Commercial Microwave Ovens Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

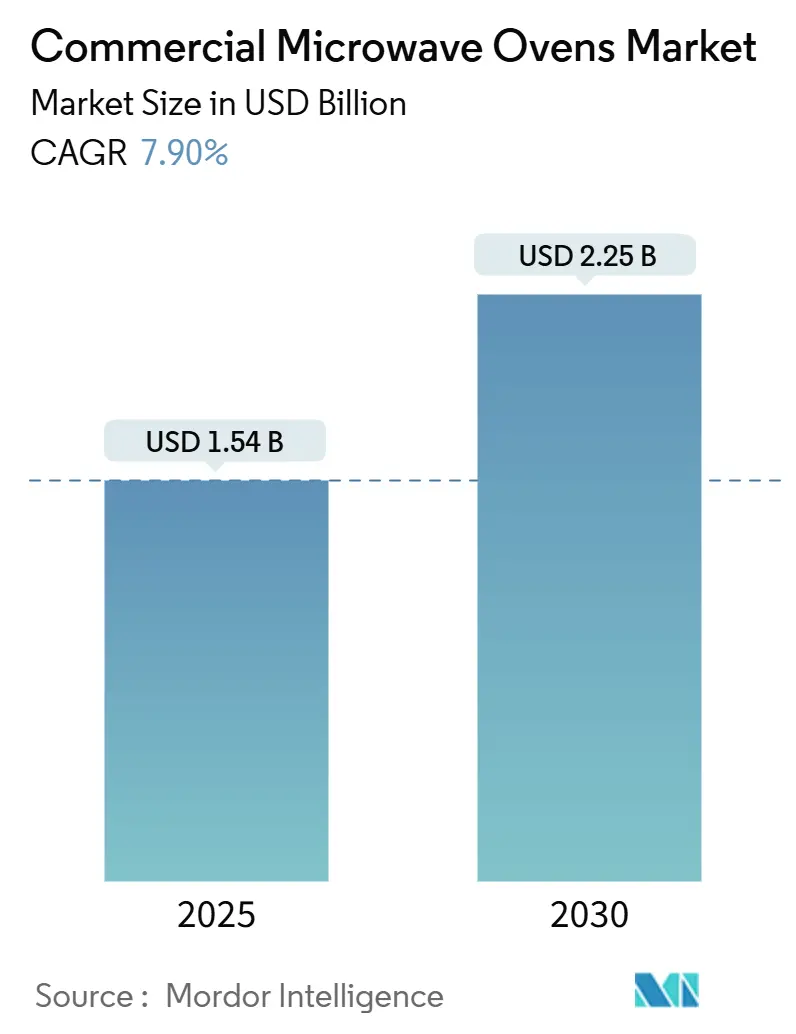

| Market Size (2025) | USD 1.54 Billion |

| Market Size (2030) | USD 2.25 Billion |

| Growth Rate (2025 - 2030) | 7.90% CAGR |

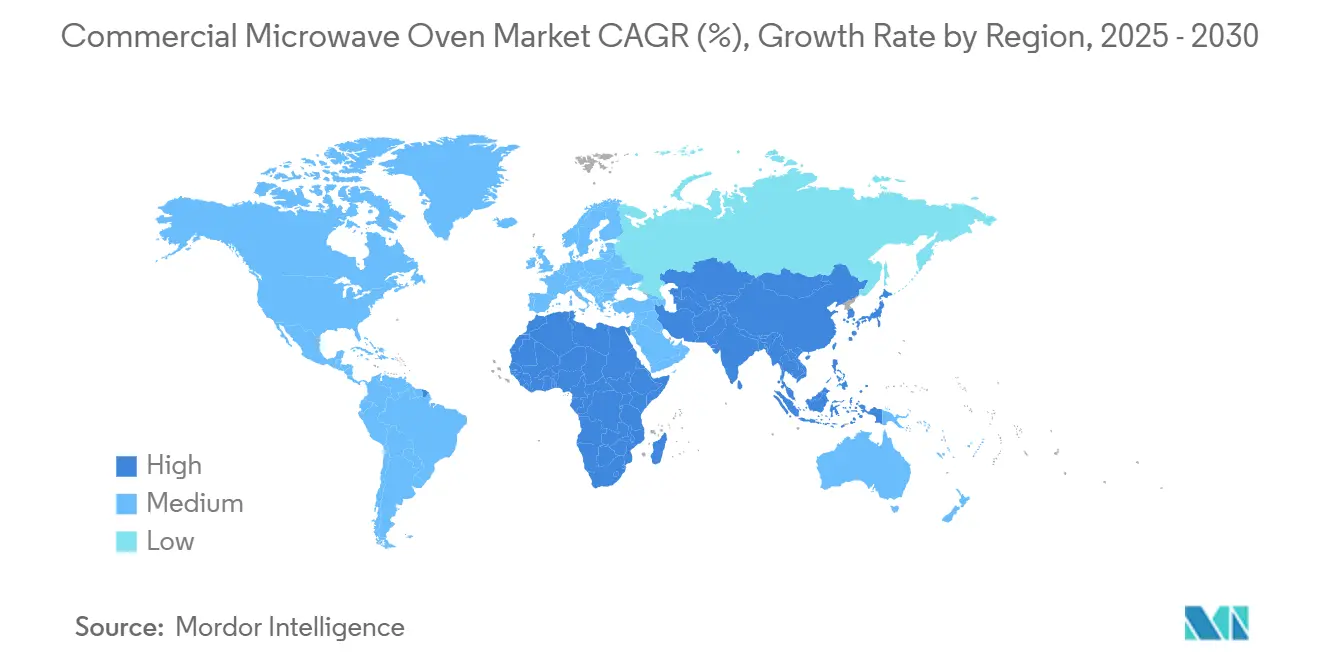

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

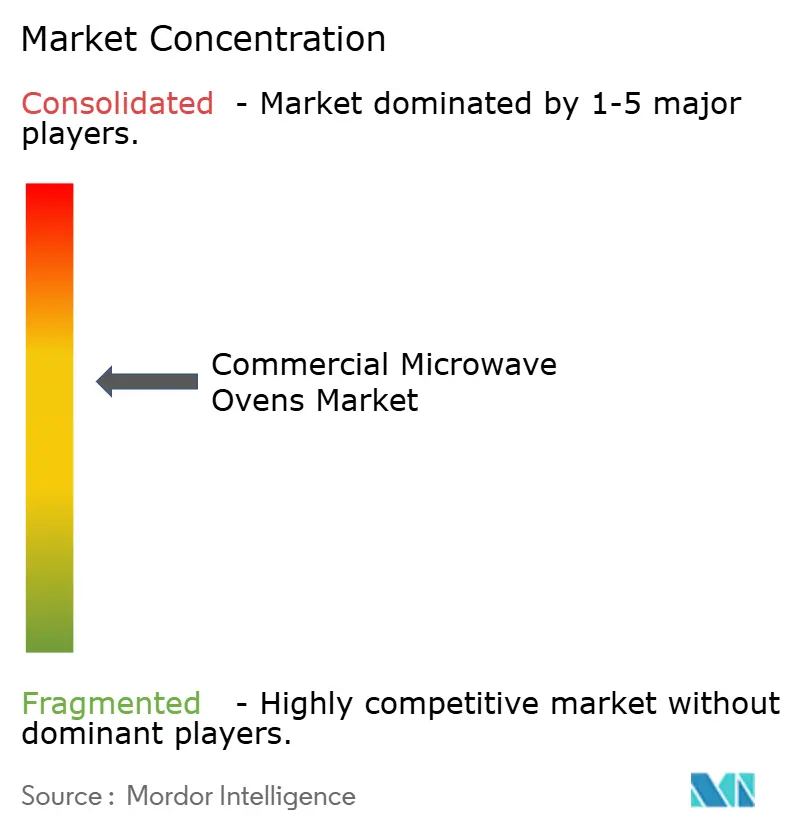

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Commercial Microwave Ovens Market Analysis by Mordor Intelligence

The commercial microwave ovens market size stood at USD 1.54 billion in 2025 and is forecast to reach USD 2.25 billion by 2030, expanding at a 7.9% CAGR. Robust demand originates from quick-service restaurants (QSRs) that rely on programmable, high-throughput ovens to offset labor shortages and keep service times below two minutes during peak traffic. Investments in AI-enabled self-diagnostics and inverter-based power systems are widening the performance gap between legacy magnetron models and next-generation solutions, helping operators meet tightening energy-efficiency mandates in North America and the European Union. Ventless high-speed combination formats that merge microwave and convection functions are winning projects in urban sites where building codes discourage costly hood installations. Meanwhile, the commercial microwave ovens market is also benefiting from the growth of digital purchasing, as procurement managers accelerate equipment evaluations through online configurators that shorten the order-to-installation cycle.

Key Report Takeaways

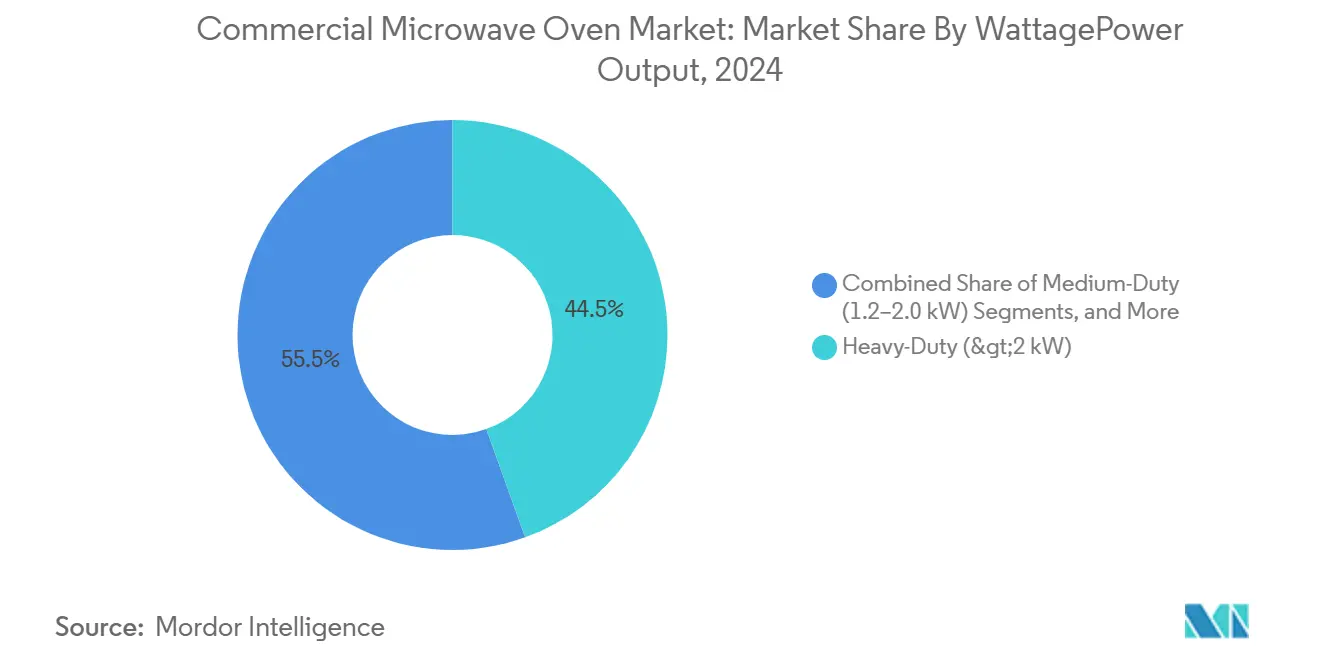

- By wattage/power output, heavy-duty ovens above 2.0 kW captured 44.52% of the commercial microwave ovens market share in 2024, and the segment is set to progress at a 7.88% CAGR through 2030.

- By product type, countertop and freestanding formats led with 52.31% revenue share in 2024, while high-speed combination ovens are advancing at a 9.56% CAGR over the same period in the commercial microwave ovens market.

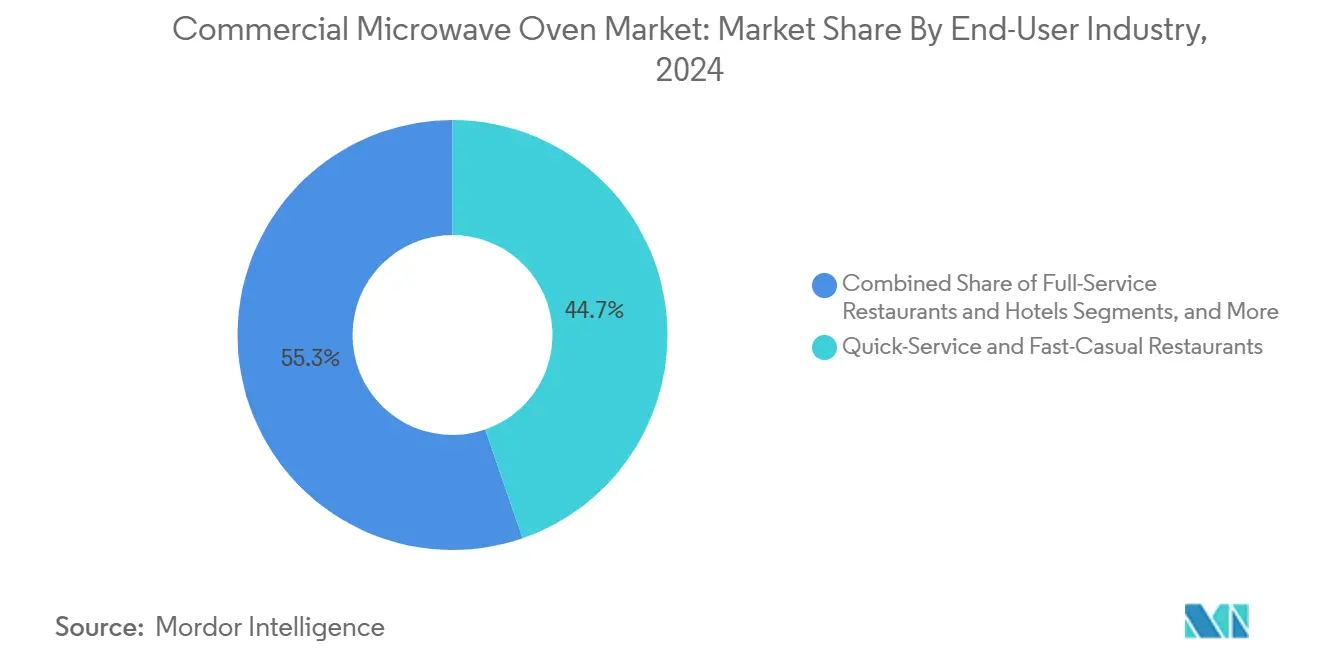

- By end-user industry, QSRs held 44.69% share of the commercial microwave ovens market size in 2024; convenience and grocery stores are projected to expand at an 8.12% CAGR to 2030.

- By distribution channel, offline dealers retained 61.53% share in 2024, but online sales are growing at an 11.31% CAGR as digital ordering gains acceptance in the commercial microwave ovens market.

- By geography, North America commanded 34.87% share in 2024, while Asia-Pacific is forecast to record the fastest CAGR at 8.45% through 2030 in the commercial microwave ovens market.

- The competitive arena, with Panasonic, Midea Group, Sharp, Ali Group, and Whirlpool collectively controlling significant market share in 2024.

Global Commercial Microwave Ovens Market Trends and Insights

Drivers Impact Analysis

| Driver | ~ (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficient magnetron and inverter technologies | +1.2% | North America and EU regulatory zones, expanding to APAC | Long term (≥ 4 years) |

| Post-COVID labour shortages boosting kitchen automation | +2.1% | North America and EU core markets | Short term (≤ 2 years) |

| Stricter food-safety audits favouring programmable ovens | +1.0% | Global, with early adoption in regulated markets | Medium term (2-4 years) |

| Ventless high-speed combo ovens gaining traction | +0.9% | Urban markets globally, concentrated in space-constrained locations | Medium term (2-4 years) |

| AI-enabled self-diagnostics reducing downtime | +0.7% | Developed markets initially, expanding to emerging economies | Long term (≥ 4 years) |

Source: Mordor Intelligence

Growing QSR Penetration and Meal-Delivery Kitchens

Ghost kitchens and delivery-only formats now anchor expansion strategies for multinational chains, elevating the commercial microwave ovens market to mission-critical status in locations that trade floor space for throughput. Compact heavy-duty units enable operators to process hundreds of orders per hour without sacrificing temperature consistency, while programmable interfaces minimize on-site training requirements. Delivery brands further embed remote monitoring software that links multiple kitchens to a centralized dashboard for live quality control. This ability to fine-tune cook cycles across disparate sites strengthens menu uniformity and reduces waste, reinforcing the role of advanced microwave platforms as productivity multipliers in lean labor environments.

Energy-Efficient Magnetron and Inverter Technologies

Solid-state microwave generators are steadily replacing vacuum-tube magnetrons in premium segments, trimming electricity consumption by up to 15% and extending component life cycles beyond 100,000 hours. Inverter circuitry delivers continuous rather than pulsed energy, permitting gentle ramp-up profiles that prevent protein drying and promote uniform reheating—attributes prized by food-safety auditors. Operators also leverage connectivity features that allow ovens to participate in utility demand-response programs, capturing rebates while meeting corporate sustainability targets. Although capital prices remain 20-25% above conventional units, total cost-of-ownership models that incorporate lower maintenance outlays are accelerating adoption in power-constrained European kitchens and high-utility-rate U.S. metropolitan areas.

Post-COVID Labor Shortages Boosting Kitchen Automation

Restaurant labor vacancy rates in the United States hovered near 12% through 2024, driving operators to automate repetitive cooking tasks wherever possible. Touchscreen-driven recipe libraries embedded in commercial microwave ovens cut training curves to a few minutes, allowing new hires to reach full productivity on their first shift. Manufacturers now preload region-specific HACCP-compatible programs that lock cooking parameters once approved, eliminating deviations that might trigger customer complaints. Enhanced self-diagnostics alert managers to door-seal wear and magnetron aging before failures occur, reducing service calls and extending run time during critical dayparts. These advantages entrench automated microwave solutions as cornerstone technologies in labor-stressed foodservice formats.

Stricter Food-Safety Audits Favouring Programmable Ovens

Updated cooking guidelines released by the USDA’s Food Safety and Inspection Service in April 2024 intensified documentation requirements for meat and poultry reheating, compelling operators to generate time-temperature logs that withstand third-party inspections [1]Source: USDA, “Cooking Guidelines for Meat and Poultry Products,” fsis.usda.gov. . Integrated data recorders inside modern commercial microwave ovens automatically capture each cook cycle, storing files in the cloud for seven years or longer as required by corporate policy. The ability to demonstrate compliance on demand converts regulatory risk into a competitive advantage for chains that standardize on programmable models. Feature-rich ovens priced 12-18% above base units are still selling briskly because audit failures can result in multi-day outlet closures that dwarf the equipment premium.

Restraints Impact Analysis

| Restraint | ~ (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising raw-material costs (steel, semiconductors) | -1.4% | Global manufacturing hubs, with spillover effects worldwide | Short term (≤ 2 years) |

| Competition from rapid-cook convection ovens | -0.8% | North America and EU markets with established convection adoption | Medium term (2-4 years) |

| Cyber-security concerns in IoT-connected models | -0.5% | Developed markets with high connectivity penetration | Medium term (2-4 years) |

| Regulatory uncertainty around RF emissions in emerging markets | -0.6% | Emerging economies with evolving regulatory frameworks | Long term (≥ 4 years) |

Source: Mordor Intelligence

Rising Raw-Material Costs (Steel, Semiconductors)

A 27% jump in hot-rolled stainless prices during 2024 forced several OEMs to institute two sequential list-price increases, narrowing the affordability gap between mid-range and entry-level microwave classes. Simultaneously, semiconductor shortages delayed delivery of touch-panel modules, stretching lead times for premium SKUs from six to 12 weeks in early 2025. Some buyers responded by extending replacement cycles or refurbishing existing fleets, curbing near-term volume growth. Market leaders with long-term supply contracts and vertically integrated fabrication facilities partially offset these headwinds, reinforcing a consolidation narrative that gradually shifts bargaining power toward larger players.

Competition from Rapid-Cook Convection Ovens

Hybrid convection systems capable of browning finished foods in 60-120 seconds are eroding microwave share in the sandwich and baked-goods categories. Equipment trials conducted by U.S. café chains in late 2024 demonstrated that crust texture and cheese melt characteristics influence consumer repeat visits more than absolute throughput speed. While the commercial microwave ovens market still rules beverage heating and pre-cooked entrée reheating, operators pursuing menu differentiation may favor rapid-cook alternatives, especially as unit pricing converges. Microwave OEMs are responding with high-speed combination lines that integrate catalytic air filtration and adjustable fan speeds, but the technology race is tightening.

Segment Analysis

By Wattage/Power Output: Heavy-Duty Dominance Reflects Volume Demands

Heavy-duty models above 2.0 kW maintained 44.52% share of the commercial microwave ovens market in 2024, a lead sustained by QSRs that value 1-minute heat-through times for frozen entrées during meal rushes. Their 7.88% CAGR outlook underscores the willingness of operators to absorb higher utility connections in return for output stability during 700-plus daily cycles. Engineering teams increasingly embed inverter modules that moderate peak draw without sacrificing cook speed, ensuring compliance with building-level energy caps in California and parts of Europe. Mid-duty units posting steady gains in institutional catering segments appeal to budgets constrained by annual capital appropriations, while light-duty categories remain common in forecourt retail where 120-volt receptacles prevail.

Field trials show that inverter-equipped heavy-duty platforms extend magnetron life by 12-15 months, trimming maintenance budgets and bolstering residual asset values at resale. Manufacturers are also standardizing modular component layouts, enabling service technicians to swap boards in minutes and restore uptime during high-occupancy windows. As energy-labeling schemes roll out across Asia-Pacific, power-to-output efficiency ratios could become formal procurement criteria, reinforcing the segment’s technological arms race and widening barriers to entry for niche brands.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Countertop Solutions Lead Despite Combo Innovation

Countertop and freestanding formats accounted for a dominant 52.31% share in 2024, primarily because their plug-and-play installation profile appeals to franchisees operating within predefined build-out budgets. These units typically require no mechanical fastening, shortening remodeling projects by as much as three days. High-speed combination ovens, projected to expand at 9.56% CAGR, are capturing new build pipelines at airport concessions and premium convenience stores where menu items demand both volumetric speed and surface browning. Built-in solutions remain entrenched in hotel banqueting suites that integrate equipment flush with stainless workstations to maximize aisle clearance.

Ventless catalytic filters, once exclusive to combi-ovens, are now appearing in countertop microwaves, allowing franchisees to bypass hood permitting even in legacy buildings. This evolution levels the playing field for small-format outlets situated in historic districts subject to strict building codes. Meanwhile, glass-touch doors and full-color LCD recipe screens are migrating down from premium lines, raising baseline usability expectations across the commercial microwave ovens market.

By End-User Industry: QSR Leadership Faces Convenience Store Challenge

QSR operators retained 44.69% share of the commercial microwave ovens market size in 2024, bolstered by standardized menus centered on frozen protein portions reheated to target core temperatures within 45–60 seconds. Yet convenience and grocery stores are logging the fastest 8.12% CAGR, propelled by the roll-out of hot grab-and-go islands that extend shopper dwell time and lift basket value. Retailers favor touchscreen-based microwaves that auto-populate recommended cook codes via UPC scans, eliminating staff guesswork and reducing customer wait times. Full-service restaurants take longer to refresh equipment inventories, but premium steak-house chains are beginning to deploy specialized models for consistent side-dish finishing during banquet events.

In institutional catering, rigid service windows make reliability paramount; thus, procurement committees tend to award longer-term supply contracts to brands offering on-site technician coverage. These multiyear deals stabilize revenue streams for OEMs and dampen unit price volatility, generating predictable replacement cycles that feed the aftermarket spare-parts ecosystem.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Transformation Accelerates Online Growth

Offline distributors remained the preferred purchasing route, controlling 61.53% of 2024 shipments thanks to value-added services such as site surveys, voltage checks and start-up calibration. However, online orders are projected to grow at an 11.31% CAGR as buyers grow comfortable finalizing specifications through 3-D product viewers and augmented-reality placement tools. Large chains now negotiate framework agreements that embed direct-to-operator e-storefronts, enabling local franchisees to purchase approved SKUs with pre-negotiated pricing and warranty terms.

For OEMs, digital channels lower the cost of customer acquisition and provide granular usage analytics once units are onboarded to cloud dashboards. Dealers are countering by bundling preventive-maintenance subscriptions and priority parts delivery, revenue streams less vulnerable to e-commerce encroachment. As cybersecurity competencies strengthen, embedded payment modules within smart-oven control panels could eventually link directly to spare-parts portals, further blurring the line between equipment and e-commerce experience.

Geography Analysis

North America retained 34.87% share in 2024, anchored by an installed base exceeding 1.1 million commercial units. Energy rebates for high-efficiency microwaves reach USD 300 per unit in some U.S. states, shortening payback periods and supporting replacement demand. The commercial microwave ovens industry in Canada is also benefiting from tax credits for kitchen electrification retrofits.

Asia-Pacific’s 8.45% CAGR forecast reflects aggressive QSR expansion in Tier-2 Chinese cities, where urban disposable incomes climbed 6.4% in 2024, and India’s deployment of convenience retail formats along new expressways. Domestic producers such as Midea Group are scaling smart-factory capacity, shipping AI-enabled ovens domestically and to Southeast Asia with lead times under 30 days [2]Source: Midea Group, “2024 Interim Financial Report,” midea.com.. In developed Asia, Japan and South Korea are early adopters of Wi-Fi-connected diagnostic dashboards that align with national digital-transformation policies.

Europe’s mature market shows a steady uptake of inverter-based designs that satisfy Eco-design directives capping idle power draw at 0.5 W from January 2026 onward. Regional operators increasingly evaluate lifecycle carbon footprints alongside acquisition cost, turning attention to recyclable chassis materials and manufacturer take-back programs. Meanwhile, Middle East and African demand is concentrated in global hotel chains and airport concessions where investment decisions hinge on demonstration of RF-emission compliance to evolving local standards [3]Source: Midea Group, “2024 Interim Financial Report,” midea.com..

Competitive Landscape

Moderate fragmentation defines the competitive arena, with Panasonic, Midea Group, Sharp, Ali Group, and Whirlpool collectively controlling a considerable but not overwhelming slice of annual unit volumes in 2024. Ali Group’s decision to merge its acquired Welbilt portfolio under a single North American brand unlocked cross-selling opportunities that align microwave sales with beverage dispensers and ice machines, strengthening bid packages targeting nationwide QSR rollouts. Panasonic and Sharp are leveraging consumer-electronics R&D pipelines to shorten innovation cycles, introducing algorithms that adjust output power in real time based on humidity-sensor feedback.

Technology differentiation is the core battleground. Midea’s latest solid-state generator eliminated traditional filament warm-up lag, enabling near-instant readiness for successive cycles and promising 50% longer mean-time-between-failures. Sharp’s Celerity platform marries European convection elements with inverter microwaves to triple cooking speed for whole poultry without preheat delays. Whirlpool has prioritized small-footprint, ventless designs that address North America’s shift toward urban footprints under 1,000 ft².

After-sales ecosystems further shape competition. Manufacturers with proprietary service networks can guarantee two-hour response windows in metropolitan markets, a decisive factor for chains losing USD 2,500 per hour of downtime during lunch peaks. Cloud-based diagnostics that auto-dispatch parts to technicians before arrival cut first-visit failure rates below 10%, improving operator loyalty and locking in subscription revenue for firmware upgrades. These service innovations blur hardware and software boundaries, making total cost of ownership the focal metric in procurement tenders and sustaining the commercial microwave ovens market’s premiumization trend.

Commercial Microwave Ovens Industry Leaders

-

Panasonic Corporation

-

Midea Group (Galanz)

-

Sharp Corporation

-

Ali Group (Amana / Menumaster)

-

Whirlpool Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Panasonic deepened its collaboration with Fresco to embed AI cooking assistants in HomeCHEF 4-in-1 ovens, enabling automated recipe adaptation.

- March 2025: Ali Group North America rebranded its operations as Welbilt after the Welbilt Inc. acquisition, strengthening brand equity among QSR buyers.

- February 2025: Middleby Corporation acquired GBT GmbH Bakery Technology to enhance European full-line bakery solutions and integrate high-volume microwave modules.

Global Commercial Microwave Ovens Market Report Scope

Microwave ovens are electronic devices that utilize electromagnetic waves for cooking and heating food and beverage products in a short period of time. Electromagnetic waves or microwaves radiate heat in the form of microwave energy. This energy is exposed to the water molecules present in food products. The commercial microwave ovens market is segmented by product duty type (commercial heavy-duty microwave ovens, commercial medium-duty microwave ovens, and commercial light-duty microwave ovens), product capacity type (under 1 cu ft type, 1 to 1.9 cu ft type, and over 2 cu ft type), application (foodservice industry, food industry, and other applications), control feature (button controls and dial controls), distribution channel (multi-branded stores, specialty stores, online stores, and other distribution channels), and geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa). The report offers the market sizes and forecasts by value (in USD) for all the above segments.

Key Questions Answered in the Report

What is the size of the commercial microwave ovens market and how fast is it growing?

The market is valued at USD 1.54 billion in 2025 and is forecast to reach USD 2.25 billion by 2030, reflecting a 7.9% CAGR.

Which wattage category commands the largest market share?

Heavy-duty models above 2.0 kW account for 44.52% of global revenue and are projected to grow at a 7.88% CAGR through 2030

Which is the fastest growing region in Commercial Microwave Ovens Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Why is Asia-Pacific the fastest-growing region?

Rapid QSR expansion in China, India and Southeast Asia, combined with urbanization and rising disposable incomes, is driving an 8.45% CAGR in the region.

How are labor shortages affecting equipment selection?

Persistent staffing gaps push operators toward programmable microwaves with self-diagnostics and preset recipes that cut training time and lower downtime.

What technologies are improving energy efficiency in commercial microwaves?

Inverter and solid-state semiconductor systems deliver continuous power modulation, reducing electricity use by up to 15% while extending component life.

How is the shift to online procurement influencing sales channels?

Although offline dealers still hold 61.53% share, online orders are growing at 11.31% CAGR as buyers use digital configurators and e-commerce portals for faster purchasing.

Page last updated on: June 26, 2025