Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

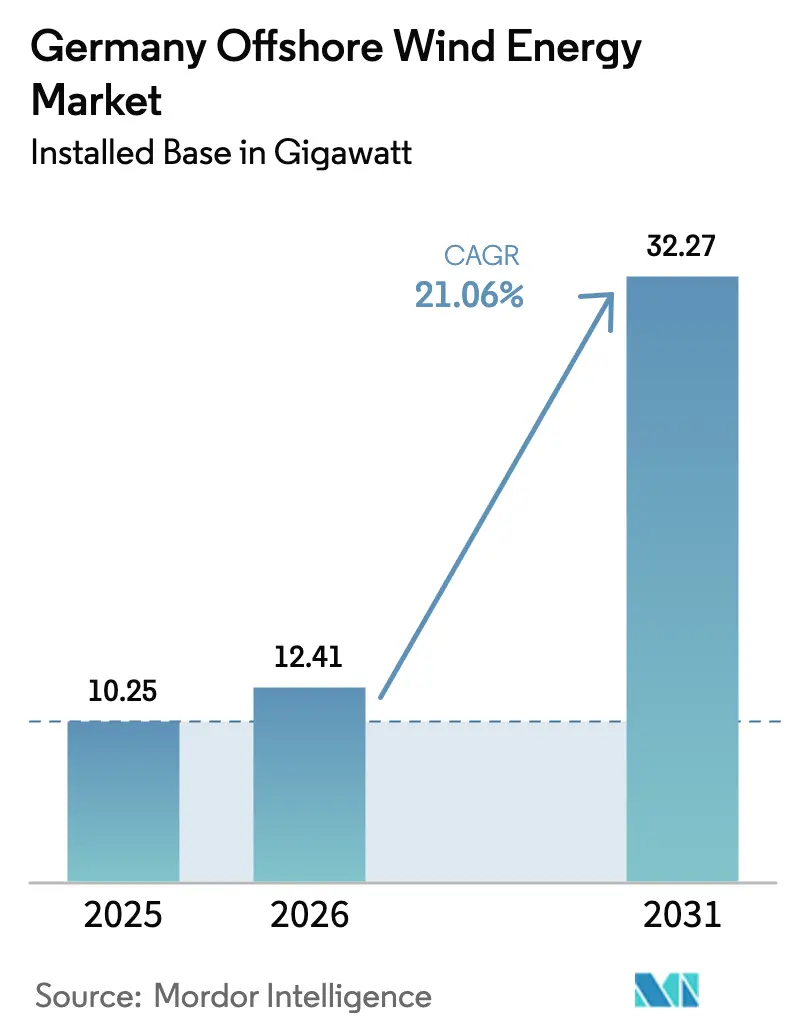

| Base Year Market Size (2025) | 10.25 gigawatt |

| Market Volume (2026) | 12.41 gigawatt |

| Market Volume (2031) | 32.27 gigawatt |

| Growth Rate (2026 - 2031) | 21.06% CAGR |

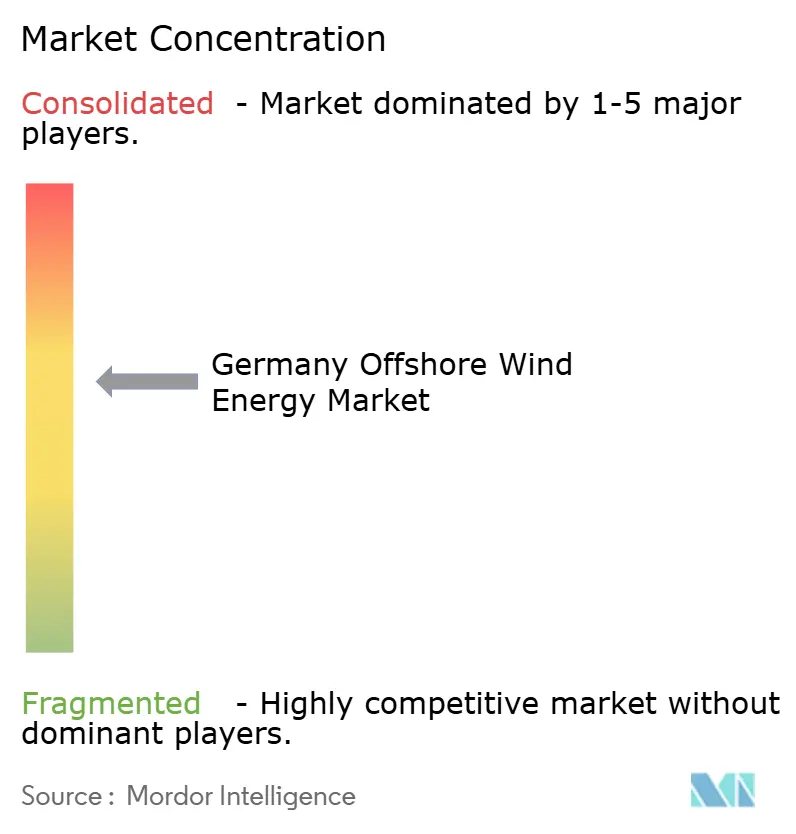

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Offshore Wind Energy Market Analysis by Mordor Intelligence

Germany Offshore Wind Energy Market size in 2026 is estimated at 12.41 gigawatt, growing from 2025 value of 10.25 gigawatt with 2031 projections showing 32.27 gigawatt, growing at 21.06% CAGR over 2026-2031.

Capacity growth aligns with the national target of 30 GW by 2030, rising corporate power-purchase agreements, and a steady fall in levelized cost as 14 MW-plus turbines become mainstream. Deeper collaboration between federal and state agencies accelerates permits, while pilot projects that link offshore wind with electrolyzers signal a shift toward integrated energy systems. Supply-chain limits around heavy-lift vessels still cap build-out speed, yet digital-twin maintenance tools are lowering unplanned downtime and lifting project returns. Taken together, these drivers position the German offshore wind energy market for sustained double-digit expansion through the decade.

Key Report Takeaways

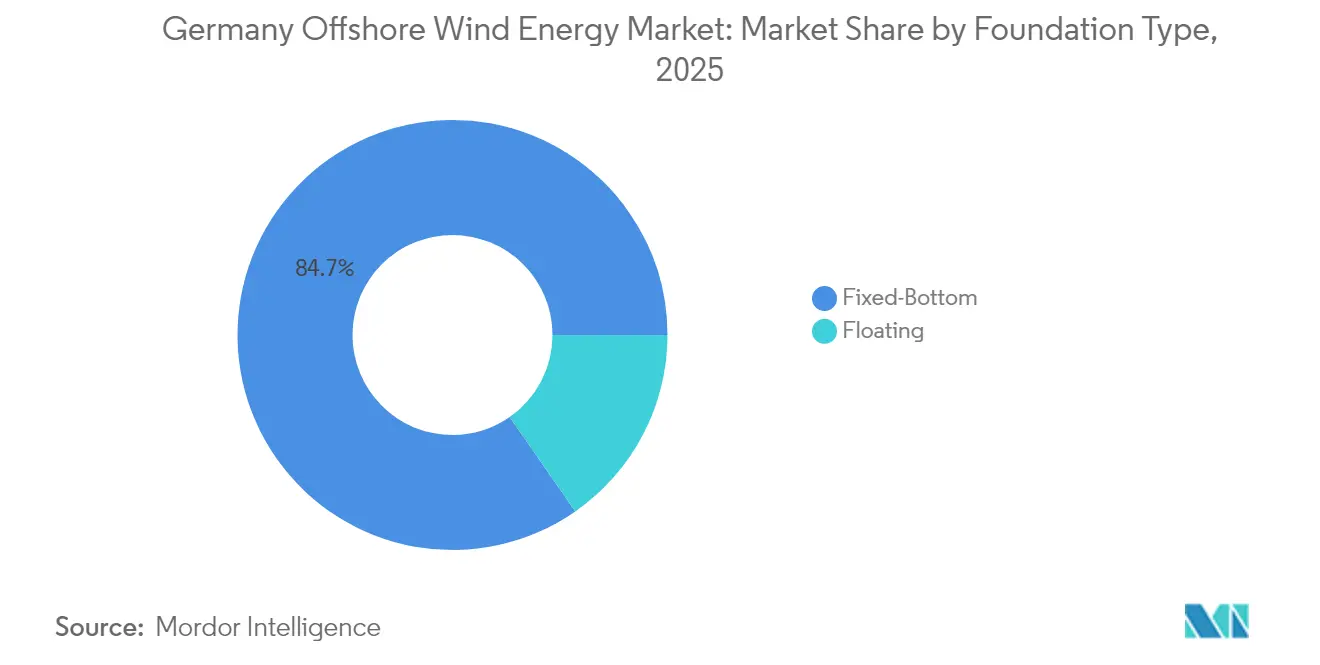

- By foundation type, fixed-bottom structures captured 84.68% of the German offshore wind energy market share in 2025, while floating foundations are forecast to expand at a 25.41% CAGR through 2031.

- By turbine capacity, units with a capacity above 6 MW held 74.12% of the German offshore wind energy market size in 2025 and are projected to grow at a 22.15% CAGR between 2026 and 2031.

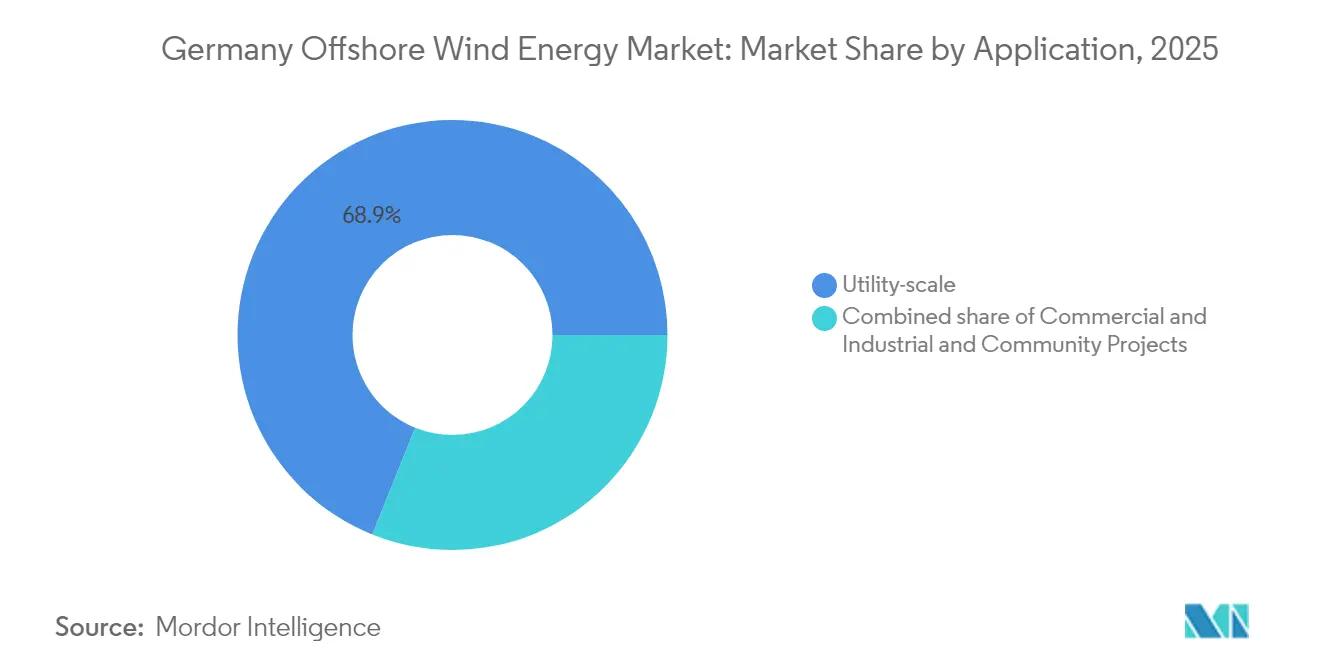

- By application, utility-scale projects accounted for 68.92% of the German offshore wind energy market size in 2025, whereas community projects are advancing at a 28.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Offshore Wind Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated 40 GW-by-2034 target | +4.2% | National, North Sea and Baltic expansion zones | Medium term (2–4 years) |

| Falling LCOE from 14–15 MW turbines | +3.8% | National, early adoption in shallow-water North Sea sites | Short term (≤ 2 years) |

| Corporate PPA boom | +4.1% | National, heavy-industry clusters across western and southern states | Short term (≤ 2 years) |

| Offshore wind-to-hydrogen pilot tenders | +2.9% | North Sea pilot zones near Heligoland | Long term (≥ 4 years) |

| Federal-state Area Development Plan timetable | +3.5% | National, coordinated seabed scheduling | Medium term (2–4 years) |

| Digital-twin O&M platforms | +2.3% | National, all operating and planned assets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Accelerated 30 GW-by-2030 National Target

The federal goal, doubled from its earlier pledge, obliges yearly additions near 3.1 GW, far above the sub-300 MW pace logged in 2023. The Federal Maritime and Hydrographic Agency has zoned precise build areas that let developers plan equipment orders and capital spending with more certainty.(1)Kelly MacGregor, “Three-Gigawatt Annual Build Needed to Hit 2030 Goal,” OilPrice, oilprice.com Faster permits and auction clarity are driving a queue of multi-gigawatt projects that will keep the German offshore wind energy market on its steep growth track. Companies are lobbying for quicker grid links so new capacity can feed demand centers in the south. Meeting the target cements Germany as Europe’s second-largest offshore arena, below only the United Kingdom.

Falling Levelized Cost from >14 MW Turbines

Rapid adoption of 14-15 MW turbines lifts output per foundation and trims array-cable runs. Siemens Gamesa’s SG 14-222 DD delivers 25% more annual energy than its 11 MW predecessor.(2)Siemens Gamesa, “SG 14-222 DD Fact Sheet,” siemensgamesa.com Fraunhofer ISE pegs 2024 LCOE at 5.5-10.3 €c/kWh, putting offshore wind on par with gas-fired power in Germany. Developers favor bigger rotors because fewer units cut crane days and vessel charters, two of the priciest items in a build budget. The trend protects margins as zero-subsidy bids become common in the German offshore wind energy market.

Federal-State North Sea–Baltic “Area Development Plan 2023” Build-out Timetable

The plan coordinates seabed leasing, environmental checks, and grid-connection studies under one schedule, replacing past patchwork rules. Uniform data sets on wind speeds and seabed conditions save developers costly surveys. Pipeline visibility also gives tier-two suppliers confidence to scale factory output. Resulting efficiencies are expected to lift the German offshore wind energy market by unlocking stranded projects and shortening lead times for new zones.

Corporate PPA Boom Among German Heavy Industry

BASF, Covestro, and Amazon have signed decade-long PPAs that let projects secure debt on merchant terms. These contracts hedge power price risk for energy-intensive firms while furnishing fixed revenue for wind-farm owners. The maturing PPA market is cutting reliance on state subsidies, sparking a self-reinforcing cycle of demand and new builds in the German offshore wind energy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-connection queue and onshore bottlenecks | -3.7% | Schleswig-Holstein and Lower Saxony | Short term (≤ 2 years) |

| Lengthy maritime environmental permitting | -2.1% | Baltic Sea protected areas | Medium term (2–4 years) |

| Heavy-lift vessel and monopile scarcity | -2.8% | North Sea and Baltic supply chain | Medium term (2–4 years) |

| High interest-rate environment | -3.4% | National, all project-finance structures | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid-Connection Queue & Onshore Transmission Bottlenecks

TenneT curtailed 9% of North Sea output in 2024 due to cable congestion. The federal regulator forecasts that 500,000 km of new lines plus transformers will be needed by 2045. Delays inflate financing costs and dent capacity factors, holding back the German offshore wind energy market during a critical scale-up phase.

Heavy-Lift Vessel & Monopile Forging Scarcity

Only a handful of European yards forge XXL monopiles, and heavy-lift vessels that can raise 3,000-ton jackets are nearly booked out until late-2027.(3)DEME Group, “Heavy-Lift Vessel Market Outlook,” deme-group.com Competition for scarce assets risks slippage in project timetables and higher EPC prices, raising entry hurdles for smaller developers in the German offshore wind energy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foundation Type: Floating Technology Gains Despite Fixed-Bottom Dominance

Fixed-bottom structures represented 84.68% of the German offshore wind energy market in 2025, driven by shallow-water zones near Borkum and Sylt, where monopile costs average EUR 1.9–2.1 million per MW. RWE’s 300-monopile reservation with Steelwind secures capacity through 2027 but signals scarcity, as European mills run at 85% utilization. Supply tightness and steel price inflation could accelerate the adoption of floating if fabrication lead times extend beyond two years.

Floating foundations held 15.32% in 2025 and are forecast to grow at a 25.41% CAGR through 2031, supported by Baltic sites beyond the 50-meter isobath and the North Sea west of Heligoland. Although the capital cost remains EUR 2.8–3.4 million per MW, floating technology eliminates costly seabed dredging and expands the developable seabed by 40% in German waters. Upcoming Arkona Basin tenders include three floating-specific zones totaling 1.2 GW, expected to connect through BalWin 5 after 2030. As turbine ratings climb, floating platforms’ higher nameplate capacities could offset upfront cost premiums, sustaining momentum in the German offshore wind energy market.

By Turbine Capacity: Above-6 MW Platforms Consolidate

Above-6 MW turbines captured 74.12% of Germany's offshore wind energy market size in 2025 and will accelerate at a 22.15% CAGR through 2031. Projects such as Vattenfall's Nordlicht clusters utilize 107 Vestas 15 MW units, each delivering 80 GWh annually, and achieve a 56% capacity factor in North Sea conditions. Direct-drive technology reduces maintenance outlays to EUR 18 per MWh, compared with EUR 26 per MWh for geared 6–8 MW turbines.

The 3–6 MW segment fell to 18.42% in 2025, and no new sub-3 MW orders have been announced since 2019, effectively rendering that class obsolete. Factory capacity at Cuxhaven and Nakskov reaches 2.7 GW per year, but rising demand could potentially exhaust the supply by 2027, underscoring the need for further investment. IEC 61400-3-1 standard revisions now accommodate rotors up to 250 meters, which supports next-generation 18 MW designs and keeps the German offshore wind energy market on its technology-upgrade path.

By Application: Community Ownership Surges

Utility-scale ventures accounted for 68.92% of installed capacity in 2025, led by Ørsted’s Borkum Riffgrund 3 (913 MW) and EnBW’s He Dreiht (960 MW). Economies of scale keep all-in CAPEX at EUR 2.9–3.2 million per MW, but grid-fee inflation is narrowing margins. Integrated utilities continue to win the largest leases, yet community ownership models are proliferating under revised federal rules that award tender premiums for local equity.

Community projects held 22.20% in 2025 and are forecast to grow at a 28.31% CAGR, buoyed by Trianel’s 400 MW Borkum cooperative and BayWa r.e.’s Schönberg farm, which reserved 25% equity for residents. Retail capital lowers project WACC by 40 basis points and enhances social acceptance, a critical factor in permitting. Commercial and industrial direct-wire setups, at 8.88% in 2025, utilize dedicated turbine clusters within utility projects, allowing off-takers to secure long-term green power. Together, these models diversify revenue streams and deepen resilience in the German offshore wind energy industry.

Geography Analysis

The North Sea remains the powerhouse of the German offshore wind energy market, supplying nearly three-quarters of installed capacity and benefiting from favorable wind speeds that push capacity factors above 50%. Recent completion of Borkum Riffgrund 3 and the start of He Dreiht construction illustrate how established port logistics, deeper water sites for larger turbines, and existing TenneT hubs reduce execution risk.

Baltic Sea prospects, although smaller in absolute terms, are scaling rapidly. The German offshore wind energy market size tied to Baltic projects is forecast to triple between 2025 and 2031 as Baltic Eagle and Arcadis Ost 1 unlock follow-up zones nearer to Hamburg’s industrial belt. Environmental assessments show lower marine-mammal sensitivity, which shortens permit reviews. The Baltic grid also allows shorter onshore reinforcement, cutting soft-cost overheads.

Inter-connector ambitions add a cross-border twist. Draft proposals envisage cable corridors that tie North Sea clusters with Danish and Dutch grids, while Baltic schemes link directly into Polish and Swedish lines. This emerging mesh will assist curtailment management and stabilize revenues across the German offshore wind energy market under higher renewable penetration scenarios.

Competitive Landscape

The market shows a moderate concentration profile anchored by five primary developers, Ørsted, RWE, Vattenfall, EnBW, and E.ON, holding a combined share near 60% of operational assets. Ørsted capitalizes on its serial project track record and early investment in digital-twin analytics that raise availability. RWE leans on domestic brand trust and cross-business hedging to secure PPAs with German heavy manufacturers.

Turbine manufacturing is essentially a two-horse race between Siemens Gamesa and Vestas, each locking in multi-farm framework deals that tilt bidding in favor of aligned developers. Siemens Energy’s 2023 move to take full control of Siemens Gamesa hints at tighter vertical integration that could compress costs on nacelles and service contracts. New entrants, chiefly oil-and-gas majors, must either overbid in capacity auctions or partner with experienced utilities to gain a foothold in the German offshore wind energy market.

Supply-chain bottlenecks remain a pivotal competitive lever. Firms that reserve heavy-lift vessel slots or monopile forging windows enjoy schedule certainty. Developers unable to guarantee logistics face financing penalties. Consequently, market power is drifting toward players capable of locking in end-to-end supply agreements early, reinforcing the consolidation pattern within the German offshore wind energy industry.

Germany Offshore Wind Energy Industry Leaders

Ørsted A/S

RWE AG

Vattenfall AB

EnBW Energie Baden-Württemberg AG

Siemens Gamesa Renewable Energy S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Ørsted completed turbine installation at Borkum Riffgrund 3 (913 MW), the largest German offshore farm to date.

- March 2025: Vattenfall reached the final investment decision for Nordlicht 1&2, totaling over 1.6 GW.

- March 2025: Ørsted’s Gode Wind 3 began commercial operations at 253 MW.

- April 2025: EnBW installed the first turbine at the 960 MW He Dreiht project.

Germany Offshore Wind Energy Market Report Scope

Offshore wind energy is clean and renewable energy obtained by taking advantage of the force of the wind that is produced on the high seas, where it reaches a higher and more constant speed than on land due to the absence of barriers.

The Germany Offshore Wind Energy Market is segmented by foundation type, Turbine Capacity, and Application. By foundation type, the market is segmented into fixed-bottom and floating. By turbine capacity, the market is segmented into up to 3 MW, 3 to 6 MW, and above 6 MW. By application, the market is segmented into utility-scale, commercial and industrial, and community projects. The market sizing and forecasts for each segment are based on gigawatts (GW) for all the above segments.

By Foundation Type

| Fixed-Bottom |

| Floating |

By Turbine Capacity

| Up to 3 MW |

| 3 to 6 MW |

| Above 6 MW |

By Application

| Utility-scale |

| Commercial and Industrial |

| Community Projects |

By Component (Qualitative Analysis)

| Nacelle/Turbine |

| Blade |

| Tower |

| Generator and Gearbox |

| Balance-of-System |

| Others (Installation, Vessels, O&M) |

| By Foundation Type | Fixed-Bottom |

| Floating | |

| By Turbine Capacity | Up to 3 MW |

| 3 to 6 MW | |

| Above 6 MW | |

| By Application | Utility-scale |

| Commercial and Industrial | |

| Community Projects | |

| By Component (Qualitative Analysis) | Nacelle/Turbine |

| Blade | |

| Tower | |

| Generator and Gearbox | |

| Balance-of-System | |

| Others (Installation, Vessels, O&M) |

Key Questions Answered in the Report

How large is Germany’s offshore wind capacity today?

Installed capacity reached 12.41 GW in 2026 and is on track for 32.27 GW by 2031.

What is the expected growth rate through 2031?

Capacity is projected to expand at a 21.06% CAGR between 2026 and 2031.

Which foundation technology is gaining ground?

Floating foundations are forecast to grow at a 25.41% CAGR as deeper Baltic sites come to auction.

Why are corporate PPAs important?

Industrial PPAs lock in sub-EUR 0.08 per kWh pricing, reduce financing spreads by about 120 basis points, and secure up to 4.2 GW of capacity.

What challenges could slow the build-out?

Grid-connection queues, onshore transmission delays, and high interest rates collectively shave up to 3.7 percentage points off forecast CAGR.

Who are the leading developers?

Ørsted, RWE, Vattenfall, and EnBW collectively hold about 70% of operating capacity but face growing competition from Shell, BP, TotalEnergies, and Equinor.

Page last updated on: