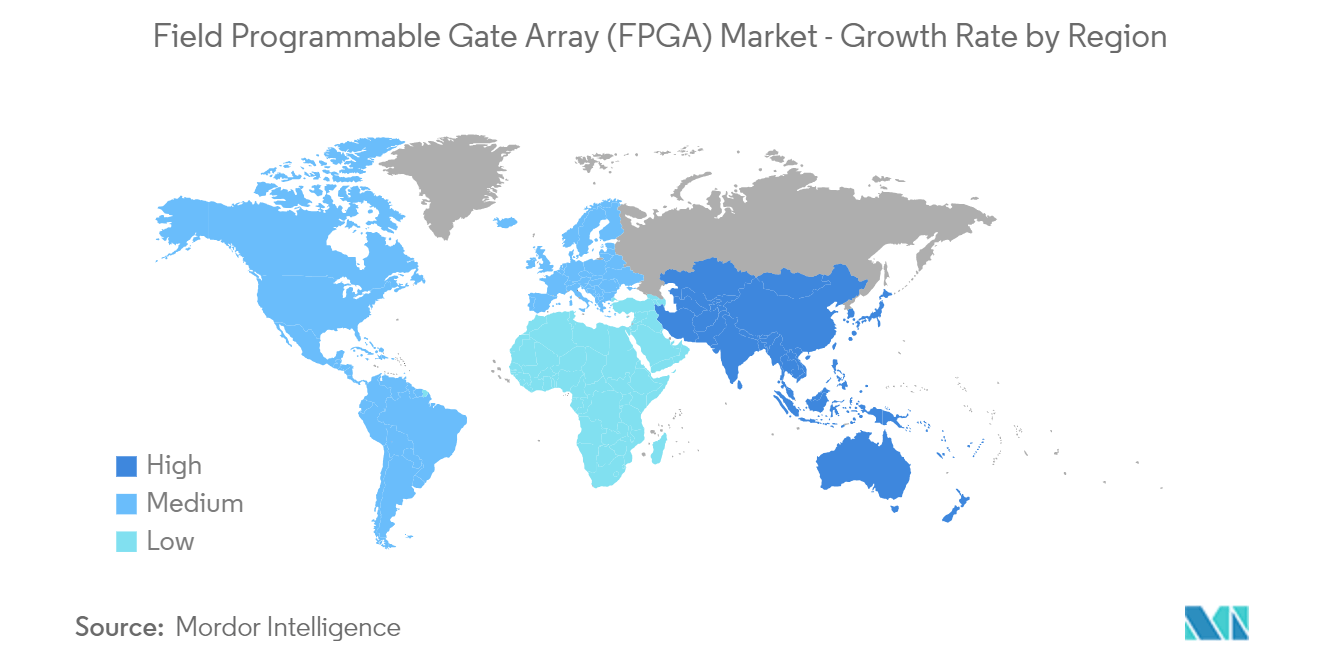

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Field Programmable Gate Array (FPGA) Market Analysis

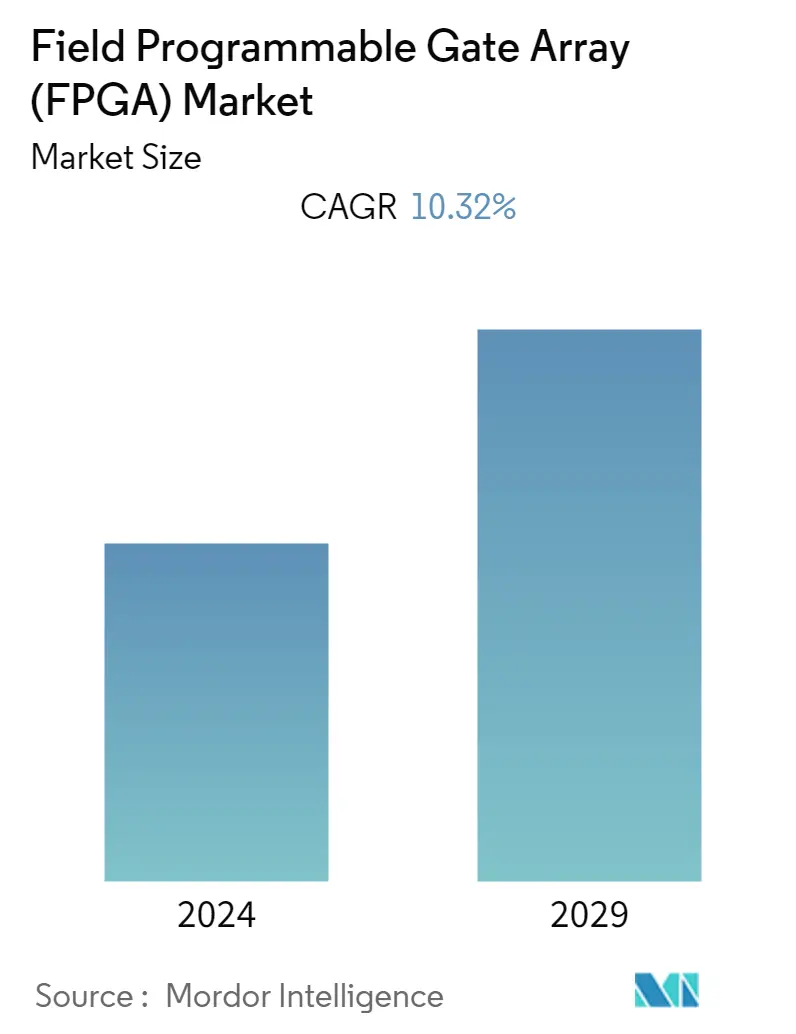

The Field Programmable Gate Array (FPGA) Market was valued at USD 6.9 billion in the previous year and is expected to grow at a CAGR of 10.32%, reaching USD 12.44 billion by the next five years. High deployment of data centers and high-performance computing is expected to propel the demand for the FPGA in the forecasted period. For instance, in March 2023, NTT intends to launch six data centers in India over the next three months, with three more in the works. Almost 70 percent of the identical capacity in these data centers has already been booked, according to NTT India MD Sharad Sanghi. The company will launch six additional data centers by the end of June, bringing its total number of operating data centers in the country to 11.

- Field programmable gate arrays (FPGAs) incorporate circuits with a programmable hardware fabric. Unlike ASICs or graphics processing units (GPUs), the circuitry inside an FPGA chip is not hard etched; it can be reprogrammed as required. This capability makes FPGAs a suitable alternative to ASICs, which need a long development time and a significant investment to design and fabricate.

- FPGAs are used in the technology industry for machine learning and deep learning. Microsoft Research displayed one of the first use cases of AI on FPGAs in the last decade as part of the company's efforts to speed up web searches. FPGAs provide a combination of programmability, speed, and flexibility, delivering performance without high cost and complexity to develop custom application-specific integrated circuits (ASICs). Microsoft's Bing search engine also uses FPGAs in production, indicating their value for deep learning applications. According to the company, Bing realized a 50% increase in throughput using FPGAs to accelerate search ranking.

- In addition, FPGAs deliver hardware customization with integrated AI and can be programmed to provide behavior like an ASIC or a GPU. The reconfigurable, reprogrammable nature of an FPGA makes itself well suited for a rapidly evolving AI landscape, enabling designers to test algorithms quickly and get to market fast. High Power Consumption Compared to ASIC restraining the market growth. Energy efficiency has always been a significant concern across various industries. Industries incorporating electronic devices always seek low-power-consuming devices. In FPGAs, power consumption is higher, and programmers do not have any control over power optimization.

- Furthermore, growth and advancement in technology development for 5G networking infrastructure and an increase in the use of FPGA in various end-user industries are some of the factors driving the studied market growth. For instance, in June 2022, Ericsson invested over USD 100 million in its energy-efficient 5G smart factory in Texas, where the equipment powering 5G networks across the United States is constructed. The factory showcases innovation powered by 5G connectivity, with abilities such as autonomous robots, augmented reality training, and many more.

- In addition, various players in the market are continuously investing in the latest technology to develop innovative products. For instance, in January 2023, FPGA startup Rapid Silicon landed USD 15 million to bring its first chip to market. The round of funding will be used to invest in Rapid Silicon's product portfolio, support its premier low-end FPGA product launch, and build on the company's momentum in adopting open-source software for commercial applications.

- The demand for data centers, artificial intelligence, and machine learning across government, enterprises, and academic entities is witnessing exponential growth due to the COVID-19 pandemic. This growth has positively impacted the need for FPGAs. It is predicted to maintain the same pace in the forecasted period, helping spread the impact and significance of FPGAs in various end-user industries.

Field Programmable Gate Array (FPGA) Market Trends

Increasing Demand for IoT is Expected to Drive the Market Growth

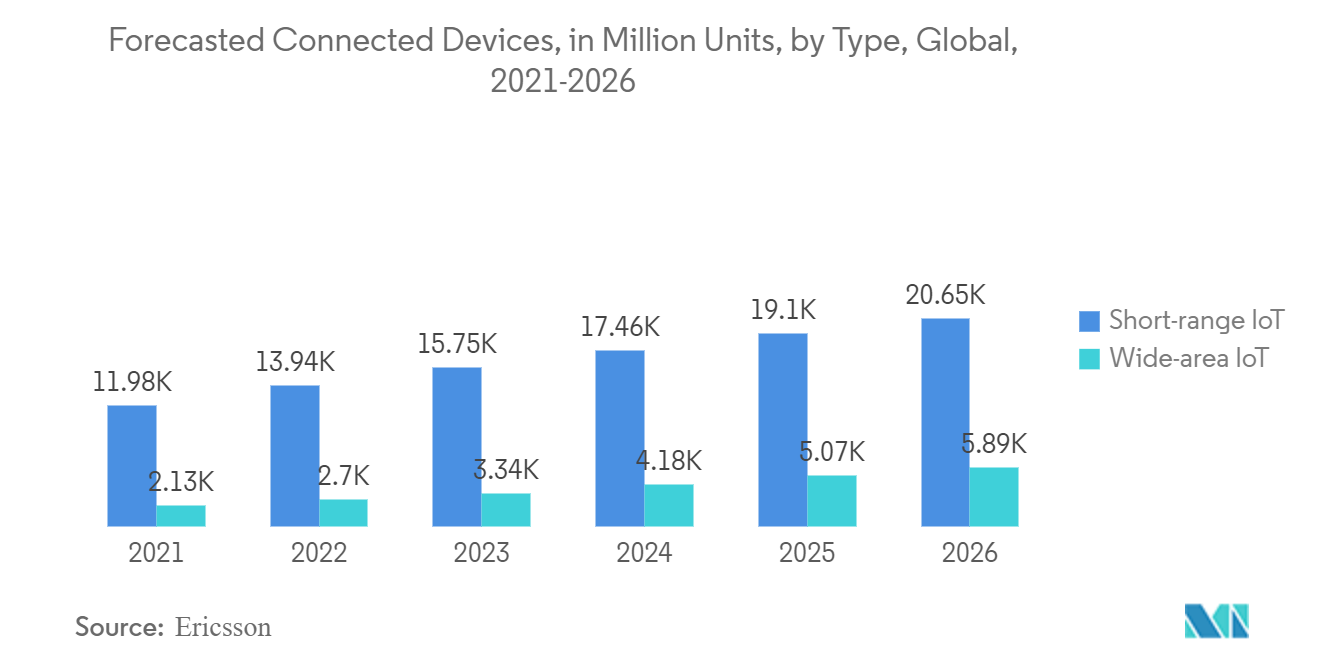

- Parallel execution is a crucial benefit of FPGAs, as several sensors, like humidity and temperature detectors, operate constantly. Since no time is required to be spent on looping and pausing for the delay, FPGAs are more power-efficient for IoT. According to the State of the IoT 2022 report, connected IoT devices are increasing by 18% to 14.4 billion globally. By 2025, this number is predicted to be over 30 billion, nearly 4 IoT devices per person on average.

- The demand for IoT is anticipated to increase even further during the forecast period, which signifies a boost in demand for semiconductors and other components. According to SEMI, the size of the semiconductor and sensor needed for IoT devices is expected to reach USD 114.2 billion by 2025.

- With the rapid increase in the number of IoT devices, chip requirement for building IoT instruments is also expected to rise during the forecast period. Reducing energy consumption, combined with the miniaturization of chips, will be prioritized by manufacturers.

- According to Ericsson, short-range IoT-connected devices recorded USD 13,939 million, and wide-area IoT-connected instruments recorded USD 2,696 million in 2022. Further, it is anticipated to reach USD 20,649 million and USD 5,885 million in 2026.

- IoT promises to be a major driving force that would create significant innovation, facilitate new business models, and enhance global society in multiple ways. Market vendors develop FPGAs to integrate them into IoT devices and solutions. For instance, Intel FPGA solutions, such as Intel Stratix 10, allow scalability and flexibility to address IoT requirements with inherent software and hardware programmability.

Asia Pacific is Expected to Hold Significant Market Share

- The Asia Pacific is a significant region for the players operating in the FPGA industry. Within the Asia Pacific, many nations, including China, India, South Korea, Taiwan, and others, have seen an enormous increase in the consumer electronics industry in the past few years. As a result, the FPGA demand in the area is seen as an influence point.

- According to the Semiconductor Equipment and Material International (SEMI), China is a significant spender on semiconductor equipment, followed by South Korea, Taiwan, and Japan. Furthermore, China is expected to maintain the top position in semiconductor equipment spending this year, while Taiwan is anticipated to regain the lead in 2024. In addition, the Chinese government encouraged its national champions and top digital enterprises to develop their domestic semiconductor manufacturing capacities to rebalance China's reliance on overseas semiconductor demand. Such an initiative may further boost the semiconductor market, propelling the demand for FPGA.

- Furthermore, the stay-at-home trend spurred by the coronavirus pandemic continues to drive the demand for semiconductor chips. For instance, according to WSTS, the estimated semiconductor industry revenue in the Asia Pacific region will reach USD 411.97 billion in 2023. Such trends encourage leading semiconductor manufacturers to enter the Asia Pacific market. For instance, ASML, one of the most prominent players in the market, recently opened a unique state-of-the-art training facility in Tainan.

- Similarly, in November 2022, Advanced Semiconductor Engineering (ASE) announced a USD 300 million investment to expand its production site in Malaysia. Moreover, China's State Council's "National Integrated Circuit Industry Development Guidelines" set the aim of becoming a global player in all semiconductor industry segments by 2030.

- In addition, the Made in China 2025 initiative supports achieving knowledge about advanced semiconductor manufacturing as a critical component of China's future economy and society. In addition, the country recently spent USD 574 billion in the healthcare sector, which may further drive the studied market growth.

- Furthermore, 5G adoption is rising in momentum for both the network and device domains. According to the report, Ericson Mobility 5G subscriptions are predicted to reach 1 b, two years earlier than 4G. Key factors include China's earlier engagement with 5G, compared to 4G, and the timely availability of instruments from several vendors. The Chinese telecom sector experienced rapid evolution in recent years, which is expected to continue until 2025. Increased population, communication services, and smartphone use fuel the industry's development. Premium connectivity and content services in China account for the majority of the market development in the country.

- China is paving the way for the FPGA market to expand. The country's demand is extending due to its significant position as the international manufacturer of consumer electronics gadgets. China is the world's largest manufacturing hub, producing 36% of the world's electronics, including smartphones, computers, cloud servers, and telecom infrastructure, establishing the country as the global electronics supply chain's most important node. The popularity of AI in China opened up a new development potential for the Chinese consumer electronics market. Smart homes and IoT (Internet of Things) will likely be significant development potential for manufacturers of FPGA in the next decade.

Field Programmable Gate Array (FPGA) Industry Overview

The Field Programmable Gate Array (FPGA) Market is moderately fragmented with the presence of major players like Xilinx Inc., Lattice Semiconductor Corporation, Quicklogic Corporation, Intel Corporation, and Achronix Semiconductor Corporation. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- December 2022- Lattice announced its first devices based on this latest platform, Lattice Avant-E FPGAs, which are developed to solve critical customer challenges at the Edge by combining class-leading energy efficiency, size, and performance with an optimized characteristic set tailored to the requirements of edge applications like data processing and AI.

- February 2022- QuickLogic Corporation announced that its PolarPro 3 family of low-power, SRAM-based FPGAs was available to solve semiconductor supply availability challenges. This favorably flexible family features power consumption lower than 55uA and a tiny footprint in small packages and die options.

Field Programmable Gate Array (FPGA) Market Leaders

Xilinx, Inc.

Lattice Semiconductor Corporation

Quicklogic Corporation

Intel Corporation

Achronix Semiconductor Corporation

*Disclaimer: Major Players sorted in no particular order

_Market_conc.webp)

Field Programmable Gate Array (FPGA) Market News

- March 2022- QuickLogic Corporation partnered with SkyWater Technology to port the eFPGA technology to the 90 nm RH90 radiation-hardened process. This rad-hard version of the technology can be embedded as an eFPGA IP core in ASIC or SoC devices or implemented as a standalone, custom rad-hard FPGA for mission-critical applications. This technology offers end customers all the flexibility benefits provided by FPGAs combined with the ruggedness of a rad-hard solution for various commercial and defense uses.

- February 2022- AMD and Xilinx announced joining a definitive agreement for AMD to achieve Xilinx in an all-stock deal valued at USD 35 billion. This will help extend the breadth of AMD's product portfolio and consumer set across diverse growth markets. Joining AMD will accelerate Xilinx's data center business expansion and enable it to pursue a broader customer base across more markets.

Field Programmable Gate Array (FPGA) Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Value Chain Analysis

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Consumers

4.3.3 Threat of New Entrants

4.3.4 Intensity of Competitive Rivalry

4.3.5 Threat of Substitutes

4.4 Impact of Macro Economic trends on the Industry

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Demand for IoT

5.2 Market Restraints

5.2.1 High Power Consumption Compared to ASIC

6. MARKET SEGMENTATION

6.1 By Configuration

6.1.1 High-end FPGA

6.1.2 Mid-range FPGA/Low-end FPGA

6.2 By Architecture

6.2.1 SRAM-based FPGA

6.2.2 Anti-fuse Based FPGA

6.2.3 Flash-based FPGA

6.3 By End-user Industry

6.3.1 IT and Telecommunication

6.3.2 Consumer Electronics

6.3.3 Automotive

6.3.4 Industrial

6.3.5 Military and Aerospace

6.3.6 Other End-user Industries

6.4 By Geography

6.4.1 North America

6.4.1.1 United States

6.4.1.2 Canada

6.4.2 Europe

6.4.2.1 Germany

6.4.2.2 United Kingdom

6.4.2.3 France

6.4.2.4 Rest of Europe

6.4.3 Asia Pacific

6.4.3.1 China

6.4.3.2 Japan

6.4.3.3 India

6.4.3.4 South Korea

6.4.3.5 Rest of the Asia Pacific

6.4.4 Latin America

6.4.4.1 Brazil

6.4.4.2 Argentina

6.4.4.3 Mexico

6.4.4.4 Rest of Latin America

6.4.5 Middle East and Africa

6.4.5.1 United Arab Emirates

6.4.5.2 Saudi Arabia

6.4.5.3 South Africa

6.4.5.4 Rest of Middle East and Africa

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 Xilinx Inc.

7.1.2 Lattice Semiconductor Corporation

7.1.3 Quicklogic Corporation

7.1.4 Intel Corporation

7.1.5 Achronix Semiconductor Corporation

7.1.6 GOWIN Semiconductor Corporation

7.1.7 Microchip Technology Incorporated

7.1.8 Efinix Inc.

- *List Not Exhaustive

8. VENDOR MARKET SHARE ANALYSIS

9. INVESTMENT ANALYSIS

10. FUTURE OF THE MARKET

Field Programmable Gate Array (FPGA) Industry Segmentation

FPGAs are pre-fabricated silicon instruments that can be electrically programmed in the field to become almost any type of digital circuit or system. They are an array of configurable logic blocks (CLBs) linked together by programmable interconnects. After manufacturing, they can be reprogrammed to meet the needs of the desired application or functionality.

The studied market is segmented by Configuration (High-end FPGA, Mid-range FPGA/Low-end FPGA), by (Architecture, SRAM-based FPGA, Anti-fuse Based FPGA, Flash-based FPGA), by End-user Industry (IT and Telecommunication, Consumer Electronics, Automotive, Industrial, Military and Aerospace), by Geography (North America (United States, Canada), Europe (Germany, United Kingdom, France, Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Rest of the Asia Pacific), Latin America (Brazil, Argentina, Mexico, Rest of Latin America), Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa, Rest of Middle East and Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| By Configuration | |

| High-end FPGA | |

| Mid-range FPGA/Low-end FPGA |

| By Architecture | |

| SRAM-based FPGA | |

| Anti-fuse Based FPGA | |

| Flash-based FPGA |

| By End-user Industry | |

| IT and Telecommunication | |

| Consumer Electronics | |

| Automotive | |

| Industrial | |

| Military and Aerospace | |

| Other End-user Industries |

| By Geography | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Field Programmable Gate Array (FPGA) Market Research FAQs

What is the current Field Programmable Gate Array (FPGA) Market size?

The Field Programmable Gate Array (FPGA) Market is projected to register a CAGR of 10.32% during the forecast period (2024-2029)

Who are the key players in Field Programmable Gate Array (FPGA) Market?

Xilinx, Inc., Lattice Semiconductor Corporation, Quicklogic Corporation, Intel Corporation and Achronix Semiconductor Corporation are the major companies operating in the Field Programmable Gate Array (FPGA) Market.

Which is the fastest growing region in Field Programmable Gate Array (FPGA) Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Field Programmable Gate Array (FPGA) Market?

In 2024, the Asia Pacific accounts for the largest market share in Field Programmable Gate Array (FPGA) Market.

What years does this Field Programmable Gate Array (FPGA) Market cover?

The report covers the Field Programmable Gate Array (FPGA) Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Field Programmable Gate Array (FPGA) Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Field Programmable Gate Array Industry Report

Statistics for the 2024 Field Programmable Gate Array (FPGA) market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Field Programmable Gate Array (FPGA) analysis includes a market forecast outlook to for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.