Dropshipping Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.51 Trillion |

| Market Size (2031) | USD 1.35 Trillion |

| Growth Rate (2026 - 2031) | 21.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dropshipping Market Analysis by Mordor Intelligence

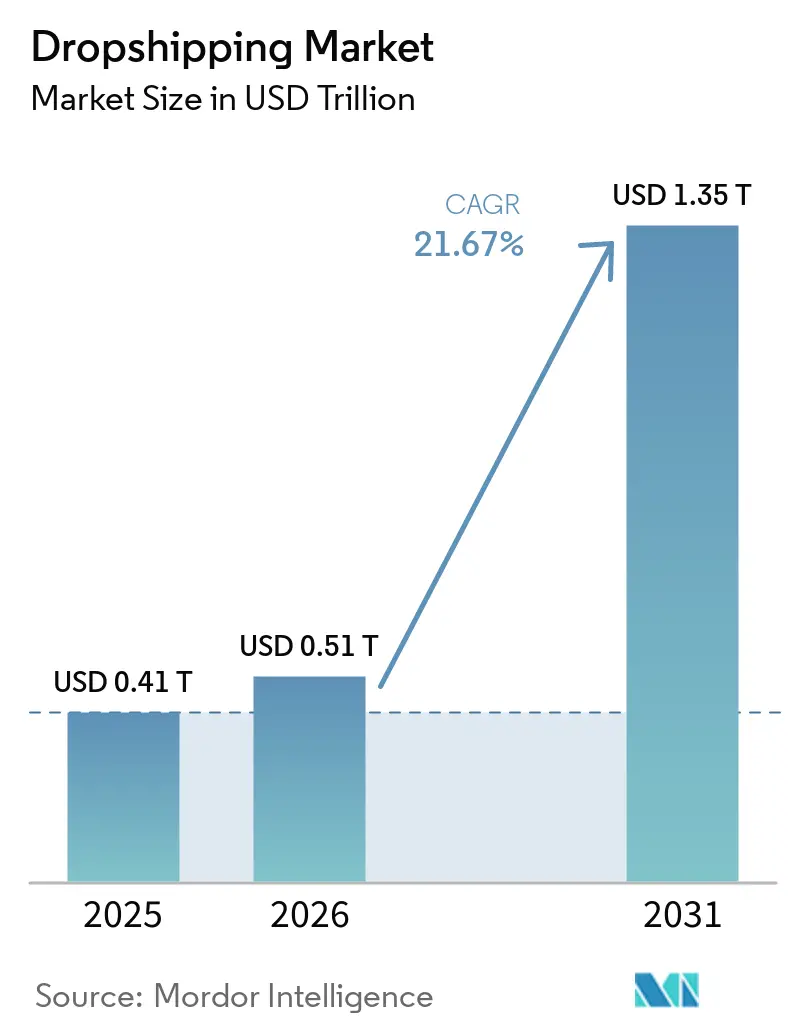

The Dropshipping market size is projected to be USD 414.93 billion in 2025, USD 507.18 billion in 2026, and reach USD 1.35 trillion by 2031, growing at a CAGR of 21.67% from 2026 to 2031.

AI-generated visual content, blockchain trust mechanisms, and micro-fulfillment hubs operated by national postal services are compressing product-launch cycles and shrinking delivery windows, creating structural tailwinds for the Dropshipping market. International orders already account for over two-thirds of global value, reflecting consumer openness to cross-border discovery when real-time landed-cost tools remove customs-related friction. Same-day fulfillment pilots led by postal operators in China, Korea, and Singapore are widening the addressable customer base by matching domestic delivery expectations. Social-commerce algorithms that surface products before explicit search intent are shifting acquisition away from keyword advertising, while recurring-purchase bundles are improving lifetime value economics in consumables and personal-care categories.

Key Report Takeaways

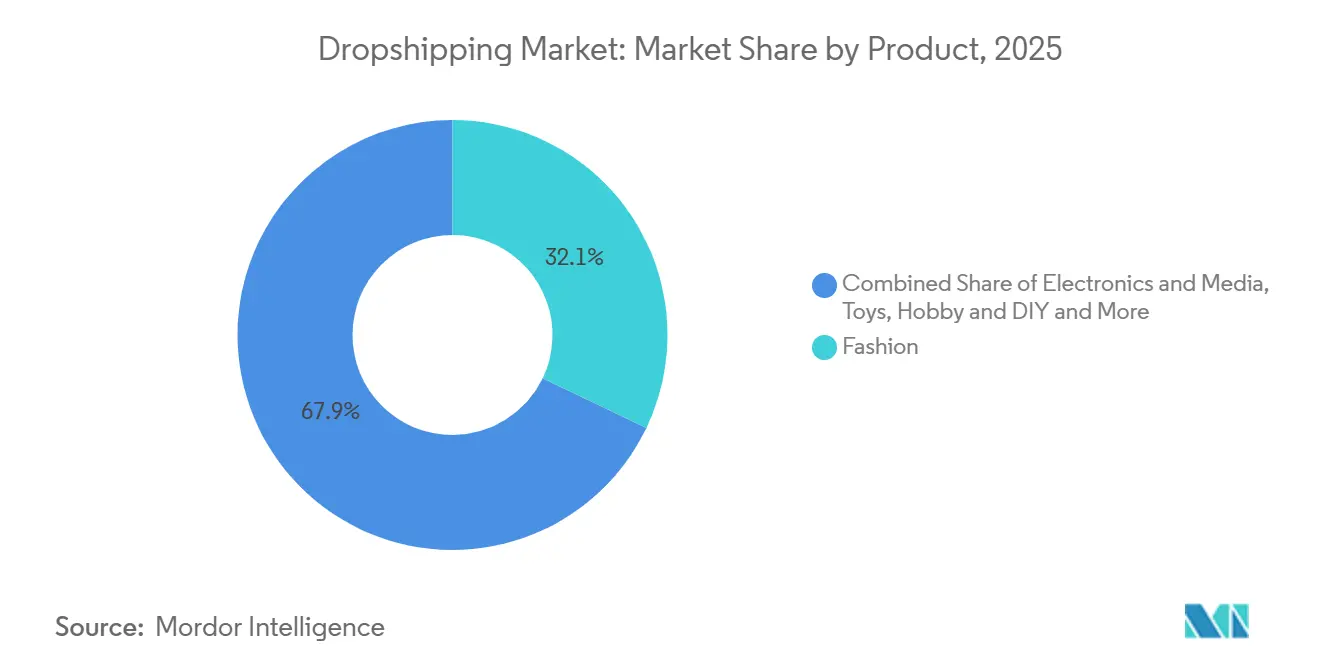

- By product category, fashion led with a 32.08% revenue share in 2025 and is projected to expand at a 23.35% CAGR through 2031.

- By destination, international deliveries held 68.98% of the total value in 2025, and recorded the highest projected CAGR at 22.14% to 2031.

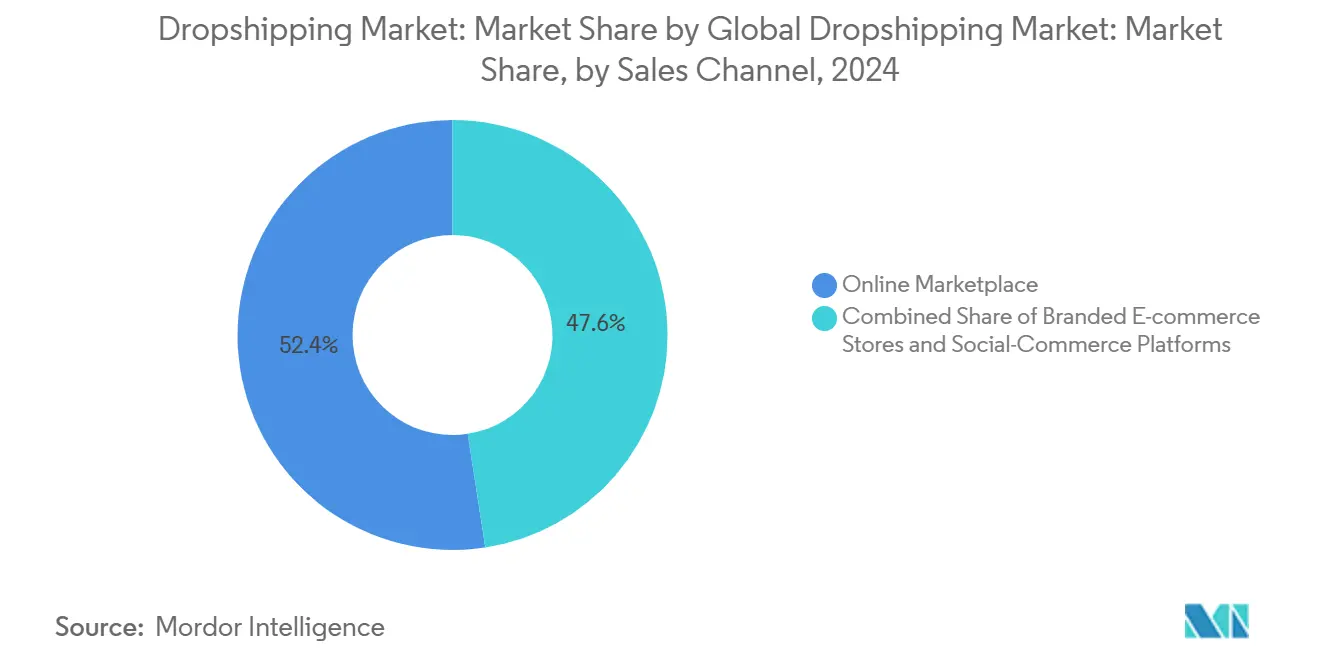

- By sales channel, online marketplaces captured 52.43% share of the Dropshipping market size in 2025, whereas social-commerce platforms are advancing at a 25.49% CAGR through 2031.

- By business model, B2C transactions commanded 70.16% share of the Dropshipping market share in 2025, and projected to be the fastest-growing model at 23.66% CAGR to 2031.

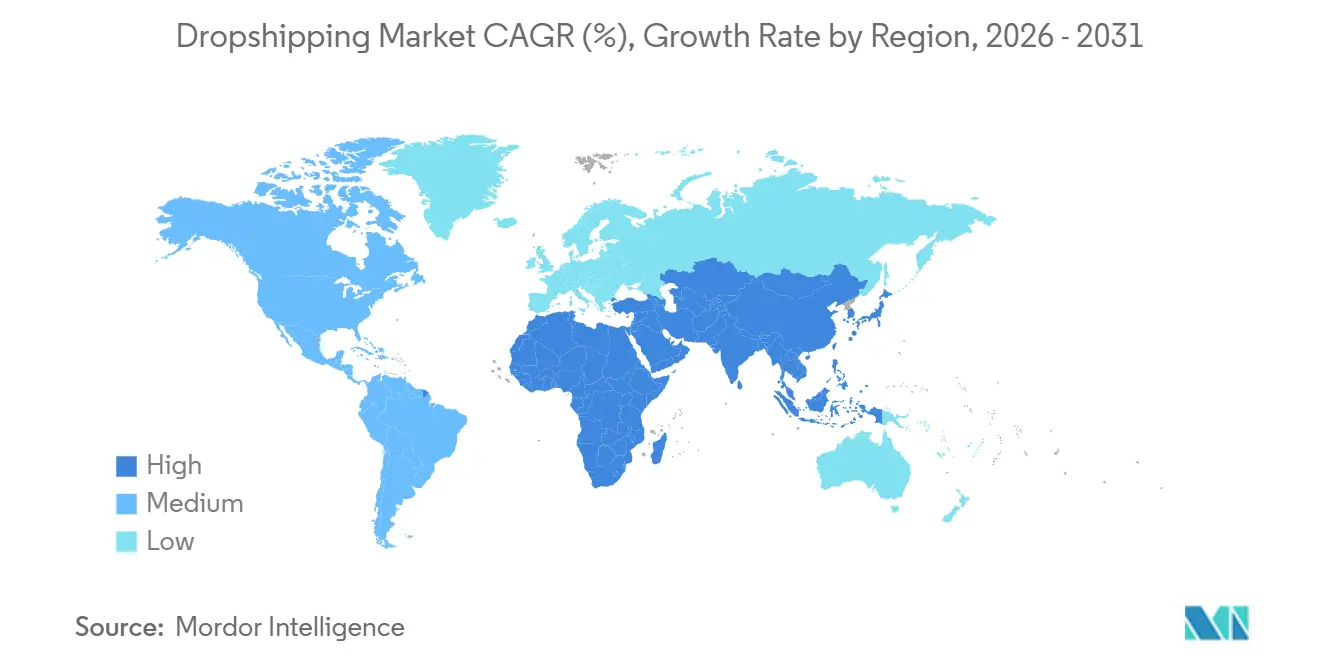

- By geography, North America accounted for 34.44% of the Dropshipping market in 2025, while Asia-Pacific is forecast to be the quickest-expanding region at a 26.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Dropshipping Market*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Instant-Generation Rich Media (AI imagery/video) slashing SKU launch lead-times | +3.9% | Global, advanced markets first | Short term (≤ 2 years) |

| Carbon-Neutral and Climate-Positive Shipping Labels lifting conversion among eco-aware cohorts | +2.6% | EU, North America, urban APAC | Medium term (2-4 years) |

| Real-Time Landed-Cost Calculators mitigating customs-clearance cart abandonment | +3.4% | Cross-border corridors, EU-US-APAC | Short term (≤ 2 years) |

| National Postal Operators opening micro-fulfilment hubs for cross-border same-day delivery | +4.2% | APAC core, expanding to EU and North America | Medium term (2-4 years) |

| Subscription-bundled replenishment models boosting lifetime value in consumables | +2.8% | North America, EU, mature APAC markets | Long term (≥ 4 years) |

| Supplier-of-Record smart contracts (blockchain) enhancing brand trust and IP protection | +3.1% | Global, B2B corridors first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Instant-Generation Rich Media Slashing SKU Launch Lead-Times

Generative-AI imagery and video tools allow merchants to publish photorealistic listings within hours, eliminating the cost and delay of traditional product photography. Rapid content iteration enables data-driven A/B testing of designs before committing to physical production, de-risking inventory bets for nano-brands. Platform integrations such as Shopify’s connection with OpenAI that lets merchants sell through ChatGPT conversations prove that conversational discovery can push these AI-rendered products directly into purchase flows. Visual commerce benefits the fashion segment most, as colorways and patterns can be swapped algorithmically, expanding SKU depth without added sampling costs. Nevertheless, marketplaces are drafting labeling rules to ensure consumers understand when images are synthetic, and compliance with those guidelines will influence adoption speed[1].

Carbon-Neutral and Climate-Positive Shipping Labels Lifting Conversion

Verified low-emission delivery options are persuading eco-conscious buyers in the EU and North America to accept premium pricing or slower transit if sustainability is certified. Postal and private carriers are embedding carbon calculators at checkout, so buyers transparently offset emissions in real time. Cainiao’s optimized five-day cross-border service illustrates how route efficiency can reduce both carbon and cost simultaneously. For merchants, displaying a climate-positive badge differentiates listings within crowded marketplaces where price competition is intense. The main hurdle is trust; third-party audits and immutable carbon ledgers are emerging as preferred validation mechanisms to prevent greenwashing[2]Ministry of Commerce, “Guideline on Accelerating Cross-Border E-commerce Export,” gov.cn.

Real-Time Landed-Cost Calculators Mitigating Cart Abandonment

Customs uncertainties have historically driven double-digit cart abandonment on international orders. Embedded APIs now pull live tariff tables, local taxes, and courier surcharges into the checkout summary, letting buyers prepay a single all-in price. Shopify’s enterprise collaboration with Oracle and Deloitte Digital integrates these calculators with ERP inventory feeds to ensure accuracy during peak traffic. The feature is most impactful for high-ticket electronics, where even small duty errors can derail a sale. Reliability depends on up-to-date tariff data and sub-second latency; outages risk immediate revenue loss and elevated refund claims.

National Postal Operators Opening Micro-Fulfillment Hubs

Postal agencies are repurposing underutilized urban facilities into micro-fulfillment nodes that stage cross-border parcels for final-mile dispatch the same day they clear customs. China’s network of more than 2,500 overseas warehouses exemplifies the public-sector scale behind this shift. By injecting state-backed logistics capacity into the Dropshipping market, postal operators level the playing field for small merchants who cannot negotiate private-carrier discounts. Seasonal volume spikes remain a challenge, so contingency routing across multiple hubs is becoming a required capability for enterprise shippers[3]China State Council, “China to Enhance Service Capabilities of Cross-Border E-Commerce,” english.www.gov.cn.

Restraints Impact Analysis of Dropshipping Market*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating multi-platform ad-inventory costs inflating customer-acquisition spend | -3.2% | Global, most acute in North America and EU | Short term (≤ 2 years) |

| Single-use packaging bans are driving up fulfillment material expenses | -2.4% | EU, expanding to APAC and North America | Medium term (2-4 years) |

| Tightened payment-network dispute thresholds triggering merchant account freezes | -2.8% | Global, concentrated in cross-border transactions | Short term (≤ 2 years) |

| Supplier insolvency risk amid consolidation of tier-2 Chinese factories | -2.6% | Global, China-dependent supply chains most vulnerable | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Multi-Platform Ad Costs Inflating Customer Acquisition

Advertising revenue at marketplaces and social platforms is climbing faster than average order values, cutting into merchant margins. Amazon surpassed USD 50 billion in ad sales during 2025, underscoring pay-to-play dynamics that squeeze smaller sellers. As TikTok Shop’s user base nears 50 million in the United States, early low-cost exposure is already giving way to auction-style bidding familiar on mature channels. Dropshippers must cultivate content-led discovery and influencer collaborations to offset rising CPMs, but these strategies require longer ramp times and specialized skill sets.

Single-Use Packaging Bans are Driving Up Fulfillment Expenses

EU directives targeting plastic waste are compelling merchants to switch to biodegradable or recycled options that cost more and may compromise product protection. Smaller dropshippers, lacking scale discounts, face the sharpest unit-cost increases. Because suppliers often control packaging overseas, United States and European sellers sometimes resort to trans-shipment repackaging, adding labor and delay. Certification logos boost brand perception among sustainability-minded customers, but failure to comply invites fines and account suspensions in regulated markets[4]Asian Development Bank, “E-Commerce Evolution in Asia and the Pacific,” adb.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Dropshipping Market Segment Analysis

By Product:

Fashion Dominance Underpinned by Visual CommerceFashion captured the leading 32.08% Dropshipping market in 2025 as immersive content and influencer collaborations propelled viral product cycles. AI-generated lookbooks shorten design iterations while regional micro-fulfillment hubs reduce return friction, encouraging customers to trial trend-driven items. The segment’s projected 23.35% CAGR keeps the overall Dropshipping market size on an upward trajectory by contributing outsized transaction volume during seasonal peaks. Apparel also benefits from subscription boxes bundling complementary accessories, extending customer lifetime revenue.

Intimate knowledge of fast-moving trends forces fashion merchants to maintain nimble supplier networks spanning China, Vietnam, and Turkey. Compliance costs tied to packaging and sustainability are climbing, yet carbon-positive shipping labels resonate strongly with Gen Z shoppers, sustaining premium pricing power. Counterfeit risk remains elevated, so blockchain-verified certificates are gaining ground among premium streetwear labels.

By Destination:

Infrastructure Propels Cross-Border TransactionsInternational orders represented 68.98% of the Dropshipping market in 2025, and projected to grow at 22.14% CAGR over the forecast period, bolstered by 2,500+ Chinese overseas warehouses that cut customs processing times. Real-time landed-cost APIs give buyers full price transparency, reinforcing trust and driving repeat purchases. Meanwhile, domestic dropship posted solid growth where postal micro-fulfillment enables same-day delivery for bulky items like home décor.

Cross-border expansion is accelerating into MENA and Latin America as Cainiao and Correios pilot joint-lane express services. Yet each corridor demands localized compliance, from VAT e-invoicing to data privacy regulations. Merchants using multi-node fulfillment split inventory strategically to minimize tariff exposure and shorten last-mile routes.

By Sales Channel:

Social Commerce Redraws Discovery PathsOnline marketplaces still account for 52.43% of value, but social-commerce feeds are eroding that dominance by serving products ahead of explicit search, aligning with younger shopping behavior. Algorithmic recommendation engines on TikTok and Instagram can lift a new SKU from obscurity to six-figure sales within days, accelerating the overall Dropshipping market.

Social-commerce platforms within the dropshipping market are growing at 25.49% CAGR over the forecast period. Marketplace sellers combat discovery loss by live-streaming flash deals and leveraging platform-level loyalty credits. Branded e-commerce sites focus on storytelling and subscription integration to safeguard first-party data. Multi-channel infrastructure is essential; inventory sync across API connections prevents overselling, and automated listing tools recycle content across channels with minimal manual touch.

By Business Model:

B2C Scale Meets Subscription StickinessB2C held a commanding 70.16% Dropshipping market share in 2025, and projected to grow at 23.66% CAGR over the forecast period. However, escalating ad costs are pivoting growth toward subscription-bundled replenishment. Predictable volume stabilizes demand for consumables, enabling forward contracts with suppliers that lock in favorable pricing. Wholesale dropship is rising among brick-and-mortar retailers outsourcing long-tail SKUs to third-party fulfillment partners, boosting shelf variety without inventory risk.

C2C resale aligns with circular-economy preferences, particularly in fashion, where transparent condition grading and authenticity checks build buyer confidence. Platform support for escrow and dispute mediation is critical, as peer-to-peer transactions carry higher trust friction than B2C.

Geography Analysis

North America Dropshipping Market

North America generated 34.44% of the Dropshipping market size in 2025, led by the United States, where Shopify’s merchant GMV surge underscores platform consolidation. Canada and Mexico are benefiting from harmonized trade rules under USMCA, which streamline cross-border duty processing and spur cross-listing of SKUs. Same-day fulfillment pilots by USPS in major United States metros further enhance customer expectations that international sellers attempt to match.

APAC Dropshipping Market

Asia-Pacific is the fastest-growing region in the dropshipping market, projected at a 26.15% CAGR, fueled by Southeast Asia’s mobile-first consumers and the proliferation of digital wallets. China remains the supply-side engine, while Korea’s USD 4 billion Shinsegae–Alibaba joint venture illustrates how domestic heroes partner with global giants to expand overseas reach. India is attracting investment as an alternative sourcing hub, though last-mile infrastructure still lags coastal China’s efficiency.

Western Europe Dropshipping Market

Europe presents a complex regulatory landscape for the dropshipping market, where single-use packaging bans and the Digital Services Act raise compliance stakes. Germany, France, and the United Kingdom demand both carbon-neutral options and clear landed-cost visibility, driving adoption of API-enabled duties calculators. Postal operators in the Netherlands and Belgium are rolling out cross-border micro-hubs that commit to next-day delivery within Schengen, narrowing the gap between domestic and imported parcels.

Mordor Intelligence provides coverage of the dropshipping market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns.

Note: Segments share of all individual segments available upon report purchase

Competitive Landscape

The Dropshipping market remains fragmented, yet consolidation signals are emerging in niche infrastructure. The Printful–Printify merger unites in-house production with 85+ outsourced partners, forming the largest print-on-demand network globally. Alibaba’s regrouping of Taobao, Tmall, and AliExpress streamlines merchant onboarding and aligns cross-border logistics under one umbrella, giving the conglomerate leverage in negotiations with carriers.

Platform providers differentiate through ecosystem partnerships. Shopify integrates Oracle back-office systems for real-time inventory and landed-cost accuracy, while Google Cloud collaboration opens enterprise procurement channels.

Logistics specialists in the dropshipping market compete on delivery SLAs; Cainiao’s five-day guarantee is pressuring DHL eCommerce and USPS GlobalPost to shorten transit commitments. Payment gateways are layering on AI-driven fraud checks to keep dispute ratios below network thresholds. Sustainable-packaging startups are courting enterprise merchants, offering compostable solutions that meet EU directives without sacrificing protective performance.

Dropshipping Industry Leaders

Shopify

AliExpress

SaleHoo

Doba

CJ Dropshipping

- *Disclaimer: Major Players sorted in no particular order

Dropshipping Market Companies Covered in this Report

- Shopify

- AliExpress

- Dropship Direct

- CJ Dropshipping

- Spocket

- Printful

- Printify

- DSers

- Modalyst

- SaleHoo

- Doba

- Dropified

- AppScenic

- Syncee

- Wholesale2B

- AliDropship

- GreenDropShip

- Zendrop

- NicheDropshipping

- Trendsi

Recent Industry Developments in Dropshipping Market

- January 2026: Cainiao added eight European micro-fulfillment hubs, enabling 48-hour delivery on 6,000 high-velocity SKUs.

- December 2024: Shinsegae Group and Alibaba formed a USD 4 billion venture combining Gmarket and AliExpress Korea to broaden seller reach.

- November 2024: Printful and Printify completed an equal-part merger, creating the world’s largest print-on-demand dropshipping infrastructure.

- September 2024: Shopify, Oracle, and Deloitte Digital launched an enterprise commerce solution integrating ERP and front-end experiences.

Dropshipping Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the global dropshipping market as the value of merchandise ordered online when the retailer owns the customer relationship, but inventory is held and shipped by a third-party supplier; according to Mordor Intelligence, this spans both cross-border and domestic orders placed through online marketplaces, branded web stores, and social-commerce platforms.

Scope exclusion: Print-on-demand, digital downloads, and crowd-funded pre-orders sit outside this analysis.

Segments Covered in This Report

- By Product

- Fashion

- Electronics and Media

- Toys, Hobby and DIY

- Furniture and Appliances

- Health, Beauty and Personal Care

- Others (Pet, Auto, etc.)

- By Destination

- Domestic

- Cross-border/International

- By Sales Channel

- Online Marketplaces

- Branded E-commerce Stores

- Social-Commerce Platforms

- By Business Model

- B2C

- B2B / Wholesale Dropship

- C2C / Resale

- Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts spoke with marketplace category managers, third-party logistics executives across North America, Europe, and Asia Pacific, plus founders of mid-size dropship stores. Their guidance confirmed supplier onboarding pace, typical margin structures, and real cross-border lead times that rarely surface in public data.

Desk Research

We began by lining up macro data from UN COMTRADE, UPU postal statistics, and World Bank consumer spend tables, then wove in sector insights from sources such as the Ecommerce Foundation and the International Postal Corporation. Company filings, 10-Ks, and select marketplace press releases anchored average selling price checks, while paid feeds from D&B Hoovers and Dow Jones Factiva added firm-level color. The sources named are illustrative; many additional references informed validation.

Market-Sizing & Forecasting

We built a top-down demand pool by linking retail e-commerce spend to the share of orders fulfilled through dropshipping, which is filtered through destination mix and product-level price matrices. Select bottom-up roll-ups, supplier counts in China and sampled order volumes, then fine-tuned totals. Key variables include e-commerce penetration, parcel shipping cost, supplier onboarding rate, marketplace take-rate trends, and social-commerce order share. Forecasts use multivariate regression blended with scenario analysis agreed upon with our primary experts.

Data Validation & Update Cycle

Outputs run through automated variance scans, peer review, and senior sign-off. Reports refresh each year, with interim updates triggered by tariff shifts, large platform policy moves, or comparable material events.

How Mordor Intelligence's Dropshipping Market Size Compares to Other Published Estimates

Published figures often diverge because providers mix fulfillment models, escalate prices differently, or refresh data on uneven cadences, and that is where Mordor Intelligence's disciplined scoping stands out.

Some publishers count gross merchandise value before refunds, while others apply one global average price or ignore duty impacts, which inflates totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.41 trn | Mordor Intelligence | - |

| USD 0.46 trn | Global Consultancy A | Includes print-on-demand sales and records pre-refund values |

| USD 0.44 trn | Industry Association B | Uses one global ASP and omits duty adjustments |

The comparison shows figures cluster yet still vary; our balanced top-down model, selective bottom-up checks, and year-round validation give decision-makers a transparent, dependable baseline.

Key Questions Answered in the Report

How big will global dropshipping revenue be by 2031?

The Dropshipping market size is forecast to reach USD 1.35 trillion by 2031, reflecting a 21.67% CAGR between 2026 and 2031.

Which product segment contributes the most value?

Fashion leads with 32.08% of 2025 revenue and is expected to sustain strong double-digit growth through 2031.

What is driving the rapid expansion in Asia-Pacific?

Mobile-first consumers, growing digital-wallet adoption, and large-scale postal micro-fulfillment investment are propelling Asia-Pacific to a 26.15% CAGR.

Why are real-time landed-cost calculators important?

They disclose total customs and tax charges up front, reducing cross-border cart abandonment and improving conversion rates.

How are sustainability regulations affecting fulfillment costs?

Bans on single-use plastics in the EU and other regions are pushing merchants toward higher-priced biodegradable packaging and adding compliance overhead.

Page last updated on: