Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 15.31 Billion |

| Market Size (2026) | USD 15.87 Billion |

| Market Size (2031) | USD 18.99 Billion |

| Growth Rate (2026 - 2031) | 3.66% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Luxury Goods Market Analysis by Mordor Intelligence

The German luxury goods market size is expected to grow from USD 15.31 billion in 2025 to USD 15.87 billion in 2026 and is forecast to reach USD 18.99 billion by 2031 at 3.66% CAGR over 2026-2031. As of 2024, apparel continues to be the top product category, though watches are becoming more popular with new designs and features. Women remain the main buyers, but interest among men is growing steadily. Additionally, the rise of online shopping is changing how luxury goods are sold, with digital platforms playing a major role in reaching customers. These trends show the market's ability to adapt while maintaining its focus on quality and exclusivity. The German luxury goods market is growing steadily as many consumers view luxury goods as valuable investments. This helps the market manage inflation while keeping prices high. Younger buyers are attracted to brands that emphasize digital-first strategies, sustainability, and exclusive limited-edition products. Meanwhile, older, wealthier consumers continue to appreciate the traditional craftsmanship and heritage offered by many luxury brands, ensuring broad appeal across different age groups. Luxury brands focus on creating high-quality and unique products by using careful design and production methods. This often includes handmade techniques, limited production, and premium materials like fine leather, precious metals, and gemstones.

Key Report Takeaways

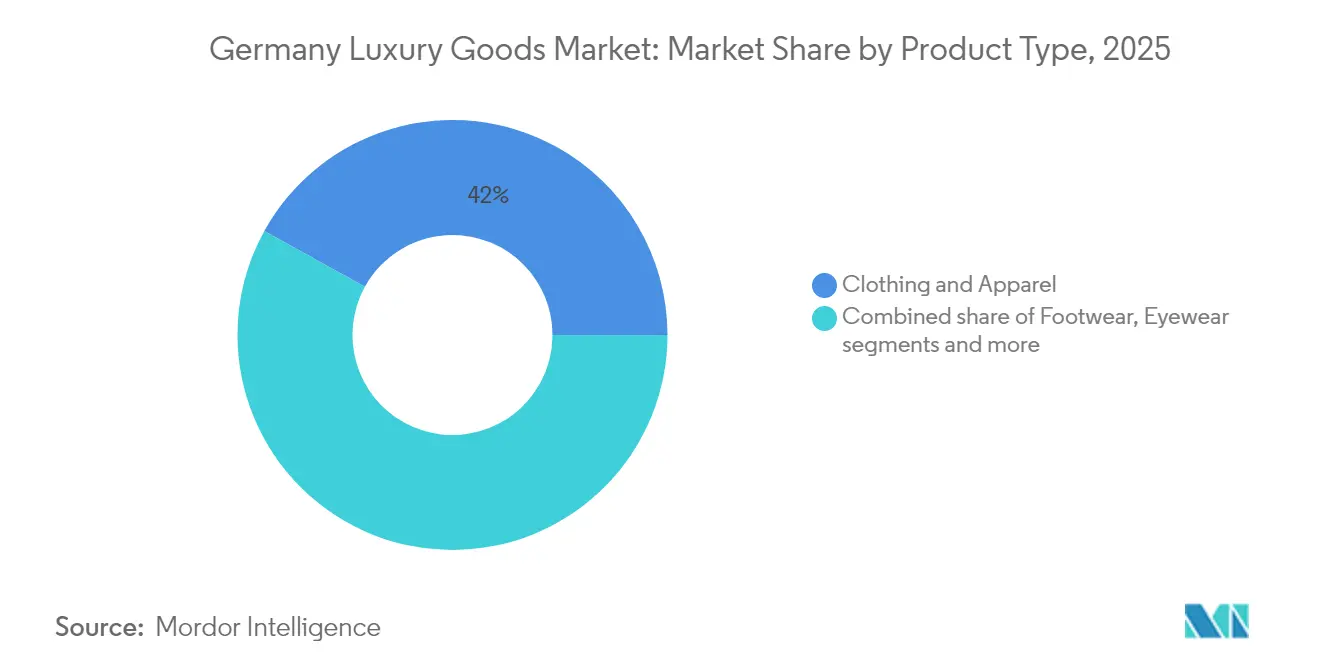

- By product type, clothing and apparel led with 41.97% of Germany luxury goods market share in 2025, while watches are forecast to advance at a 3.88% CAGR through 2031.

- By end user, women accounted for a 54.22% share of the Germany luxury goods market size in 2025, whereas the men’s segment is set to grow at 4.29% CAGR to 2031.

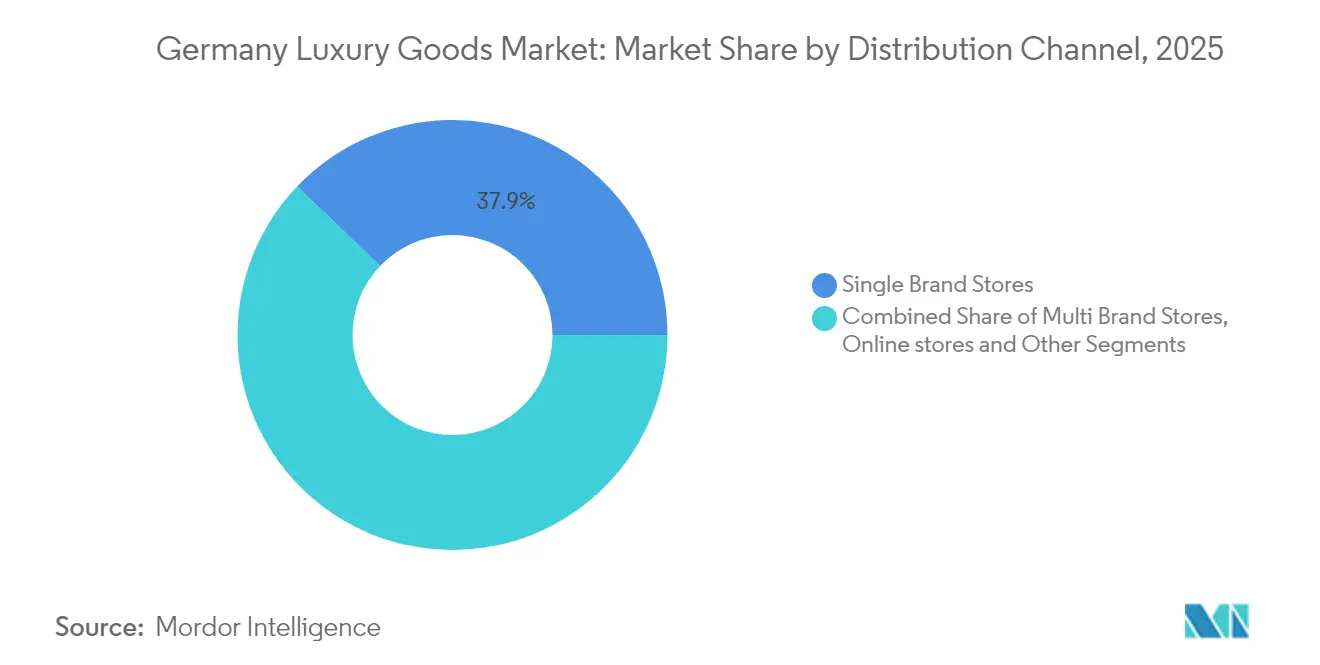

- By distribution channel, single brand stores held 37.86% revenue in 2025, yet online stores are advancing at a 4.77% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Luxury Goods Market Trends and Insights

Drivers Impact Table*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer shift toward sustainable and eco-certified luxury products | +0.8% | Germany, with spillover to DACH region | Medium term (2-4 years) |

| Influence of social media and celebrity endorsement | +0.6% | Strong resonance in German urban centers | Short term (≤ 2 years) |

| Consumers inclination towards limited edition products | +0.5% | Germany, particularly Berlin, Munich, Hamburg | Short term (≤ 2 years) |

| Product innovation in terms of raw material and design | +0.7% | Germany, leveraging engineering heritage | Medium term (2-4 years) |

| Rising disposable income and eealth accumulation in Germany | +0.4% | Germany, concentrated in Bavaria, Baden-Württemberg | Long term (≥ 4 years) |

| Growth of experience-based luxury and personalization services | +0.6% | Germany, with expansion to Austria, Switzerland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer shift toward sustainable and eco-certified luxury products

German consumers are increasingly prioritizing environmentally friendly products when making purchasing decisions. They are willing to spend more on items that use sustainable and circular production methods, as they see eco-certifications as a symbol of genuine luxury. Chanel’s newly launched Nevold platform, in June 2025, which incorporates recycled materials, showcases how luxury brands can secure limited resources while meeting growing consumer demands for sustainability. Furthermore, stricter regulations, such as the Corporate Sustainability Due Diligence Directive, are driving companies to enhance transparency in their supply chains [1]Source: European Commission, “Corporate Sustainability Due Diligence,” europa.eu. Brands that adopt sustainable practices early are gaining a significant advantage in the market. As a result, sustainability is becoming just as important as brand logos in representing status, enabling these brands to capture a larger share of the German luxury goods market.

Influence of social media and celebrity endorsement

Digital storytelling is quickly changing how luxury brands connect with customers in Germany’s high-end market. Hugo Boss’s partnerships with famous celebrities have been very successful. For example, the long-term collaboration with David Beckham started in Q3 2024 with the Fall/Winter campaign, while the Spring/Summer 2024 collection featured Gisele Bündchen. These celebrity campaigns, along with exciting events in Berlin, doubled social media engagement and reached 40 million livestream views. This led to a 6% increase in digital sales in Q3 and made digital channels contribute 19% of the company’s total revenue in 2023, with a 26% growth in Q4. Younger luxury shoppers in Germany are using digital platforms more often. These efforts have reduced the cost of attracting new customers and strengthened social proof, as digital storytelling combines celebrity influence, advanced technology, and event-based engagement into a seamless luxury experience.

Consumers’ inclination toward limited-edition products

Exclusivity is becoming a major factor in increasing the value of luxury goods in Germany. In 2024, brands focused on releasing exclusive, limited-edition products to create excitement among buyers and raise their selling prices, particularly in the watches and jewelry segments. For instance, Nomos Glashütte launched its Tangente 38 Date “Colour Rush” series at Watches & Wonders 2024. This collection featured 31 unique dial designs, with each design limited to just 175 pieces, making them highly exclusive and desirable. Similarly, MeisterSinger celebrated its 20th anniversary by introducing the Enamel 1Z Edition, a rare and sought-after product limited to only 24 handcrafted units, further emphasizing its exclusivity. True rarity increases both the practical and social value of luxury items, while forced or fake scarcity can harm customer trust. German luxury buyers, who have a strong appreciation for craftsmanship and technical precision, are particularly attracted to limited-edition, collectible products. These items not only highlight exceptional artisanal skills but also carry a sense of heritage and exclusivity, making them even more appealing. This approach fits well with the preferences of German consumers and allows brands to maintain exclusivity, increase sales, and avoid problems like overproduction or excess inventory.

Product innovation in raw material and design

Material science is playing a key role in helping brands stand out in Germany’s luxury goods market. In 2024, Hugo Boss made significant progress in its sustainability journey by introducing HeiQ AeoniQ, a plant-based, high-performance fiber [2]Source: Hugo Boss AG, “Hugo Boss Invests in a Sustainable Apparel Technology,” Hugo Boss Group, group.hugoboss.com. This innovative material is designed to replace polyester by 2030 and is already being used in some of their sneakers, polo shirts, and outerwear. This development shows that it is possible to create eco-friendly materials without compromising on the quality and luxury that customers expect. Consumers today are increasingly looking for products that are not only high-quality but also environmentally responsible. By adopting such materials, brands are addressing this demand while maintaining the high standards of German craftsmanship and engineering. Additionally, by openly sharing these advancements, brands are reinforcing Germany’s reputation for precision and quality while aligning with the modern focus on sustainable luxury. This approach builds stronger trust with consumers in a market where sustainability and innovation are becoming critical factors in purchasing decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of counterfeit products | -0.4% | Germany, with cross-border e-commerce challenges | Short term (≤ 2 years) |

| Lesser demand from price sensitive consumers | -0.6% | Germany, particularly affecting mid-luxury segments | Medium term (2-4 years) |

| Economic uncertainty and inflation impact on consumer spending | -0.5% | Germany, with broader European implications | Short term (≤ 2 years) |

| Stringent regulatory environment and compliance costs | -0.3% | Germany, setting precedent for EU-wide adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of counterfeit products

In Germany, counterfeit luxury goods are causing significant financial losses for brands, amounting to billions every year. Social media platforms like TikTok are making it easier for people to access fake luxury items, despite increased efforts by customs to seize these products. For instance, in late 2023, customs officials at Frankfurt Airport confiscated 2,164 counterfeit luxury watches from a shipment originating in Hong Kong. If these items had been genuine, their value would have been around EUR 170 million. Counterfeit goods not only harm the exclusivity of luxury brands but also confuse customers about pricing and reduce trust in authentic products. To tackle this issue, luxury brands in Germany are turning to advanced technologies. Hugo Boss, for example, introduced NFC tags in its 2024 ski-jacket collection. These tags are linked to blockchain-based digital authentication, allowing customers and officials to verify the product's authenticity instantly. These passports enhance traceability and make it harder for counterfeiters to tamper with products. While these technological solutions help protect brand reputation and reassure customers, they also come with challenges. Implementing such measures increases operational costs, adds complexity to processes, and can slow down the introduction of new products in Germany’s luxury market.

Economic uncertainty and inflation impact on consumer spending

In May 2025, Germany's inflation rate, as gauged by the year-on-year change in the consumer price index (CPI), rose to +2.1%, as reported by the German Federal Statistical Office [3]Source: Statistisches Bundesamt (Destatis), “Inflation Rate in May 2025 Remains at 2.4%," destatis.de. This inflationary rise has tightened household budgets, curbing discretionary spending and altering consumer priorities. Middle-income Germans are now adopting a more conservative financial stance, delaying non-essential purchases and leaning towards premium yet accessible alternatives. Their choices reflect a pragmatic adaptation to economic strains; luxury has shifted from being merely aspirational to a privilege contingent on financial stability. On the other hand, high-net-worth individuals, largely shielded from cost-of-living pressures, are intensifying their acquisitions, seeking both cultural significance and asset durability. Items like limited-edition timepieces, investment-grade jewelry, and heritage fashion are increasingly recognized as valuable assets. This trend is accentuating the divide in Germany’s luxury market: while price-sensitive buyers pull back, elite consumers are driving demand for rarity, craftsmanship, and long-term value appreciation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Apparel Dominance Faces Watch Innovation

In 2025, clothing and apparel dominated Germany's luxury goods market, claiming a 41.97% share. This was buoyed by a diverse price range and a consumer base known for its fashion-forward and quality-centric mindset. Demand prominently revolves around elevated wardrobe staples and everyday premium basics, emphasizing sustainability and sophisticated tailoring. Take, for example, Cologne's Armedangels. This label has carved a niche with its minimalist capsule collections, using organic cotton and recycled fabrics. Meanwhile, Berlin Fashion Week's high-impact couture not only amplifies brand desirability but also underscores cultural relevance. This is particularly true for maisons that collaborate with local artisans from Metzingen, Munich, and Berlin.

Furthermore, watches are carving out a prominent niche in Germany's luxury landscape, boasting a projected CAGR of 3.88% through 2031. Increasingly, consumers view these timepieces not just as accessories but as long-term value assets. This evolving perspective has led collectors to regard mechanical watches more as vehicles of tangible wealth than mere ornaments. A testament to this trend, Rolex has made a bold move with a CHF 1 billion investment in a new Swiss manufacturing facility, slated to commence operations by 2029. This decision highlights Rolex's strategic alignment with global demand, pressures from waitlists, and the imperative to boost capacity while maintaining its exclusivity. Meanwhile, German watchmakers in Glashütte, like A. Lange & Söhne and Glashütte Original, are capitalizing on this momentum. They're doubling down on their storied legacies, emphasizing limited annual outputs and intricate in-house movements. Such attributes continue to draw collectors who value rarity, craftsmanship, and lasting worth

By End User: Men Drive Growth in Women-Dominated Market

Women contributed 54.22% of the German luxury goods market size in 2025, driven by higher engagement with fashion, accessories, and experiential gifting. German women are driving the move toward sustainability and convenience. Brands are offering beauty subscriptions designed for eco-conscious customers. In-store strategies, such as styling lounges, wellness events, and mentorship dinners, help build loyalty by providing meaningful experiences along with product interaction. Collaborations with artists and designers, like the limited-edition beauty box launched in Berlin featuring designs by a local illustrator, have turned shopping into a culturally engaging experience.

Male demand is accelerating at a 4.29% CAGR, helped by evolving grooming standards and elevated casualwear. Hugo Boss has been at the forefront with sportswear partnerships that introduce tailored technical fabrics into hybrid work-leisure lines, such as its 2024 Hugo Blue denim-technical joggers collection and ski-inspired softshell shirts. Contemporary male consumers, particularly young professionals, view high-end sneakers, premium skincare routines, and even high-complication mechanical watches as markers of personal success. This upward trend is expanding category breadth and boosting average basket size in the Germany luxury goods market.

By Distribution Channel: Digital Transformation Accelerates

In 2025, single-brand stores captured 37.86% of Germany's luxury goods market, owing to their knack for offering immersive experiences and upholding high service standards. Flagship boutiques on Munich’s Maximilianstraße and Frankfurt’s Goethestraße transcend mere retail; they curate brand narratives steeped in heritage, artistry, and exclusivity. Brands such as Berluti, Cartier, and Louis Vuitton amplify in-store engagement with rotating exhibitions like Berluti’s leather craftsmanship showcase in Frankfurt and exclusive events, including designer meet-and-greets, invitation-only art shows, and cocktail evenings. Many flagship stores boast VIP salons and personalized styling lounges, enabling loyal clients to preview collections privately. This not only deepens emotional ties to the brand but also justifies their premium pricing.

Online luxury retail is on the rise, projected to grow at a 4.77% CAGR through 2031. To navigate this digital evolution, brands are pushing boundaries beyond conventional e-commerce. Take Hugo Boss: in mid-2024, they launched HUGO BOSS XP, a Web3-enabled loyalty program. Shoppers earn NFT-based tokens, HUGO XP and BOSS XP, through purchases or store visits. These tokens grant access to personalized styling, exclusive digital collectibles, luxury concierge services, and early peeks at limited-edition drops. By merging tangible experiences with digital perks, Hugo Boss is cultivating loyalty and community, catering to a new wave of digitally-savvy luxury consumers.

Geography Analysis

Southern Germany is a major contributor to luxury spending in the country, especially in regions like Bavaria and Baden-Württemberg. These areas are economically strong, with many automotive engineers, tech entrepreneurs, and owners of small and medium-sized businesses. Luxury retailers here benefit from customers who spend more on average, making it an attractive market for global luxury brands. Munich’s shopping streets are often compared to Milan’s high-end Quadrilatero district, while Stuttgart’s closeness to Porsche and Mercedes-Benz factories ensures a steady demand for premium leather goods and luxury watches.

Northern Germany, with cities like Hamburg and Berlin, adds creativity and innovation to the luxury market. Hamburg’s maritime history influences its fashion trends, attracting wealthy individuals from the shipping industry who invest in luxury yacht accessories and high-end Swiss watches. Berlin, on the other hand, is known for its cutting-edge fashion and focus on sustainability. Many brands test eco-friendly materials and circular business models, such as leasing luxury items, in Berlin’s concept stores. The city’s growing population of young professionals and digital nomads has also boosted demand for unique luxury experiences, including gourmet events and collaborations between streetwear and luxury brands.

Western Germany benefits from Frankfurt’s role as a financial hub, which drives demand for luxury goods. Bankers and consultants in the region often purchase high-value items like investment-grade jewelry and custom-tailored suits, with many making these purchases at Frankfurt Airport, a major hub for luxury travel retail. The region’s strong logistical connections to neighboring countries like Luxembourg, Belgium, and the Netherlands make it easier to deliver products quickly and efficiently. Additionally, Germany’s high e-commerce penetration, ranked third globally, supports the luxury market through urban click-and-collect centers and flexible return policies.

Competitive Landscape

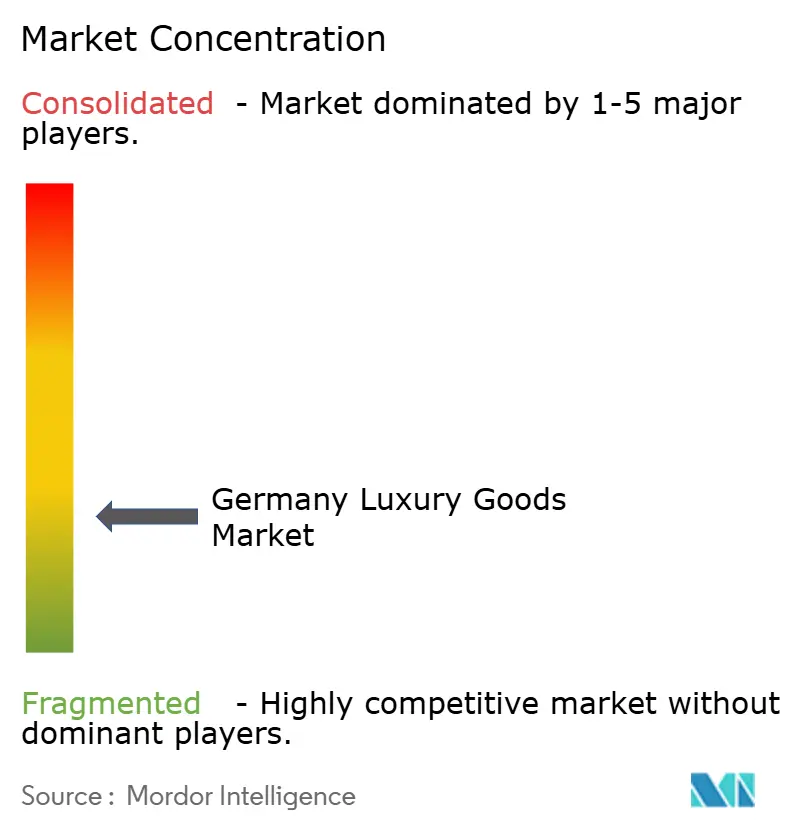

The German luxury goods market is fragmented, with global giants, regional players, and innovative newcomers. Major global companies like LVMH, Kering, and Richemont focus on establishing a strong presence in key cities such as Munich, Düsseldorf, and Cologne by investing in high-street stores. At the same time, they are enhancing their online platforms to offer personalized shopping experiences, catering to the growing demand for convenience and customization. Regional brands like Hugo Boss leverage their rich German tailoring heritage to stand out in the market. They are also adopting sustainable practices, such as using circular fabrics and advanced 3D design tools, to align with strict environmental and social governance (ESG) standards. These efforts not only meet regulatory requirements but also appeal to environmentally conscious consumers who value sustainability in luxury products.

Hugo Boss builds on its German tailoring roots with sustainability-driven innovations such as circular fabrics and 3D digital design. Its Pre-Loved resale program also reflects the growing market demand for responsible luxury. Boutique German labels stand out with eco-conscious materials, artisan collaborations, and small-batch production models, offering consumers a rich blend of classic and contemporary luxury.

Technology and sustainability are now central forces shaping the market. Brands in Germany increasingly adopt digital product passports using QR codes and NFC to verify authenticity and product history, in line with the EU’s incoming 2026 digital passport requirements. Richemont’s German operations also use AI-enabled servicing reminders to enhance after-sales care for luxury watches. In parallel, German start-ups are pioneering innovative materials from bio-fabricated leathers to lab-grown diamonds, reflecting the younger generation’s growing demand for sustainable luxury. Partnerships with local universities and manufacturing hubs further support material innovation and environmental responsibility across the product lifecycle.

Germany Luxury Goods Industry Leaders

-

Kering SA

-

LVMH Moët Hennessy-Louis Vuitton SE

-

HUGO BOSS AG

-

Hermès International SA

-

Compagnie Financière Richemont SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Hugo Boss entered the winter sports market with the launch of a premium skiwear range. The collection combined technical performance with contemporary design, targeting affluent consumers drawn to alpine fashion and luxury experiences. This move aligned with a broader industry trend of luxury brands investing in niche activewear categories to diversify their product portfolio.

- March 2024: German e-commerce giant Zalando expanded its designer shopping experience, introducing a more curated platform for premium and luxury fashion. The update included elevated visual merchandising, personalized styling tools, and exclusive collaborations, aiming to attract high-value consumers and position Zalando as a serious player in the luxury e-commerce segment.

- February 2024: Frankfurt Airport unveiled plans for its new Terminal 3, aimed at redefining the shopping experience through a world-class retail environment. The terminal incorporated premium and luxury boutiques, interactive digital features, and experiential zones designed to elevate airport retail to match urban luxury shopping destinations.

- January 2024: A German luxury brand unveiled the NUBIAN handbag, a futuristic vegan accessory available in two exclusive holographic finishes, grey and black. The handbag featured cutting-edge plant-based materials, combining innovative design with environmental responsibility. This launch highlighted the brand’s commitment to sustainability without compromising luxury, aligning with the growing demand among high-end consumers for cruelty-free, eco-conscious fashion.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we define the German luxury goods market as the annual retail value of new, premium-priced personal products, apparel, footwear, leather articles, jewelry, watches, and prestige beauty items sold to end consumers within Germany. These goods command price points well above the mass and bridge segments and convey craftsmanship, heritage, and exclusivity.

Scope Exclusion: Motor vehicles, yachts, wine and spirits, luxury hospitality experiences, and pre-owned goods lie outside this study.

Segmentation Overview

-

By Product Type

- Clothing and Apparel

- Footwear

- Eyewear

- Leather Goods

- Jewelry

- Watches

- Beauty and Personal Care

-

By End User

- Men

- Women

- Unisex

-

By Distribution Channel

- Single Brand Stores

- Multi Brand Stores

- Online Stores

- Other Distribution Channels

Detailed Research Methodology and Data Validation

Primary Research

We interviewed senior buyers at department stores, owners of high-street boutiques in Munich and Hamburg, managers of digital luxury platforms, and advisors who track high-net-worth shoppers across Europe. Their insights on purchase frequency, average selling prices, and the true share of online sales helped close gaps left by desk research and sharpen critical assumptions.

Desk Research

Our analysts first mapped demand and supply signals using tier-1 public repositories such as Destatis household expenditure tables, Eurostat retail trade indices, German Customs import flows for HS codes covering leather handbags and timepieces, and UN Comtrade jewelry data. Company filings lodged with BaFin, luxury brand annual reports, and shopping center leasing disclosures yielded store counts and sales densities. Respected business dailies and the German Fashion Council offered context on trend shifts and regulatory talks.

Depth was added through paid datasets, D&B Hoovers for brand-level financials and Dow Jones Factiva for curated news on flagship openings and pop-up trials.

The sources cited here are illustrative; numerous additional references informed data collection, validation, and clarification.

Market-Sizing & Forecasting

We begin with a top-down reconstruction of domestic consumption that melds retail trade receipts, import values net of re-exports, and tourist VAT refund tallies; outputs are then cross-checked through a selective bottom-up roll-up of branded store networks and sample ASP × unit throughput. Key variables feeding the model include per capita disposable income, resident high-net-worth population, inbound leisure arrivals, luxury fashion price inflation, and e-commerce penetration. Forecasts are produced via multivariate regression blended with scenario analysis, allowing sensitivity tests around currency swings and discretionary spend cycles. Divergences between the two build approaches are moderated toward the more evidence-rich baseline.

Data Validation & Update Cycle

All figures pass multi-layer checks where analysts flag outliers against historic series, peer benchmarks, and live media signals. A senior reviewer signs off only after anomalies are resolved. Models refresh annually, with interim updates triggered by material events such as VAT changes, currency shocks, or major mergers.

Why Mordor's Germany Luxury Goods Baseline Commands Confidence

Published estimates often diverge because firms bundle unlike products, rely on sell-in instead of sell-through data, or roll forecasts forward without fresh fieldwork.

Our disciplined scope, multi-source model, and yearly refresh keep totals anchored in current market reality.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.31 B (2025) | Mordor Intelligence | - |

| USD 17.08 B (2025) | Global Consultancy A | Includes automobiles and pre-owned sales, inflating totals |

| USD 17.80 B (2024) | Global Consultancy B | Derives figures from global brand revenues, not German retail spend |

| USD 15.99 B (2024) | Industry Association C | Uses import statistics only, omitting online cross-border purchases |

The comparison shows that once scope creep and single-source dependence are removed, our balanced mix of official statistics, channel checks, and verified assumptions delivers a transparent, reproducible baseline decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the Germany luxury goods market in 2026?

The Germany luxury goods market is valued at USD 15.87 billion in 2026.

How fast is the Germany luxury goods market expected to grow?

The market is forecast to expand at a 3.66% CAGR and reach USD 18.99 billion by 2031.

Which product segment holds the largest Germany luxury goods market share?

Clothing and apparel led with 41.97% market share in 2025.

Which distribution channel is expanding quickest in the Germany luxury goods market?

Online stores are advancing at a 4.77% CAGR between 2026 and 2031, outpacing other channels.

Page last updated on: