Germany SLI Battery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.23 Billion |

| Market Size (2026) | USD 1.26 Billion |

| Market Size (2031) | USD 1.42 Billion |

| Growth Rate (2026 - 2031) | 2.42% CAGR |

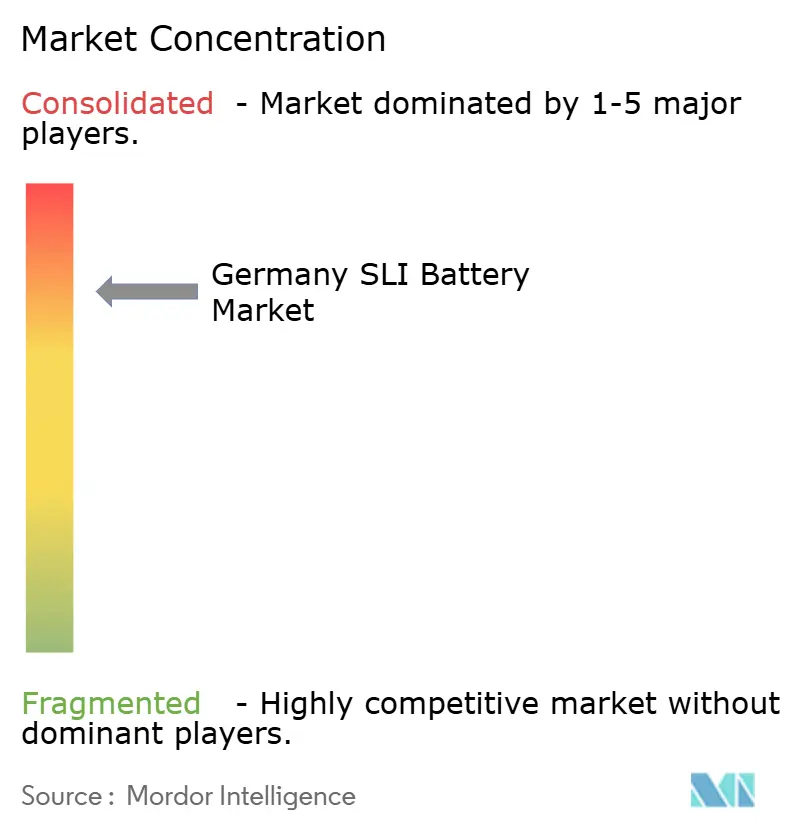

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany SLI Battery Market Analysis by Mordor Intelligence

Germany SLI Battery Market size in 2026 is estimated at USD 1.26 billion, growing from 2025 value of USD 1.23 billion with 2031 projections showing USD 1.42 billion, growing at 2.42% CAGR over 2026-2031.

This steady growth reflects a balancing act between an aging vehicle parc that prolongs replacement demand and the structural decline in new internal-combustion registrations. Catalysts include accelerating start-stop penetration, stricter CO₂ rules that still require 12-volt back-up batteries on 48 V mild hybrids, and persistent winter-related breakdowns that push fleets toward premium chemistries. Technology shifts toward Absorbent Glass Mat (AGM) lines, predictive-maintenance platforms, and recycled-content mandates further influence procurement strategies, while lithium-ion auxiliary batteries in premium electric vehicles create longer-term substitution pressure. Competitive intensity remains moderate, anchored by Clarios, Exide Technologies, and Varta AG, but regional specialists and Asian entrants intensify pricing pressure, especially in conventional flooded tiers. Headline risks range from lead-price volatility and shrinking domestic smelting capacity to evolving EU sustainability regulations that tighten recycled-content thresholds.

Key Report Takeaways

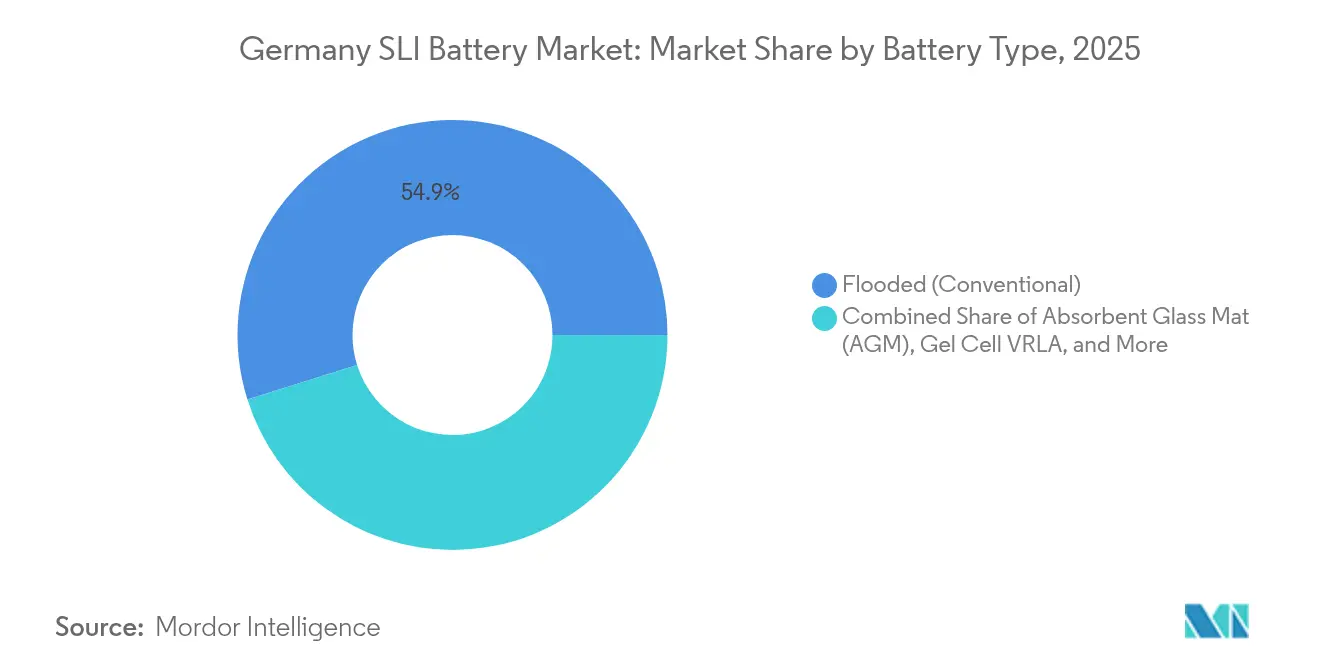

- By battery type, flooded conventional units led with 54.85% of Germany's SLI battery market share in 2025; AGM variants are forecast to expand at a 6.55% CAGR through 2031.

- By voltage, 12-volt batteries commanded 68.05% share of the German SLI battery market size in 2025, while above-60-volt segments are projected to register a 7.35% CAGR to 2031.

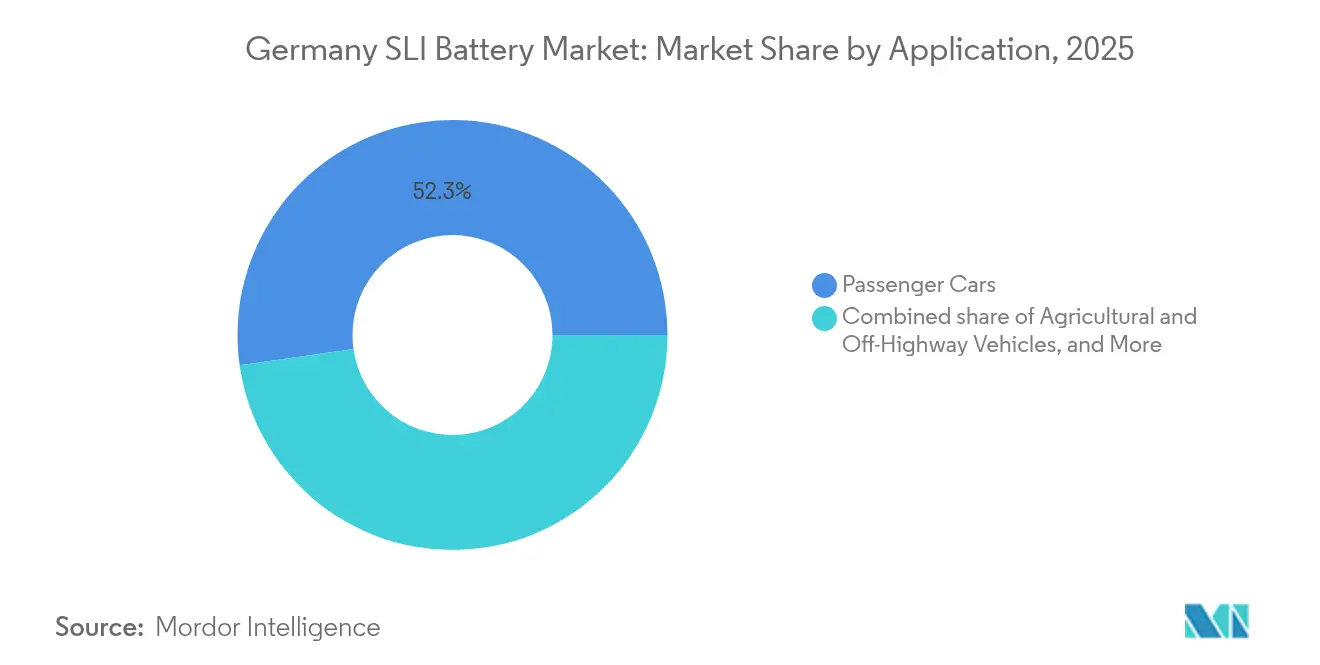

- By application, passenger cars accounted for 52.25% of the German SLI battery market size in 2025, and agricultural and off-highway vehicles are advancing at a 5.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

National developments in Germany connect differently with activity unfolding across other parts of the world. In the global sli battery market coverage, Mordor Intelligence integrates these into a single analytical framework.

Germany SLI Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging vehicle parc boosting replacement demand | +0.8% | Germany-wide, concentrated in rural and suburban regions | Long term (≥ 4 years) |

| Rapid OEM roll-out of start-stop (micro-hybrid) vehicles | +0.7% | Germany, with spillover to Central Europe | Medium term (2-4 years) |

| Severe winter cranking-power needs in Central Europe | +0.3% | Germany, Austria, Poland, Czech Republic | Short term (≤ 2 years) |

| 48V hybrid architectures still require 12V SLI back-up | +0.5% | Germany, with early adoption in premium OEM segments | Medium term (2-4 years) |

| Predictive-maintenance digital aftermarket platforms | +0.2% | Germany, pilot deployments in fleet and commercial segments | Long term (≥ 4 years) |

| EU 2023/1542 recycled-content mandate lifting domestic demand | +0.4% | Germany, broader EU compliance zone | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Vehicle Parc Boosting Replacement Demand

Germany’s passenger-car fleet reached 49.1 million units in January 2024, with an average age of 10.3 years, up from 9.8 years in 2020.[1]Kraftfahrt-Bundesamt, “Fahrzeugzulassungen Januar 2024,” kba.de Cars older than eight years often need at least one battery replacement, and the expanding 10-to-15-year cohort drives a stable aftermarket regardless of new-car volatility. Vehicle owners in rural and suburban areas extend lifecycles to 12–14 years, so flooded batteries cycle every four to five years, while AGM units last up to seven. Even though new registrations slipped 1% in 2024, the installed base grew, preserving distributor throughput.[2]Verband der Automobilindustrie, “Neuzulassungen 2024,” vda.de The trend also nudges customers toward Enhanced Flooded Battery or AGM upgrades to reduce repeat failures in retrofitted start-stop cars.

Rapid OEM Roll-Out of Start-Stop (Micro-Hybrid) Vehicles

Start-stop systems penetrated roughly 68% of the German parc by 2024, and more than 90% of new cars now ship with the feature as standard.[3]EUROBAT, “Start-Stop Battery Market 2024,” eurobat.org Europe produced 13 million start-stop batteries in 2024, with AGM holding 61% and Enhanced Flooded 39%, reflecting OEM preferences for cycle-life durability. Volkswagen, BMW, and Mercedes-Benz specify AGM for premium trims, creating bifurcated demand that favors converters equipped for dual-chemistry production. Clarios has earmarked EUR 200 million between 2022 and 2026 to add 50% AGM capacity, anticipating a 95% penetration plateau by 2028.

Severe Winter Cranking-Power Needs in Central Europe

Temperatures below −10 °C reduce lead-acid capacity by up to 40% and raise cranking demands more than 50%.[4]ADAC, “Pannenstatistik 2024,” adac.de Battery failure consistently tops roadside-assistance charts in winter, accounting for nearly 40% of call-outs. Distributors and fleets respond with pre-winter replacement campaigns that cluster sales in the fourth quarter. AGM batteries, offering around 20% higher cold-cranking performance at −18 °C, win favor among logistics operators despite a 15–25% price premium, and gel-cell VRLA solutions persist in standby applications where sub-zero reliability is non-negotiable.

48 V Hybrid Architectures Still Require 12 V SLI Back-Up

Volkswagen’s Passat mild hybrid debuted in May 2024, pairing a 48 V lithium-ion pack with a traditional 12 V AGM unit. Mercedes-Benz, BMW, and Audi have layered similar systems onto combustion platforms, and global 48 V vehicle production reached 9.3 million units in 2024, projected to 17.3 million by 2028, with Europe holding 47%. Every mild hybrid still specifies a 12 V backup to keep control units running if the 48 V net faults, anchoring incremental SLI demand even as electrification accelerates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing shift to Li-ion auxiliary batteries in new EVs | -0.5% | Germany, concentrated in premium BEV segments (BMW, Mercedes, Porsche) | Medium term (2-4 years) |

| Decline in new ICE car registrations | -0.4% | Germany-wide, accelerating in urban centers | Short term (≤ 2 years) |

| Lead-price volatility under EU Critical Raw Materials Act | -0.2% | Germany, broader EU supply chain | Short term (≤ 2 years) |

| Shrinking German lead-smelting capacity due to green-tax tightening | -0.3% | Germany, localized at Berzelius and other non-ferrous smelters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Shift to Li-Ion Auxiliary Batteries in New EVs

BMW now equips several models with 12 V lithium-ion units that trim 8–10 kg and outperform lead-acid in colder climates. Mercedes-Benz and Porsche pilots follow, and EUROBAT data show European auxiliary lithium-ion demand rising from under 0.5 GWh in 2024 to beyond 5 GWh by 2030. Weight savings and longer service life appeal to premium OEMs, but high cost and immature recycling networks limit broader uptake, preserving lead-acid relevance in mainstream segments for the forecast horizon.

Decline in New ICE Car Registrations

Germany registered 2.81 million new cars in 2024, down 1% year-on-year, with combustion and mild hybrids falling toward the 70% mark as CO₂ rules tighten. OEMs plan to phase out new combustion platforms by 2030, eroding first-fit SLI volumes by 2–3% annually. The aftermarket still benefits from an aging parc, but converters pivot toward AGM and Enhanced Flooded lines that command higher margins per unit to cushion volume erosion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Type: AGM Momentum as Start-Stop Peaks

Flooded batteries held a 54.85% share in 2025, but AGM lines will grow at a 6.55% CAGR as start-stop saturation approaches 90% of new registrations. Enhanced Flooded variants bridge cost and durability gaps in volume segments, while gel-cell VRLA supplies niche standby sectors. Clarios is investing EUR 200 million to lift AGM capacity 50% by 2026, anticipating aftermarket pull when today’s start-stop cars enter the replacement window.

Conventional flooded batteries dominate price-sensitive fleets, yet performance shortfalls during harsh winters and rising predictive-maintenance adoption lead operators to pay the AGM premium. Varta introduced a color-coded Enhanced Flooded line in 2024 that lowers electrolyte stratification, extending life 15–20%. Moll’s Advanced Flooded Battery targets similar durability at 20% less cost than AGM, keeping flooded chemistries competitive. Gel-cell VRLAs, while small in automotive, remain favored for telecom and UPS environments with strict safety norms.

By Battery Voltage: 12 V Dominance Meets 48 V Emergence

The 12 V class accounted for 68.05% of 2025 shipments, underscoring its centrality across combustion, mild-hybrid, and BEV auxiliary circuits. Above-60-V segments, led by 48 V mild hybrids, are forecast to grow at a 7.35% CAGR as OEMs deploy belt-starter-generators to trim CO₂ emissions. Each 48 V model still installs a 12 V AGM safety battery, preserving traditional SLI demand even as lithium-ion traction packs proliferate.

OEMs are evaluating DC-DC architectures that could delete the 12 V unit, yet functional-safety rules delay volume adoption. Meanwhile, ADAC data show 58% of 2020-built BEV breakdowns in 2023 were caused by 12 V failures, reinforcing the chemistry’s indispensability. Industrial motive-power systems above 60 V witness early lithium-ion substitution, but lead-acid remains entrenched in lower-duty forklifts where upfront costs dictate procurement.

By Application: Passenger Cars Anchor, Agriculture Accelerates

Passenger cars supplied 52.25% of volume in 2025, driven by a 49.1 million-vehicle parc and a 10.3-year average age. Light commercial vans grow at mid-single digits alongside e-commerce logistics, adopting AGM to cut roadside downtime. Heavy trucks expand more slowly, reflecting longer replacement cycles and emerging hydrogen buses in municipal fleets.

Agricultural and off-highway vehicles will post a 5.65% CAGR through 2031, fueled by Stage V emissions rules and zero-emission construction mandates that still rely on 12 V AGM back-ups for control systems. Industrial motive-power sectors face lithium-ion and sodium-ion pilots, yet lead-acid retains safety and cost advantages until the total cost of ownership falls further. Standby telecom and UPS niches grow slowly as data-center operators shift to higher-density chemistries, but lead-acid endures where low-temperature resilience is essential.

Geography Analysis

Germany remains the epicenter of the Central European aftermarket, benefiting from dense workshop networks and premium-OEM clusters that adopt advanced chemistries first. Harsh winters in northern and eastern states amplify fourth-quarter replacement spikes, while a 13.5% BEV registration share in 2024 signals electrification’s rise yet leaves 70% of new cars with combustion or mild-hybrid drivetrains that still install 12 V batteries. Lead-recycling capacity operates near 95% collection, but smaller AGM and EFB formats yield less lead per unit, squeezing smelter economics in the face of stricter NOₓ and SO₂ caps.

The Berzelius smelter’s retrofit challenges illustrate tightening green taxes that may reduce domestic refining output, increasing reliance on imports, and lengthening supply chains. Germany’s central role in European automotive supply chains means start-stop, 48 V, and lithium-ion auxiliary innovations surface locally before rolling into neighboring markets, offering first-mover advantages to German converters that scale premium lines early. Agricultural and off-highway equipment gains steam in southern regions where construction projects adopt zero-emission targets, and industrial forklifts in logistics hubs continue to balance lead-acid durability against lithium-ion performance advantages.

Mordor Intelligence's coverage of the sli battery market extends across other regions including Europe and Middle East and Africa, while country-specific intelligence is also available for United Kingdom, Italy, China, United States, India, and France, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The German SLI battery market features moderate concentration. Clarios, Exide Technologies, and Varta AG hold a majority share through distributor depth, OEM approvals, and lifetime brand equity. Banner GmbH and Hoppecke Batterien exploit industrial and standby niches, leveraging customization and quick lead times. Asian challengers GS Yuasa, Amara Raja, and HBL Power expand via Turkey-based hubs to undercut flooded-battery prices; GS Yuasa’s European sales rose 20% in FY 2024.

Technology differentiation centers on cycle life, cold-cranking amps, and digital maintenance integration. Bosch Battery Guard and Continental ProViu Connect embed health telemetry, cutting fleet downtime and steering buyers toward AGM upgrades. Clarios’s EUR 200 million AGM expansion positions it for aftermarket dominance as start-stop penetration peaks. Varta’s talks with Porsche over a stake in its V4Drive lithium-ion subsidiary reveal incumbent strategies to hedge against auxiliary-battery electrification. Moll’s Advanced Flooded launches, and EnerSys’s FIAMM acquisition highlight tactical moves to grab share in cost-sensitive or industrial sub-segments.

Germany SLI Battery Industry Leaders

Clarios (VARTA brand)

Exide Technologies

Varta AG

Hoppecke Batterien GmbH & Co KG

Banner GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: The inaugural Primobius battery recycling facility, located at Mercedes-Benz in Kuppenheim, celebrated its grand opening. This plant, dedicated to the industrial recycling of traction batteries, underscores Germany's commitment to amplifying its battery recycling efforts.

- August 2024: Clarios unveiled a significant EUR 200 million initiative (spanning 2022–2026) aimed at bolstering AGM/VRLA SLI battery production across Europe. The centerpiece of this expansion is the Hanover plant in Germany, marking a pivotal investment in the SLI supply chain catering to both German OEMs and aftermarket channels.

- March 2024: Exide Technologies, a European lead-acid battery manufacturer, announced the acquisition of BE-Power, a German lithium battery tech firm, to enhance the development and assembly of lithium-ion batteries and power modules.

- February 2024: The EU's Sustainable Battery Regulation, which includes categories such as "SLI/automotive battery," came into effect. This regulation imposes new labelling, reporting, and design-for-recycling mandates, directly impacting SLI battery manufacturers and importers in Germany.

Germany SLI Battery Market Report Scope

An SLI (starting, lighting, and ignition) battery is a type of rechargeable battery designed primarily for automotive applications. It is used to start the engine, power the vehicle's lighting system, and ignite the fuel. These batteries are typically lead-acid batteries, favored for their reliability and ability to deliver high surge currents needed to start an engine.

The German SLI battery market is segmented by battery type, battery voltage, and application. By battery type, the market is segmented into flooded, enhanced flooded, absorbent glass mat (AGM), and gel cell VRLA. By battery voltage, the market is segmented into up to 12V, 12V, 48V, and above 60V. By application, the market is segment into passenger cars, light commercial vehicles, heavy commercial vehicles, two-/three-wheelers, agricultural & off-highway vehicles, industrial motive power (forklifts, material-handling), and stand-by/backup (telecom, UPS). For each segment, market sizing and forecasts are presented on a value (USD) basis.

| Flooded (Conventional) |

| Enhanced Flooded (EFB) |

| Absorbent Glass Mat (AGM) |

| Gel Cell VRLA |

| Up to 12 V |

| 12 V |

| 48 V |

| Above 60 V |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Two-/Three-Wheelers |

| Agricultural and Off-Highway Vehicles |

| Industrial Motive Power (Forklifts, Material-Handling) |

| Stand-by/Backup (Telecom, UPS) |

| By Battery Type | Flooded (Conventional) |

| Enhanced Flooded (EFB) | |

| Absorbent Glass Mat (AGM) | |

| Gel Cell VRLA | |

| By Battery Voltage | Up to 12 V |

| 12 V | |

| 48 V | |

| Above 60 V | |

| By Application | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| Two-/Three-Wheelers | |

| Agricultural and Off-Highway Vehicles | |

| Industrial Motive Power (Forklifts, Material-Handling) | |

| Stand-by/Backup (Telecom, UPS) |

Key Questions Answered in the Report

How large is the Germany SLI battery market in 2026?

The Germany SLI battery market size is USD 1.26 billion in 2026 and is forecast to reach USD 1.42 billion by 2031.

What is driving AGM battery demand in Germany?

Rising start-stop penetration, harsh winter conditions, and predictive-maintenance adoption are pushing fleets and owners toward AGM chemistries with longer cycle life and higher cold-cranking power.

Why does a 48 V mild hybrid still need a 12 V battery?

The 12 V unit powers critical control, safety, and infotainment circuits when the 48 V network is offline, providing a fail-safe back-up that satisfies functional-safety rules.

How is EU regulation affecting lead sourcing?

Regulation 2023/1542 and the Critical Raw Materials Act demand higher recycled content and local sourcing, driving up scrap prices and encouraging vertically integrated recycling.

Which segment shows the fastest growth through 2031?

Above-60-volt batteries, mainly 48 V mild-hybrid systems, are projected to grow at a 7.35% CAGR as German OEMs expand belt-starter-generator adoption.

Who are the leading suppliers in the Germany SLI battery space?

Clarios, Exide Technologies, and Varta AG dominate, with Banner, Hoppecke, GS Yuasa, and emerging lithium-ion entrants adding competitive diversity.

Page last updated on: