Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 106.23 Billion |

| Market Size (2030) | USD 155.58 Billion |

| Growth Rate (2025 - 2030) | 11.21% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany E-commerce Market Analysis by Mordor Intelligence

The Germany e-commerce market stands at USD 106.23 billion in 2025 and is forecast to reach USD 155.58 billion by 2030, registering an 11.21% CAGR. Demand momentum comes from accelerated fiber roll-out, SEPA-friendly payment innovation, and sustained investor appetite for quick-commerce fulfilment capacity. Government spending of EUR 17 billion (USD 18.4 billion) on the Federal Gigabit Initiative, combined with Mittelstand digitalisation and rising smartphone penetration, is eroding the urban–rural digital divide while boosting conversion rates.[1]European Commission, “Germany’s Digital Strategy,” digital-strategy.ec.europa.eu Regulatory pressure on dominant marketplaces is opening space for specialised platforms, and financing rounds such as Flink’s USD 150 million raise point to continued capital support for last-mile innovation. Collectively, these tailwinds underpin resilient household spending online despite macro uncertainty, positioning the Germany e-commerce market for compound growth through 2030.

Key Report Takeaways

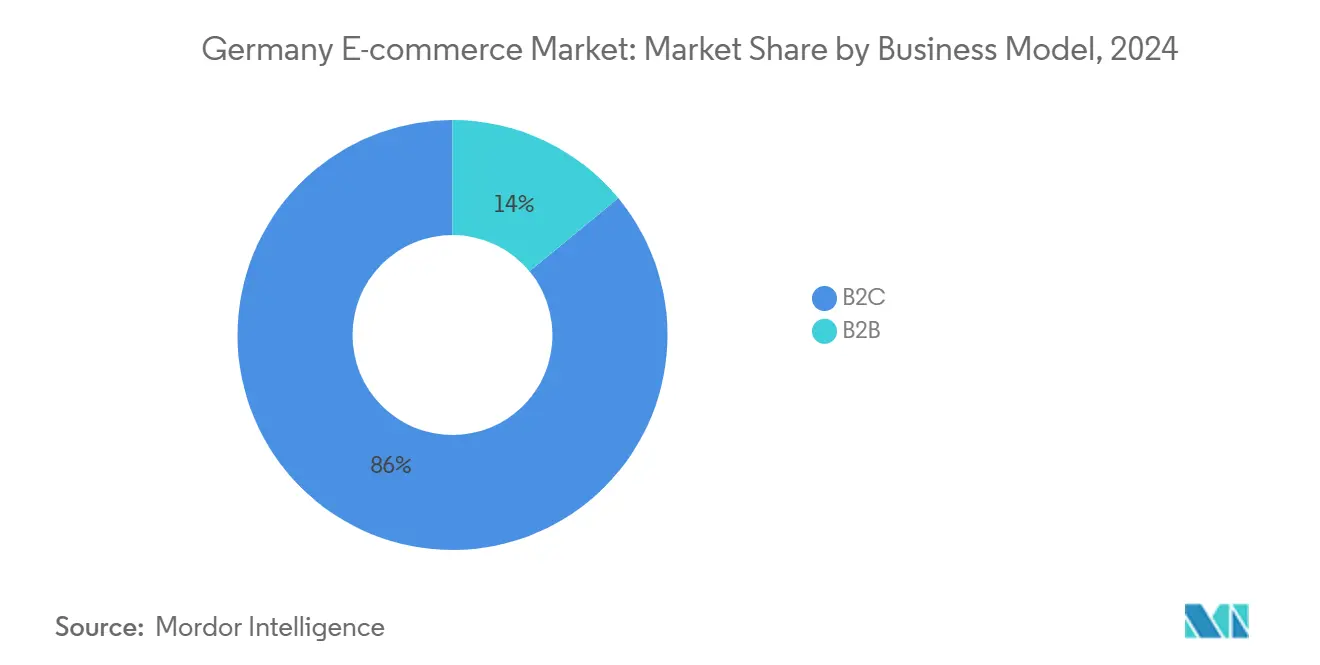

- By business model, B2C held 86% of the Germany e-commerce market share in 2024, while B2B is projected to expand at a 15.2% CAGR through 2030.

- By device type, smartphones captured 63% revenue share in 2024; the segment is forecast to grow at 11.5% CAGR to 2030.

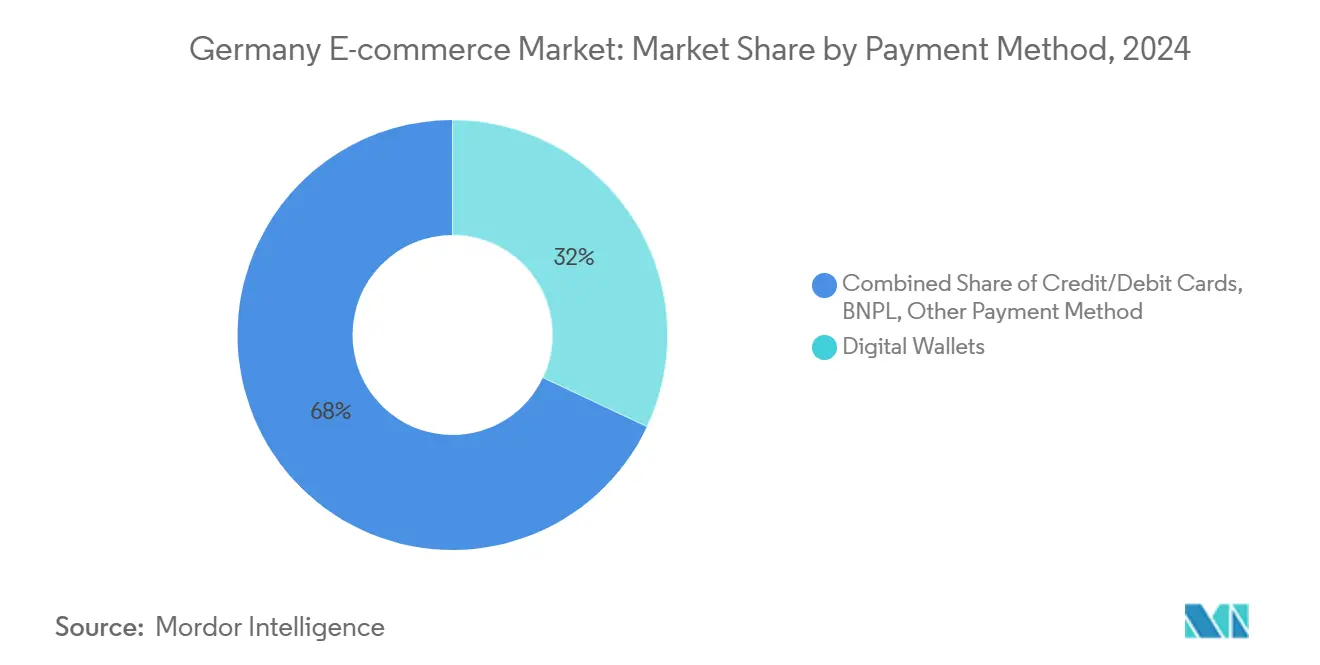

- By payment method, digital wallets commanded 32% share in 2024, whereas Buy Now Pay Later is advancing at a 17.9% CAGR over the same period.

- By product category, consumer electronics led with 23% revenue share in 2024; food & beverages is projected to post the fastest 16.3% CAGR through 2030.

Germany E-commerce Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of SEPA-friendly payment options fuels conversion rates | +2.1% | Germany, broader EU integration | Medium term (2-4 years) |

| Federal Gigabit Initiative widens rural high-speed coverage | +1.8% | Rural Germany, secondary cities | Long term (≥ 4 years) |

| Rise of quick-commerce start-ups drives same-day delivery demand | +1.5% | Urban centers, expanding to suburbs | Short term (≤ 2 years) |

| Digitalisation of Mittelstand procurement platforms (B2B) drives the market | +1.3% | Industrial regions, B2B corridors | Medium term (2-4 years) |

| Sustainability-driven preference for carbon-neutral shipping drives the market | +0.9% | Environmentally conscious demographics | Long term (≥ 4 years) |

Source: Mordor Intelligence

Expansion of SEPA-friendly payment options fuels conversion rates

SEPA integration has shifted shopper behaviour as digital wallets already account for 65% of domestic online transactions, displacing traditional bank transfers.[2]Noda Pay, “Wallet adoption in German e-commerce,” noda.live The 2024 launch of the Wero wallet delivers fee-free, bank-based payments and directly challenges PayPal’s 92.4% adoption, lowering cart abandonment that once stood at 27% when preferred options were missing. Merchants benefit from unified euro-denominated clearing across 36 countries, enabling cross-border growth without FX friction. Real-time open-banking transfers, valued at EUR 8.6 billion (USD 9.3 billion) by 2030, further compress processing fees. Improved authorisation rates lift gross merchandise value, sustaining the Germany e-commerce market’s double-digit expansion.

Federal Gigabit Initiative widens rural high-speed coverage

Only 40.3% of rural households enjoyed FTTH connections in September 2024, yet the EUR 17 billion (USD 18.4 billion) Gigabit Strategy targets 50% coverage by 2025.[3]DOT Magazine, “Gigabit roll-out status 2024,” dotmagazine.online EIB loans of EUR 415 million (USD 449 million) extend fibre to 500,000 remote homes, bringing video commerce and AR shopping to underserved regions. A legal “right to fast internet” commencing January 2025 assures minimum speeds, while a technology-neutral approach supports 5G fixed-wireless alternatives. As access converges with urban benchmarks, rural online spending intensity is catching up, enlarging the Germany e-commerce market over the long term.

Rise of quick-commerce start-ups drives same-day delivery demand

Quick-commerce has recalibrated from unsustainable 15-minute promises to profitable 90-minute and same-day windows. Flink’s USD 150 million Series C earmarks 30 hubs across Germany and the Netherlands to balance density with efficiency. Heritage retailers like CECONOMY integrate Uber’s courier network, cutting fulfilment to 90 minutes for electronics. Frankfurt-based Grovy channels EUR 3 million (USD 3.3 million) into eco-friendly operations, while consumer expectations settle on reliability over ultra-fast novelty. These operational refinements reduce logistics burn rates and reinforce adoption of the Germany e-commerce market in metropolitan corridors.

Digitalisation of Mittelstand procurement platforms (B2B) drives the market

Germany’s Mittelstand represents a EUR 1.7 trillion (USD 1.84 trillion) B2B e-commerce prospect as procurement goes online. Mandatory e-invoicing above EUR 250 (USD 270) from 2025 accelerates ERP upgrades. Industry 4.0 surveys show 95% of firms recognise digital potential and 60% have live applications. Marketplace revenues jumped 52% as unified catalogues cut sourcing time; Alstom’s partnership with 3D Spark yielded EUR 15 million (USD 16.2 million) in savings, underscoring hard ROI. Such cost efficiencies feed into price competitiveness and amplify the Germany e-commerce market’s expansion on the enterprise side.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compliance costs of VerpackG & recycling mandates hinders the market | -1.4% | National, affecting all e-commerce operators | Short term (≤ 2 years) |

| Last-mile labour shortages amid ageing workforce hinders the market | -1.1% | Urban logistics hubs, rural delivery routes | Medium term (2-4 years) |

| Bundeskartellamt scrutiny on dominant marketplaces hinders the market | -0.8% | Large marketplace operators, platform economy | Long term (≥ 4 years) |

Source: Mordor Intelligence

Compliance costs of VerpackG & recycling mandates hinders the market

VerpackG exposes sellers to fines up to EUR 200,000 (USD 216,000) for non-registration while obliging dual-system fees that strain thin e-commerce margins. The EU Packaging Regulation effective February 2025 forces 25% recycled plastic in bottles, climbing to 30% by 2030, compelling packaging redesign. Platform operators must audit suppliers via the LUCID register under extended producer responsibility, or risk sales bans. Compliance burdens fall hardest on SMEs, delaying entry and tempering the Germany e-commerce market’s overall CAGR in the near term.

Last-mile labour shortages amid ageing workforce hinders the market

Truck drivers and logistics specialists rank among the top 10 shortage occupations according to 2024 labour data. Demographic ageing intersects with rising parcel volumes; last-mile delivery already represents 50% of shipping emissions and the most labour-intensive cost node. New e-learning licences and recognition of Ukrainian qualifications provide incremental supply but cannot offset structural deficits. Wage escalation and subcontractor scarcity elevate delivery fees, marginally dampening the Germany e-commerce market growth outlook through 2028.

Segment Analysis

By Business Model: B2C Dominance Meets Rapid B2B Upswing

The B2C channel accounted for 86% of the Germany e-commerce market in 2024 as 84% of residents over 16 shopped online. Yet the B2B segment is pacing a 15.2% CAGR to 2030, propelled by procurement reforms among Mittelstand suppliers. Mandatory e-invoicing from 2025 necessitates digital interfaces, while platforms such as Unite’s Mercateo simplify sourcing and cut administrative friction. Mixed B2B/B2C formats unlock operational synergies, with REWE Group’s online revenue additions helping lift total sales to EUR 84 billion (USD 90.7 billion) in 2023.

Momentum should lift the Germany e-commerce market size for B2B transactions from a secondary share in 2025 toward parity later this decade as 90% of firms expect more than half of their purchases to be online by 2025. Growth also spills into export-oriented supply chains, reinforcing ERP integration and fostering data-driven contracting. The Germany e-commerce market share held by pure B2C players could narrow modestly as digital procurement scales across automotive, machinery, and chemicals corridors.

By Device Type: Smartphone-Led Purchasing Patterns

Smartphones generated 63% of Germany e-commerce market revenue in 2024 and will advance at an 11.5% CAGR through 2030. Mobile accounts for 63.67% of internet traffic, and 65.5 million residents engage in social-commerce discovery journeys. Enhanced biometric authentication and digital wallet acceptance further smooth checkout processes on smaller screens.

Desktop usage endures for high-value items and B2B ordering because large displays aid complex specification reviews. Smart TVs and voice assistants remain complementary, yet retailers are unifying inventories across devices so that cart contents synchronise seamlessly. As 5G penetration widens, richer video experiences bolster engagement rates, ensuring the Germany e-commerce market size captured via mobile keeps expanding while desktop value per transaction stays elevated.

By Payment Method: Wallets Gain Ground, BNPL Scales Fast

Digital wallets held 32% transaction share in 2024, underscoring a decisive shift away from cash and direct bank transfers. The Germany e-commerce market size associated with wallets is projected to scale alongside SEPA real-time rails, as Wero and PayPal compete on fee transparency. BNPL solutions, growing at 17.9% CAGR, resonate with German preferences for structured instalments, mitigating credit-card reluctance.

Debit card adoption will edge from 94.65% to 95.98% penetration by 2029, whereas credit cards remain under 10% because of debt-averse culture. Open banking reaches EUR 8.6 billion (USD 9.3 billion) in transaction value by 2030, giving merchants lower interchange routes and reinforcing data-driven loyalty targeting within the Germany e-commerce industry.

Note: Segment shares of all individual segments available upon report purchase

By Product Category: Electronics Command Value; Groceries Accelerate

Consumer electronics captured 23% revenue share in 2024 thanks to sustained demand for IT peripherals, smartphones, and wearables. Average basket sizes are high, cushioning logistics costs. Food & beverages, however, is expanding at 16.3% CAGR as quick-commerce widens cold-chain coverage and consumers prioritise convenience.

Fashion & apparel maintains large volumes but must juggle EU sustainability directives that call for circular practices. Beauty & personal care rides digital pharmacy growth, with the online pharmacy market moving toward USD 56.59 billion by 2030. Furniture returns remain a profitability drag; nonetheless, AR visualization tools and bundled return policies mitigate uncertainty. Collectively, these shifts reaffirm the diversified demand base underpinning the Germany e-commerce market.

Geography Analysis

Germany leads continental online retail by combining economic heft with deliberate infrastructure outlays; Amazon alone booked USD 37.3 billion in German-sourced revenue, second globally after the United States. The USD 18.4 billion Gigabit budget aims for 50% fibre coverage by 2025, placing Germany ahead of the EU-27 average though still behind Scandinavian benchmarks. SEPA’s 36-country sweep eliminates currency-conversion frictions, cutting abandonment rates by 27% whenever preferred payment choices are presented.

Urban nodes such as Berlin, Munich, and Hamburg host concentrated quick-commerce experimentation; Flink’s proposed 30 micro-fulfilment centres target these dense markets to compress delivery windows. North Rhine-Westphalia leads B2B platform adoption as its manufacturing heritage dovetails with OTT research networks, generating 73.4% of local marketplace revenue. Rural segments gain impetus from EUR 415 million (USD 449 million) in EIB loans earmarked for last-mile fibre, closing historic adoption gaps.

Regulatory leadership extends Germany’s influence across Europe; the Bundeskartellamt’s enhanced supervision of Amazon and Apple sets precedent for Digital Markets Act enforcement. Bilateral cooperation with the United States on AI and digital sovereignty further internationalises standards, while a USD 1.7 billion AI allocation channels funds into quantum computing and public-service digitalisation. These initiatives bolster the Germany e-commerce market’s attractiveness for foreign direct investment even as competition intensifies.

Competitive Landscape

The Germany e-commerce market features moderate concentration, with Amazon capturing well over half of online retail expenditure yet facing reinforced oversight since its designation as having “paramount significance for competition”. Zalando’s EUR 6.50 (USD 7.0) per share tender for ABOUT YOU is expected to close in summer 2025, unlocking EUR 100 million (USD 108 million) in annual synergies and raising group GMV by a forecast 5–10% CAGR to 2028. This consolidation strengthens local fashion positioning against Amazon and Shein.

Omnichannel integration remains a priority; Otto Group recorded EUR 15 billion (USD 16.2 billion) in revenue for 2025, crediting sustainability-linked packaging and carbon-neutral shipping for higher customer retention. CECONOMY’s alliance with Uber supports 90-minute delivery for electronics, with AI-infused demand forecasting helping lift FY 2024/25 sales to EUR 22.4 billion (USD 24.2 billion) and online revenue to EUR 5.1 billion (USD 5.5 billion).

White-space potential persists in B2B procurement where Unite, Mercateo and niche vertical platforms compete for Mittelstand wallet share. Quick-commerce differentiation hinges on sustainable economics rather than speed, evidenced by Flink’s move toward micro-hubs and Grovy’s culture-led positioning. Meanwhile, regulatory scrutiny over packaging and labour practices forces incumbents to invest in compliant processes, potentially raising barriers to entry and entrenching scale advantages for leading players within the Germany e-commerce market.

Germany E-commerce Industry Leaders

-

Amazon.de

-

eBay.de

-

eBay Kleinanzeigen

-

Idealo Internet GmbH

-

Otto GmbH and Co KG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2025: Zalando SE announced a public tender offer for ABOUT YOU at EUR 6.50 (USD 7.0) per share, a 107% premium, aiming for completion by summer 2025 pending antitrust clearance. The deal consolidates fashion GMV and should unlock marketing, logistics, and tech synergies.

- December 2024: EU Packaging Regulation received final approval, mandating 25% recycled plastic in bottles by 2025 and 30% by 2030, adding compliance urgency for e-commerce sellers.

- October 2024: CECONOMY expanded its 90-minute delivery partnership with Uber after online sales reached EUR 5.1 billion (USD 5.5 billion) and implemented AI demand-planning tools.

- September 2024: Flink raised USD 150 million in Series C funding to establish 30 distribution hubs, prioritising same-day delivery and path-to-profitability milestones.

- September 2024: Merck KGaA and Siemens agreed to deploy the Xcelerator platform for modular manufacturing, reducing time-to-market and capex across healthcare and electronics verticals.

Germany E-commerce Market Report Scope

E-commerce refers to the internet's commercial transaction of goods and services. These transactions are primarily conducted via various business models, such as B2C and B2B. E-commerce platforms offer advantages such as minimized inventory cost, improved profit margins, various discounts, hassle-free delivery of goods and services, etc.

The Germany E-commerce Market is Segmented into B2C E-commerce (Beauty and Personal Care, Consumer Electronics, Fashion and Apparel, Food and Beverage, Furniture and Home), and B2B E-commerce.

| By Business Model | B2C |

| B2B | |

| By Device Type | Smartphone / Mobile |

| Desktop and Laptop | |

| Other Device Types | |

| By Payment Method | Credit / Debit Cards |

| Digital Wallets | |

| BNPL | |

| Other Payment Method | |

| By B2C Product Category | Beauty and Personal Care |

| Consumer Electronics | |

| Fashion and Apparel | |

| Food and Beverages | |

| Furniture and Home | |

| Toys, DIY and Media | |

| Other Product Categories |

By Business Model

| B2C |

| B2B |

By Device Type

| Smartphone / Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method

| Credit / Debit Cards |

| Digital Wallets |

| BNPL |

| Other Payment Method |

By B2C Product Category

| Beauty and Personal Care |

| Consumer Electronics |

| Fashion and Apparel |

| Food and Beverages |

| Furniture and Home |

| Toys, DIY and Media |

| Other Product Categories |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the forecast value of the Germany e-commerce market by 2030?

The market is expected to reach USD 155.58 billion by 2030, reflecting an 11.21% CAGR.

Which business model is growing fastest in German online retail?

B2B commerce is expanding at a 15.2% CAGR as Mittelstand firms digitise procurement.

How dominant are smartphones in German online shopping?

Smartphones account for 63% of spending and will continue to outpace other devices at 11.5% CAGR.

What regulatory change most affects packaging for German e-commerce sellers?

The EU Packaging Regulation mandates 25% recycled plastic in bottles by 2025 and 30% by 2030.

Why is SEPA-friendly payment innovation important?

It cuts cross-border fees and lowers cart abandonment by offering familiar, fee-free euro payments.

How significant is quick-commerce in Germany’s delivery landscape?

It is shifting toward sustainable same-day models, with players like Flink investing in micro-hubs to enhance reach and profitability.

Page last updated on: June 23, 2025