Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

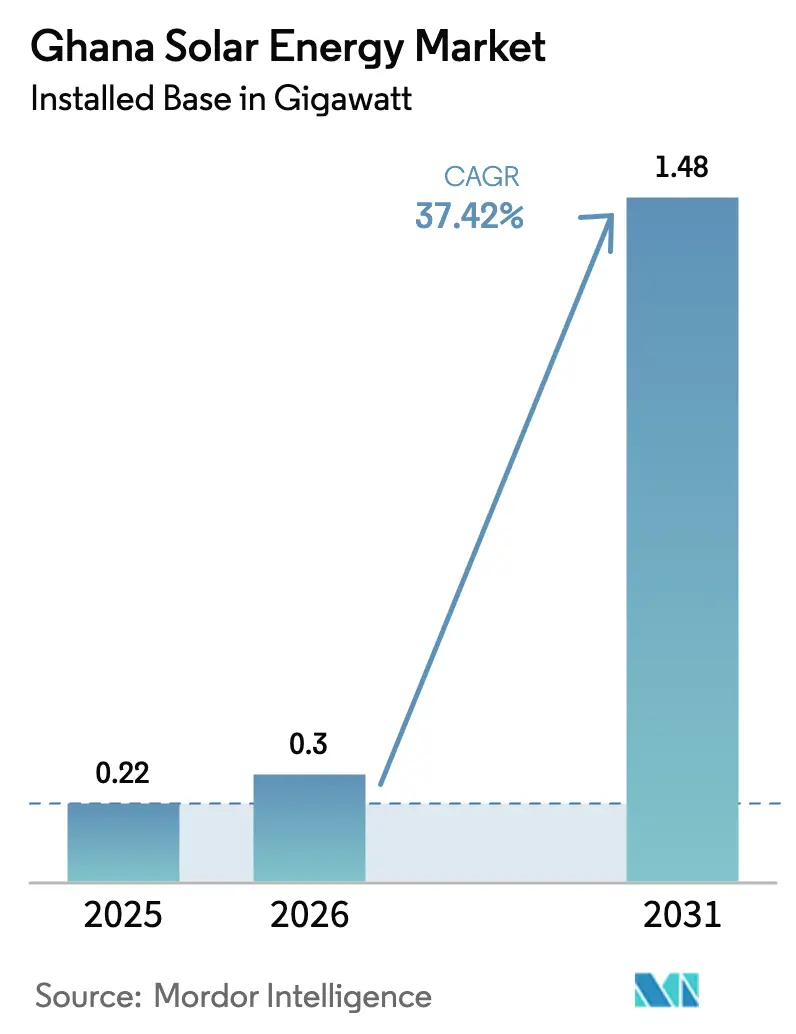

| Base Year Market Size (2025) | 0.22 gigawatt |

| Market Volume (2026) | 0.3 gigawatt |

| Market Volume (2031) | 1.48 gigawatt |

| Growth Rate (2026 - 2031) | 37.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ghana Solar Energy Market Analysis by Mordor Intelligence

Ghana Solar Energy Market size in 2026 is estimated at 0.3 gigawatt, growing from 2025 value of 0.22 gigawatt with 2031 projections showing 1.48 gigawatt, growing at 37.42% CAGR over 2026-2031.

Falling photovoltaic (PV) module prices, a four-year government target to add 2 GW of new solar capacity, and expanded access to concessional finance have collectively pushed solar levelized costs below thermal alternatives even without subsidies.(1)International Finance Corporation, “Dawa Solar Project Disclosure,” ifc.orgUtility-scale developers benefit from duty and value-added-tax waivers on imported equipment, while commercial-industrial (C&I) customers are accelerating adoption to hedge against frequent grid outages and rising tariffs. Off-grid solutions, mini-grids, and solar-home systems are advancing fastest as rural electrification agencies target the remaining 11% of households without grid access. Execution risks, however, persist around grid-absorption limits, cedi depreciation, and a moratorium on new power-purchase agreements that favors well-capitalized sponsors with development-finance-institution backing.

Key Report Takeaways

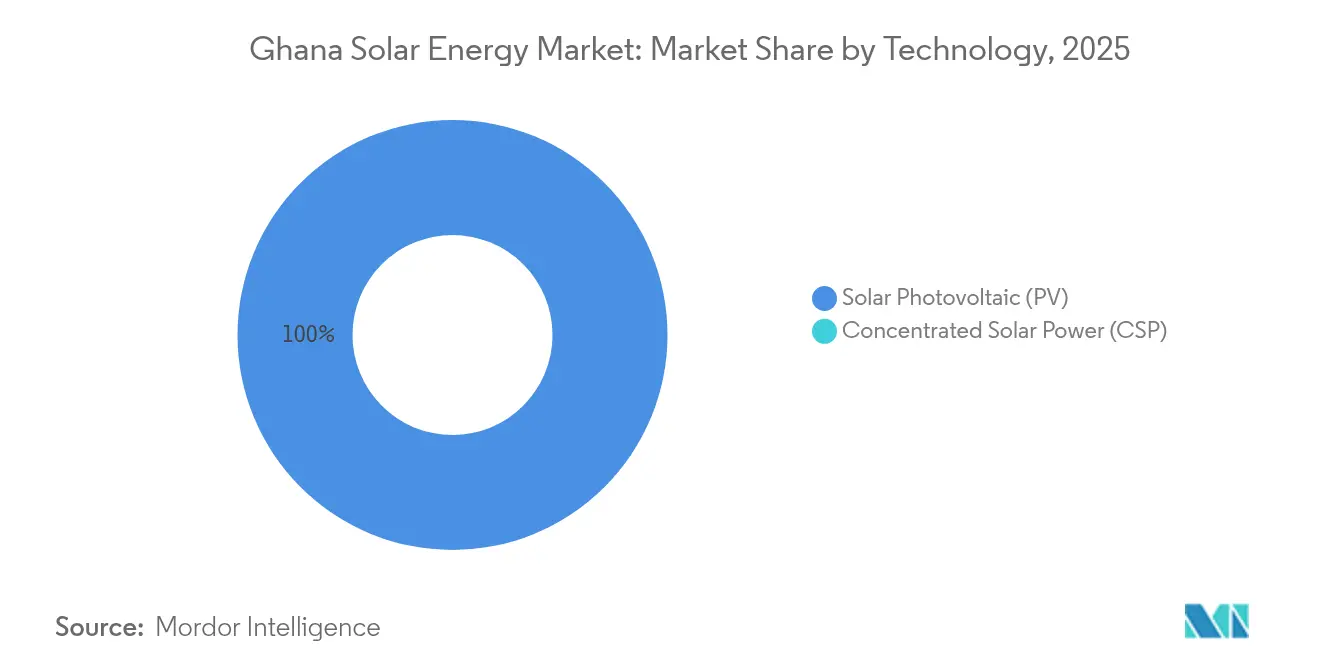

- By technology, solar photovoltaic commanded 100.00% of the Ghana solar energy market share in 2025, and the segment is projected to sustain a 37.42% CAGR through 2031.

- By grid type, on-grid installations captured 72.10% of the Ghana solar energy market share in 2025, while off-grid systems are poised to grow at a 39.85% CAGR to 2031.

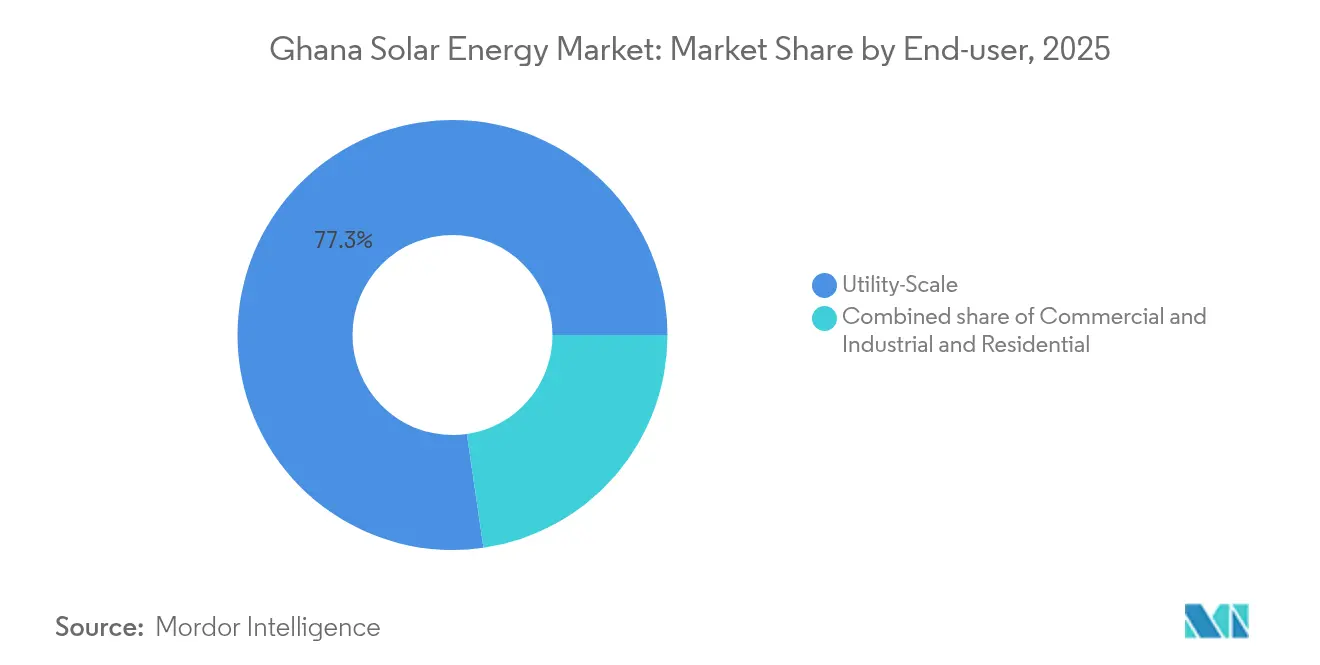

- By end-user, utility-scale plants accounted for 77.30% of the Ghana solar energy market size in 2025, whereas commercial-industrial arrays are advancing at a 39.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Ghana Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling PV module prices and tax exemptions | +12.50% | National, with concentration in Greater Accra, Ashanti, and Northern regions | Short term (≤ 2 years) |

| Concessional financing from World Bank and IFC | +10.80% | National, prioritizing utility-scale projects in Bono East and Upper West | Medium term (2-4 years) |

| Rural electrification through mini-grids and solar home systems | +8.20% | Northern, Upper East, Upper West, and Volta Lake communities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Falling PV Module Prices and Tax Exemptions

Global factory-gate module prices dropped to USD 0.10–0.12 per watt in 2024, down 60% from 2022 as Chinese oversupply hit export channels. Ghana’s Exemptions Act 2022 (Act 1083) keeps import duties at 0%–5%, cutting landed system costs 15%–20% compared with pre-2022 levels.(2)Ghana Revenue Authority, “Exemptions Act 2022,” gra.gov.ghLower capex has reduced payback periods for C&I rooftop arrays in Tema and Kumasi from seven to under five years. More than 100 IEC-aligned PV standards adopted by the Ghana Standards Authority in 2024 have shortened lender due diligence cycles, improving bankability. The upside is partially offset by a 14% year-to-date slide in the cedi that inflates local-currency equipment costs and highlights the importance of hedging and local-content strategies.

Concessional Financing from World Bank and IFC

Development-finance institutions committed over USD 400 million to Ghanaian solar deals between 2024 and early 2025, including a USD 130 million IFC facility for the 200 MW Dawa Solar Park and a USD 250 million World Bank energy-sector efficiency loan that bundles transmission upgrades. Interest rates are 300–500 basis points below domestic benchmarks of 28%–32%, lifting internal rates of return for utility-scale projects. AfDB’s USD 85 million Scaling-up Renewable Energy Program is underwriting 35 mini-grids and 12,000 net-metered systems, while AFD’s SUNREF Ghana line channels subordinated debt through local banks to broaden SME access. The Green Climate Fund injected USD 16.2 million into Ecobank’s Affirmative Solar Action Program for 10 MW of distributed installations on public facilities.(3)Green Climate Fund, “Affirmative Solar Action Program,” greenclimate.fund

Rural Electrification Through Mini-Grids and Solar-Home Systems

The 2025 national plan targets 35 solar mini-grids and 381 solar-powered public facilities to lift electrification from 89.03% to 90%. Mini-grid levelized costs have fallen to USD 0.38 per kWh, versus diesel costs of USD 0.55 per kWh in remote communities. Pay-as-you-go providers such as PEG Africa use mobile-money platforms and remote-shutoff functionality to reduce default risk and securitize receivables. AfDB financing covers 12,000 stand-alone systems, reflecting a hybrid rural strategy that pairs grid extension, mini-grids, and solar-home systems for capital efficiency. Persistent land-acquisition delays and the absence of a cost-reflective feed-in tariff still constrain private-sector participation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid congestion and limited transmission capacity | -5.30% | National, acute in Greater Accra and Ashanti regions | Medium term (2-4 years) |

| Cedi depreciation raising import costs | -4.10% | National, affecting all project developers | Short term (≤ 2 years) |

| Slow net-metering rollout | -3.20% | National, concentrated in urban and peri-urban distribution zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Congestion and Limited Transmission Capacity

Electricity Company of Ghana (ECG) distribution losses stood at 30% in 2024, reflecting aging assets, theft, and undersized transformers. Transmission constraints in Ashanti and Northern regions force developers to cluster near coastal substations, elevating curtailment risk during off-peak demand. A 2024 moratorium on new power-purchase agreements, imposed to address USD 1.6 billion in payables, has frozen much of the utility-scale pipeline. Although the World Bank has allocated USD 80 million for grid upgrades, procurement delays may push commissioning into 2027. Net-metering rules adopted in 2023 allow export up to 1 MW, yet fewer than 500 systems had been certified by end-2024 owing to ECG’s limited metering capacity.

Cedi Depreciation Raising Import Costs

The cedi lost 14% against the U.S. dollar in the first 11 months of 2024 after a 20.6% slide in 2023, lifting interbank rates from GHS 11.97 to GHS 13.90 per USD.(4)Bank of Ghana, “Interbank FX Rates,” bog.gov.gh Solar projects import up to 80% of their hardware, exposing them to exchange-rate swings that can erode 5%–10% of modeled returns when hedging tools are unavailable or costly. The IMF’s Extended Credit Facility caps non-concessional borrowing, reducing fiscal buffers that could otherwise backstop currency risk. Domestic loans priced at 28%–32% are uneconomic for 20-year solar assets, pushing developers toward dollar-denominated debt. Depreciation also inflates O&M outlays for inverter spares and tracker parts, underscoring the value of local assembly partnerships.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Photovoltaic Dominance Unchallenged

Solar PV retained 100.00% share of the Ghana solar energy market in 2025 and is projected to grow at a 37.42% CAGR to 2031. Crystalline-silicon modules, mainly monocrystalline PERC and TOPCon, accounted for more than 85% of procurement tenders, reflecting developer focus on higher efficiency and reduced land footprint. Concentrated Solar Power remains absent because Ghana’s direct-normal irradiance averages 4.5–5.5 kWh/m²/day, below the 6.0 threshold needed to justify tower or trough plants WORLDBANK.ORG. Bifacial modules, deployed at the Dawa Solar Park, raise yields 10%–15% but carry a 15%–20% price premium. Thin-film accounts for less than 5% of shipments, confined to building-integrated façades where aesthetics outweigh output.

Inverters show a split between string units for C&I rooftops and central units for utility-scale fields. Hybrid inverters with battery-management systems are gaining traction in off-grid and mini-grid schemes. Single-axis trackers can add 15%–20% energy but cost 25%–30% more than fixed-tilt racking, limiting adoption to large projects. Legislative Instrument 2449 sets minimum module efficiencies at 16% for monocrystalline and 15% for polycrystalline panels, filtering out sub-standard imports and aligning local installations with global Tier-1 quality benchmarks.

By Grid Type: Off-Grid Acceleration Outpaces On-Grid Base

On-grid installations controlled 72.10% of the Ghana solar energy market share in 2025, led by PPAs with ECG and captive C&I arrays that export surplus under net-metering guidelines. Off-grid capacity, however, is growing at a 39.85% CAGR on the back of mini-grids around Volta Lake and PAYG solar-home systems in the Northern belt. The AfDB-funded 35 mini-grids supply 24-hour electricity at USD 0.38 per kWh, cutting diesel costs nearly in half. PAYG providers peg daily repayments to mobile-money micro-transactions that align with rural income flows and reduce collection risk.

On-grid expansion is hampered by ECG’s losses and the PPA freeze. Net-metered exports remain limited because ECG lacks bidirectional meters and automated billing. Off-grid developers confront tariff-setting uncertainty, but hybrid mini-grids that mix solar, batteries, and diesel offer a balanced cost-reliability profile. The 2025 target for 35 new mini-grids and 381 solar-equipped public facilities marks a policy pivot to decentralized electrification, contingent on faster environmental permitting and land-lease approvals.

By End-User: Commercial-Industrial Surge Reshapes Demand

Utility-scale plants held 77.30% of installed capacity in 2025, anchored by Bui Power Authority’s 45 MW hybrid project and the 200 MW Dawa Solar Park. Yet C&I systems are expanding at 39.24% CAGR as mines, telecom towers, and food processors install behind-the-meter arrays to counter tariff inflation and brownouts. AngloGold Ashanti and Newmont plan 20% renewable penetration at Ghanaian mines by 2027, while MTN and Vodafone are retrofitting 3,000 cell towers with solar-battery hybrids. Daystar Power’s Solar-as-a-Service model has signed 27 MW of C&I contracts, proving that third-party ownership can unlock demand where balance-sheet constraints exist.

Residential uptake remains below 5% of capacity, constrained by high upfront costs and slow net-meter rollout. Utility-scale PPAs deliver USD 0.04–0.06 per kWh but carry off-taker risk due to ECG’s payables backlog. C&I payback periods of four to six years are acceptable because they eliminate diesel fuel at USD 0.30 per kWh. Africa’s largest rooftop array, a 10 MW system on a Tema logistics warehouse, illustrates how large roofs can bypass land scarcity. Residential growth should gain momentum post-2027 once consumer-finance products mature.

Geography Analysis

Greater Accra, Ashanti, and Bono East host roughly two-thirds of Ghana’s solar megawatts because they combine irradiance above 5 kWh/m²/day with proximity to load centers and substations. Greater Accra leads the Ghana solar energy market with the 200 MW Dawa Solar Park and C&I rooftops in the Tema industrial zone, where tariffs near GHS 1.20 per kWh (USD 0.09) make solar cost-competitive. Bono East is emerging as a floating-solar hub on the 400 km² Bui Reservoir, where Bui Power Authority plans to scale from 5 MW to 65 MW by 2027. Northern, Upper East, and Upper West regions, where grid access lags at 60%–70%, are earmarked for mini-grids under the 2025 rural-electrification plan.

Volta Lake islands benefit from AfDB-funded hybrids that replace gensets costing USD 0.55 per kWh. Coastal regions enjoy strong irradiance and existing transmission but face land constraints, steering developers toward rooftops and carports. Ashanti’s mining and light-manufacturing clusters drive C&I demand that offsets ECG outages. Participation in the West African Power Pool is currently limited to hydro and thermal exports, though future interconnector upgrades could facilitate renewable trading. Universal access will need an additional 500 MW of distributed solar by 2030, concentrated in the northern belt. The Renewable Energy Master Plan allocates 447.5 MW to utility-scale, 200 MW to distributed generation, and 20 MW to stand-alone systems across all 16 regions, favoring solar where it can displace diesel or defer costly grid extension.

Competitive Landscape

The Ghana solar energy market is moderately fragmented; no single firm controls more than 15% of installed capacity. State-owned Bui Power Authority leads utility-scale builds by leveraging sovereign guarantees and concessional finance, commissioning 45 MW in 2024 and planning 65 MW of floating PV by 2027. Tier-1 module suppliers Trina Solar, JinkoSolar, and REC Solar capture 80%–85% of tenders by meeting efficiency and safety rules under Legislative Instrument 2449. Local engineering-procurement-construction specialists such as Meinergy Ghana and SunPower Innovations partner with international OEMs to comply with rising local-content quotas.

Growth white spaces include: C&I PPAs for mines and telecom firms seeking tariff hedges, PAYG solar-home systems in northern districts, and hybrid mini-grids on Volta Lake islands. Daystar Power’s zero-capex model demonstrates the viability of third-party ownership for SMEs, while PEG Africa leverages mobile-money integration to scale PAYG portfolios. Technology differentiation around bifacial modules, trackers, and hybrid inverters remains capital-constrained because the market lacks performance-based incentives that reward higher yields.

Ghana Solar Energy Industry Leaders

Trina Solar Ltd

JinkoSolar Holdings Co. Ltd

SunPower Innovations

Translight Solar

Redavia Solar Power

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Bui Power Authority inaugurated a 45 MW hybrid solar plant at the Bui Generating Station, including Africa’s largest operational floating array.

- October 2024: Bui Power Authority commissioned the first 30 MW of the 50 MW Yendi project, backed by AfDB concessional debt.

- July 2024: IFC approved a USD 130 million loan to LMI Holdings for the 200 MW Dawa Solar Park. IFC's support includes direct loans and blended finance, helping LMI build West Africa's largest private solar plant to power industry, with phases targeting 2026/2027 completion, aiming for large-scale industrial clean energy.

- June 2024: In a significant move for West Africa's renewable energy landscape, Ghana's Bui Power Authority (BPA) has activated a pioneering 5 MW floating solar photovoltaic (FSPV) array on the Bui reservoir. This innovative project, seamlessly integrated with hydro power, enhances efficiency through water cooling, conserves land, and serves as a testbed for a more ambitious 250 MW initiative, underscoring Ghana's commitment to renewable energy advancement.

Ghana Solar Energy Market Report Scope

Solar power means using the sun's energy to produce electricity, either directly as thermal energy (heat) or indirectly through photovoltaic cells in solar panels and clear photovoltaic glass.

The Ghana solar energy market is segmented by technology, grid type, end-user, and component type. By technology, the market is segmented into solar photovoltaic (PV) and concentrated solar power (CSP). By grid type, the market is segmented into on-grid and off-grid. By end-user, the market is segmented into utility-scale, commercial and industrial, and residential. By component, the market is segmented into solar modules, inverters, mounting and tracking systems, balance-of-system and electricals, energy storage, and hybrid integration.

The report also covers the market size and forecasts for the Ghana solar energy market. For each segment, market sizing and forecasts have been done based on installed capacity.

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration |

Key Questions Answered in the Report

What was the installed solar capacity in Ghana at the end of 2026?

The Ghana solar energy market size reached 300 MW in 2026.

How fast is Ghana’s solar capacity expected to grow between 2026 and 2031?

Total capacity is projected to expand at a 37.42% CAGR, reaching 1,480 MW by 2031.

Which solar segment is growing fastest by end-user?

Commercial-industrial systems lead growth at a 39.24% CAGR as mines, telecom towers, and factories adopt behind-the-meter arrays.

What share of Ghana’s 2025 solar capacity came from on-grid projects?

On-grid plants accounted for 72.10% of installed capacity in 2025.

Why are mini-grids attractive for rural Ghana?

Hybrid solar mini-grids deliver electricity at USD 0.38 per kWh, undercutting diesel gensets by up to 50%, while supporting the government’s plan to close the rural access gap.

Which policy offers the biggest cost relief for solar imports?

The Exemptions Act 2022 waives duties and VAT on PV equipment, trimming landed costs by 15%–20%.

Page last updated on: