Germany Hybrid Electric Vehicle Battery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

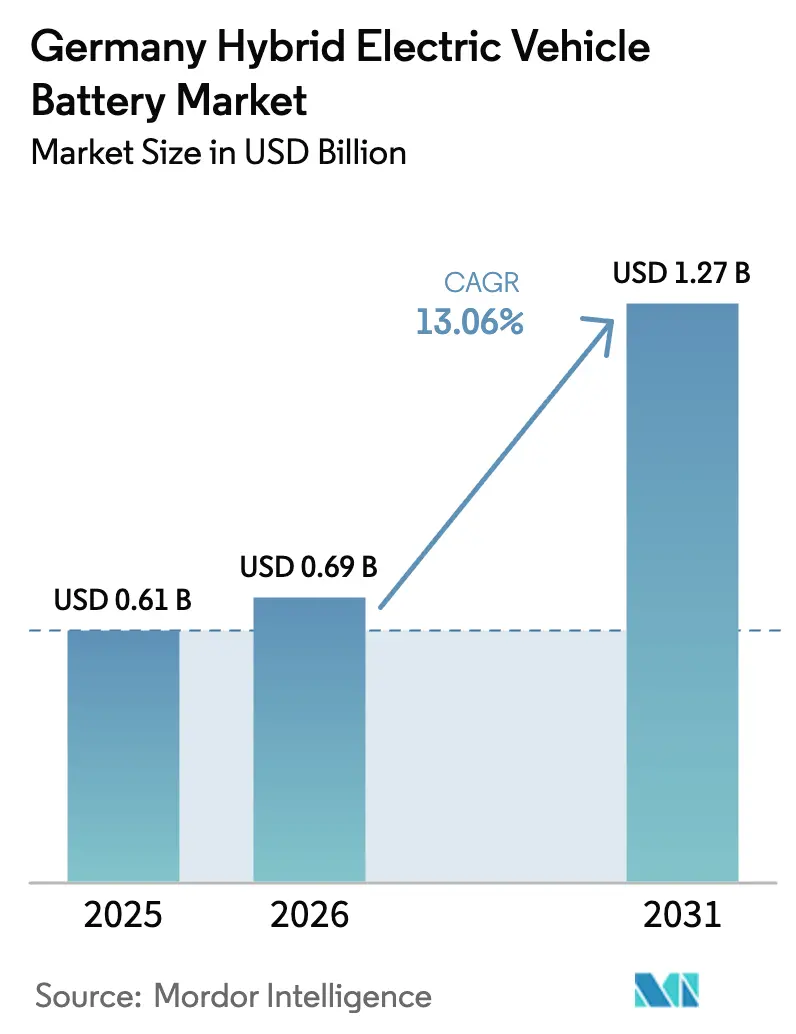

| Base Year Market Size (2025) | USD 0.61 Billion |

| Market Size (2026) | USD 0.69 Billion |

| Market Size (2031) | USD 1.27 Billion |

| Growth Rate (2026 - 2031) | 13.06% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Hybrid Electric Vehicle Battery Market Analysis by Mordor Intelligence

Germany Hybrid Electric Vehicle Battery Market size in 2026 is estimated at USD 0.69 billion, growing from 2025 value of USD 0.61 billion with 2031 projections showing USD 1.27 billion, growing at 13.06% CAGR over 2026-2031.

Tightening EU fleet-average CO₂ limits, accelerating OEM vertical-integration programs, and the slow ramp-up of domestic cell plants are combining to raise local battery demand faster than supply. CATL’s Erfurt factory produced only 8 GWh in 2024 against national demand exceeding 60 GWh, forcing most carmakers to continue importing cells from Asia while new giga-factories in Salzgitter and Heide move through construction.[1]VDI/VDE-IT, “Battery Production and Demand in Germany 2024,” vdivde-it.de Falling lithium-ion pack prices, which averaged USD 139 /kWh globally in 2023, are improving plug-in hybrid economics and supporting the substitution of diesel engines in fleet applications. At the same time, the rise of 48-volt mild hybrids gives manufacturers a low-cost compliance path, and premium brands are adopting 800-volt architectures to unlock ultra-fast charging. Execution risk around giga-factory build-outs and real-world PHEV emissions scrutiny temper the growth outlook, but do not derail it.

Key Report Takeaways

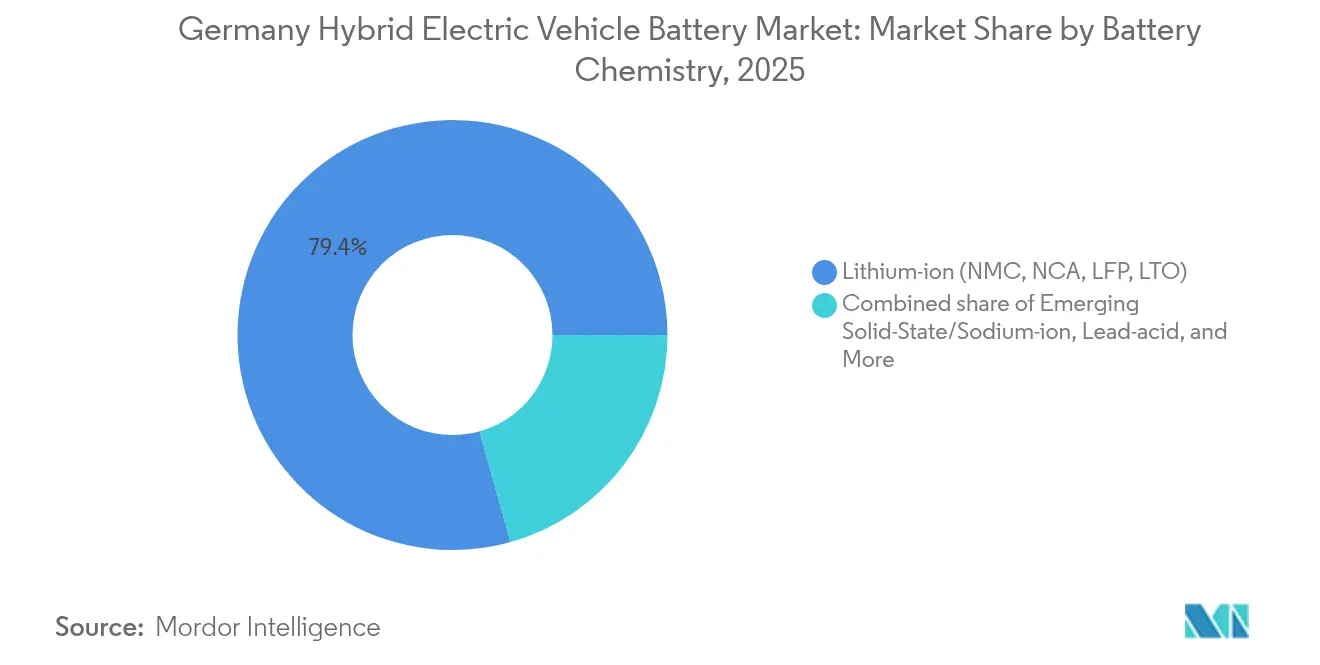

- By battery chemistry, lithium-ion led with 79.35% revenue share in 2025; emerging solid-state and sodium-ion technologies are forecast to expand at a 27.1% CAGR to 2031.

- By degree of hybridization, mild hybrids held 48.10% of the German hybrid electric vehicle battery market share in 2025, while the same segment is projected to post the highest 15.1% CAGR through 2031.

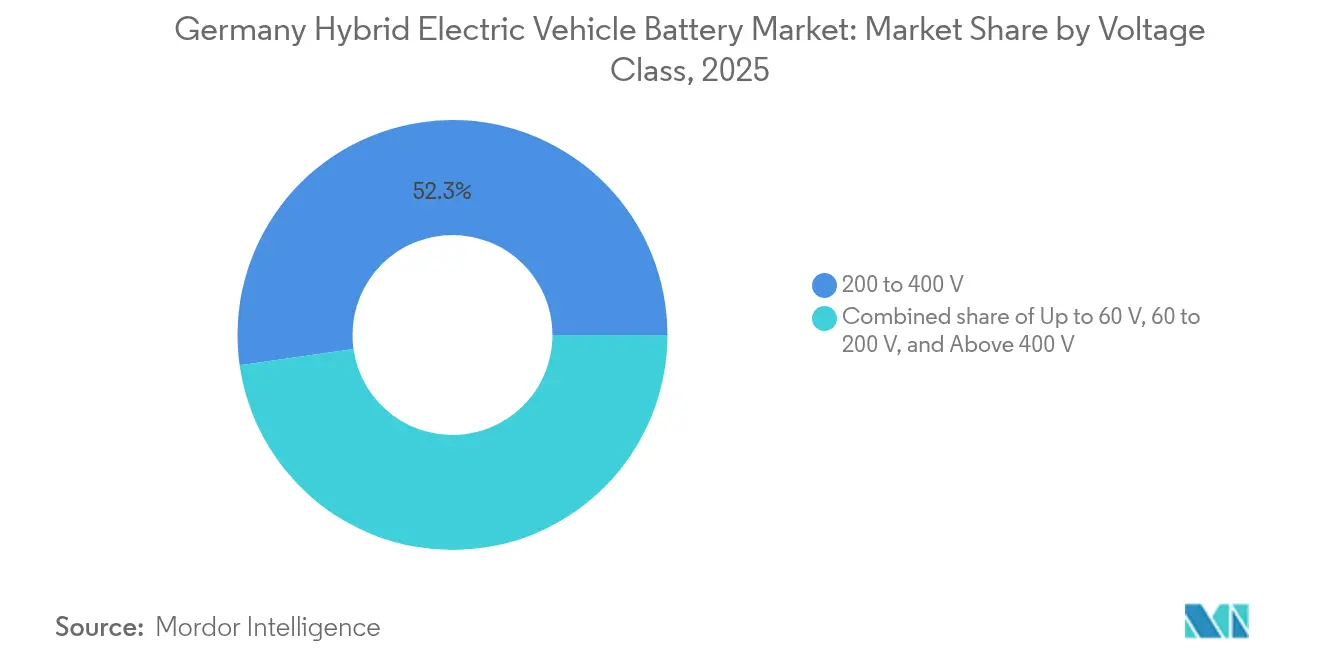

- By voltage class, the 200-to-400-volt category accounted for a 52.25% share of the German hybrid electric vehicle battery market size in 2025, and the above-400-volt class is advancing at a 17.2% CAGR through 2031.

- By vehicle class, passenger cars captured a 56.70% share of the German hybrid electric vehicle battery market size in 2025 and are rising at a 15.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Figures recorded within Germany feed into a worldwide estimate while studying the global industry. Mordor Intelligence's hybrid electric vehicle battery market size captures this aggregation.

Germany Hybrid Electric Vehicle Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter EU CO₂-fleet limits accelerating HEV adoption | 3.20% | Germany, broader EU-27 | Medium term (2-4 years) |

| Rapid decline in lithium-ion battery $/kWh | 2.80% | Global, Germany procurement | Short term (≤ 2 years) |

| OEM giga-factory investments inside Germany | 2.50% | Germany (Salzgitter, Heide, Erfurt) | Long term (≥ 4 years) |

| Tax incentives for hybrid company cars | 1.40% | Germany federal and Länder | Short term (≤ 2 years) |

| Sodium-ion pilot lines entering German supply chain | 0.90% | Germany, early EU sites | Long term (≥ 4 years) |

| Corporate fleet CO₂ mandates (Scope-3) lifting demand | 1.60% | Germany, EU corporates | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter EU CO₂-Fleet Limits Accelerating HEV Adoption

EU passenger-car fleet targets fall to 93.6 g/km in 2025, exposing OEMs to EUR 95 penalties for each gram of excess CO₂ per vehicle sold, which makes 48-volt systems a cost-effective way to secure 10-15% savings without the capital load of full EV platforms.[2]European Commission, “Regulation (EU) 2023/851 Amending CO₂ Emission Standards,” europa.eu Germany’s annual output of nearly 4 million vehicles concentrates compliance risk, so automakers are layering mild hybrids across high-volume models while premium brands push high-voltage plug-in hybrids for deeper cuts. BloombergNEF projects the region’s EV share will hit 41% by 2027, with hybrids bridging gaps where public charging or consumer willingness to pay remain limited.[3]BloombergNEF, “Battery Price Survey 2024,” bloomberg.com Cell suppliers that fail to reserve capacity for 48-volt packs risk losing share as OEMs scramble to secure contracts ahead of the 2025 deadline.

Rapid Decline in Lithium-Ion Battery $/kWh

Pack-level prices slipped to USD 139 /kWh in 2023 and could drop below USD 100 by 2027 as scale, LFP adoption, and dry-electrode processes mature. Volkswagen’s PowerCo and Koenig & Bauer are piloting dry coating that may trim cell-factory energy use by 15-20% once the proof-of-concept arrives in 2025.[4]Koenig & Bauer, “Dry Coating Technology Partnership with PowerCo,” koenig-bauer.com Lower pack costs let carmakers position plug-in hybrids against diesel in fleet bids, yet raw-material volatility means long-term supply deals remain critical.

OEM Giga-Factory Investments Inside Germany

Volkswagen, Northvolt, and CATL collectively earmarked over EUR 5 billion for cell plants in Salzgitter, Heide, and Erfurt, targeting a combined 114 GWh before 2027. Northvolt broke ground in 2024 with EUR 902 million in state aid but filed for U.S. Chapter 11 in November 2024, highlighting execution risk. Volkswagen cut Salzgitter’s initial ramp to half capacity amid softer demand, while CATL is scaling Erfurt to 14 GWh with LFP cost advantages. Domestic output reduces logistics emissions and meets upcoming battery passport rules, yet OEMs still hedge with Asian suppliers until new factories prove yield and cost targets.

Tax Incentives for Hybrid Company Cars

Germany allows a 0.5% monthly benefit-in-kind rate for PHEVs that offer at least 40 km electric range or emit under 50 g/km CO₂, compared with 1% for conventional cars, keeping plug-in hybrids popular among companies that represent roughly 60% of national registrations. Political debate on the real-world effectiveness of these incentives may tighten eligibility, so OEMs are contemplating larger 15-20 kWh packs to stay within future thresholds, even if that lifts curb weight.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Battery life-cycle replacement cost uncertainty | −1.8% | Germany, EU fleet operators | Medium term (2-4 years) |

| Phase-out of PHEV purchase subsidies after 2023 | −2.3% | Germany federal | Short term (≤ 2 years) |

| Real-world PHEV emission scrutiny tightening rules | −1.5% | Germany, EU regulators | Medium term (2-4 years) |

| EU raw-material refining deficit for next-gen chemistries | −1.2% | EU-wide, Germany impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Battery Life-Cycle Replacement Cost Uncertainty

Hybrid-pack warranties cover 8 years or 160,000 km, yet a 15 kWh PHEV pack can cost EUR 5,000-10,000 to replace, equaling 15-25% of residual value. Limited third-party refurbishment and proprietary BMS lock-outs compound fears, depressing used-vehicle prices and raising lease costs. OEMs investing in closed-loop recycling and modular repair, such as Volkswagen’s PowerCo, aim to cut life-cycle costs and reassure buyers.

Phase-Out of PHEV Purchase Subsidies After 2023

The December 2023 end of the Umweltbonus for plug-in hybrids removed up to EUR 4,500 per vehicle, helping push 2024 EV sales 29% below prior forecasts. Consumers are shifting toward mild hybrids, while OEMs channel plug-in variants into higher-margin premium segments. Battery suppliers must rebalance capacity toward small 48-volt packs even as they maintain energy-dense lines for fleet PHEVs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: Lithium-Ion Stays Dominant as Alternatives Scale

Lithium-ion retained 79.35% of the German hybrid electric vehicle battery market share in 2025, fueled by mature supply chains and energy densities up to 280 Wh/kg. Nickel-rich NMC dominates premium plug-in hybrids, while LFP is gaining mild-hybrid traction thanks to its cobalt-free cost edge. The German hybrid electric vehicle battery market size for lithium-ion packs is projected to rise in tandem with vehicle output, yet solid-state and sodium-ion chemistries are forecast to post a 27.1% CAGR, capitalizing on safety and raw-material advantages.

Solid-state prototypes promise 400 Wh/kg and are drawing BMW and Mercedes-Benz partnerships, whereas sodium-ion pilot lines aim at 48-volt systems where density is less critical. The resulting multi-chemistry landscape forces suppliers to keep flexible production and dual-sourcing strategies.

By Degree of Hybridization: Mild Hybrids Command Volume

Mild hybrids secured 48.10% of the German hybrid electric vehicle battery market share in 2025 and are expanding at a 15.1% CAGR as OEMs deploy 48-volt systems across high-volume models. System costs hover around EUR 800-1,200, roughly one-third of plug-in hybrid bills, delivering 10-15% fuel savings that meet interim CO₂ rules.

Plug-in hybrids remain essential for premium and fleet segments that demand 50 km electric range, yet subsidy loss and emissions scrutiny cap unit growth. Full hybrids are squeezed between the cost-effectiveness of mild hybrids and the range capability of plug-ins, prompting many brands to streamline offerings.

By Voltage Class: Fast-Charge Platforms Accelerate

The 200-to-400-volt class captured 52.25% of the 2025 value, reflecting mainstream plug-in hybrid architectures. Above-400-volt systems, led by Porsche and other premium OEMs, are on track for a 17.2% CAGR, enabling 800-V fast-charging that cuts session times below 15 minutes.

In contrast, the sub-60-volt tier, principally 48-V mild hybrids, dominates unit volumes but not capacity due to pack sizes of 0.5-1.5 kWh. Voltage segmentation is polarizing toward 48 V for compliance and 800 V for performance, leaving the mid-range to decline as technology curves advance.

By Vehicle Class: Passenger Cars Lead but Commercial Fleets Race Ahead

Passenger cars held 56.70% of the German hybrid electric vehicle battery market size in 2025 and are climbing at a 15.6% CAGR through 2031 as brands refresh model lines with mild and plug-in variants. Private buyers favor long-range plug-in hybrids for tax savings, while company fleets adopt mild hybrids for low TCO.

Commercial vehicles, especially last-mile delivery vans, are growing faster from a smaller base as Scope-3 mandates take effect. These duty cycles require high-durability packs and rugged thermal designs, opening white-space for suppliers that specialize in industrial-grade solutions.

Geography Analysis

Germany generated about 60 GWh of battery demand in 2023 but produced only 8 GWh domestically, underscoring reliance on Asian imports until Salzgitter and Heide reach scale after 2025. Northern states such as Schleswig-Holstein gain visibility by pairing wind-powered giga-factories with low-carbon footprints, whereas Lower Saxony anchors Volkswagen’s PowerCo hub.

Bavaria and Baden-Württemberg remain engineering centers for Mercedes-Benz and BMW, focusing on high-voltage and solid-state R&D. The geographic split means northern clusters chase volume and renewable energy, while southern hubs pursue premium chemistries and closed-loop recycling, aligning with EU Battery Regulation carbon-footprint labels that start in 2027.

Neighboring Poland and Hungary are adding large cell plants from LG Energy Solution, Samsung SDI, and CATL, supplying German OEMs and diversifying risk. Spain’s emerging Valencia hub further supports regional balance. Germany, therefore, evolves from a pure demand center to an integrated node combining owned plants, cross-border sourcing, and advanced-chemistry leadership.

Mordor Intelligence evaluates the hybrid electric vehicle battery market across all key regional markets, including Europe, North America, and South America, with deeper country-level insights covering United Kingdom, Italy, United States, India, China, and France.

Competitive Landscape

Asian incumbents, CATL, LG Energy Solution, Samsung SDI, Panasonic, still supply most German hybrid cells, yet European challengers and OEM captive ventures are reshaping the field. CATL is scaling Erfurt to 14 GWh and targeting 2025 profitability with LFP pricing power. Northvolt’s 60 GWh Heide project illustrates European ambition but also capital risk after its 2024 U.S. bankruptcy filing.

Volkswagen’s PowerCo pilots dry-electrode coating to shave 15-20% from cell production cost, seeking a home-field cost advantage. Porsche’s majority stake in Varta’s V4Drive brings ultra-high-power cylindrical cells in-house, underscoring OEM moves toward technology ownership.

Opportunity spaces include ruggedized pack integrators for commercial vehicles and recycling firms that meet EU recycled-content quotas. Competitive edge is migrating from pure GWh scale to system-level innovation, manufacturing process IP, and upstream material security, propelling consolidation among standalone cell makers while rewarding vertically integrated players.

Germany Hybrid Electric Vehicle Battery Industry Leaders

LG Energy Solution

Contemporary Amperex Technology Co Ltd.

BYD Company

Samsung SDI

Panasonic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Porsche AG finalized the acquisition of a majority stake in V4Drive Battery GmbH, securing ultra-high-power cylindrical cell technology for future 800-V platforms.

- December 2024: Volkswagen PowerCo and Koenig & Bauer confirmed progress on dry-powder electrode coating, aiming for a mid-2025 proof-of-concept that could cut cell costs by up to 20%.

- November 2024: Northvolt AB filed for U.S. Chapter 11, casting uncertainty over the 60 GWh Heide plant backed by EUR 902 million German state aid.

- September 2024: Volkswagen announced a reduced ramp at the Salzgitter cell factory, citing cost pressure and softer demand, and will run at roughly half its initial capacity.

Germany Hybrid Electric Vehicle Battery Market Report Scope

A hybrid electric vehicle (HEV) battery is a critical component of a hybrid vehicle's powertrain system. The battery allows hybrid electric vehicles to achieve better fuel efficiency and lower emissions compared to traditional internal combustion engine vehicles by enabling regenerative braking, which captures and stores energy that would otherwise be lost during braking. The stored energy can then be used to reduce the load on the internal combustion engine or power the vehicle at low speeds, contributing to the overall efficiency and eco-friendliness of hybrid vehicles.

The German hybrid electric vehicle battery market is segmented by battery chemistry, degree of hybridization, voltage class, and vehicle class. By battery chemistry, the market is segmented into Lithium-Ion Battery, Lead-Acid Battery, Sodium-Ion Battery, and Others. The market is segmented by degree of hybridization into Mild Hybrid (48 V MHEV), Full Hybrid (HEV), Plug-in Hybrid (PHEV), and Range-Extender Hybrid. By voltage class, the market is divided into Up to 60 V, 60 to 200 V, 200 to 400 V, and Above 400 V. By vehicle class, the market is segmented into Passenger Cars, Commercial Vehicles, Two-/Three-Wheelers, and Off-Highway and Specialty. The report offers market size forecasts in revenue (USD) for all the above segments.

| Lithium-ion (NMC, NCA, LFP, LTO) |

| Nickel-Metal Hydride (NiMH) |

| Lead-acid |

| Emerging Solid-State/Sodium-ion |

| Mild Hybrid (48 V MHEV) |

| Full Hybrid (HEV) |

| Plug-in Hybrid (PHEV) |

| Range-Extender Hybrid |

| Up to 60 V |

| 60 to 200 V |

| 200 to 400 V |

| Above 400 V |

| Passenger Cars |

| Commercial Vehicles |

| Two-/Three-Wheelers |

| Off-Highway and Specialty |

| By Battery Chemistry | Lithium-ion (NMC, NCA, LFP, LTO) |

| Nickel-Metal Hydride (NiMH) | |

| Lead-acid | |

| Emerging Solid-State/Sodium-ion | |

| By Degree of Hybridization | Mild Hybrid (48 V MHEV) |

| Full Hybrid (HEV) | |

| Plug-in Hybrid (PHEV) | |

| Range-Extender Hybrid | |

| By Voltage Class | Up to 60 V |

| 60 to 200 V | |

| 200 to 400 V | |

| Above 400 V | |

| By Vehicle Class | Passenger Cars |

| Commercial Vehicles | |

| Two-/Three-Wheelers | |

| Off-Highway and Specialty |

Key Questions Answered in the Report

What is the forecast value of the Germany hybrid electric vehicle battery market in 2031?

The market is projected to reach USD 1.27 billion by 2031, reflecting a 13.06% CAGR from 2026-2031.

Which battery chemistry holds the largest share in German hybrids?

Lithium-ion chemistries accounted for 79.35% of 2025 revenue, far ahead of other chemistries.

Why are 48-volt mild hybrids growing rapidly in Germany?

They deliver 10-15% fuel-savings at one-third the cost of plug-in systems, helping automakers achieve EU CO₂ targets.

How will sodium-ion technology impact future hybrid batteries?

Sodium-ion pilot lines planned for 2026 could lower material costs for 48-volt packs and diversify raw-material sourcing.

What risks threaten new German giga-factory projects?

Cost overruns, softer vehicle demand, and supply-chain financing challenges have already slowed expansions at Salzgitter and Heide.

Which vehicle segment will add the most battery demand through 2031?

Passenger cars remain the largest volume driver, but commercial vans show the fastest incremental growth due to Scope-3 mandates.

Page last updated on: