Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

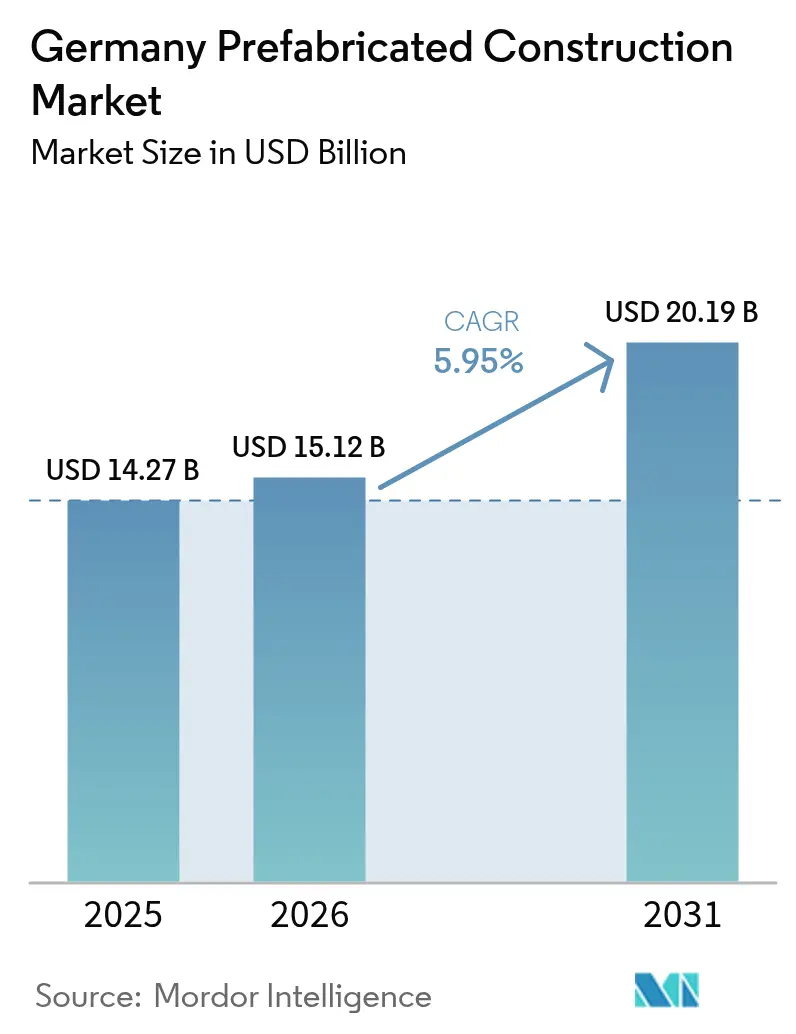

| Base Year Market Size (2025) | USD 14.27 Billion |

| Market Size (2026) | USD 15.12 Billion |

| Market Size (2031) | USD 20.19 Billion |

| Growth Rate (2026 - 2031) | 5.95% CAGR |

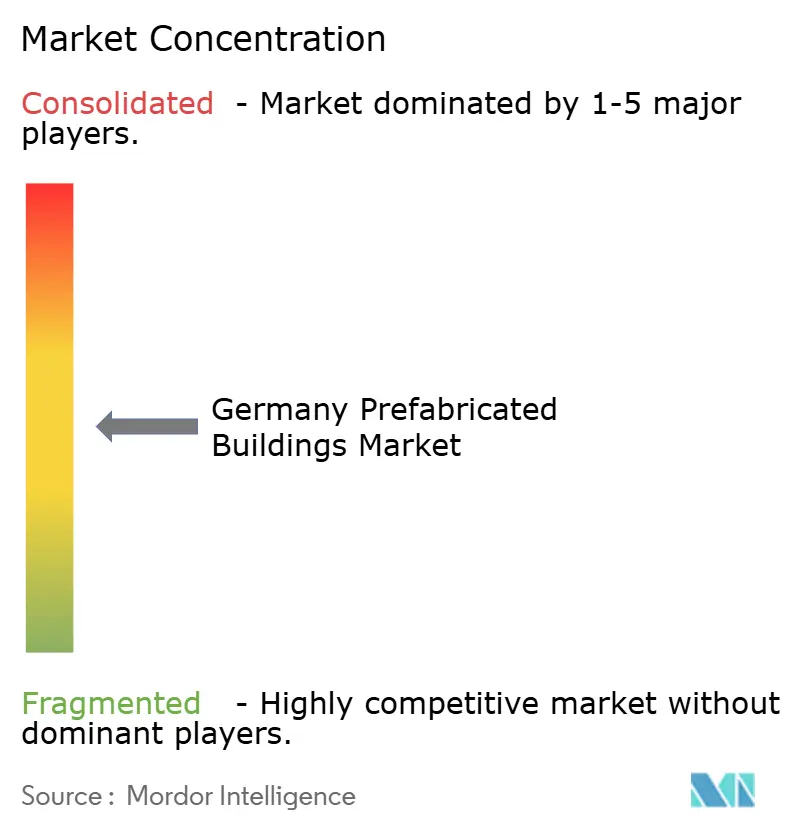

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Prefabricated Construction Market Analysis by Mordor Intelligence

The Germany Prefabricated Construction Market size is projected to be USD 14.27 billion in 2025, USD 15.12 billion in 2026, and reach USD 20.19 billion by 2031, growing at a CAGR of 5.95% from 2026 to 2031.

Mounting housing shortages, a widening skilled-labor gap, and firm policy mandates to lower construction-sector carbon emissions are steering public and private developers toward factory-controlled assembly. Municipal housing agencies are prioritizing serial delivery methods because modules shorten site programs by as much as 50%, trim weather-related downtime, and lock in cost certainty. Corporates are following, attracted by net-zero certifications and the ease of integrating high-performance envelopes, heat pumps, and rooftop solar in the factory. Suppliers that combine vertical integration with digital design tools command a rising price premium because they guarantee material provenance, accelerate approvals, and minimize re-work. Meanwhile, plant capacity limits, transport width restrictions, and fragmented permitting rules temper the overall speed at which the Germany prefabricated construction market can scale.

Key Report Takeaways

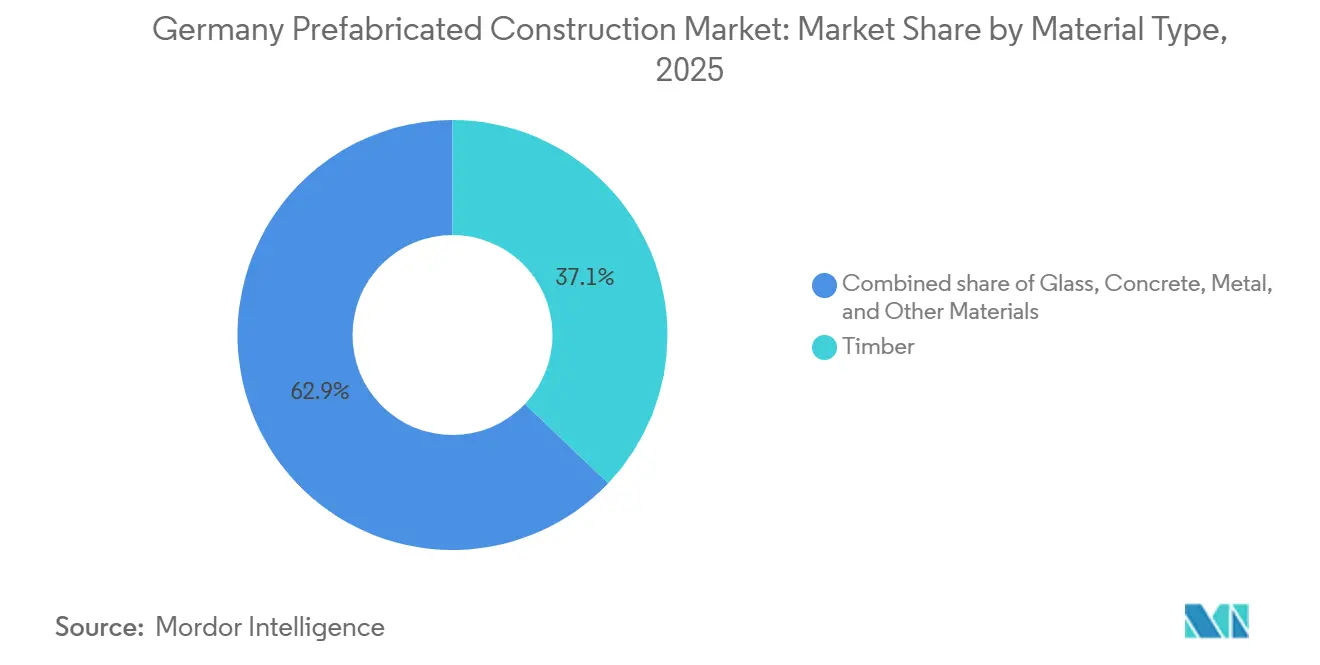

- By material type, timber led with 37.1% of Germany prefabricated construction market share in 2025, while glass-intensive façades are projected to grow at a 6.55% CAGR through 2031.

- By application, residential captured 59.5% of the Germany prefabricated construction market size in 2025; commercial is advancing at a 6.38% CAGR to 2031.

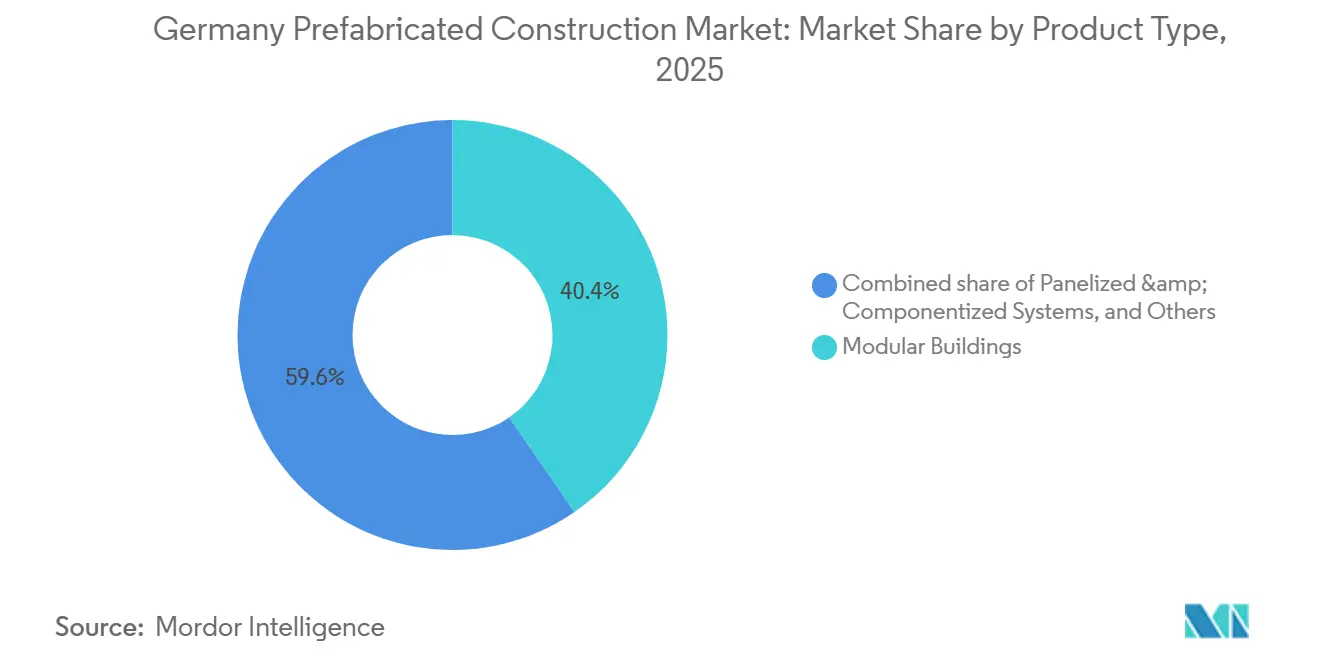

- By product type, modular units held 40.4% of Germany prefabricated construction market share in 2025, yet panelized systems are set to expand at a 6.44% CAGR over 2026-2031.

- Berlin accounted for 20.4% of the Germany prefabricated construction market size in 2025, whereas Hamburg records the fastest projected CAGR at 6.93% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Prefabricated Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing shortages and faster delivery needs accelerating the adoption of modular and panelized construction | +1.8% | National, with acute pressure in Berlin, Munich, Frankfurt, Hamburg | Medium term (2–4 years) |

| High on-site labor costs and skilled-trade gaps are increasing the shift toward factory-built methods | +1.5% | National, especially southern Germany | Long term (≥ 4 years) |

| Strong demand for energy-efficient buildings is boosting the uptake of high-performance prefab envelopes | +1.3% | National, aligned with GEG compliance | Medium term (2–4 years) |

| Growing use of timber-hybrid and lightweight prefab systems supporting multi-storey projects | +1.0% | National urban infill | Long term (≥ 4 years) |

| Standardized designs and repeatable components improve cost certainty for developers and contractors | +0.9% | National residential and education sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Housing Shortages And Faster Delivery Needs Accelerate the Adoption Of Modular And Panelized Construction

Germany faces a housing backlog estimated at 700,000 units, and public buyers now award contracts on the basis of delivery speed as much as price[1]Federal Ministry for Housing, Urban Development and Building, “Alliance for Affordable Housing,” bmwsb.bund.de . Factory-built modules trim program lengths by 30%-50%, allowing municipalities to meet annual targets without enlarging project teams. The Alliance for Affordable Housing allocates USD 15.8 billion in subsidies that explicitly favor serial construction, further reducing investor risk. GOLDBECK’s 860-unit Greenpark scheme in Berlin-Neukölln, due in 2026, illustrates how volumetric units land on constrained plots in days instead of months. This alignment of policy, cost, and speed positions the Germany prefabricated construction market for sustained residential demand.

High On-Site Labor Costs And Skilled-Trade Gaps Increasing Shift Toward Factory-Built Methods

Sector wages have risen 4.2% per year since 2024, while retirements outpace new apprentices, especially in Bavaria and Baden-Württemberg[2]Institute for Employment Research, “Labour Market Report 2025,” iab.de . Moving 80% of labor hours into plants lets producers introduce robotics, fixed jigs, and parallel workflows that lift productivity by up to 30%. ALHO reports 70% fewer site labor hours per project, cutting safety incidents and noise complaints. Developers value this insulation from subcontractor shortages because loans accrue interest whether crews are present or not. As plant utilization rises, labor substitution will remain a durable cost lever for the Germany prefabricated construction market.

Strong Demand For Energy-Efficient Buildings Boosting Uptake Of High-Performance Prefab Envelopes

The Buildings Energy Act (GEG) requires near-zero energy performance, making airtight prefab panels with U-values below 0.15 W/m²K attractive to buyers[3]Federal Ministry for Economic Affairs and Climate Action, “Energy in Buildings,” bmwk.de . The BEG program adds a 15% retrofit bonus when façade elements arrive pre-insulated, spurring orders for serial upgrades. Vonovia used Baufritz timber modules to elevate 74 flats to KfW-55 without evicting tenants, proving the tenant-in-place model. Factory assembly simplifies the integration of heat pumps and solar-ready ducts that are cumbersome on sites. Energy mandates, therefore, amplify the technical edge of the Germany prefabricated construction market over conventional construction.

Growing Use Of Timber-Hybrid And Lightweight Prefab Systems Supporting Multi-Storey Projects

Cross-laminated timber paired with steel or concrete cores now qualifies for fire classes up to F90, opening the mid-rise segment to off-site producers. Lighter superstructures reduce foundation loads by 20%-30%, saving cost and enabling builds on soft soils. GOLDBECK’s 42,000 m² Siemens Campus Module 8 combines timber-concrete floors with geothermal heat pumps to achieve carbon-neutral operation. Investors value the embedded-carbon savings, estimating roughly 1 ton of CO₂ sequestered per cubic meter of timber. These credentials strengthen ESG positioning for the Germany prefabricated construction industry.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Planning approvals and building-code compliance requirements are extending project timelines | –0.8% | National, varied across 16 states | Medium term (2–4 years) |

| Limited factory capacity and supplier bottlenecks are constraining large-scale rollouts | –0.7% | National, tightest for timber and glazing | Short term (≤ 2 years) |

| Transport and site installation constraints for large modules increase the total delivered cost | –0.5% | Dense urban cores | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Planning Approvals And Building-Code Compliance Requirements Extending Project Timelines

Germany’s fragmented permitting landscape obliges developers to navigate 16 sets of state regulations, each interpreting fire and energy rules differently. Municipal staff unfamiliar with modular systems often request extra calculations, stretching reviews by three to six months. The 2024 Growth Initiative promises digital portals, yet rollout lags; some offices still demand paper submissions. Even with a national system approval, cranes, access roads, and hydrant placements need fresh local sign-off. These steps erode some of the time gains that the Germany prefabricated construction market achieves in factories.

Limited Factory Capacity And Supplier Bottlenecks Constraining Large-Scale Rollouts

High utilization at cross-laminated timber mills, precast plants, and triple-glazing lines extends material lead times to 12-16 weeks. GOLDBECK’s USD 54.5 million Kirchberg plant will add 25,000 m² of output but requires two years to fully ramp. Smaller firms lacking capital find slot allocations tight and prices firm. Glazing makers prioritize long-term contracts, forcing spot buyers to accept delays or substitutions that undermine energy targets. Capacity gaps, therefore, cap how fast the Germany prefabricated construction market can satisfy surging demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Timber Dominance Reflects Carbon And Integration Advantages

Timber commanded 37.1% of Germany prefabricated construction market share in 2025, well ahead of concrete, metal, and glass alternatives. Deep local forestry supply, short haul distances, and carbon-credit recognition bolster its position. Vertically integrated players such as WeberHaus and SchwörerHaus control sawmills, panel lines, and on-site crews, shaving weeks off schedules and locking in quality. Concrete retains importance for high-load industrial halls and hospitals, prompting GOLDBECK to invest in additional precast lines that raise the overall Germany prefabricated construction market size across mixed-material projects.

Glass-heavy façades are the fastest-growing subset, advancing at a 6.55% CAGR through 2031 as office landlords chase daylight metrics and thermal performance. Triple-pane curtain walls now achieve U-values below 0.8 W/m²K, exceeding GEG standards without opaque spandrels. Timber-hybrid frames support these skins while keeping embodied carbon low, forging a synergy that attracts ESG funds. Concrete and steel suppliers answer with lighter composite slabs and recycled-aggregate mixes, keeping material diversity alive within the Germany prefabricated construction market.

By Application: Residential Volume Meets Commercial Velocity

Residential held 59.5% of the Germany prefabricated construction market size in 2025, buoyed by the federal 400,000-unit housing target and time-bound subsidies. Social-housing agencies opt for repeatable layouts that volumetric units deliver almost ready for occupancy. Custom-home buyers also favor panelized timber frames that accommodate non-standard façades without cost overruns. Residential demand secures baseline plant throughput and underpins long-term supplier contracts across the Germany prefabricated construction market.

Commercial space is the fastest mover, rising at a 6.38% CAGR to 2031 as corporates demand net-zero operations and flexible fit-outs. The 42,000 m² Siemens Campus Module 8 demonstrates a turnkey path to CO₂ neutrality through prefab timber-concrete floors and geothermal heating. Schools and clinics occupy a strategic middle ground: they need rapid delivery and low disruption, lining up well with modular teaching blocks and surgical suites that install in vacations or weekend windows. This blend of scale and speed keeps application diversity high across the Germany prefabricated construction market.

By Product Type: Modular Units Lead, Panelized Systems Gain Flexibility

Modular buildings captured 40.4% of Germany prefabricated construction market share in 2025, thanks to fully fitted 3D units that slash site labor by 70%. Education and healthcare buyers value the predictability of stacking near-finished rooms over traditional phase sequencing. Transport width caps and inner-city crane limits, however, restrict module size, nudging some architects toward slimmer volumetric footprints that erode economies of scale.

Panelized and componentized systems are projected to grow at a 6.44% CAGR through 2031 because they ship flat, bypass most escort fees, and allow curved or stepped façades. GOLDBECK Elements sells precast walls, stairs, and façade sections directly to general contractors, extending the company’s Germany prefabricated construction market size beyond turnkey projects. Hybrid “kit-of-parts” approaches knit panels around standardized service cores, offering a compromise between speed and architectural freedom. This flexibility positions panelization to capture incremental share over the coming decade.

Geography Analysis

Berlin held 20.4% of Germany prefabricated construction market size in 2025, powered by infill redevelopments on former rail yards and brownfields that favor rapid modular assembly. The city planning office has pre-approved several systemic designs, trimming local reviews to eight weeks and helping meet a 20,000-unit annual delivery goal. Corporate campuses also emerge, with mixed-use clusters near tech hubs requesting ESG-compliant, energy-positive buildings that volumetric units enable. Tight plots encourage crane-time optimization, giving panelized systems an edge on narrow streets where swing radius is restricted.

Hamburg is projected to grow at a 6.93% CAGR to 2031 as HafenCity and Grasbrook waterfront programs impose strict carbon ceilings and tight completion dates. Developers install hybrid timber-concrete towers near active docks to cut noise, dust, and ship-route disruptions. Modular hotel blocks and student apartments dominate early phases, while retrofit façades wrap post-war housing estates to meet the 2030 Near-Zero Energy target. The port authority streamlines night-time oversize permits, trimming logistics surcharges that can otherwise stall volumetric deliveries.

Munich and Frankfurt trail marginally in present share yet post strong commercial pipelines fueled by finance and tech tenants wanting green office space on fast schedules. Construction wages above USD 55 per hour intensify the incentive to shift labor into factories. Land scarcity rewards systems that erect superstructures in days, freeing streets quickly. Smaller regional cities absorb standardized schools, care homes, and emergency facilities under the THW program, extending the Germany prefabricated construction market footprint into lower-density areas despite longer haul distances from factories.

Competitive Landscape

The competitive landscape is moderately concentrated, with a small group of leading producers collectively holding a significant share of the market’s revenue. This distribution reflects a mid-level concentration environment, characteristic of markets where several large players coexist alongside numerous smaller competitors. GOLDBECK posted USD 6.9 billion turnover and USD 7.6 billion new orders in fiscal 2024/25, underscoring economies of scope across 15 European plants. Its new subsidiary, GOLDBECK Elements, monetizes excess precast capacity by selling walls and façades to peer contractors, mirroring the “platform” logic common in manufacturing.

ALHO, KLEUSBERG, and Cadolto hold pole positions in healthcare and education because their volumetric rooms arrive pre-wired, pre-plumbed, and infection-control ready, shortening hospital downtime. Timber specialists WeberHaus, SchwörerHaus, and Baufritz pull ahead in carbon-critical residential markets through vertical control of forests, sawmills, CNC lines, and on-site crews. This single-source chain reassures municipal buyers about provenance and ESG audits, a rising tender precondition.

Midsize entrants harness digital twins and robotic saw lines, lowering break-even batch sizes and letting architects customize façades without derailing factory takt time. However, transport rules and permitting complexity reinforce economies of compliance, favoring incumbents with in-house logistics teams and multi-state code experts. The strategic race therefore tilts toward capacity expansion, component sales, and deep advisory services that embed suppliers early in design, consolidating influence across the Germany prefabricated construction market.

Germany Prefabricated Construction Industry Leaders

ALHO Systembau GmbH

Romakowski GmbH & Co. KG

MCE GmbH Niederlassung Rhein-Main

Deutsche Fertighaus Holding

Fertighaus Weiss GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: GOLDBECK’s 860-unit Greenpark project in Berlin-Neukölln is on track for handover, confirming political delivery targets inside one election cycle.

- August 2025: GOLDBECK launched GOLDBECK Elements GmbH, offering precast walls, stair cores, and façades to third-party contractors across Europe.

- October 2025: GOLDBECK completed Module 8 at Siemens Campus Erlangen, a 42,000 m² carbon-neutral office incorporating timber-concrete floors and geothermal heat pumps.

- September 2025: The German Federal Agency for Technical Relief granted GOLDBECK a framework for up to 60 standardized facilities by 2030.

Germany Prefabricated Construction Market Report Scope

By Material Type

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Others |

By Product Type

| Modular Buildings |

| Panelized & Componentized Systems |

| Other Prefab Types |

By City

| Berlin |

| Munich |

| Frankfurt |

| Hamburg |

| Rest of Germany |

| By Material Type | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application | Residential |

| Commercial | |

| Others | |

| By Product Type | Modular Buildings |

| Panelized & Componentized Systems | |

| Other Prefab Types | |

| By City | Berlin |

| Munich | |

| Frankfurt | |

| Hamburg | |

| Rest of Germany |

Key Questions Answered in the Report

What is the current size and five-year outlook for Germany’s prefabricated construction sector?

Turnover stands at USD 15.12 billion in 2026 and is projected to reach USD 20.19 billion by 2031, reflecting a 5.95% CAGR driven by housing targets, labor scarcity, and low-carbon mandates.

Which material dominates German off-site construction?

Timber holds a 37.1% production share because local forests, carbon credits, and vertically integrated mills give wood systems both cost and sustainability advantages.

Why are German developers shifting work from sites to factories?

Accelerated schedules, high wages, and tight trade availability move up to 80% of labor under roof, trimming build times by as much as half while locking in quality and energy-code compliance.

Where does most prefabricated demand come from today?

Residential schemes account for 59.5% of 2025 output as cities chase a 400,000-unit housing goal, though commercial space is the fastest riser at a 6.38% CAGR through 2031.

Which cities set the pace for new orders?

Berlin leads with 20.4% of 2025 activity, while Hamburg posts the fastest growth at 6.93% thanks to port-area redevelopments that favor modular delivery.

What still slows wider adoption of factory-built systems?

Fragmented state-level permitting, limited plant capacity for timber and glazing, and oversized-load transport fees dilute some of the time and cost gains of volumetric modules.

Page last updated on: