Electrosurgical Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

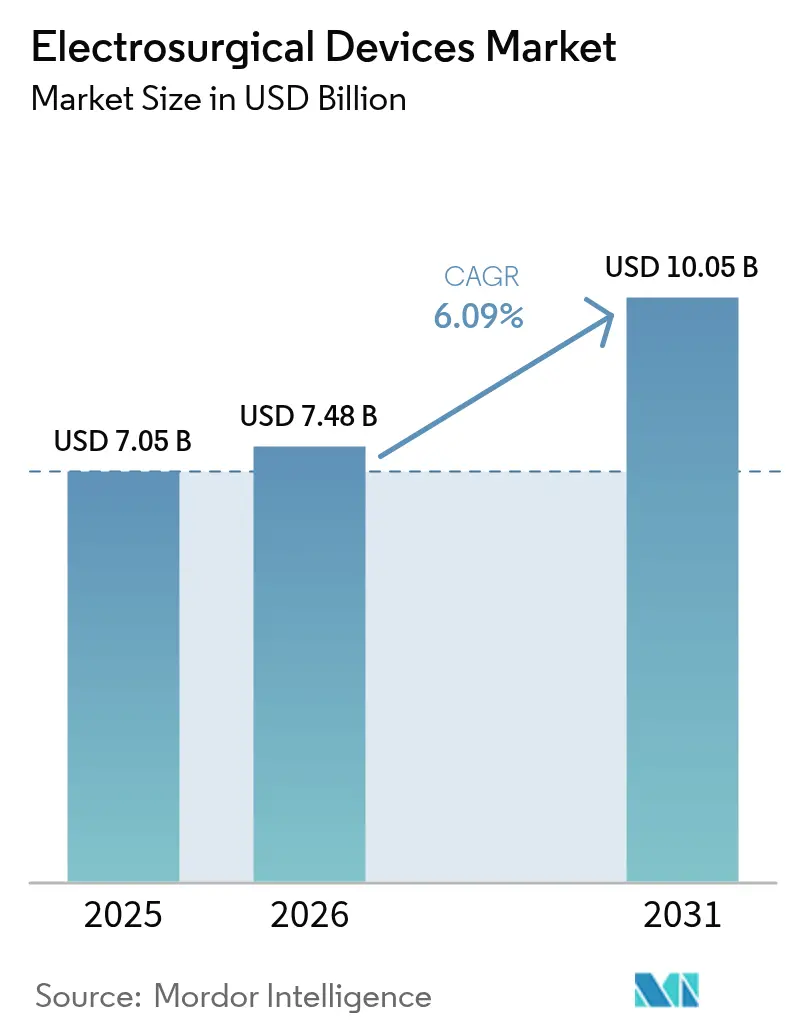

| Market Size (2026) | USD 7.48 Billion |

| Market Size (2031) | USD 10.05 Billion |

| Growth Rate (2026 - 2031) | 6.09% CAGR |

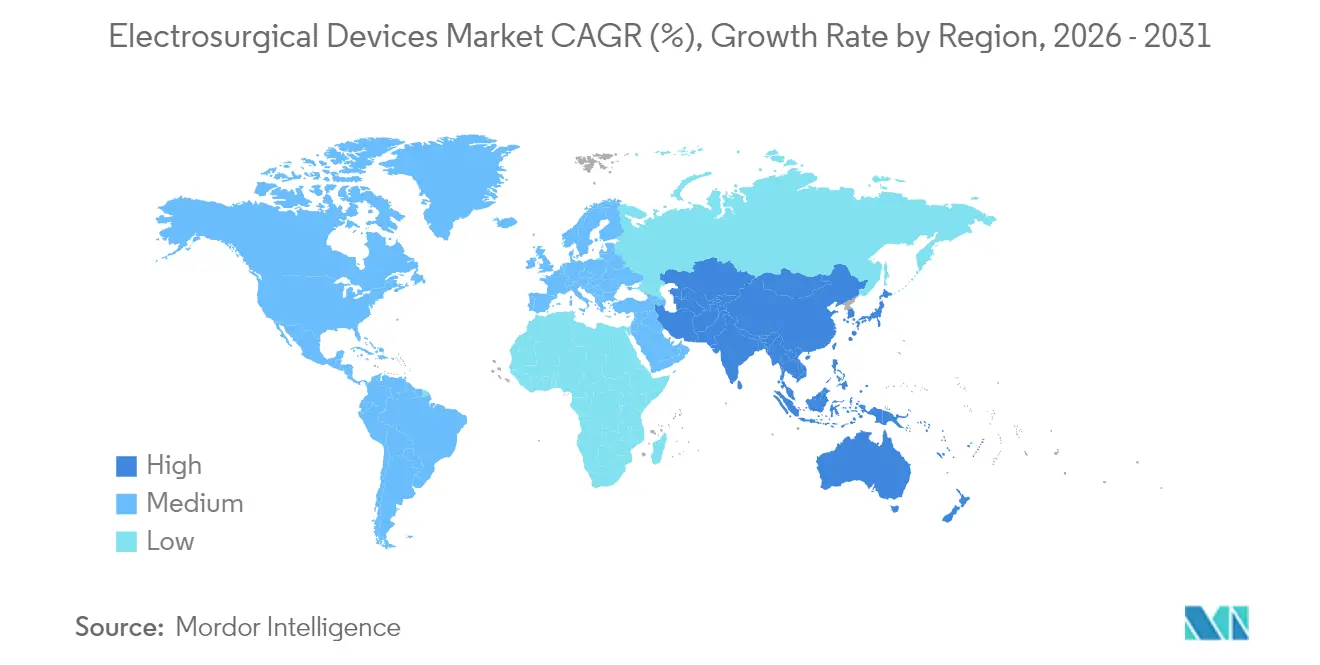

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

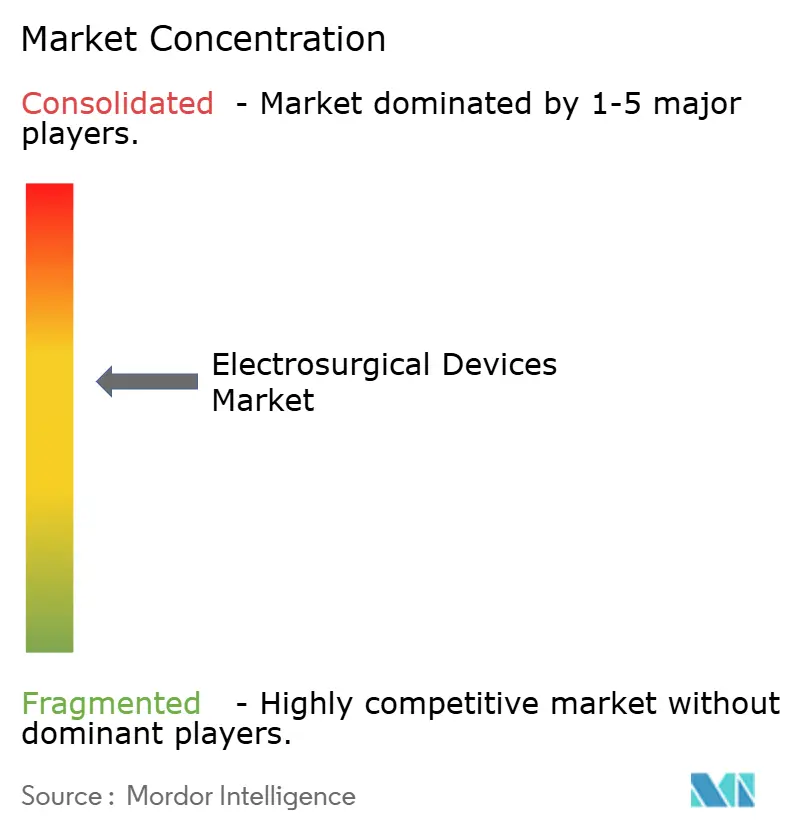

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrosurgical Devices Market Analysis by Mordor Intelligence

The electrosurgical devices market size was valued at USD 7.05 billion in 2025 and estimated to grow from USD 7.48 billion in 2026 to reach USD 10.05 billion by 2031, at a CAGR of 6.09% during the forecast period (2026-2031). Spurred by demographic pressure, hospitals and ambulatory facilities are moving swiftly from legacy monopolar generators to integrated, AI-guided energy platforms that modulate power in real time. A steady shift toward minimally invasive procedures, coupled with the proliferation of ambulatory surgical centers (ASCs), is underpinning consistent demand for compact, high-precision systems. Supply-chain localization incentives in the United States and European Union reinforce domestic manufacturing, while rare-earth and tungsten price swings are tightening cost controls across the electrosurgical devices market. Competitive intensity remains moderate as incumbents defend share through acquisitions, intelligent instrument launches and platform bundling strategies that embed energy delivery, robotics and smoke evacuation into a single ecosystem.

Key Report Takeaways

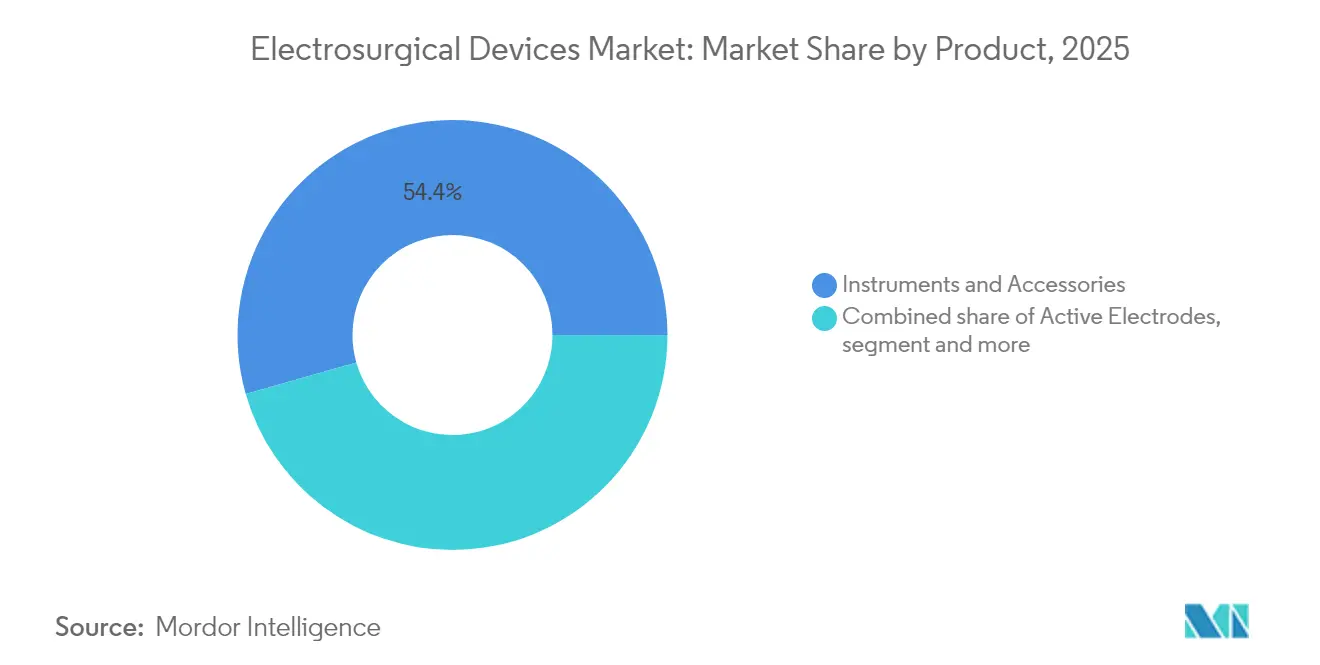

- By product, Instruments & Accessories led with 54.42% of electrosurgical devices market share in 2025; Active Electrodes are on track to expand at a 7.58% CAGR through 2031.

- By application, General Surgery accounted for 30.25% of the electrosurgical devices market size in 2025, whereas Cosmetic & Plastic Surgery is projected to accelerate at an 7.92% CAGR to 2031.

- By energy modality, Bipolar Radio-frequency captured 46.30% share in 2025, while Ultrasonic energy is projected to surge at a 7.28% CAGR through 2031.

- By end user, Hospitals commanded 57.92% share in 2025 as ASCs record the fastest future growth at an 8.12% CAGR.

- By region, North America retained leadership with a 41.60% revenue share in 2025; Asia-Pacific is poised for the quickest regional climb, advancing at an 8.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electrosurgical Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in chronic diseases & ageing population | +1.8% | Global; strongest in North America and Europe | Long term (≥ 4 years) |

| Minimally-invasive surgery preference | +1.5% | Global; led by North America and Asia-Pacific | Medium term (2–4 years) |

| Technology shift to intelligent energy | +1.2% | North America & European Union; spill-over to APAC | Medium term (2–4 years) |

| Outpatient surgery center boom | +0.9% | North America primary; emerging in Europe | Short term (≤ 2 years) |

| AI-guided tissue sensing | +0.6% | Advanced markets in North America & EU | Long term (≥ 4 years) |

| Supply-chain localization incentives | +0.4% | USA & EU focus with indirect global effect | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rise in Chronic Diseases & Ageing Population

Global longevity gains mean more poly-morbid patients entering operating rooms, and cardiovascular procedures alone are projected to climb sharply as diabetes incidence rises. Surgeons therefore require bipolar and ultrasonic platforms capable of controlled hemostasis inside fragile, comorbid tissue fields. Intelligent energy consoles deliver precise wattage adjustments that minimize thermal spread, easing concerns in elderly cohorts with limited physiologic reserve. The same demographic trend is escalating volume in joint-replacement revisions and oncologic resections, extending the addressable base of the electrosurgical devices market. Hospitals in North America and Western Europe are doubling down on generator upgrades that embed tissue-impedance monitoring so that any inadvertent rise in tissue temperature is recognized and corrected within milliseconds. Over the long term, the compounding effect of aging and chronic illness adds a 1.8 percentage-point tailwind to overall CAGR projections.

Minimally-Invasive Surgery Preference

Payers and providers increasingly rank shorter length of stay and faster return-to-work as prime value metrics. Laparoscopic, thoracoscopic and endoscopic approaches inherently depend on slim, low-heat instruments, which explains why advanced bipolar and ultrasonic shears dominate capital budgets for minimally invasive suites. Compact electrosurgical generators designed to dock under mobile towers free up valuable real estate inside crowded ORs. Micro-incision adoption in Asia-Pacific is now approaching growth curves once unique to the United States, broadening revenue potential for integrated smoke evacuation and temperature-controlled RF electrodes. A recent four-year economic model showed that temperature-controlled radiofrequency instruments yielded plan-level savings of USD 20 million and USD 3,531 per treated patient, reinforcing pay-for-value arguments.

Technology Shift to Intelligent Energy Platforms

Instead of static cut-coag settings, next-generation consoles use algorithmic feedback loops that sense tissue impedance 4,000 times per second and maintain optimal joule delivery. Medtronic’s TissueFect™ circuit typifies this advance, automatically tapering power to protect adjacent structures during vessel sealing.[1]Medtronic, “Valleylab™ FX8 Energy Platform,” medtronic.com Such platforms combine monopolar, bipolar and ultrasonic modes in a single footprint, reducing instrument exchanges and OR time. The embedded software records energy profiles, creating a data repository that hospitals mine for quality-improvement analytics. These performance benefits translate into a 1.2 percentage-point lift on the electrosurgical devices market CAGR.

Outpatient Surgery Center Boom (ASC Build-Outs)

Seventy-two percent of U.S. surgeries already happen in ASCs, and procedure volumes are projected to climb another 25% this decade.[2]Health Industry Distributors Association, “Ambulatory Surgery Center Market Report,” hida.orgASC economics emphasize predictable, turnkey instruments; hence, demand is shifting from fully featured hospital-grade towers to package-priced, single-procedure kits. Manufacturers that layer service contracts and rapid exchange programs on top of their generator fleet gain share because center operators equate uptime with revenue. The surge of new ASCs in suburban corridors also normalizes disposable active electrodes configured for one-time use, combating cross-contamination without high-temperature sterilization equipment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of skilled electrosurgeons | −1.1% | Global; most acute in emerging markets | Long term (≥ 4 years) |

| Stringent device re-certification (EU-MDR) | −0.8% | European Union with global spill-over | Medium term (2–4 years) |

| Thermal injury litigation risk spike | −0.5% | North America; gradually spreading worldwide | Short term (≤ 2 years) |

| Rare-earth & tungsten price volatility | −0.3% | Global supply chain impact | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Electrosurgeons

Simulation-based curricula such as SAGES’ FUSE program have improved knowledge scores, yet demand for fully credentialed electrosurgeons still outstrips supply. In low- and middle-income countries, many operating rooms lack proctorship, causing hospitals to delay generator upgrades until staff competencies rise. A 2023 observer-blinded study documented that residents’ comfort performing Loop Electrosurgical Excision jumped only after 10 guided practice sessions, underscoring the steep learning curve. Skill scarcity subtracts 1.1 percentage points from the electrosurgical devices market CAGR forecast.

Stringent Device Re-Certification (EU-MDR)

The Medical Device Regulation obliges evidence bundles, unique device identifiers and ongoing post-market surveillance. Notified-body bottlenecks have stretched certificate renewals to 12–18 months, delaying product launches and compelling some small OEMs to exit Europe. Larger competitors absorb compliance overhead but must triage R&D portfolios, slowing rollouts elsewhere.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Innovative Instruments Expand Elective Use

Instruments and Accessories delivered 54.42% of 2025 revenue, anchoring the electrosurgical devices market size at USD 3.84 billion for the category. Disposable bipolar forceps, ultrasonically activated shears and smoke evacuation pencils create a recurring sales flywheel that cushions seasonal procedure swings. Rising procedure complexity now favors active electrodes embedded with thermal sensors that relay impedance data to generators in under 10 milliseconds. Hospitals purchasing these intelligent tips typically lock into proprietary cable ecosystems, which further entrenches brand loyalty and drives higher lifetime account value for vendors. Ultrasonic and hybrid RF-ultrasonic blades are gaining in niche domains such as trans-oral and robotic thyroidectomy where traditional monopolar arcs risk nerve damage.

Active Electrodes represent the fastest-growing subsegment, advancing at a 7.58% CAGR as surgeons seek tactile feedback and auto-stop features that mitigate stray energy. The electrosurgical devices market share within specialty accessories is expected to tilt toward single-use, sensor-enabled tips because infection-control officers increasingly bar reprocessed electrodes without full traceability. Generator demand remains steady; however, consoles built before 2016 lack field-upgradable firmware slots, accelerating replacement cycles. Meanwhile, accessory bundles that integrate smoke evacuation capture pads are moving rapidly through U.S. outpatient procurement pipelines, fulfilling state smoke-free OR mandates.

Note: Segment shares of all individual segments available upon report purchase

By Application: General Surgery Provides Volume Stability

General Surgery generated 30.25% of 2025 sales, reflecting the breadth of appendectomy, hernia, and cholecystectomy cases that rely on standardized energy settings. This considerable base underpins predictable cash flow even when elective orthopedic or cosmetic volumes dip. In parallel, rising elective aesthetics demand lifts Cosmetic & Plastic Surgery, which is projected to clip along at an 7.92% CAGR. Patients in this segment prioritize low scarring and controlled coagulation, making ultrasonic dissectors and fine-tip bipolar forceps the instruments of choice.

Cardiovascular and Neurosurgery teams gravitate toward dual-modality consoles able to switch from 1 MHz bipolar sealing to 47 kHz ultrasonic dissection without changing handpieces. Gynecologic oncologists adopt thermal-sensor shears to reduce serosal injury during laparoscopic hysterectomy. The electrosurgical devices market size derived from hybrid specialty suites is expected to climb steadily because cross-disciplinary teams prefer a single, fully featured generator platform. Future procedure growth will also derive from orthopedic revisions that use RF-based capsular release to optimize joint space before implant insertion.

By Energy Modality: Bipolar Dominance Encounters Ultrasonic Momentum

Bipolar Radio-frequency held 46.30% revenue share in 2025 by virtue of its controlled current path, making it indispensable for vessel sealing up to 7 mm in diameter. Generators now ship with over-temperature auto-cease logic, reassuring risk managers worried about thermal spread. Yet, ultrasonic handpieces are gaining at 7.28% CAGR because they offer simultaneous cut-and-seal with negligible plume and minimal collateral heat, easing visual field management during laparoscopy.

Hybrid bipolar-ultrasonic devices are entering mainstream OR inventories, allowing a single instrument to handle omentum, mesentery and thick fascia without a tool change. Clinical engineers value console modularity that lets facilities add an ultrasonic board post-purchase, preserving capital. An ex-vivo study on the Anovo electrode reported well-defined coagulation margins in 97.6% of samples, validating precision claims. Looking ahead, pulsed-field ablation concepts may enter general surgery once energy-shaping software demonstrates equivalency in tissue selectivity.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospitals Rule, ASCs Race Ahead

Hospitals remained the primary outlet in 2025, securing 57.92% of transactions as tertiary centers invested in complex, multi-energy towers capable of open, laparoscopic and robotic cases. Teaching institutions also procure auxiliary modules—argon plasma, smoke evacuation, plume filters—to meet research and compliance benchmarks. However, the ASC segment is sprinting forward at an 8.12% CAGR, lured by predictable patient volumes and payer carve-outs that reimburse outpatient settings at favorable rates.

Operators running multi-state ASC chains standardize on one generator model across dozens of sites to leverage bulk discounts and streamline staff training. Single-use electrode kits appeal to these centers because they reduce instrument-tracking overhead. Specialty clinics—ENT, dermatology and fertility—acquire compact tabletop units that plug into standard 120-volt outlets, widening the lower end of the electrosurgical devices market. Vendor financing programs and per-procedure leasing are gaining traction, offering cash-light clinics a viable pathway to technology adoption without heavy upfront capital.

Geography Analysis

North America secured 41.60% of 2025 revenue as U.S. hospitals leveraged robust reimbursement schemes and an expansive ASC network to refresh fleets with AI-enabled energy consoles. Canada’s single-payer system, under budget constraint, nonetheless upgraded to integrated smoke evacuation to meet newly enacted occupational safety standards. Mexico’s private hospitals invested in premium bipolar-ultrasonic hybrids to boost medical-tourism competitiveness. Supply-chain localization grants in the United States are shortening lead times for printed circuit boards and ferrite cores, aligning with federal resilience goals.

Asia-Pacific is the fastest-growing theatre, posting an 8.55% CAGR forecast through 2031. China anchors regional demand thanks to an ambitious hospital-modernization drive and Made-in-China 2025 incentives that nudge domestic OEMs to co-develop intelligent energy platforms with universities. Japan, burdened by the world’s most rapidly aging population, sources precision ultrasonic scalpel systems for laparoscopic colectomy. India’s private hospital chains package electrosurgery towers within turnkey surgical bundles offered to international medical tourists at bundled, transparent pricing. Australia and South Korea import advanced bipolar sealing devices to tackle rising bariatric and oncologic surgery volumes, further expanding the electrosurgical devices market size across the Pacific Rim.

Europe registers stable, mid-single-digit growth as Germany, France and the United Kingdom upgrade OR suites while steering through EU-MDR documentation hurdles. Southern European countries benefit from EU recovery funds that partially subsidize capital purchases of smoke evacuation and plume filtration systems. Nordic hospitals, early adopters of data-rich surgical platforms, integrate generator data streams into national surgical quality registries, reinforcing evidence-based procurement. Eastern European and GCC growth remains opportunistic; however, large infrastructure programs in Saudi Arabia’s Vision 2030 and the United Arab Emirates’ medical free-zones are opening fresh avenues for premium energy platforms. South America and Africa collectively contribute a modest share today but hold upside potential as universal healthcare expansions unfold.

Competitive Landscape

Major manufacturers command a substantial portion of global revenue, placing the sector in a realm of moderate concentration. Medtronic leverages its Valleylab FX 8 console and LigaSure advanced sealer line to cross-sell into robotics alliances, including the Hugo™ robotic platform. Johnson & Johnson aligns its Dualto™ generator with the forthcoming Ottava™ robot, chasing fully integrated “energy-plus-robot” ecosystems that lock customer lifetime value. Olympus expands ultrasonic portfolios through incremental tip enhancements that lower cavitation noise and improve cutting speed.

Strategic M&A continues: Medtronic’s 2024 acquisition of Fortimedix added ultra-manual articulating instruments that feed directly into energy-assisted laparoscopy bundles, while Teleflex’s 2025 purchase of BIOTRONIK’s vascular assets augments its ablation pipeline. Competitors unable to match scale are focusing on differentiated AI tissue-recognition software embedded in handpieces. Patent-protected firmware updates, deliverable over-the-air, allow mid-tier vendors to iterate faster than legacy hardware refresh cycles, narrowing performance gaps within the electrosurgical devices market.

Regulators have begun piloting Predetermined Change Control Plans to streamline approval for software-only improvements, which could intensify competitive cadence as players push monthly firmware releases. Large GPOs in the United States now negotiate value-based contracts tied to postoperative complication rates, encouraging manufacturers to furnish real-world evidence collected by cloud-linked consoles. Collective bargaining power of multiregional ASC chains is also compressing margins at the lower end of generator portfolios.

Electrosurgical Devices Industry Leaders

Applied Medical Resources Corporation

Medtronic PLC

Olympus Corporation

Boston Scientific Corporation

B. Braun SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Medtronic obtained CE Mark for its robot-driven LigaSure vessel-sealing device, broadening its European foothold in intelligent surgical energy systems.

- July 2025: Intuitive Surgical secured FDA clearance for the Vessel Sealer Curved, expanding electrosurgical capabilities on da Vinci platforms.

- March 2025: Johnson & Johnson MedTech launched its Dualto electrosurgical generator engineered for seamless integration with the Ottava robot.

- November 2024: Medtronic completed the acquisition of Fortimedix Surgical, strengthening its advanced instrument roster.

Global Electrosurgical Devices Market Report Scope

Electrosurgical devices are instruments and equipment that are used for surgical cutting or controlling bleeding by causing coagulation at the surgical site using an alternating electric current.

The electrosurgical devices market is segmented by product (electrosurgical generators, active electrodes, electrosurgical instruments and accessories (bipolar instruments, monopolar instruments accessories)), application (neurosurgery, gynecology surgery, cardiovascular surgery, cosmetic surgery, general surgery, orthopedic surgery, and other applications), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally.

The report offers the value (in USD) for the above segments.

| Electrosurgical Generators | |

| Active Electrodes | |

| Instruments and Accessories | Bipolar Instruments |

| Monopolar Instruments | |

| Ultrasonic & Advanced Energy | |

| Accessories (Cables, Tips, Smoke Evac) |

| General Surgery |

| Neurosurgery |

| Gynecology Surgery |

| Cardiovascular Surgery |

| Orthopedic Surgery |

| Cosmetic & Plastic Surgery |

| Other Specialized Procedures |

| Monopolar Radio-frequency |

| Bipolar Radio-frequency |

| Ultrasonic |

| Hybrid/Advanced Bipolar-Ultrasonic |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics & Offices |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Electrosurgical Generators | |

| Active Electrodes | ||

| Instruments and Accessories | Bipolar Instruments | |

| Monopolar Instruments | ||

| Ultrasonic & Advanced Energy | ||

| Accessories (Cables, Tips, Smoke Evac) | ||

| By Application | General Surgery | |

| Neurosurgery | ||

| Gynecology Surgery | ||

| Cardiovascular Surgery | ||

| Orthopedic Surgery | ||

| Cosmetic & Plastic Surgery | ||

| Other Specialized Procedures | ||

| By Energy Modality | Monopolar Radio-frequency | |

| Bipolar Radio-frequency | ||

| Ultrasonic | ||

| Hybrid/Advanced Bipolar-Ultrasonic | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics & Offices | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected growth rate for the electrosurgical devices market through 2031?

The electrosurgical devices market is forecast to expand at a 6.09% CAGR between 2026 and 2031.

Which product category currently generates the highest revenue?

Instruments & Accessories lead the market, accounting for 54.42% of 2025 sales.

Why are ambulatory surgery centers important to future demand?

ASCs prioritize cost-efficient, high-throughput procedures and are projected to grow at an 8.12% CAGR, creating robust demand for easy-to-use electrosurgical systems.

Which energy modality is gaining traction fastest?

Ultrasonic energy is advancing at a 7.28% CAGR due to its simultaneous cut-and-seal capability with minimal thermal spread.

How is EU-MDR affecting manufacturers?

Stricter re-certification rules extend approval cycles by up to 18 months and raise compliance costs, marginally slowing new-product introductions.