Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

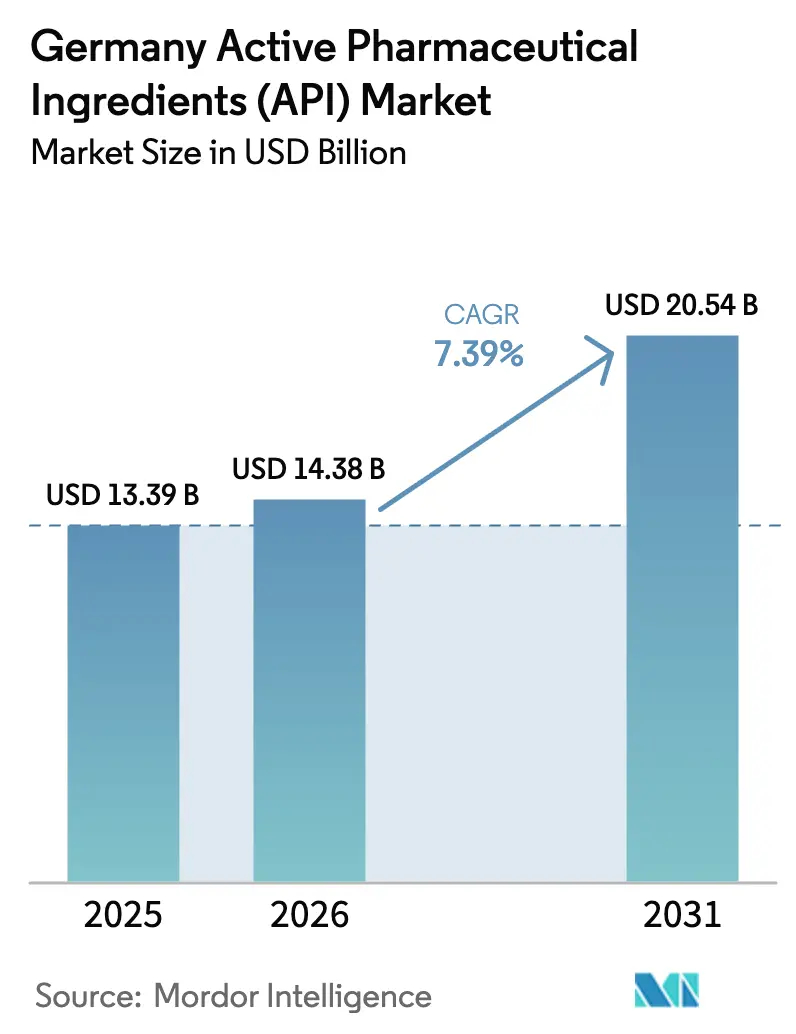

| Base Year Market Size (2025) | USD 13.39 Billion |

| Market Size (2026) | USD 14.38 Billion |

| Market Size (2031) | USD 20.54 Billion |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Active Pharmaceutical Ingredients (API) Market Analysis by Mordor Intelligence

The Germany active pharmaceutical ingredients market size was valued at USD 13.39 billion in 2025 and estimated to grow from USD 14.38 billion in 2026 to reach USD 20.54 billion by 2031, at a CAGR of 7.39% during the forecast period (2026-2031). Robust domestic demand for high-potency compounds, EU incentives that reward near-shoring, and sustained capital inflows into biologics hubs in Bavaria and Hessen underpin the upward trajectory. Leading multinationals have publicly committed multi-billion-dollar expansions that anchor long-term capacity, while continuous-flow manufacturing and digital-twin retrofits lift plant yields and reinforce the Germany active pharmaceutical ingredients market’s cost-competitiveness. At the same time, energy inflation and Asian price competition compress margins for standard small-molecule lines, steering manufacturers toward higher-value oncology and biologic niches. Overall, the Germany active pharmaceutical ingredients market benefits from a policy environment that prizes supply-chain security and environmental compliance, creating durable barriers to entrants that lack both technical depth and ESG credentials.

Key Report Takeaways

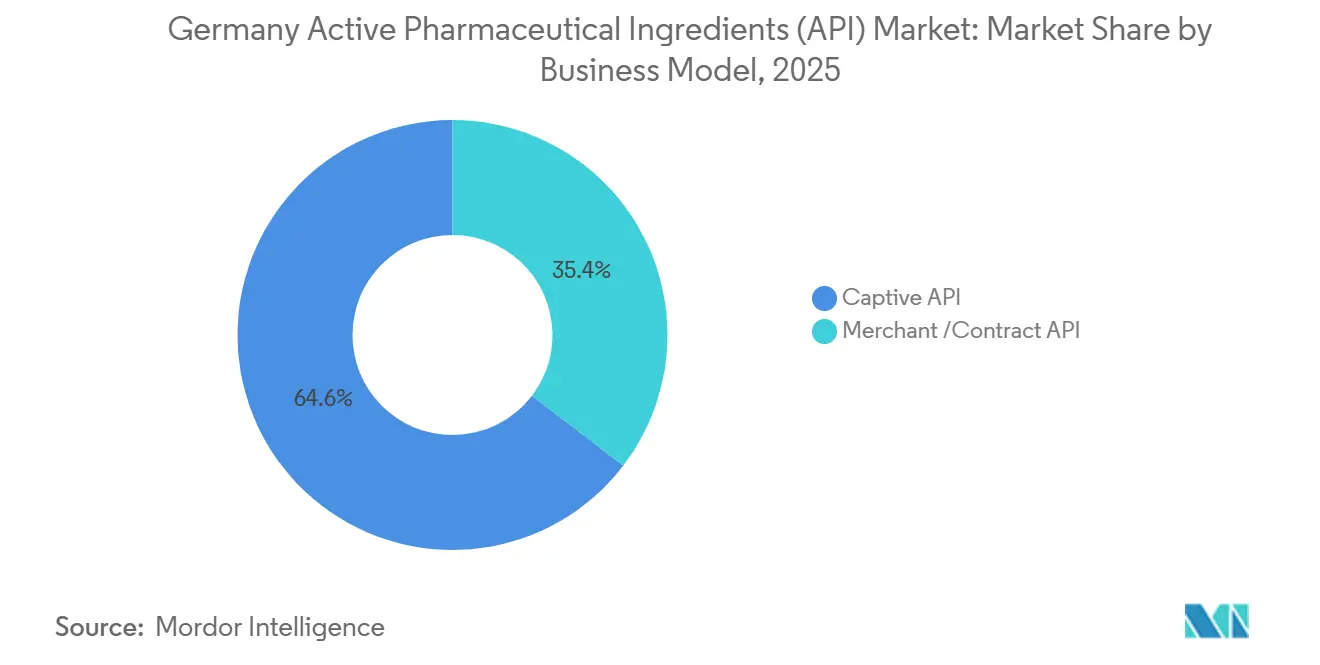

- By business model, captive production held 64.62% of Germany active pharmaceutical ingredients market share in 2025, whereas merchant APIs are advancing at a 7.78% CAGR through 2031.

- By synthesis type, synthetic compounds captured 69.74% revenue share in 2025; biotech APIs are expanding at a 7.86% CAGR to 2031.

- By molecule size, small molecules accounted for 67.85% of the German active pharmaceutical ingredients market size in 2025, while large-molecule therapeutics are growing at an 7.92% CAGR.

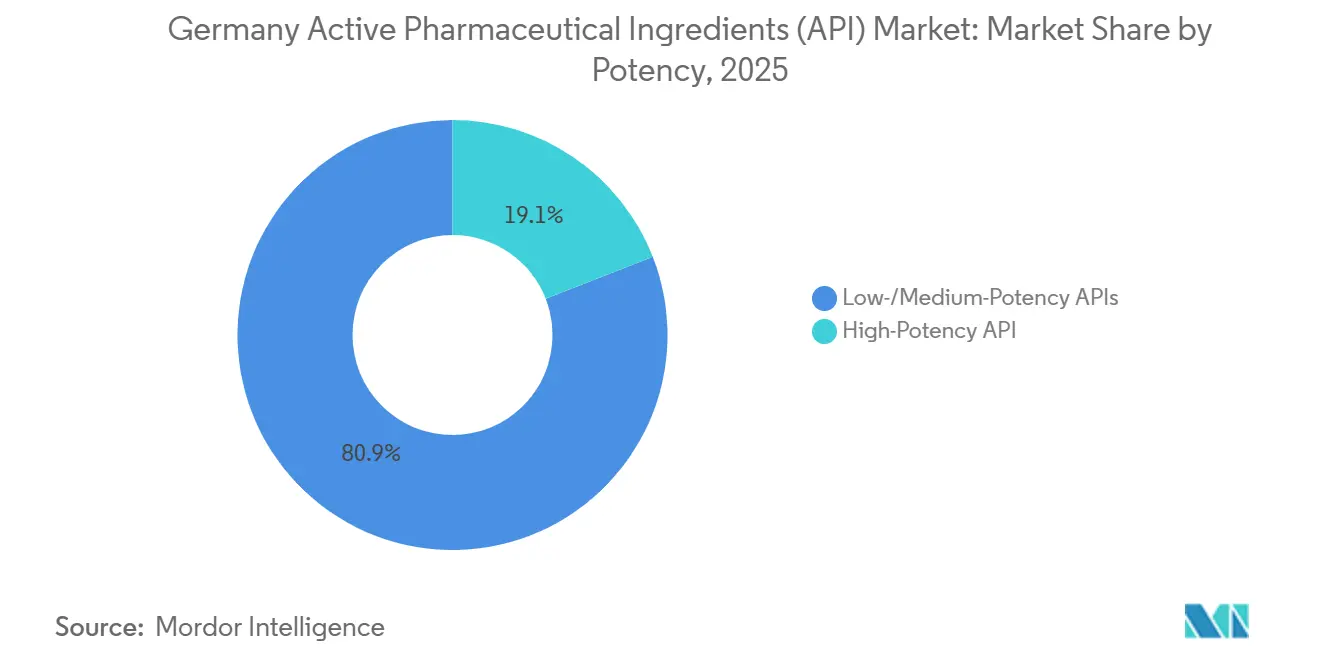

- By potency, low-to-medium-strength products represented 80.92% of demand in 2025; high-potency APIs are forecast to rise at an 8.00% CAGR through 2031.

- By therapeutic area, cardiovascular agents led with a 28.32% share of the Germany active pharmaceutical ingredients market size in 2025, and oncology APIs are advancing at an 8.07% CAGR.

- By end-user, pharma and biopharma companies commanded 71.98% of the Germany active pharmaceutical ingredients market share in 2025, whereas CDMOs/CMOs record the fastest CAGR at 7.83% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Active Pharmaceutical Ingredients (API) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust German Demand for High-Potency APIs Driven by Oncology Pipelines | +1.2% | Germany, with spillover to EU markets | Medium term (2-4 years) |

| EU-Level Incentives for Near-Shoring Critical APIs After COVID-19 Supply Shocks | +0.9% | Germany and broader EU region | Long term (≥ 4 years) |

| Rising Biotech Investment Clusters in Hessen & Bavaria Supporting Biologic API’s | +0.8% | Regional concentration in Hessen & Bavaria | Medium term (2-4 years) |

| Accelerated Adoption of Continuous-Flow Manufacturing In German CDMOs | +0.7% | Germany, with technology export potential | Short term (≤ 2 years) |

| Public Funding for "Green Chemistry" to Meet Stringent German ESG Norms | +0.6% | Germany, with EU regulatory influence | Long term (≥ 4 years) |

| Digital Twin/Industry 4.0 Retrofits Improving Yield at Legacy API Plants | +0.5% | Germany, with global technology transfer | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust German Demand for High-Potency APIs Driven by Oncology Pipelines

High-potency APIs (HPAPIs) now fetch premium pricing because their stringent containment requirements restrict global capacity. Lonza’s 30-year record in HPAPI containment illustrates how accumulated know-how becomes a moat. German producers replicate this strategy, leveraging oncology pipelines that now exceed 160 development projects across Bavarian biotech firms to lock in long-term contracts. The network effect of clustered oncology expertise lowers transaction costs and accelerates tech transfer, strengthening Germany’s grip on this complex, higher-margin slice of the Germany active pharmaceutical ingredients market.

EU-Level Incentives for Near-Shoring Critical APIs After COVID-19 Supply Shocks

The EU Critical Medicines Act earmarks EUR 80 million to trim reliance on Asian suppliers, a policy that disproportionately favors the Germany active pharmaceutical ingredient market because the country already hosts best-in-class GMP infrastructure. Heightened geopolitical risk, exemplified by China’s expanded Anti-Espionage Law, raises compliance uncertainty for European importers and tilts sourcing toward local plants. As inspectors face travel restrictions and legal exposure in Asia, German manufacturers command a “security premium” that cushions margin pressure.

Rising Biotech Investment Clusters in Hessen & Bavaria Supporting Biologic API’s

Bavaria’s 540 biotech companies secured EUR 910 million in 2024 financing, nearly double the prior year. Hessen complements this dynamism: BioSpring’s Offenbach RNA facility will be among the world’s largest and adds several hundred million euros in capacity. Physical proximity among research institutes, start-ups, and large plants fuels faster scale-up of biologic APIs, a segment growing nearly 8% annually within the broader Germany active pharmaceutical ingredient market.

Accelerated Adoption of Continuous-Flow Manufacturing In German CDMOs

Continuous-flow lines can lift yields 40% while cutting waste and energy use, aligning perfectly with Germany’s ESG targets. CordenPharma is integrating such systems into a EUR 900 million peptide build-out and has already locked in EUR 3 billion in multi-year GLP-1 contracts[1]Source: CordenPharma, “€900m Investment in GLP-1 Peptide Production,” cordenpharma.com. Early mover advantages materialize because continuous-flow installations require deep process-control expertise that most low-cost rivals still lack.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Natural-Gas & Electricity Costs Squeezing API Margins | -1.80% | Germany, with broader EU implications | Short term (≤ 2 years) |

| Intense Price Competition from Indian & Chinese Imports in Non-Protected Classes | -1.20% | Global, with particular pressure on German manufacturers | Medium term (2-4 years) |

| Complex Variation filing Requirements Under EU EMA & German BfArM | -0.70% | Germany and EU regulatory jurisdictions | Medium term (2-4 years) |

| Skilled-Labor Shortages in High-Containment Facilities | -0.50% | Germany, with spillover to specialized EU markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Natural-Gas & Electricity Costs

Natural gas supplies 30% of Germany’s base-chemical energy demand, so spikes in spot prices squeeze API margins hardest among energy-intensive lines. Sector-wide profit fell 12% between 2018 and 2024, prompting firms such as Chemische Fabrik Berg to conduct exhaustive energy audits. While solar and biomass retrofits are underway, short-term cash flow pressure may still compel some small plants to curtail production or refocus on premium HPAPIs that absorb cost inflation.

Price Competition from Indian & Chinese Imports

Imports cover 67% of API certificates registered in Europe, with Indian and Chinese suppliers dominating price-sensitive antibiotics and analgesics. German firms counter by doubling down on complex molecules and biologic niches, yet commoditized segments remain exposed. The availability of cheaper alternatives restrains the German active pharmaceutical ingredients market from passing the full burden of energy inflation to downstream formulators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Captive Dominance Underpins Supply Security

Captive operations represented 64.62% of 2025 revenue, underscoring big pharma’s preference for secure, vertically integrated supply chains. The Germany active pharmaceutical ingredient market size for captive lines equals USD 8.65 billion in 2025, and growth continues as companies internalize production of mission-critical compounds for oncology and diabetes. However, merchant lines are advancing at a 7.78% CAGR as CDMOs scale specialized capacity. CordenPharma’s EUR 900 million peptide program exemplifies this shift, allowing drug sponsors to flex capacity without fresh capital deployments. In the near term, captive and merchant models will coexist, with sponsors carving out non-core chemistries to external partners while shielding patented blockbusters.

Merchant providers thrive on deep GMP expertise, regulatory familiarity, and the ability to co-develop processes that compress time-to-clinic. By 2031, the merchant slice is projected to surpass USD 7.4 billion, reflecting Germany’s position as the EU’s regulatory gold standard. In addition, merchant lines attract SMEs developing orphan drugs that lack the scale to justify captive facilities. As the Germany active pharmaceutical ingredient market matures, dual-sourcing strategies that mix in-house and outsourced supply are likely to dominate risk-mitigation playbooks.

By Synthesis Type: Biotech APIs Re-Shape Manufacturing Paradigms

Synthetic molecules held 69.74% of spending in 2025, or roughly USD 9.34 billion of the Germany active pharmaceutical ingredient market size. Mature chemistries, process know-how, and sound sourcing of petrochemical precursors underpin this lead. Yet biotechnological APIs are expanding at a 7.86% CAGR, with mRNA, peptides, and viral vectors redefining factory footprints. Wacker’s USD 110 million mRNA hub in Halle can supply 200 million vaccine doses per year. Such assets accelerate the adoption of single-use bioreactors and advanced purification, skills not easily replicated elsewhere.

As biologics penetrate oncology, metabolic, and rare-disease pipelines, process skill sets transition from solid-phase synthesis to cell-culture optimization and chromatography. This transition pushes average selling prices upward, cushioning inflation in raw-material costs. By 2031, biotech APIs are on track to capture beyond 35% of Germany active pharmaceutical ingredient market revenue, gradually narrowing the historic gap with synthetic incumbents.

By Molecule Size: Large Molecules Drive Premium Growth

Small molecules still control 67.85% of sales or USD 9.08 billion in 2025. Their entrenched therapeutic reach in cardiovascular, CNS, and infectious diseases ensures stable baseline demand. Yet large-molecule biologics are expanding at an 7.92% CAGR, adding incremental USD 2.49 billion through 2031. Buffer-media build-outs such as Rentschler Biopharma’s Laupheim project illustrate the infrastructure scale required to underpin monoclonal and gene-therapy pipelines.

Higher structural complexity of biologics increases entry barriers and secures premium pricing. Furthermore, extended exclusivity periods delay generic erosion, offering a revenue hedge for plants willing to invest in stainless-steel fermenters and controlled environments. The Germany active pharmaceutical ingredient market share of biologics therefore, serves as a bellwether for the sector’s strategic pivot toward targeted therapies.

By Potency: HPAPIs Command Strategic Premiums

Conventional APIs account for 80.92% of volumes but just under 60% of dollar revenue because high-potency lines enjoy superior margins. HPAPI volumes expand at an 8.00% CAGR, outpacing the overall Germany active pharmaceutical ingredient market. New oncology candidates often require containment levels OEB 4-5, and German firms have already built segregated cleanrooms, negative-pressure suites, and automated powder transfer, deterring low-cost entrants.

Higher capital intensity raises switching costs for customers, encouraging long-term supply agreements that stabilize cash flows. This is especially critical as energy price volatility challenges cost planning. Expect HPAPIs to cross the 25% revenue threshold by 2031, further entrenching Germany’s role as the EU’s safest supplier of cytotoxic and hormonal actives.

By Therapeutic Area: Oncology Accelerates Market Evolution

Cardiovascular actives led with 28.32% revenue in 2025 on the back of mature statin and antihypertensive franchises, yet growth is plateauing. Oncology APIs, meanwhile, grow at 8.07% CAGR, adding USD 1.71 billion to the Germany active pharmaceutical ingredient market size by 2031. Over 30% of global R&D pipelines now target cancer, and Germany’s oncology clusters already host 160 projects.

Infectious disease, metabolic disorder, CNS, and respiratory APIs each contribute mid-single-digit growth, balancing portfolio exposure. Future upside comes from antibody-drug conjugates (ADCs), which marry biologic targeting with HPAPI warheads, a perfect fit for Germany’s dual strengths in biologics and containment

By End-User: CDMOs Capture Outsourcing Tailwinds

Direct pharma demand represented 71.98% of the Germany active pharmaceutical ingredient market in 2025. However, big sponsors increasingly outsource non-core synthesis, handing CDMOs a 7.83% CAGR runway. Proximity to EU regulators, strong IP protection, and deep talent pools enable German CDMOs to command premium price points versus Asian peers, especially for GMP batches used in phase-I/II trials.

CROs and academia make up a niche but critical segment for early-stage, low-volume runs, often enrolling the same CDMOs once compounds enter late-stage development. The blurred boundaries between clinical and commercial production further benefit service providers that offer cradle-to-launch capabilities, reinforcing Germany’s status as the one-stop shop for EU drug innovators

Geography Analysis

The Germany active pharmaceutical ingredient market benefits from a regulatory regime managed by BfArM and EMA that offers transparent timelines and mutual-recognition pathways, reducing compliance friction for exporters in neighboring states. Digital transformation grants and green-chemistry subsidies from the federal BMBF funnel public resources into plant modernization, magnifying private investment multipliers.

Southern clusters dominate biotech innovation. Bavaria’s superstar hub around Munich thrives on university-industry collaboration, contributing EUR 910 million in fresh capital during 2024 alone. Hessen leverages Frankfurt’s transport nodes and a dense chemical heritage; BioSpring’s RNA mega-plant and Sanofi’s EUR 1.3 billion insulin site anchor the local value chain. Northern Germany hosts Wacker’s mRNA center, giving the country a balanced geographic spread of modalities from peptides to nucleic acids.

Supply-chain security considerations further tilt EU procurement toward German facilities. Around 67% of API certificates still point to Asia, yet the EU’s draft Critical Medicines list prioritizes contracts with local producers, handing the Germany active pharmaceutical ingredient market a structural demand floor. The same incentives channel orphan-drug sponsors toward German CDMOs to de-risk launch timelines and align with ESG disclosure norms enforced across EU capital markets.

Competitive Landscape

The top five players hold an estimated less than half of Germany active pharmaceutical ingredient market revenue, indicating moderate concentration. Leaders such as Boehringer Ingelheim, Sanofi, and Bayer pursue vertical integration to secure supply but also license excess capacity to third parties, smoothing asset utilization. Investments skew toward biologics, HPAPIs, and peptide lines, all defensible against low-cost Asian supply.

Strategic differentiation hinges on manufacturing technology. Continuous-flow reactors, digital twins, and AI-based predictive maintenance underpin 30%-plus yield gains at retrofitted sites like Roche’s Mannheim diagnostics plant [SCiencedirect.com]. Meanwhile, green-chemistry pilots like BAM’s IMPACTIVE project show how mechanochemistry can slash solvent footprints, satisfying both regulators and ESG-minded investors.

Competition also intensifies via M&A. Fagron’s 2025 purchase of Euro OTC & Audor Pharma consolidates raw-material distribution and secures local market access. New entrants focus on mRNA and cell-therapy APIs, but must overcome capital hurdles, GMP training shortages, and the pending EU AI Act that will add algorithmic-validation steps to process controls.

Germany Active Pharmaceutical Ingredients (API) Industry Leaders

Teva Pharmaceutical Industries Ltd

Pfizer Inc.

Novartis AG

BASF SE

Merck KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Fagron Group closed its takeover of Euro OTC & Audor Pharma, becoming Germany’s second-largest raw-material supplier

- June 2024: Wacker inaugurated a USD 110 million mRNA competence center in Halle with capacity for 80 million vaccine doses per year

Germany Active Pharmaceutical Ingredients (API) Market Report Scope

An Active Pharmaceutical Ingredient (API) is a part of any drug that produces its effects. Some drugs, such as combination therapies, have multiple active ingredients to treat different symptoms or act in different ways. They are produced using highly technological industrial processes during the research and development and the commercial production phase.

The Germany active pharmaceutical ingredient (API) Market is Segmented by Business Mode (Captive API and Merchant API), Synthesis Type (Synthetic and Biotech), Drug Type (Generic and Branded), and Application (Cardiology, Oncology, Pulmonology, Neurology, Orthopedic, Ophthalmology, and Other Applications). The report offers the value (in USD billion) for the above segments.

By Business Model

| Captive API |

| Merchant / Contract API |

By Synthesis Type

| Synthetic API |

| Biotech API |

By Molecule Size

| Small-Molecule |

| Large-Molecule / Biologic |

By Potency

| High-Potency API |

| Low/Medium Potency API |

By Therapeutic Area

| Oncology |

| Cardiovascular |

| Infectious Diseases |

| Metabolic Disorders |

| CNS & Neurology |

| Respiratory |

| Others |

By End-User

| Pharma & Biopharma Companies |

| CDMOs / CMOs |

| CROs & Academia |

| By Business Model | Captive API |

| Merchant / Contract API | |

| By Synthesis Type | Synthetic API |

| Biotech API | |

| By Molecule Size | Small-Molecule |

| Large-Molecule / Biologic | |

| By Potency | High-Potency API |

| Low/Medium Potency API | |

| By Therapeutic Area | Oncology |

| Cardiovascular | |

| Infectious Diseases | |

| Metabolic Disorders | |

| CNS & Neurology | |

| Respiratory | |

| Others | |

| By End-User | Pharma & Biopharma Companies |

| CDMOs / CMOs | |

| CROs & Academia |

Key Questions Answered in the Report

What is the current value of the German Active Pharmaceutical Ingredients market?

The market is valued at USD 14.38 billion in 2026 and is projected to reach USD 20.54 billion by 2031.

Which segment is growing the fastest?

Oncology APIs lead with an 8.07% CAGR during the forecast period (2026-2031), fueled by expanding cancer drug pipelines and premium pricing.

How big is the captive production slice?

Captive operations hold 64.62% of 2025 revenue as firms prioritize supply security and IP protection.

Why are high-potency APIs important?

HPAPIs offer higher margins and entry barriers due to containment requirements, expanding at an 8.00% CAGR through 2031.

What role do CDMOs play in Germany?

CDMOs serve rising outsourcing demand, recording a 7.83% CAGR through 2031 by providing specialized capacity close to EU customers.

Page last updated on: