Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.74 Billion |

| Market Size (2031) | USD 2.25 Billion |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

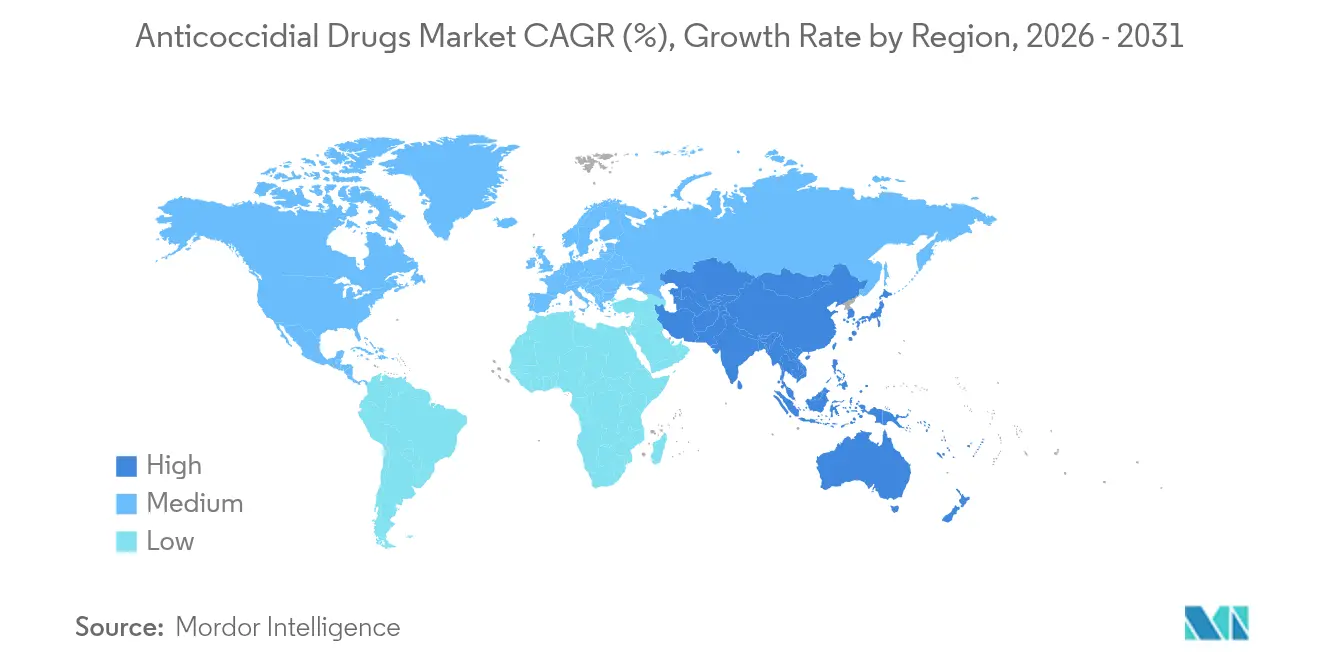

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anticoccidial Drugs Market Analysis by Mordor Intelligence

The Anticoccidial Drugs Market size was valued at USD 1.66 billion in 2025 and is estimated to grow from USD 1.74 billion in 2026 to reach USD 2.25 billion by 2031, at a CAGR of 5.28% during the forecast period (2026-2031).

Robust demand from integrated poultry and cattle operations, widening residue restrictions in export channels, and a measured pivot toward botanical feed additives are reshaping competitive dynamics. Ionophore products still underpin 54.22% of 2025 revenue, yet formulators are accelerating investment in phytogenic blends and live-attenuated vaccines to counter antimicrobial-resistance headwinds. China’s 25.1 million-tonne poultry output in 2024 and India’s 8% annual broiler expansion are amplifying Asia-Pacific procurement, while volatility in glucose-based fermentation inputs compresses margins for commodity producers. U.S. Section 232 tariff risks and the FDA’s Veterinary Feed Directive continue to steer North American buyers toward locally manufactured ionophores and vaccine rotations.

Key Report Takeaways

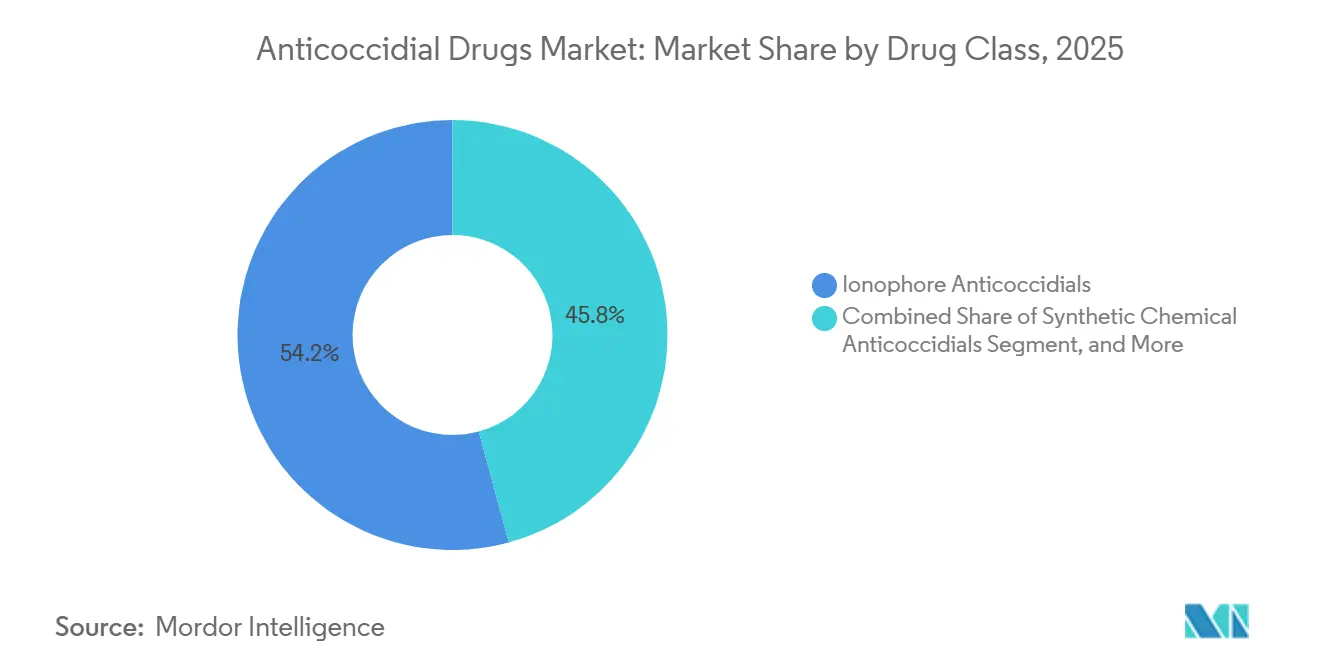

- By product category, ionophores led with 54.22% of the anticoccidial market share in 2025, while botanical and phytogenic alternatives are projected to expand at a 5.86% CAGR through 2031.

- By animal type, cattle accounted for 58.07% of the anticoccidial market in 2025; companion animals are advancing at a 7.99% CAGR through 2031.

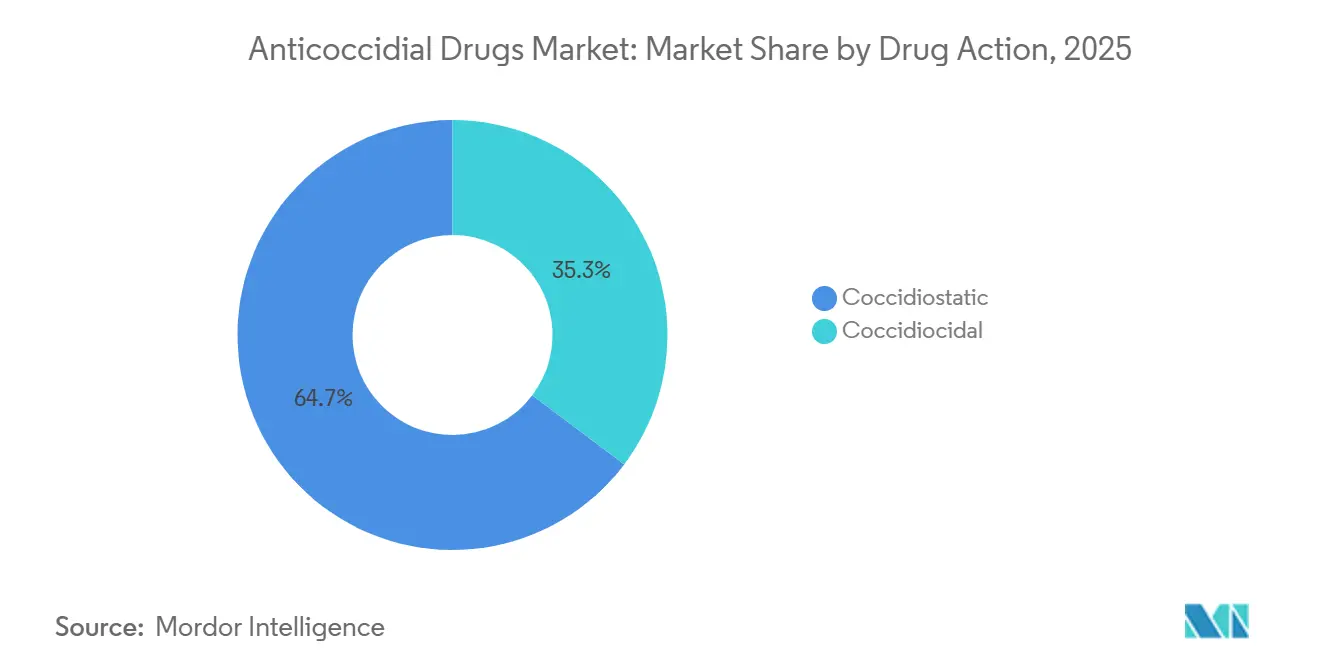

- By drug action, coccidiostatic formulations accounted for 64.72% of 2025 revenue, whereas coccidiocidal agents are on track for a 6.78% CAGR through 2031.

- By distribution channel, veterinary hospitals held a 42.68% share of the anticoccidial market in 2025, and online pharmacies recorded the fastest projected CAGR of 6.98% to 2031.

- By geography, North America accounted for 40.91% of revenue in 2025; Asia-Pacific is forecast to be the fastest-growing region at a 9.35% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anticoccidial Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Integrated Poultry Production in Emerging Economies | +1.8% | Asia-Pacific core, spill-over to Middle East & Africa | Medium term (2-4 years) |

| Rising Prevalence and Economic Burden of Coccidiosis on Intensive Livestock | +1.2% | Global, concentrated in tropical and subtropical zones | Long term (≥ 4 years) |

| Regulatory Preference for Non-Medically Important Antimicrobials | +0.9% | North America & EU, influencing export-oriented producers in Latin America and Asia | Medium term (2-4 years) |

| Industry Shift Toward Preventive Feed Additives to Improve Feed Efficiency | +0.7% | Global, strongest uptake in North America and Western Europe | Short term (≤ 2 years) |

| Adoption of Precision-Dosing Micro-Encapsulated Anticoccidials Via IoT Monitoring | +0.5% | North America & EU early adopters, gradual diffusion to large-scale Asia-Pacific integrators | Long term (≥ 4 years) |

| Tariff-Driven Localization of Ionophore API Manufacturing | +0.4% | United States, secondary effects in India and Brazil | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Integrated Poultry Production in Emerging Economies

Vertically integrated producers in China, India, and the Gulf states continue to consolidate disease-control protocols, mandating standardized anticoccidial regimens that cut mortality and improve feed efficiency.[1]National Bureau of Statistics of China, “China Poultry Production 2024,” stats.gov.cn Expanded contract-grower networks embed ionophore rotation rules into supply agreements, compressing purchasing cycles and favoring volume-discount negotiations with top manufacturers.

Rising Prevalence and Economic Burden of Coccidiosis on Intensive Livestock

Global economic losses exceed USD 10 billion, driven by suboptimal weight gain and elevated feed-conversion ratios in high-density systems. Cage-free mandates in the EU and North America inadvertently raise litter contact, lifting incidence by 15-20%.[2]European Food Safety Authority, “Welfare Transition and Coccidiosis Incidence,” efsa.europa.eu Ionophore-based prevention remains economically justified whenever mortality tops 2% in broilers.

Regulatory Preference for Non-Medically Important Antimicrobials

The FDA’s Veterinary Feed Directive exempts ionophores from growth-promotion bans, allowing continued non-prescription use, whereas the EMA imposes lesion-score benchmarks yet maintains registrations for salinomycin and monensin. Formulators prioritize ionophore extensions to leverage this regulatory latitude.

Industry Shift Toward Preventive Feed Additives to Improve Feed Efficiency

Micro-encapsulated blends such as Kemin’s FORMYL enable delayed intestinal release, delivering an 8-12% uplift in average daily gain for weaned piglets. Retail sustainability scorecards from McDonald’s and Tyson Foods are accelerating procurement of reduced-antimicrobial feeds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Antimicrobial Resistance & Rotation Fatigue Among Existing Drug Classes | -1.1% | Global, most acute in Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Stringent Residue Limits & Prophylactic Bans in Key Export Markets | -0.8% | Export-oriented producers in Brazil, Thailand, targeting EU and Japan | Medium term (2-4 years) |

| Rapid Uptake of Multi-Valent Eimeria Vaccines in NAE Poultry Segments | -0.6% | North America and Western Europe, niche penetration in premium segments | Short term (≤ 2 years) |

| Volatile Ionophore-Precursor Prices from Supply-Chain Shocks | -0.5% | Global, transmitted through feed-additive supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Antimicrobial Resistance & Rotation Fatigue Among Existing Drug Classes

WHO surveillance in 15 countries logged monensin-resistant Eimeria in more than 40% of Asian broiler flocks, shortening effective rotation windows from 12 to 6 months.[3]World Health Organization, “AMR Surveillance in Livestock 2025,” who.int Adding drug classes increases feed costs by up to USD 0.02 per bird, nudging integrators toward vaccines despite higher unit prices.

Stringent Residue Limits & Prophylactic Bans in Key Export Markets

EU and Japanese residue ceilings compel Brazilian and Thai exporters to adopt multi-day withdrawal periods or vaccine-only programs, reducing treatment flexibility and lifting feed-conversion ratios by 3-4%. Smallholders struggle to finance parallel NAE and conventional lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Ionophores Anchor Revenue, Botanicals Capture Innovation Premium

Ionophore anticoccidials held 54.22% of the anticoccidial market share in 2025, led by monensin’s wide species label and USD 300 million-plus annual sales. Regionally, Asia-Pacific buyers favor salinomycin and narasin for pelleting stability, while combination products target breeder flocks with extended cycles.

Botanical alternatives are growing at a 5.86% CAGR, leveraging organic certification pull-through. Rabar’s Cox-Free reduced mortality by 63% in Brazil and India, while dsm-firmenich’s AccuGut C.1 delivered feed-conversion parity within 2% of monensin in field trials. Ceva’s Hungary facility, due to end-2026, will add 8 billion vaccine doses per year to serve the NAE tier.

By Animal Type: Cattle Dominance Masks Companion-Animal Surge

Cattle accounted for 58.07% of the anticoccidial market in 2025, riding on feedlot adoption of monensin, which lifts feed efficiency by 5-8% and trims methane by up to 15%. Poultry remains secondary in value yet primary in volume, with broiler shuttle programs rotating ionophores and triazines.

Companion-animal revenue is expanding at a 7.99% CAGR as telemedicine platforms normalize coccidiosis diagnosis in puppies and kittens. Ponazuril courses retail at USD 30-50, yielding higher per-dose margins than livestock tonnage.

By Drug Action: Coccidiostats Lead, Coccidiocidals Regain Ground

Coccidiostat formulations accounted for 64.72% of 2025 revenue, reflecting monensin’s immunomodulatory advantage in continuous production. Decoquinate adds calf and lamb coverage, permitting controlled exposure.

Coccidiocidal agents are on a 6.78% CAGR trajectory as resistance undermines stasis strategies. Zoetis’ Clinacox Advance extended protection to 28 days and slashed mortality by 35% in EU trials.

By Distribution Channel: Hospitals Retain Control, E-Commerce Scales Refills

Veterinary hospitals retained 42.68% distribution in 2025 by bundling prescription authority with biosecurity consulting for integrators. Covetrus aggregates clinic demand to secure bulk rates.

Online pharmacies, led by Chewy, are scaling at a 6.98% CAGR as blockchain registries streamline prescription verification and cut fulfillment to under 24 hours.

Geography Analysis

North America accounted for 40.91% of revenue in 2025, underpinned by 9.5 billion U.S. broilers and 95 million cattle that incorporate monensin into feed protocols. Canada’s premium egg sector accelerated vaccine uptake, while Mexico’s peso volatility widened API import costs.

Asia-Pacific is projected to expand at a 9.35% CAGR, propelled by China’s 25.1 million-tonne poultry output and India’s contract-grower ascent. Resistance hotspots in southern China are driving up diclazuril demand despite pricing 30-40% higher.

Europe’s stringent MRLs and welfare rules prioritize vaccines, whereas Latin America balances ionophore economics with EU residue compliance. Middle East & Africa rely on imported APIs; Bimeda’s Dubai hub now supplies South African integrators following its acquisition of Afrivet.

Competitive Landscape

The anticoccidial market is moderately concentrated. Zoetis exited commodity ionophores by divesting its USD 400 million MFA portfolio to Phibro but invested USD 686 million in 2024 R&D to advance biologics. Ceva raised EUR 5.5 billion in 2025 to finance an 8 billion-dose vaccine plant and aims to go public by 2027.

Phibro’s acquisition added six plants and lifted MFA revenue by 9% year-on-year, but left the firm exposed to the risk of EU nicarbazin reauthorization. dsm-firmenich and Rabar differentiate through IoT analytics and phytogenic sourcing, respectively, while U.S. tariff moves may catalyze domestic fermentation entrants.

Anticoccidial Drugs Industry Leaders

Phibro Animal Health Corporation

Vetoquinol S.A.

Elanco Animal Health Incorporated

Zoetis Inc.

Virbac S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Elanco and Medgene announced an H5N1 vaccine for dairy cattle, widening disease-prevention portfolios beyond traditional coccidiosis applications.

- February 2025: Zoetis obtained a conditional FDA license for its Avian Influenza Vaccine H5N2 Subtype for chickens.

- January 2025: MSD Animal Health acquired global rights to the VECOXAN parasiticide brand.

- November 2024: Boehringer Ingelheim introduced VETMEDIN Solution, the first FDA-approved liquid for canine heart failure.

- October 2024: Phibro closed its USD 350 million purchase of Zoetis’ medicated feed additive portfolio.

- October 2024: Elanco secured FDA approval for Credelio Quattro, a broad-spectrum parasiticide for dogs.

Global Anticoccidial Drugs Market Report Scope

As per the scope of the report, coccidiosis is one of the most frequent and prevalent parasitic diseases among animals. Its symptoms include weight loss, mild intermittent to severe diarrhea, feces containing mucus or blood, dehydration, and decreased breeding. Any drug used to combat the progression of coccidiosis in birds or animals, both food-producing and non-food producing, is termed an anticoccidial drug.

The Anticoccidial Drugs Market is segmented by Product (Ionophore Anticoccidials, Synthetic Chemical Anticoccidials, Botanical & Phytogenic Alternatives, Combination Products, Live Attenuated & Recombinant Vaccines), Animal Type (Poultry [Broilers, Layers, Breeders], Cattle, Swine, Sheep & Goats, Aquaculture, Companion Animals), Drug Action (Coccidiostatic, Coccidiocidal), Distribution Channel (Veterinary Hospitals, Veterinary Clinics, Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

By Product

| Ionophore Anticoccidials |

| Synthetic Chemical Anticoccidials |

| Botanical & Phytogenic Alternatives |

| Combination Products |

| Live Attenuated & Recombinant Vaccines |

By Animal Type

| Poultry | Broilers |

| Layers | |

| Breeders | |

| Cattle | |

| Swine | |

| Sheep & Goats | |

| Aquaculture | |

| Companion Animals |

By Drug Action

| Coccidiostatic |

| Coccidiocidal |

By Distribution Channel

| Veterinary Hospitals |

| Veterinary Clinics |

| Online Pharmacies |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Ionophore Anticoccidials | |

| Synthetic Chemical Anticoccidials | ||

| Botanical & Phytogenic Alternatives | ||

| Combination Products | ||

| Live Attenuated & Recombinant Vaccines | ||

| By Animal Type | Poultry | Broilers |

| Layers | ||

| Breeders | ||

| Cattle | ||

| Swine | ||

| Sheep & Goats | ||

| Aquaculture | ||

| Companion Animals | ||

| By Drug Action | Coccidiostatic | |

| Coccidiocidal | ||

| By Distribution Channel | Veterinary Hospitals | |

| Veterinary Clinics | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the anticoccidial market be by 2031?

The anticoccidial market size is projected to reach USD 2.25 billion by 2031, expanding at a 5.28% CAGR from 2026 to 2031.

Which product class dominates revenue today?

Ionophore anticoccidials command 54.22% of 2025 sales, driven by monensin’s broad species label and dual feed-efficiency claims.

What is the fastest-growing animal segment?

Companion-animal demand is advancing at a 7.99% CAGR as pet owners increasingly seek prescription treatments through online pharmacies.

Why is Asia-Pacific the highest-growth region?

Rapid poultry expansion in China and India, combined with integrated business models, is pushing Asia-Pacific toward a 9.35% regional CAGR.

How are regulations shaping product development?

FDA exemptions for ionophores and EU residue ceilings are steering formulators toward non-medically important ionophores, vaccines, and botanical blends that comply with export standards.

Page last updated on: