Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 14.25 Billion |

| Market Size (2026) | USD 14.84 Billion |

| Market Size (2031) | USD 18.19 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Telecom MNO Market Analysis by Mordor Intelligence

The Germany Telecom MNO Market size was valued at USD 14.25 billion in 2025 and estimated to grow from USD 14.84 billion in 2026 to reach USD 18.19 billion by 2031, at a CAGR of 4.15% during the forecast period (2026-2031).

Network-modernization investments approaching EUR 50 billion through 2030, the federal Gigabit Strategy, and swift 5G standalone roll-outs are sustaining momentum even as economic growth moderates. Operators are prioritizing fiber-to-the-home coverage, fixed–mobile convergence bundles, and AI-enabled network automation to strengthen average revenue per user (ARPU) and cut operating costs. Enterprise digitalization, particularly in manufacturing and automotive clusters, is accelerating premium connectivity demand, while consumer data traffic keeps climbing on the back of streaming. Regulatory pressure, including stringent energy-efficiency rules and spectrum-coverage obligations, is reshaping capital-allocation priorities and nudging smaller players toward partnership or exit.

Key Report Takeaways

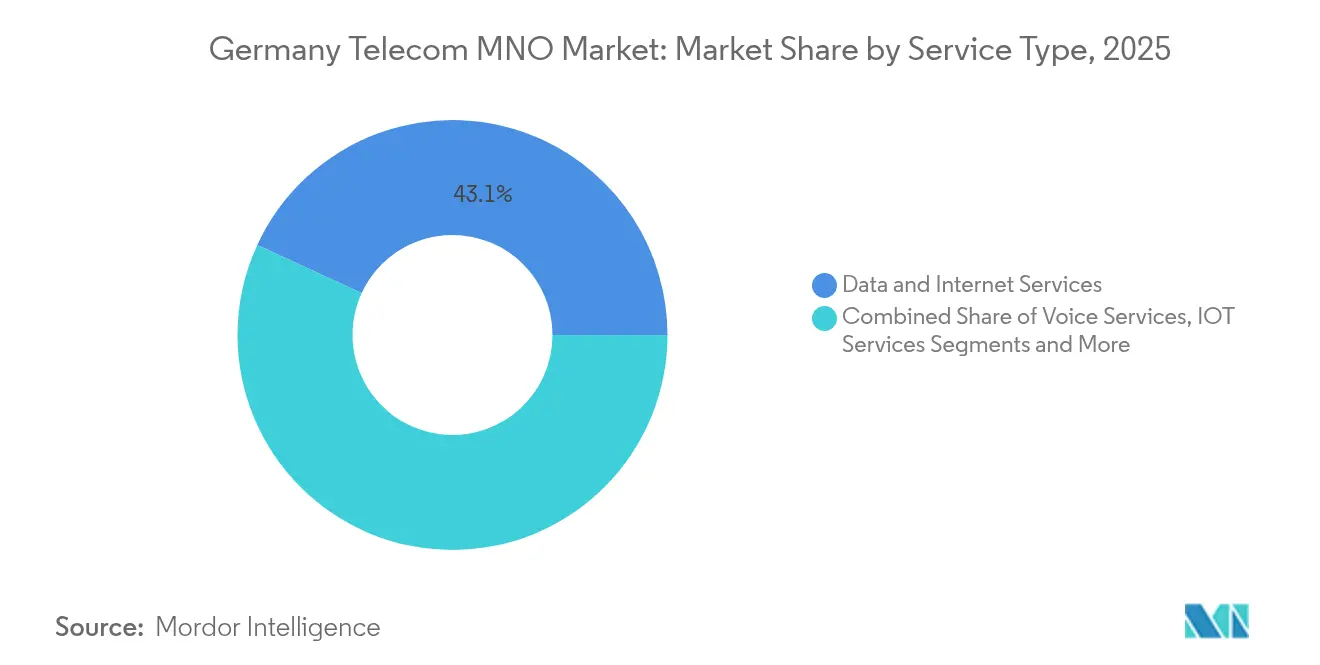

- By service type, Data and Internet Services captured 43.12% of German telecom market share in 2025.

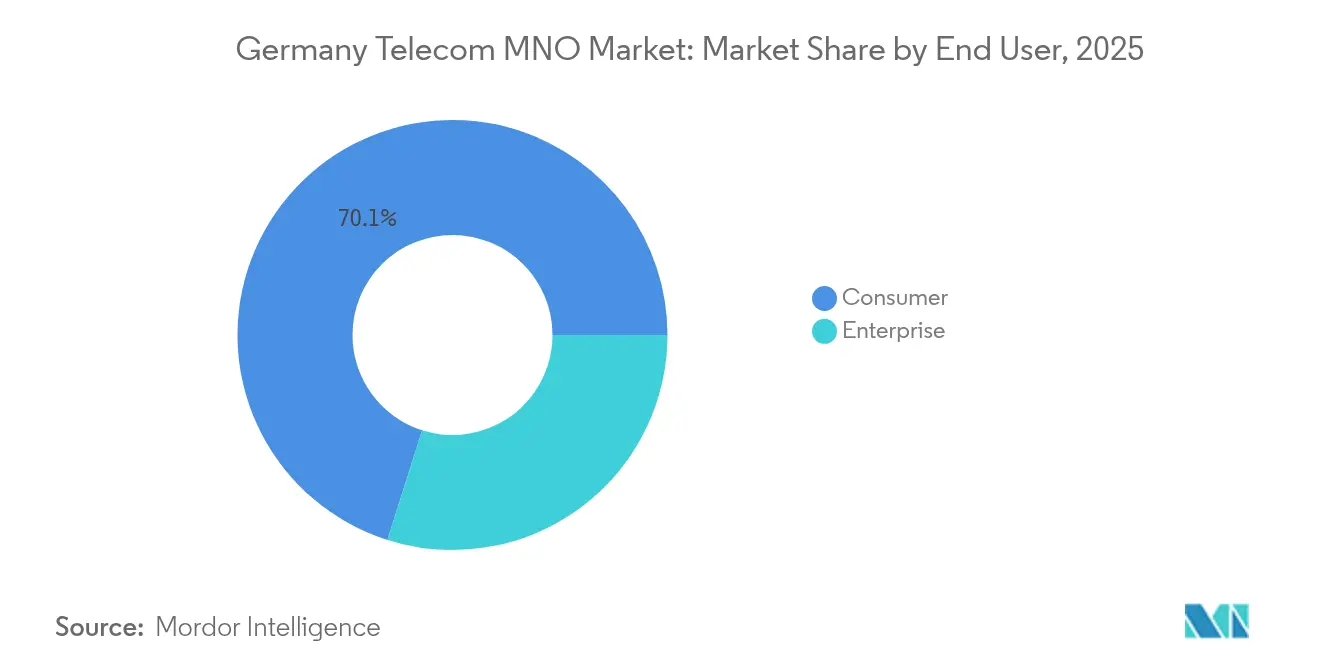

- By end-user, enterprise services are projected to grow at a 4.62% CAGR between 2025 and 2031, outpacing consumer growth.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging FTTH build-out and government gigabit targets | +1.2% | National, early urban gains | Medium term (2-4 years) |

| Rapid 5G standalone roll-outs powering eMBB demand | +0.9% | National, industrial regions | Short term (≤ 2 years) |

| Enterprise digitalization and campus-network uptake | +0.7% | Manufacturing hubs nationwide | Medium term (2-4 years) |

| Fixed–mobile convergence bundles boosting ARPU | +0.5% | National | Short term (≤ 2 years) |

| AI-based network automation cutting OPEX | +0.4% | National | Long term (≥ 4 years) |

| Rising spectrum-sharing and neutral-host models | +0.3% | Industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging FTTH Build-out and Government Gigabit Targets

Germany’s Gigabit Strategy requires 50% of premises to be fiber-connected by 2025 and near-universal coverage by 2030, spurring aggressive capital programs.[1]Federal Ministry for Digital and Transport, “Gigabit Strategy of the Federal Government,” bmvi.de EUR 3 billion in federal Gigabitförderung 2.0 subsidies accelerates builds in underserved districts, while Deutsche Telekom aims for 10 million additional fiber lines by 2030 and Vodafone leverages Unitymedia assets to pass 25 million homes. Operators with deeper fiber footprints command higher ARPU through multi-play bundles and premium enterprise links. Early deployments create temporary market fragmentation favoring fiber-rich localities, yet nationwide roll-out remains a prerequisite for long-term competitiveness. Successful execution directly lifts German telecom market revenue trajectories by expanding capacity for data-heavy services.

Rapid 5G SA Roll-outs Powering eMBB Demand

All three national carriers met initial 99% coverage targets by 2024, and Deutsche Telekom plans 99% population reach in 2025.[2]Light Reading, “Germany achieves 100 Mbit/s everywhere all the time,” lightreading.com Standalone architecture unlocks low-latency network slicing crucial for manufacturing and automotive campuses at BMW, Mercedes-Benz, and Volkswagen sites. Consumers are also driving revenue uplift as mobile data usage rose 30-34% year-over-year across operators, monetized via larger allowances and unlimited plans. Operators gain efficiency from retiring legacy cores and converging frequency layers, which lowers per-gigabyte costs while improving user experience. Early 5G SA adopters therefore secure durable competitive advantages and stimulate incremental German telecom market growth.

Enterprise Digitalization and Campus-Network Uptake

The industrial IoT economy doubled to EUR 16.8 billion between 2017 and 2022, with automotive IoT expanding more than 20% annually as factories embed sensor networks and connected-car platforms. Private 5G campus solutions offer guaranteed throughput and security, letting operators charge premium fees. Vodafone earmarked EUR 250 million for B2B cloud telephony and unified communications, while Deutsche Telekom’s campus networks at BMW, Mercedes-Benz, and Tesla illustrate willingness to pay for mission-critical connectivity. Small and midsize enterprises are also shifting toward cloud-based collaboration, though price sensitivity caps premium uptake. Nonetheless, enterprise contracts underpin higher-margin segments and reinforce the German telecom market’s enterprise-led expansion trajectory.

Fixed–Mobile Convergence Bundles Boosting ARPU

Bundled offers integrating broadband, mobile, and entertainment are central to churn reduction. The July 2024 law abolishing landlord-collected cable fees compelled providers to compete directly for 12 million households, intensifying the need for sticky convergent propositions. Deutsche Telekom, O2, Vodafone, and Sky now promote discount structures and unified billing that elevate household ARPU and lower acquisition costs. Cross-selling opportunities arise as subscribers migrate from single-service to triple-or quad-play bundles, mitigating price pressure in standalone segments. The strategy’s success, however, hinges on seamless service integration and transparent pricing perceived as valuable by price-conscious consumers.

Restraints Impact Analysis*

| Restraint | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MDU cable-TV law slashing fixed revenue | −0.8% | Urban rental markets | Short term (≤ 2 years) |

| Stringent energy-efficiency rules raising capex | −0.4% | National | Medium term (2-4 years) |

| High fiber & 5G capex burden on challengers | −0.3% | National, smaller operators | Medium term (2-4 years) |

| OTT voice migration eroding legacy revenues | −0.2% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

MDU Cable-TV Law Slashing Fixed Revenue

The July 2024 repeal of the Nebenkostenprivileg removed automatic inclusion of cable TV in rental bills, exposing Vodafone’s MDU subscriber base to direct competition and slashing the cohort from 8.5 million to 4 million accounts.[3]Telecoms, “Germany Takes the Shine off Vodafone’s Otherwise Solid First Half,” telecoms.com An estimated EUR 800 million in annual revenue is at risk sector-wide, with Tele Columbus losing 40% of TV customers in mere months. Streaming platforms such as Netflix, Amazon Prime, Waipu, and Zattoo now vie for the same households without bearing network costs, intensifying price pressure. Operators must reposition TV within convergent bundles to defend share, yet short-term churn spikes and EBITDA compression remain likely.

Stringent Energy-Efficiency Rules Raising Capex

European sustainability directives mandate measurable reductions in network power consumption, compelling operators to invest in renewable sourcing, liquid-cooling radio units, and advanced energy-management software. These outlays push per-site 5G deployment costs higher just as competitive intensity rises, squeezing free cash flow. Smaller carriers lack the scale economics to spread environmental-compliance spend, nudging them toward infrastructure-sharing or consolidation. While green credentials can enhance brand appeal, the near-term capital burden restrains German telecom market expansion capacity by diverting funds from revenue-generating projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Lead Market Evolution

Data and Internet Services delivered USD 6.15 billion in 2025, 43.12% of the German telecom market share, and are CAGR-forecast at 4.33% through 2031 on buoyant video streaming and enterprise cloud connectivity. Operators documented mobile data surges-Vodafone 34% to 1.8 billion GB, Deutsche Telekom 30% to 2.4 billion GB, and O2 beyond 3 billion GB-while fixed consumption surpassed 121 billion GB with average household loads of 275 GB monthly. 5G standalone and fiber upgrades underpin differentiated service tiers that fetch premium pricing from industrial users seeking network-slice guarantees. Consequently, German telecom market size gains at the segment level will continue to eclipse legacy categories.

Voice Services still produced USD 3.91 billion (27.45% share) in 2025, but OTT migration and planned 2G shutdowns by 2028 portend gradual contraction. Telefónica Deutschland already routes 80% of calls via VoLTE, and both Deutsche Telekom and Vodafone are reallocating spectrum to 5G. IoT and M2M Services, worth USD 1.36 billion in 2025, exhibit the fastest 4.45% CAGR, reflecting Germany’s leadership in connected-factory and automotive telematics. Pay-TV and other value-added services face direct streaming competition, yet roaming and wholesale traffic are recovering alongside international travel. As data-centric products outpace voice, overall portfolio mix shifts toward higher-growth, margin-accretive categories.

By End-user: Enterprise Segment Drives Premium Growth

Enterprise accounts generated USD 4.26 billion in 2025, equivalent to 29.90% of the German telecom market, and are set to widen to USD 5.59 billion by 2031 at a 4.62% CAGR. Private 5G networks and industrial IoT projects in automotive and machinery verticals confer pricing power because latency guarantees and security assurances are mission critical. The German telecom market size for campus-network contracts is enlarging as manufacturers digitize production lines and autonomous-vehicle testing zones. Vodafone’s EUR 250 million B2B fund and Deutsche Telekom’s multi-plant deals highlight operator focus on value-rich accounts that dampen volatility. Aggressive cloud-telephony uptake among SMEs adds incremental layers, though average revenue per line remains below large-enterprise benchmarks.

Consumer services retained USD 9.99 billion in 2025, 70.10% of the German telecom market. Data traffic climbed 30-34% year-over-year across major networks, yet intense price rivalry tempered ARPU lift. Regulatory changes, including the cable-TV billing shift, eroded legacy fixed revenue streams, forcing providers to cross-sell mobile and entertainment bundles. Future growth depends on widespread adoption of fixed–mobile convergence, premium 5G data plans, and differentiated content partnerships. While overall consumer uptake underpins volume, margin recovery will rely on disciplined pricing and loyalty-driven initiatives that limit churn.

Competitive Landscape

Germany’s nationwide regulatory framework drives homogeneous baseline coverage, yet regional disparities in fiber density and industrial concentration create revenue pockets. Southern states such as Bavaria and Baden-Württemberg host dense automotive and machinery clusters where enterprise campus-network demand is strongest, supporting above-average ARPU for Deutsche Telekom and O2. Northern federal states lag in FTTH penetration, steering operators to prioritize subsidy-backed rural builds that bolster long-term German telecom market size expansion while tempering near-term margins. Urban centers like Berlin, Hamburg, and Munich already record gigabit-class fixed availability above 80%, enabling early 5G SA monetization through bundled plans and premium entertainment.

Rural broadband gaps are narrowing as the Gigabitförderung 2.0 program subsidizes unserved communities. Open-access fiber builders partner with incumbent operators under wholesale-only models, widening reach without duplicating investment. While subsidy frameworks reduce capital intensity, execution complexity lengthens deployment timelines, requiring robust project-management capabilities. Consequently, regional roll-out speed influences competitive dynamics: first movers can lock in high-value residential contracts, whereas laggards face price compression.

Cross-border traffic with Austria, the Netherlands, and Poland is rising as roaming returns to pre-pandemic levels, lifting wholesale revenues. Edge-data-center initiatives around Frankfurt’s internet hubs accelerate low-latency application adoption, reinforcing Germany’s role as continental connectivity nexus. Yet energy-cost differentials across Länder influence siting of network infrastructure, with renewable-rich locales attracting new deployments. Aggregate geography-specific factors collectively steer investment sequencing, shaping overall German telecom market performance.

Germany Telecom MNO Industry Leaders

Deutsche Telekom AG

Vodafone GmbH

O2 Telefonica Germany GmbH & Co. OHG

1&1 AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Vodafone Germany introduced AI-enabled network-incident prediction, targeting 30% reduction in outages by year-end.

- May 2025: O2 Telefónica Deutschland finalized a 10-year renewable-energy PPA covering 100% of its base-station electricity demand.

- November 2024: Tele Columbus reported a 40% drop in TV subscribers following the law change.

- July 2024: Nebenkostenprivileg repeal took effect, ending landlord-collected cable TV fees for 12 million households.

Germany Telecom MNO Market Report Scope

The Germany telecom mno market is defined based on the revenues generated from the services used in various end-user applications across Germany. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting the growth of the market in terms of drivers and restraints.

The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study also tracks the revenue accrued from the various services used in various end-user industries across Germany. In addition, the study provides the Germany Telecom market trends, along with key vendor profiles.

The scope of the study has been segmented based on the Services (Voice Service (Wired and wireless), Data and Messaging Services, and OTT and PayTVServices) across Germany. Germany's Telecom Market is segmented by Services (Voice Services (Wired, Wireless), Data and Messaging Services, and OTT/Pay TV Services). The market sizes and forecasts are provided in terms of value in USD million for all the above segments.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Service Types (VAS, Roaming And International Services, Enterprise And Wholesale Services, etc.) |

End-user

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Service Types (VAS, Roaming And International Services, Enterprise And Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What impact did the 2024 cable-TV billing reform have?

The law cut automatic landlord billing for 12 million flats, halving Vodafone’s MDU TV base and putting roughly EUR 800 million of annual revenue at risk.

Why are enterprises critical for German operators?

Enterprises pay premium rates for private 5G and IoT connectivity, driving a 4.62% CAGR that outpaces the consumer segment.

How are operators managing 5G deployment costs?

Carriers are adopting tower carve-outs, network-sharing, and AI-based automation to balance capital intensity with efficiency gains.

What is the outlook for fiber investment?

Operators plan nearly EUR 50 billion in cumulative fiber upgrades through 2031 under the federal Gigabit Strategy, aiming for nationwide gigabit access.

Page last updated on: