Market Overview

| Study Period | 2021 - 2030 |

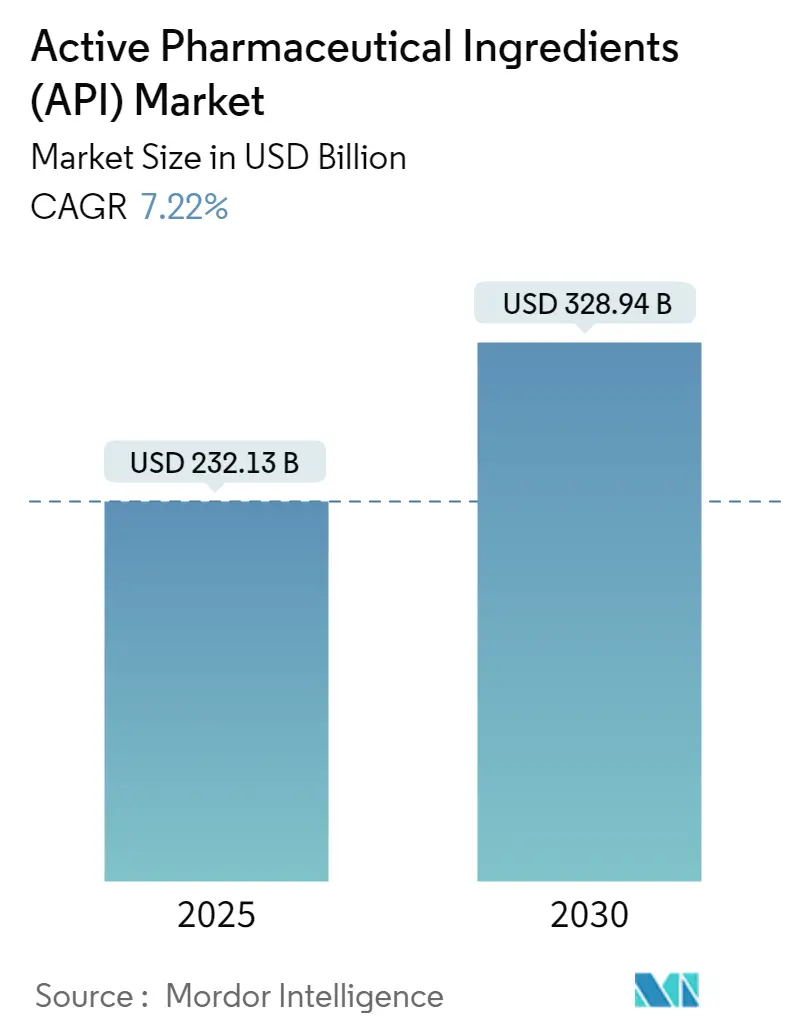

| Market Size (2025) | USD 232.13 Billion |

| Market Size (2030) | USD 328.94 Billion |

| Growth Rate (2025 - 2030) | 7.22% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

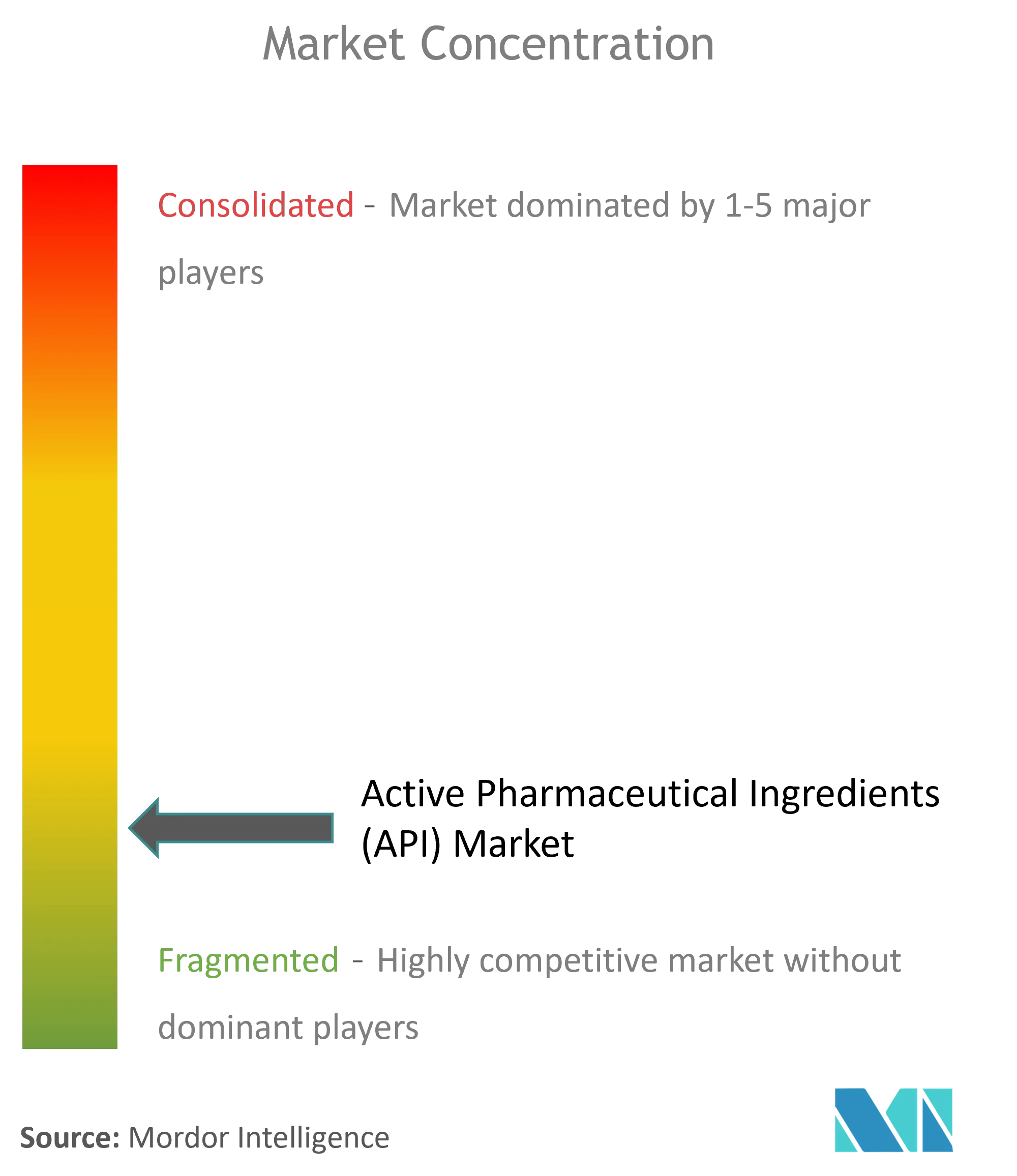

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Active Pharmaceutical Ingredients (API) Market Analysis by Mordor Intelligence

The Active Pharmaceutical Ingredients Market size is estimated at USD 232.13 billion in 2025, and is expected to reach USD 328.94 billion by 2030, at a CAGR of 7.22% during the forecast period (2025-2030).

Sustained growth stems from the pharmaceutical sector’s pivot toward specialized, higher-value molecules, rising demand for targeted therapies, and greater reliance on outsourcing. North America retains leadership on account of stringent regulatory oversight and an established manufacturing base, while Asia is capturing incremental volumes by offering cost-competitive, technologically sophisticated capacity. Strategic reshoring in the United States and Europe, growing adoption of continuous manufacturing, and accelerated development of mRNA platforms are reshaping competitive dynamics. Capital inflows into high-potency and biologic APIs, together with heightened emphasis on supply-chain resilience, are creating further expansion opportunities for companies that combine quality systems with advanced process know-how.

Key Report Takeaways

- By geography, North America led with 41.23% of active pharmaceutical ingredients market share in 2024, whereas Asia is projected to record the fastest 7.70% CAGR through 2030.

- By therapeutic area, cardiovascular applications accounted for 23.71% of the active pharmaceutical ingredients market size in 2024; oncology is advancing at an 8.16% CAGR to 2030.

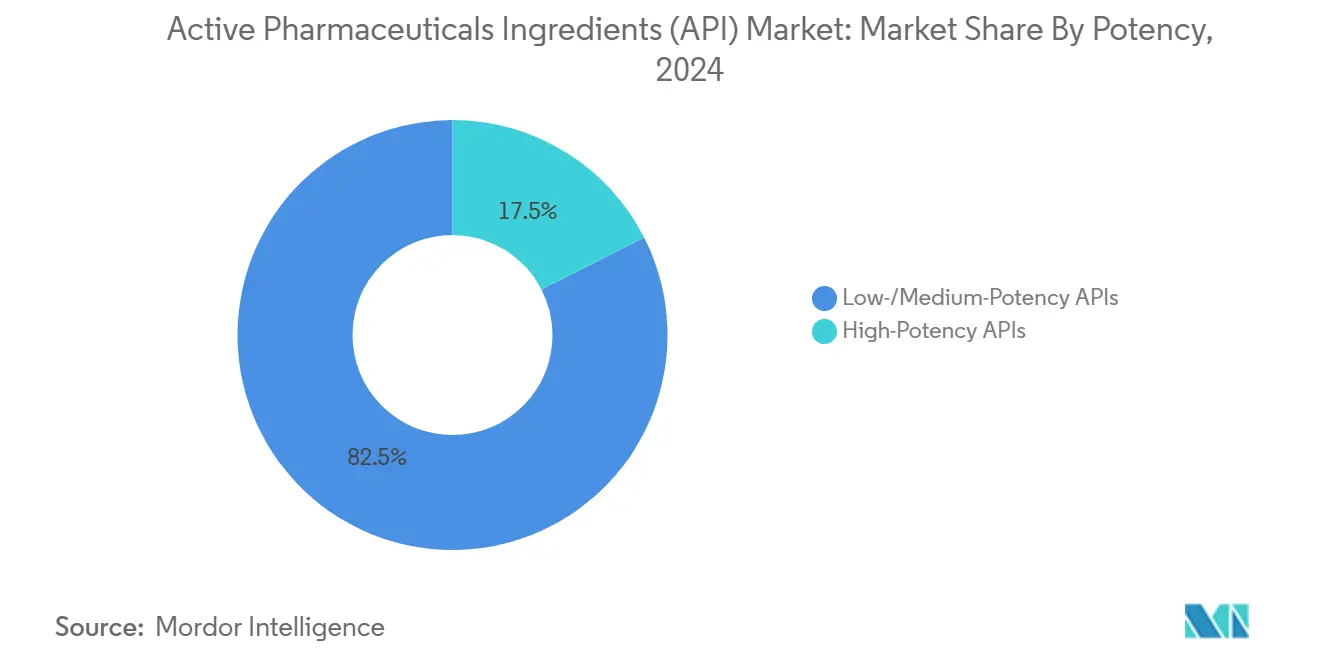

- By potency, low/medium-potency compounds dominated with 82.50% share in 2024, while high-potency APIs are set to expand at a 12.50% CAGR.

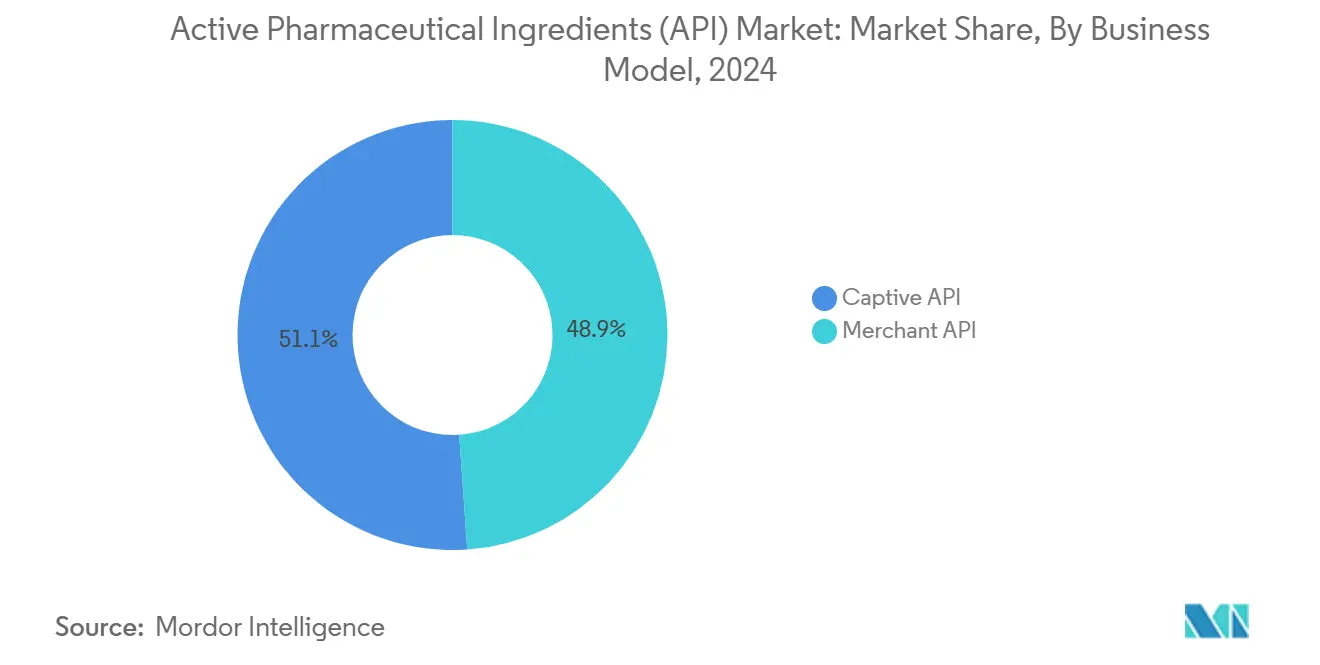

- By business model, captive manufacturing held 51.09% share of the active pharmaceutical ingredients market size in 2024; the merchant segment is growing at 8.07% through 2030.

- By synthesis type, synthetic APIs commanded 65.35% of 2024 revenue; biotech APIs are forecast to register a 9.07% CAGR.

- By molecule type, small molecules captured 62.50% of 2024 sales, whereas biologics are projected to grow at a 10.02% CAGR.

Global Active Pharmaceutical Ingredients (API) Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Surging Demand for High-Potency APIs (HPAPIs) | ~+1.6 | Global, with oncology clusters in US/EU | Medium term (~3-4 yrs) |

| Rapid Expansion of CDMOs Supporting Small/Mid-Sized Pharma | ~+1.2 | APAC, EU, North America | Medium term (~3-4 yrs) |

| Accelerated Vaccine & mRNA Platform Commercialization Post-COVID-19 | ~+0.8 | North America, EU, APAC | Short term (≤2 yrs) |

| Shift Toward Continuous Manufacturing Boosting Output Efficiency | ~+0.5 | North America, EU | Long term (≥5 yrs) |

| Re-shoring Initiatives in US & EU to Reduce China Dependency for Key Starting Materials | ~+0.4 | US, EU | Medium term (~3-4 yrs) |

| Growing Demand for Sustainable “Green Chemistry” Routes Driven by ESG Mandates | ~+0.3 | Global | Long term (≥5 yrs) |

Source: Mordor Intelligence

Surging Demand for High-Potency APIs (HPAPIs)

Heightened focus on precision oncology is driving a sharp uptick in HPAPI requirements, with these molecules already comprising more than 30% of the research pipeline. HPAPIs allow lower dosages yet deliver superior therapeutic outcomes, compelling manufacturers to invest in highly contained facilities. Lonza alone has developed over 50 HPAPI compounds during the past 15 years, operating dedicated lines in Visp and Nansha while meeting FDA and ANVISA standards [1]Lonza AG, “HPAPI Handling and Development,” lonza.com. Such specialised infrastructure creates formidable entry barriers, enabling established firms to secure premium pricing and long-term supply agreements. The swell in potent-compound programs is reshaping capital allocation, prompting both innovators and CDMOs to expand isolator-based suites and advanced analytics capabilities. As oncology pipelines mature, HPAPI volumes are likely to keep rising, reinforcing the segment’s role as a core value driver in the active pharmaceutical ingredients market.

Rapid Expansion of Contract Development & Manufacturing Organizations (CDMOs)

Pharmaceutical companies are increasingly outsourcing API development and commercial manufacturing to CDMOs to optimise capital deployment and accelerate launch timelines. Merchant API output is projected to grow at an 8.07% CAGR through 2030, outpacing captive production. CDMOs now deliver integrated solutions that encompass route scouting, scale-up, analytical development, and regulatory documentation, thereby reducing clients’ risk and infrastructure burden. Investment momentum is most visible in capabilities for high-potency, sterile, and complex synthetic processes that demand niche expertise. Competition among CDMOs is shifting from pure cost advantages toward differentiation based on quality systems and end-to-end technical support, a trend that is redefining value creation across the active pharmaceutical ingredients market.

Accelerated Vaccine & mRNA Platform Commercialisation Post-COVID-19

The success of mRNA vaccines has validated a versatile platform that dramatically compresses development cycles. Companies such as Moderna have 20-plus candidates in active registration pathways, spanning infectious disease, oncology, and rare genetic disorders. mRNA programs rely on lipid components, nucleoside-modified RNA, and refined purification steps, expanding demand for novel APIs and specialised excipients. As clinical data accumulates, developers are adopting modular, continuous processes that enable rapid switchovers between products. The resulting supply-chain activity is reinforcing the strategic importance of technologically agile API suppliers, bolstering long-term growth prospects for the active pharmaceutical ingredients market.

Shift Toward Continuous Manufacturing Boosting Output Efficiency

Continuous flow processes offer tighter reaction control, lower solvent use, and improved safety profiles relative to batch operations. The FDA’s vocal endorsement underscores the technology’s ability to reduce shortages and reinforce quality. Early adopters are already realising shorter cycle times and real-time release potential, especially for high-volume generic APIs and products requiring strict impurity control. Equipment makers are responding with skid-mounted, modular units that facilitate stepwise integration. Continuous manufacturing aligns with Quality by Design principles, confers competitive pricing, and supports environmental targets, making it a catalyst for efficiency across the active pharmaceutical ingredients market.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Volatility in Supply of Key Starting Materials From China & India | ~-1.4 | Global, acute in North America & EU | Short term (≤2 yrs) |

| Capacity Fragmentation Intensifying Price Pressure in Generic Small Molecules | ~-1.2 | APAC, Global generics | Medium term (~3-4 yrs) |

| Inflation-Linked Escalation in Energy & Solvent Costs Impacting Margins | ~-0.8 | Global, especially EU | Short term (≤2 yrs) |

| Complex Global Regulatory Harmonization for Biotech APIs | ~-0.5 | Global, acute in US/EU | Medium term (~3-4 yrs) |

Source: Mordor Intelligence

Volatility in Supply of Key Starting Materials from China & India

USP data show that only 4% of 2023 US drug master files cited domestic manufacturing, whereas India and China together accounted for more than 80%. Disruptions in either hub can ripple through global supply chains, triggering spot shortages and cost spikes. Reliance on single-region sources also complicates regulatory inspections and heightens geopolitical risk. Manufacturers are therefore assessing dual-sourcing strategies, investing in supply-chain visibility tools, and lobbying for incentives to localise critical starting materials. These measures increase compliance costs and elongate development timelines, tempering headline growth in the active pharmaceutical ingredients market.

Capacity Fragmentation Intensifying Price Pressure in Generic Small Molecules

Generic small-molecule APIs face thin margins as numerous producers vie for commoditised, off-patent volumes. India files roughly half of active DMFs with the FDA, followed by China at 32%, fuelling oversupply and driving down prices. Western producers struggle to match the cost economics of these hubs, prompting consolidation and exit from low-margin molecules. While this dynamic speeds the bifurcation between commodity and specialised APIs, it also limits profit pools and dampens short-term revenue expansion within the active pharmaceutical ingredients market.

Segment Analysis

By Business Model: Outsourcing Races Ahead of Captive Production

Merchant suppliers generated 48.91% of 2024 revenue, while captive operations retained a narrow majority at 51.09%. The merchant segment’s 8.07% projected CAGR indicates rising confidence in external partners to handle scale-up under stringent quality expectations. Pharmaceutical companies are reserving in-house capacity for proprietary, high-value molecules yet are transferring late-life-cycle and generic APIs to CDMOs to maximise asset utilisation. The active pharmaceutical ingredients market size for outsourced production is forecast to accelerate further as complex synthetic routes and potency requirements favour specialist providers.

Investment flows into containment suites, continuous processing lines, and advanced analytical laboratories underscore the structural shift in favour of CDMOs. The active pharmaceutical ingredients market therefore rewards suppliers that combine end-to-end development services with proven regulatory track records, particularly for oncology and rare-disease programs that necessitate flexible, small-batch production.

Note: Segment shares of all individual segments available upon report purchase

By Synthesis Type: Biotech APIs Erode Synthetic Dominance

Synthetic pathways still underpin 65.35% of 2024 shipments, yet biotech APIs are set to grow at 9.07% through 2030, narrowing the gap. Recent progress in cell-line engineering, expression optimisation, and downstream purification is lowering unit costs, bringing complex biologics within reach of broader therapeutic categories. The active pharmaceutical ingredients market size for biotech routes is expanding fastest in monoclonal antibodies, peptides, and nucleic-acid-based therapeutics.

Meanwhile, synthetic manufacturers are integrating biocatalysis and chemoenzymatic cascades to shorten step counts and improve yields. This convergence blurs historical distinctions and diversifies risk, anchoring both synthesis modes within a single, more resilient supply architecture. In the near term, synthetic APIs will remain indispensable for small molecules that benefit from mature, scalable chemistries, yet the growth trajectory clearly favours biotech processes.

By Molecule Type: Biologics Mount a Sustained Challenge

Small molecules held 62.50% revenue share in 2024, but biologics are advancing at a striking 10.02% CAGR. Demand for recombinant proteins, antibody-drug conjugates, and cell-based therapies is re-shaping capital allocation strategies, with major manufacturers adding multi-suite bioreactor capacity. The active pharmaceutical ingredients market share for large molecules is therefore poised to climb steadily, particularly in immuno-oncology and autoimmune indications.

These complex entities demand ultraclean environments, single-use technologies, and sophisticated analytics, reinforcing the value of specialised suppliers. For small-molecule producers, competitive advantage now hinges on green chemistry, continuous flow, and process intensification to defend relevance. Over the forecast horizon, a balanced product mix that spans small and large molecules will likely dominate board-room planning, anchoring long-term resilience in the active pharmaceutical ingredients market.

By Potency: High-Potency Compounds Capture Investor Attention

Low- and medium-potency APIs accounted for 82.50% of 2024 revenue, yet the high-potency segment is on track for a 12.50% CAGR. Oncology programs dominate the potent-compound pipeline, requiring occupational exposure levels below 10 µg/m³ and advanced containment. The active pharmaceutical ingredients market size for high-potency products is therefore expanding faster than any other category.

Significant brownfield and greenfield investments underscore the trend. Cambrex recently allocated USD 30 million to its North Carolina site to add isolator-based suites, while Axplora and MilliporeSigma are enlarging HPAPI footprints in Europe and the United States. As product complexity rises, companies that possess validated, scalable potent-compound lines will enjoy pricing power and long-term supply contracts, reinforcing their strategic significance within the active pharmaceutical ingredients market.

Note: Segment shares of all individual segments available upon report purchase

By Therapeutic Area: Oncology Sets the Innovation Pace

Cardiovascular therapies led with 23.71% share in 2024 because of chronic disease prevalence and large patient pools. Oncology is advancing fastest at an 8.16% CAGR as breakthroughs in immunotherapies and targeted small molecules drive mid-single-digit dollar expansion annually. These programs often depend on HPAPIs and intricate synthesis or expression routes, raising technical thresholds. The active pharmaceutical ingredients market size allocated to oncology thus carries a premium, incentivising capacity expansion among specialised CDMOs.

Central nervous system APIs are also gathering momentum, aided by improved blood-brain barrier penetration technologies and novel mechanisms for neurodegenerative diseases. Both trends accentuate the market’s tilt toward low-volume, high-value molecules that demand precise process control, reinforcing broader shifts already evident across the active pharmaceutical ingredients market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America retained a 41% revenue share in 2024 on the back of a robust R&D ecosystem, premium pricing, and supportive intellectual-property frameworks. Washington’s May 2025 executive order to streamline facility approvals is expected to accelerate domestic capacity additions, with Eli Lilly allocating USD 5.3 billion to a new Indiana API complex [2] Eli Lilly & Co., “Lilly to Invest USD 5.3 Billion in Indiana Facilities,” lilly.com

. These developments aim to mitigate concentration risk by re-establishing local production for critical medicines.

Asia-Pacific represents the strongest growth engine, posting a projected 7.70% CAGR through 2030. India and China file 82% of FDA DMFs, anchoring their dominance in cost-sensitive segments. Beijing’s sizeable antibiotic and analgesic output underscores substantial scale advantages, while India’s Production Linked Incentive scheme is funding greenfield units for fermentation and complex synthesis. Fast-growing biologic and HPAPI pipelines are further attracting multinational partnerships, cementing Asia’s central role in the active pharmaceutical ingredients market.

Europe maintains a notable position in complex, high-value APIs owing to stringent quality standards and deep scientific talent. Although its global share is edging downward, the region continues to lead in continuous manufacturing, green chemistry, and potency containment. European firms are differentiating with expertise in controlled substances and low-volume biologics, fostering resilient niches within the broader active pharmaceutical ingredients market.

Competitive Landscape

The market exhibits a dual-structure: innovative APIs reside within moderately concentrated captive networks owned by large pharmaceutical companies, while generic APIs remain highly fragmented. Cost-advantaged producers in India and China dominate commoditised molecules, fuelling price-based rivalry. In response, incumbents such as Teva and Pfizer are divesting non-core units and funnelling resources toward complex, higher-margin substances.

Technological differentiation is becoming decisive. Early adopters of continuous flow, advanced analytics, and green-solvent systems are securing supply agreements with innovators seeking robust, environmentally conscious partners. EUROAPI’s acquisition of oligonucleotide specialist BianoGMP highlights strategic positioning at the interface of small and large molecule expertise, reflecting broader white-space opportunities in peptides and conjugated compounds.

Regulators are reinforcing these shifts. The FDA’s support for continuous manufacturing provides a compliance tail-wind for technology leaders while raising hurdles for firms reliant on traditional batch operations. Consolidation is thus expected to intensify, with companies that couple process innovation with regulatory excellence poised to capture disproportionate value within the active pharmaceutical ingredients market.

Active Pharmaceutical Ingredients (API) Industry Leaders

-

Teva Pharmaceutical Industries Ltd

-

Pfizer Inc.

-

Merck KGaA

-

BASF SE

-

Viatris, Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: • President Trump signed an executive order streamlining domestic drug-manufacturing approvals and tightening overseas inspections.

- April 2025: Eli Lilly announced a USD 5.3 billion investment to build new API facilities in Indiana.

- February 2025: Novo Nordisk expanded peptide-API capacity to meet surging demand for GLP-1 receptor agonists.

- January 2025: Cambrex completed a USD 30 million expansion of HPAPI suites in North Carolina.

Global Active Pharmaceutical Ingredients (API) Market Report Scope

As per the scope of the report, an active pharmaceutical ingredient (API) is a part of any drug that produces its effects. Some drugs, such as combination therapies, have multiple active ingredients to treat different symptoms or act in different ways.

The active pharmaceutical ingredients (API) market is segmented by business mode into captive API and merchant API, by synthesis type, the market is bifurcated into synthetic and biotech, based on the type of drug the market is segregatted into generic and branded, based on the application the market is classified into cardiology, pulmonology, oncology, ophthalmology, neurology, orthopedic, and other applications, and by geography the market is divided inot North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| By Business Model | Captive API | ||

| Merchant / Contract API | |||

| By Synthesis Type | Synthetic APIs | ||

| Biotech APIs | |||

| By Molecule Size | Small Molecule | ||

| Large Molecule / Biologics | |||

| By Potency | High-Potency APIs | ||

| Low-/Medium-Potency APIs | |||

| By Therapeutic Area | Oncology | ||

| Cardiovascular | |||

| Infectious Diseases | |||

| Metabolic Disorders | |||

| CNS & Neurology | |||

| Respiratory | |||

| Ophthalmology | |||

| Others | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

By Business Model

| Captive API |

| Merchant / Contract API |

By Synthesis Type

| Synthetic APIs |

| Biotech APIs |

By Molecule Size

| Small Molecule |

| Large Molecule / Biologics |

By Potency

| High-Potency APIs |

| Low-/Medium-Potency APIs |

By Therapeutic Area

| Oncology |

| Cardiovascular |

| Infectious Diseases |

| Metabolic Disorders |

| CNS & Neurology |

| Respiratory |

| Ophthalmology |

| Others |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the active pharmaceutical ingredients market by 2030?

The market is forecast to reach USD 328.94 billion by 2030.

Which region is expected to grow the fastest in the active pharmaceutical ingredients market?

Asia-Pacific is projected to grow at a 7.70% CAGR through 2030, making it the fastest-expanding region.

Why are high-potency APIs gaining importance?

HPAPIs enable targeted therapies, especially in oncology, delivering strong efficacy at low doses and driving a forecast 12.50% CAGR for the segment.

How is continuous manufacturing influencing API production?

Continuous flow processes enhance yield, cut solvent use, and align with FDA quality initiatives, offering a cost and compliance edge to early adopters.

What drives the growing reliance on CDMOs?

Outsourcing to CDMOs allows pharmaceutical firms to reduce capital expenditure, access specialised expertise, and bring products to market faster, underpinning an 8.07% CAGR for merchant APIs.

Which therapeutic area will post the highest API growth?

Oncology leads with an 8.16% CAGR owing to rapid advances in precision medicine and immunotherapies.

Page last updated on: June 11, 2025