Container Shipping Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 123.14 Billion |

| Market Size (2031) | USD 142.07 Billion |

| Growth Rate (2026 - 2031) | 2.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

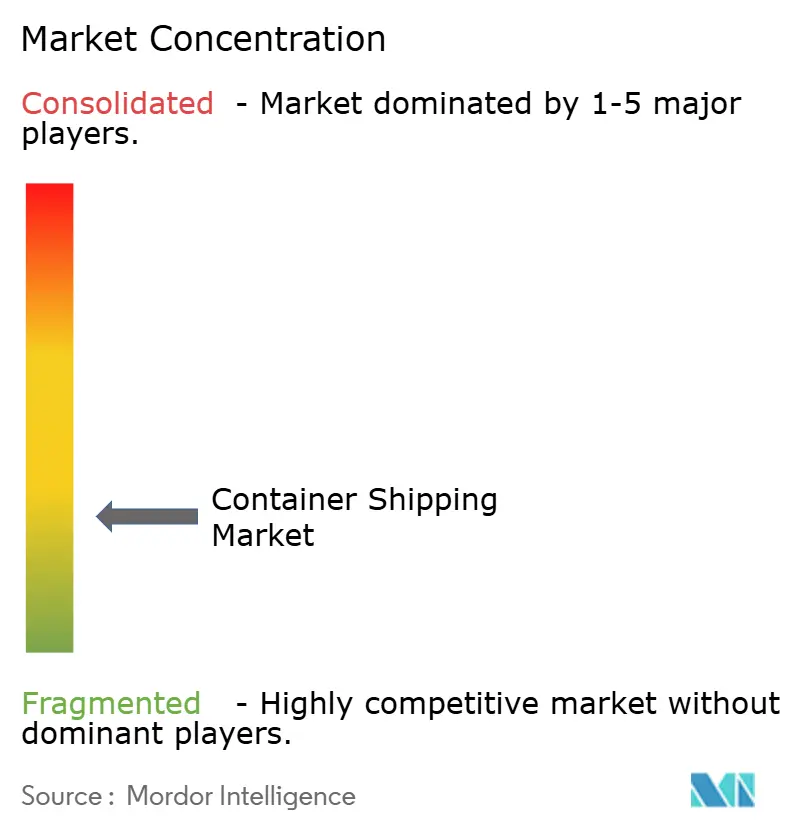

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Container Shipping Market Analysis by Mordor Intelligence

The Container Shipping Market size is expected to grow from USD 119.65 billion in 2025 to USD 123.14 billion in 2026 and is forecast to reach USD 142.07 billion by 2031 at 2.92% CAGR over 2026-2031.

Slower fleet-wide speed, ongoing Red Sea diversions, and an expanded regulatory cost base are moderating supply even as trade agreements and e-commerce replenish underlying demand. Carriers are concentrating on network reliability, with new alliance formations targeting on-time performance above 90% while reallocating capacity toward the most resilient corridors. Terminal ownership continues to rise as a defensive hedge against landside congestion and as a lever to capture new revenue pools. Fuel cost volatility remains the primary profitability swing factor, yet dual-fuel newbuild orders and incremental efficiency upgrades are gradually lowering per-unit emissions and bunker consumption. Against this backdrop, the container shipping market is transitioning from rate-driven earnings to efficiency-driven returns as technology adoption and environmental compliance reshape operating models.

Key Report Takeaways

- By container size, 40-foot units captured 50.62% of container shipping market share in 2025, and the segment is projected to post a 3.74% CAGR to 2031.

- By container type, reefer containers are expected to expand at a 3.36% CAGR through 2031, outpacing general-purpose boxes thanks to pharmaceutical and fresh produce demand.

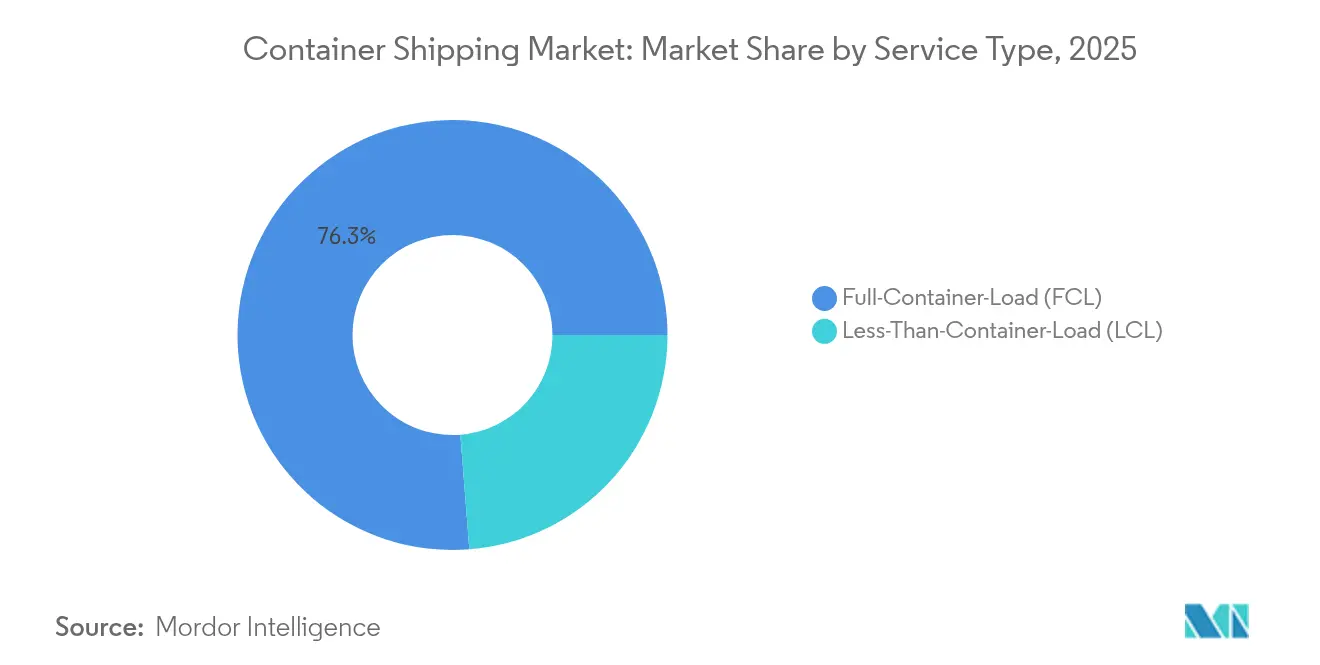

- By service, Full-Container-Load accounted for 76.25% of the container shipping market size in 2025 and is forecast to advance at a 3.12% CAGR during 2026-2031.

- By end-user, the FMCG and retail segment led with 26.45% share in 2025; healthcare and pharmaceuticals is projected to record a 3.62% CAGR to 2031.

- By geography, Asia-Pacific held 40.55% of 2025 revenue and is anticipated to maintain the fastest regional growth at a 4.12% CAGR through 2031, supported by intra-Asian trade integration and port capacity additions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Container Shipping Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising volume of international trade | +0.8% | Global | Medium term (2-4 years) |

| Expansion of free-trade agreements | +0.4% | EU-Mercosur, USMCA regions | Long term (≥ 4 years) |

| Rapid e-commerce containerization | +0.6% | North America, Asia-Pacific | Short term (≤ 2 years) |

| IMO 2023 carbon regulations drive renewal | +0.5% | Global | Medium term (2-4 years) |

| Arctic route viability | +0.2% | Northern Europe, Asia-Pacific | Long term (≥ 4 years) |

| AI-enabled predictive routing & scheduling | +0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Volume of International Trade

World merchandise trade is recovering on the back of stabilizing consumer spending and restocking cycles, prompting carriers to redeploy idle capacity onto North American and Mediterranean gateways. Longer voyage distances caused by Red Sea detours have temporarily absorbed excess tonnage, protecting rate integrity even as new vessels deliver. Port call data show double-digit throughput rebounds at U.S. East Coast hubs, highlighting the flexibility of the container shipping market to redirect flows quickly. Equipment repositioning costs have increased, yet higher backhaul utilization is offsetting part of the burden. The durability of trade growth remains linked to household purchasing power and to how swiftly geopolitical flashpoints normalize.

Expansion of Free-Trade Agreements

The EU–Mercosur deal, concluded in December 2024, is set to unlock EUR 56 billion (USD 61.80 billion) in additional goods trade and reshape South Atlantic services[1]“EU–Mercosur Trade Agreement,” European Commission, europa.eu . Carriers that already control terminals in Santos and Buenos Aires are preparing dedicated loops to capture origin-destination volumes that were traditionally transshipped in the Caribbean. Simultaneously, USMCA provisions are reinforcing North American near-shoring, a trend visible in the rising share of Mexican gateways handling U.S.-bound cargo. Broader regionalization is nudging fleet planners to design shorter, high-frequency strings instead of relying solely on long-haul east-west trunk routes. Over the long term, the container shipping market benefits from lower tariff barriers as well as harmonized customs processes that reduce dwell times and enhance service predictability.

Rapid E-commerce Containerization

Retailers shifting to omni-channel fulfillment models have accelerated box cycle times and increased demand for smaller shipment lots. East Coast ports recorded record monthly throughput in early 2025 following an extended holiday restock season, with e-commerce goods accounting for a growing share of inbound containers. LCL consolidators are capturing value by offering digital booking platforms with real-time visibility, enabling small shippers to match sailing schedules more efficiently. The surge in parcel-ready freight has prompted a wave of automation investments in yard and gate operations to handle higher gate moves per container. These dynamics are expanding the addressable base of the container shipping market while incentivizing carriers to differentiate through data transparency.

IMO 2023 Carbon Regulations Drive Fleet Renewal

Implementation of EEXI and CII benchmarks is advancing a two-tier vessel market where compliant tonnage secures premium rates. As of October 2024, the orderbook included more than 500 dual-fuel ships, signaling a structural pivot toward methanol and LNG propulsion. Early adopters report measurable operating cost savings despite elevated capital outlays, particularly when bunker prices spike. Financing conditions favor well-capitalized lines, raising barriers for smaller operators and promoting further consolidation. Over the medium term, the regulations are expected to enhance the reputation of the container shipping market among shippers with aggressive decarbonization targets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile bunker fuel prices | -0.4% | Global | Short term (≤ 2 years) |

| Escalating geopolitical trade tensions | -0.6% | Red Sea, US–China routes | Medium term (2-4 years) |

| Chronic port-side congestion bottlenecks | -0.3% | Singapore, Mediterranean hubs | Short term (≤ 2 years) |

| Cyber-attacks on digital ship-to-shore systems | -0.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Bunker Fuel Prices

Very-Low-Sulfur Fuel Oil averaged USD 630 / t in 2024, and the inclusion of shipping in the EU Emissions Trading System has added USD 170–210 / t for intra-European voyages[2]“ETS Extension to Maritime Transport,” European Commission, europa.eu. Price gyrations compel carriers to adjust freight rates through bunker adjustment factors that often lag market swings, eroding margins. Wide spreads between LNG, methanol, and conventional bunkers complicate multi-fuel procurement strategies. Hedging offers partial relief but demands financial sophistication that not all operators possess. Consequently, energy efficiency retrofits and slow steaming remain immediate tools to absorb cost shocks within the container shipping market.

Escalating Geopolitical Trade Tensions

Sustained insecurity in the Red Sea keeps roughly 70% of Suez-bound capacity rerouted around the Cape of Good Hope, lengthening round voyages by 10–14 days. On the Pacific, proposals to impose million-dollar port security fees on Chinese-owned vessels illustrate growing regulatory risk[3]“Proposed Maritime Security Fees,” Office of the United States Trade Representative, ustr.gov. These frictions undermine network stability, raise insurance premiums, and force cargo owners to hold higher inventories. Medium-term strategic planning thus includes scenario buffers that inflate capacity requirements and temper the organic growth potential of the container shipping market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Container Size: Standardization Drives Efficiency

The 40-foot segment held 50.62% of 2025 revenue, reflecting its status as the industry’s workhorse unit that maximizes vessel stowage and aligns with rail and truck dimensions. The container shipping market size for 40-foot boxes is projected to grow alongside equipment replacement cycles and inland infrastructure upgrades that favor high-cube variants. Robust demand from electronics and apparel shippers reinforces fleet utilization, while sustained production of high-cube designs lifts per-unit load factors. Port-side investments in double-lift crane spreaders further cement the operational preference for this size. The 20-foot segment remains vital for dense commodities and infrastructure-limited terminals in developing economies, though its relative share is expected to edge lower as shippers consolidate loads to reduce per-tonne carbon footprints. Specialized sizes such as 45-foot units cater to pallet-wide cargo niches, yet their uptake is restricted by limited backhaul demand and compatibility gaps in certain rail corridors.

Growth in the 40-foot category is also supported by digitized container tracking, which improves door-to-door visibility and enables leaner inventory planning for high-volume retailers. Leasing companies are accelerating fleet renewal to incorporate smart-box technology, a move that enhances asset rotation and reduces idle time. Combined, these factors should keep the 40-foot segment at the core of the container shipping market through 2031.

By Container Type: Specialized Cargo Drives Premium Growth

General-purpose containers accounted for 63.40% of 2025 throughput, underpinning the bulk of consumer and industrial trade flows. However, reefer units are forecast to log a 3.36% CAGR, outpacing standard boxes on the back of sustained demand for temperature-controlled pharmaceuticals and perishables. Enhanced insulation, integrated telemetry, and lower power draw raise the profitability of refrigerated services despite higher capital costs. Pharmaceutical firms are shifting high-value biologics from air to ocean freight, lured by validated cold-chain corridors that deliver cost savings without compromising product integrity. In food supply chains, the push to cut waste is increasing the share of fresh produce shipped in high-accuracy reefers with continuous monitoring. Consequently, carriers are dedicating larger reefer plugs on newbuild designs, signaling confidence in sustained premium demand. The general-purpose segment, while mature, remains central to the container shipping market, with incremental innovation focused on theft-resistant locks and end-to-end tracking rather than on transformative design changes.

A parallel trend involves the retro-fitting of CO₂-based refrigeration systems, improving energy efficiency and reducing global warming potential relative to older HFC units. These technology upgrades, combined with regulatory drivers in food and pharma, are likely to keep reefers at the forefront of revenue growth.

By Service: FCL Dominance Reflects Scale Economics

Full-Container-Load services captured 76.25% of 2025 shipments, underscoring the economies realized when shippers can fill an entire box. The container shipping market size for FCL bookings is expected to continue expanding due to automation of booking interfaces and greater spot visibility, which simplify end-to-end execution for high-volume importers. Greater vessel size and port efficiency have lowered per-box handling costs, reinforcing the structural advantage of FCL. Less-Than-Container-Load, while accounting for 23.75% of volume, remains essential for SMEs entering new export markets. Digital forwarders now integrate predictive load aggregation and dynamic routing, narrowing transit gaps versus FCL and lifting the attractiveness of consolidation. Hybrid models that allow partial-fill bookings in real time are emerging, blurring the boundary between the two services and increasing utilization rates across both categories. In the long run, the container shipping market expects margin coexistence as FCL retains volume leadership and LCL captures growing share among e-commerce entrepreneurs.

Improved customs pre-clearance and milestone visibility on shared consignments are tempering historic concerns over cargo delays and damage in LCL operations. As platforms scale, network density increases, enabling more direct consol services that further close the cost-to-transit gap with traditional FCL.

By End-User Industry: Diversification Creates Opportunities

FMCG and retail goods commanded 26.45% of 2025 revenue, benefitting from resilient household spending and the ongoing consumer shift to online channels. Fast-moving inventory cycles and seasonality spur high frequency of box turns, sustaining carrier preference for stable, contract-based volumes. The healthcare and pharmaceuticals segment shows the fastest growth at a 3.62% CAGR, propelled by rising demand for temperature-controlled biologics and vaccines. Regulatory compliance necessitates validated cold-chain corridors, raising switching costs and supporting premium rates for service providers with specialized assets. Manufacturing and automotive cargo continues to require synchronized delivery windows aligned with just-in-time production, making schedule reliability a critical differentiator. Electronics shipments, although moderating after pandemic peaks, remain high-value loads sensitive to security and climate control, further boosting the share of smart containers equipped with cargo condition sensors. Industrial chemicals sustain steady volume but face mounting environmental scrutiny that could shift certain bulk commodities to regional production over time.

Diversified end-user exposure cushions the container shipping market against sector-specific downturns and allows carriers to balance spot and contract mix strategically across economic cycles.

Geography Analysis

Asia-Pacific commanded 40.55% of 2025 revenue, reinforcing its status as the manufacturing and export engine of the container shipping market. Chinese GDP expansion near 5% and accelerated port automation in Shanghai, Ningbo-Zhoushan, and Busan are sustaining the region’s slot demand. Intra-Asian trade lanes are registering some of the highest frequency growth, propelled by ASEAN supply-chain integration and electronics component flows. The emergence of the Northern Sea Route as a summer alternative for Asia–Europe cargo offers an additional resilience layer, though uptake remains constrained by ice-class fleet scarcity and geopolitical risk. Continued investment in hinterland rail networks and free-trade zones supports a robust outlook, with the region projected to deliver a 4.12% CAGR through 2031.

North America experienced a 13.1% rebound in loaded container imports during 2024, led by retail restocking and e-commerce fulfillment demand. East Coast gateways such as Savannah and New York–New Jersey benefited from shipper diversification away from West Coast labor uncertainties and from deeper channel dredging that accommodates larger neo-Panamax vessels. Mexico’s west-coast port of Lázaro Cárdenas is attracting direct Asia services, offering rail connectivity into the U.S. Midwest. Long-beach terminal retrofits emphasizing zero-emission yard equipment align with state regulations and bolster the environmental credentials of the container shipping market in the region. While potential labor negotiations pose near-term volatility, the structural trend toward onshore inventory buffers and near-shoring supports medium-term growth.

Europe’s picture is mixed. Northern hubs such as Rotterdam and Antwerp-Bruges posted modest gains after a soft 2023, whereas Mediterranean transshipment hubs enjoyed volume windfalls of about 30% as carriers bypassed the Suez Canal. The container shipping market size in Southern Europe therefore expanded even as regulatory costs rose under the FuelEU Maritime and ETS frameworks. Investments in port community systems and intermodal rail corridors are improving hinterland connectivity, yet congestion risk lingers when Mediterranean hubs become overflow valves during crisis reroutes. Brexit-related customs friction has stabilized, although UK gateways continue to handle lower direct Far East services than before 2021.

Competitive Landscape

Oligopolistic concentration defines the container shipping market, with the top 10 carriers controlling roughly 85% of deployed capacity. MSC’s USD 24 billion acquisition of Hutchison Ports terminals added 51 million TEU of annual handling capacity, cementing the line’s integrated port-to-ocean model and lifting its projected terminal market share to 15% by 2028. Alliance realignment effective January 2025 dissolved the 2M partnership and established the Maersk–Hapag-Lloyd Gemini network, targeting schedule reliability above 90% through tighter service loops and coordinated slow steaming. The Ocean Alliance extended its pact through 2032, emphasizing service breadth rather than direct consolidation.

Technology adoption is now the premier differentiation lever. MSC and CMA CGM deploy AI-based voyage planning and predictive maintenance suites that lower bunker consumption and unplanned downtime. DB Schenker’s Ocean Bridge platform expands data access to shippers, integrating inland milestones and carbon footprint dashboards. These digital advances heighten switching costs for cargo owners and create service quality tiers within an otherwise commoditized rate environment.

Regulatory compliance is accelerating capital expenditure across the fleet. The orderbook of more than 500 dual-fuel ships favors lines with robust balance sheets and long-term charter portfolios. Smaller regional carriers face strategic choices between niche specialization and partnership with larger alliances to satisfy shippers’ decarbonization goals. Consequently, merger and acquisition activity is likely to continue, particularly where integrated logistics capabilities align with port ownership.

Container Shipping Industry Leaders

MSC Mediterranean Shipping Company

A.P. Moller – Maersk

CMA CGM

COSCO Shipping Lines

Hapag-Lloyd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: MSC completed the acquisition of Hutchison Ports’ terminal assets outside China for EUR 22.765 billion (USD 25.12 billion), adding 39 terminals across 21 countries and 51 million TEU of annual capacity.

- January 2025: CMA CGM acquired majority control of Santos Brasil, operator of Tecon Santos, the largest South American box terminal at 2.5 million TEU, with an expansion plan to 3.0 million TEU.

- January 2025: Alliance restructuring took effect with the Maersk–Hapag-Lloyd Gemini cooperation, while MSC began operating independently with close to 20% global capacity.

- December 2024: The EU–Mercosur free-trade agreement was finalized, paving the way for EUR 56 billion (USD 61.80 billion) in incremental trade between the two blocs.

Global Container Shipping Market Report Scope

Container shipping refers to transportation through containers from one place to another. Unlike conventional shipping, container shipping uses containers of various standard sizes to load, transport, and unload goods or objects. As a result, containers can be moved by trains, ships, and trucks.

The report provides a comprehensive background analysis of the container shipping market, covering the current market trends, restraints, technological updates, and detailed information on various segments and the industry's competitive landscape. The impact of COVID-19 has also been incorporated and considered during the study.

The container shipping market is segmented by size (small, large, and high cube containers), type (general container shipping and reefer container shipping), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers market size and forecasts value (USD) for all the above segments.

| 20-Foot (TEU) |

| 40-Foot (FEU) |

| Others |

| General |

| Reefer |

| Full-Container-Load (FCL) |

| Less-Than-Container-Load (LCL) |

| FMCG and Retail |

| Manufacturing and Automotive |

| Healthcare and Pharmaceuticals |

| Electronics and Electrical Equipment |

| Industrial Chemicals and Raw Materials |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Container Size | 20-Foot (TEU) | |

| 40-Foot (FEU) | ||

| Others | ||

| By Container Type | General | |

| Reefer | ||

| By Service | Full-Container-Load (FCL) | |

| Less-Than-Container-Load (LCL) | ||

| By End-User Industry | FMCG and Retail | |

| Manufacturing and Automotive | ||

| Healthcare and Pharmaceuticals | ||

| Electronics and Electrical Equipment | ||

| Industrial Chemicals and Raw Materials | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

How big is the Container Shipping Market?

The Container Shipping Market size is expected to reach USD 123.14 billion in 2026 and grow at a CAGR of 2.92% to reach USD 142.07 billion by 2031.

What is the current Container Shipping Market size?

In 2026, the Container Shipping Market size is expected to reach USD 123.14 billion.

What is the expected value of the container shipping market in 2031?

The container shipping market is forecast to reach USD 142.07 billion by 2031 at a 2.92% CAGR.

Which container size holds the largest share of global traffic?

The 40-foot container segment led with 50.62% share of 2025 revenue and is projected to maintain dominance through 2031.

Which region is growing fastest for container lines?

Asia-Pacific is forecast to post the highest regional CAGR at 4.12% between 2026 and 2031, buoyed by intra-Asian trade expansion.

Why are reefer containers gaining importance?

Rising demand for temperature-controlled pharmaceuticals and perishables is driving reefer container volumes, which are set to grow at a 3.36% CAGR.

How are environmental regulations affecting vessel orders?

IMO energy-efficiency rules and EU carbon costs are accelerating orders for dual-fuel ships, with more than 500 such vessels on order as of late 2024.

What was the largest recent port acquisition?

MSC’s purchase of Hutchison Ports’ global terminals for EUR 22.765 billion (USD 25.12 billion) in Mar 2025 added 51 million TEU of handling capacity and marked the biggest port asset deal on record.

Page last updated on: