GCC Drone Pilot Training Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

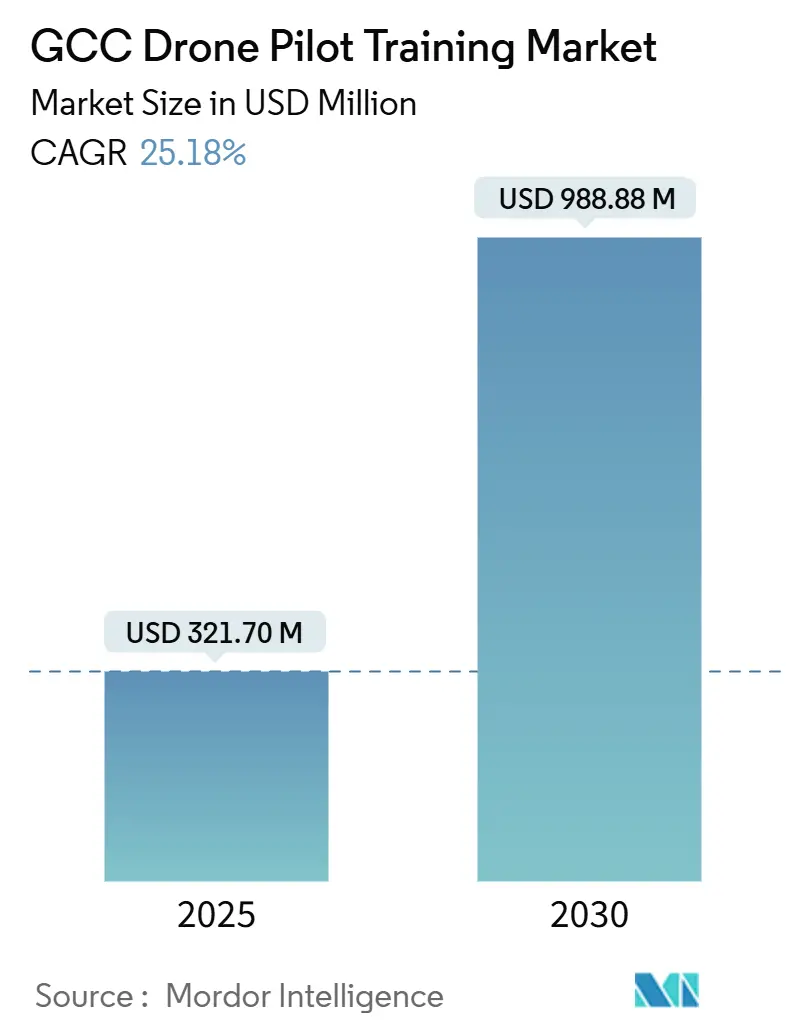

| Market Size (2025) | USD 321.70 Million |

| Market Size (2030) | USD 988.88 Million |

| Growth Rate (2025 - 2030) | 25.18% CAGR |

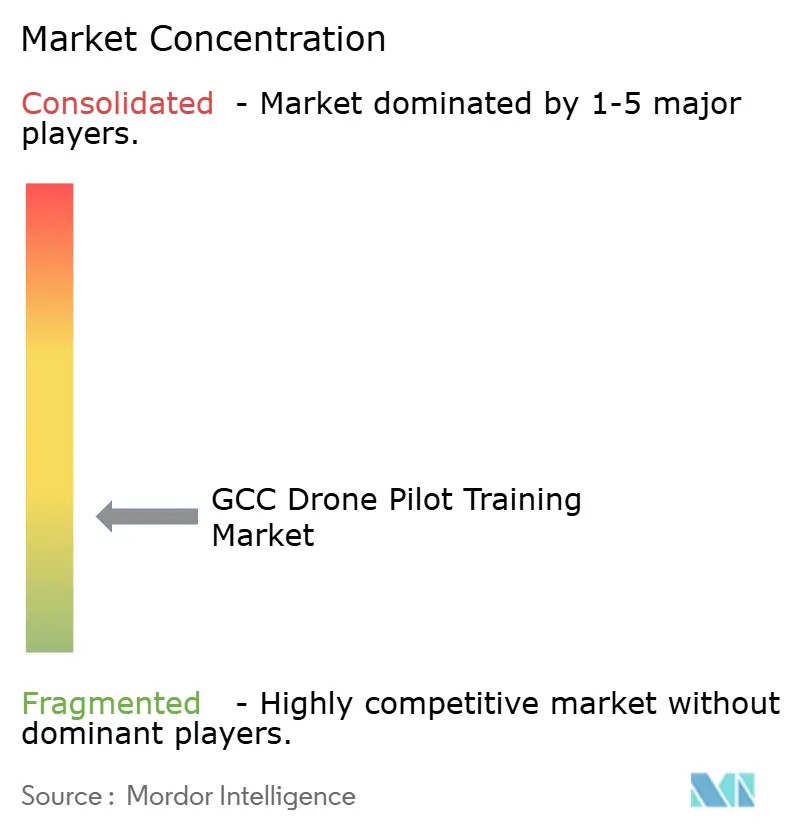

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Drone Pilot Training Market Analysis by Mordor Intelligence

The GCC drone pilot training market size stands at USD 321.7 million in 2025 and is projected to reach USD 988.8 million by 2030, registering a 25.18% CAGR. This sharp rise mirrors government Vision 2030 diversification targets, growing oil-and-gas inspection needs, and expanding smart-city programs that lift demand for licensed drone crews. Regulatory harmonization around the International Civil Aviation Organization (ICAO) Standards issued in March 2025 is steering operators toward accredited academies, while the United Arab Emirates (UAE) alone forecasts a requirement for 22,000 additional pilots and crew by 2033. Rotary-wing courses dominate enrolment today, yet hybrid vertical-take-off-and-landing (VTOL) curricula are accelerating as urban-air-mobility trials start in Saudi Arabia and the United Arab Emirates. Meanwhile, instructor shortages and high insurance premiums temper short-term growth. However, widespread bilingual Arabic-English programs and female-only cohorts signal an inclusive workforce transformation that underpins the long-run outlook.

Key Report Takeaways

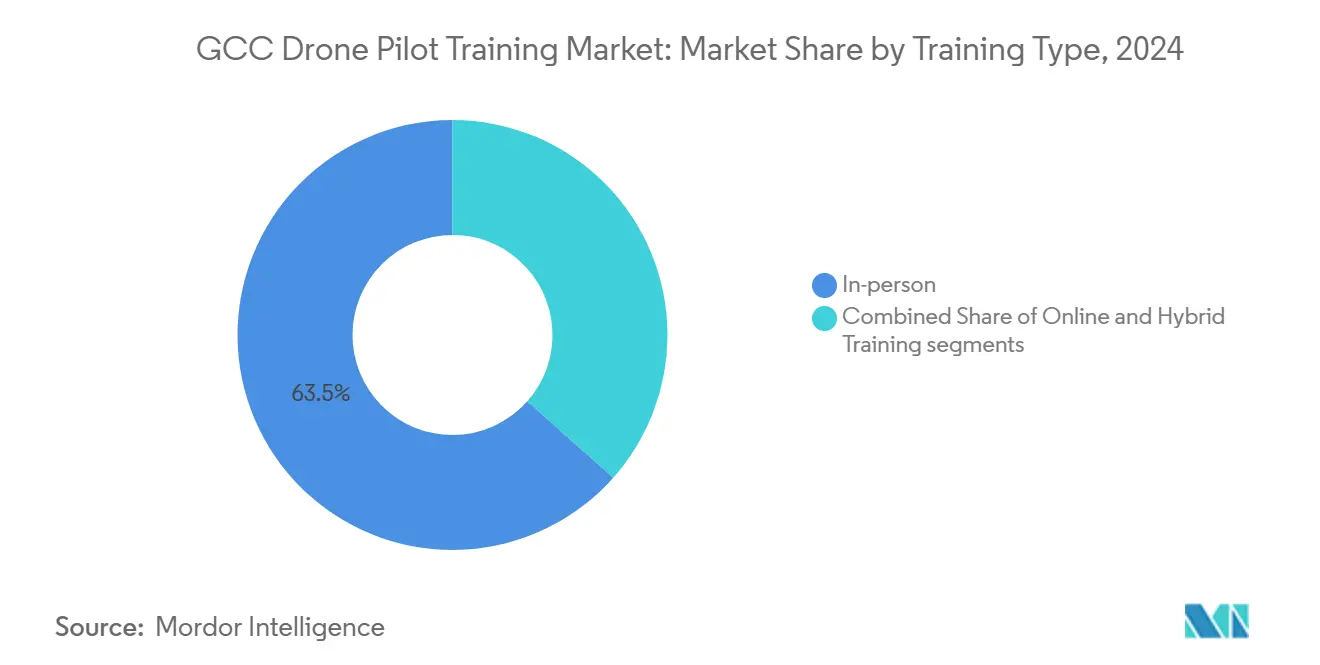

- By training type, in-person instruction led with 63.45% of GCC drone pilot training market share in 2024, while hybrid programs are advancing at a 17.51% CAGR through 2030.

- By drone class, rotary-wing courses held 69.78% revenue share in 2024, and hybrid VTOL offerings are forecasted to expand at a 21.56% CAGR to 2030.

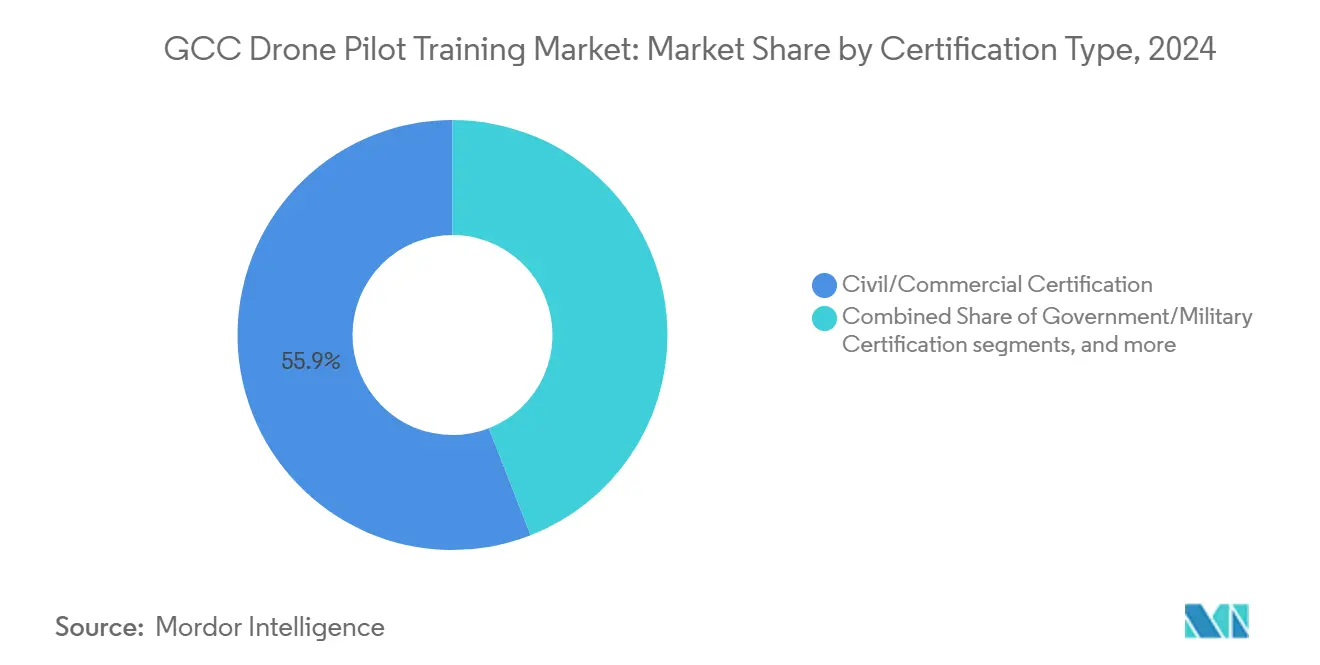

- By certification type, civil and commercial licences accounted for a 55.92% share of the GCC drone pilot training market in 2024, whereas government and military certifications are growing at a 20.35% CAGR.

- By end-user industry, media and entertainment commanded 37.89% revenue share in 2024, with government and defense enrolment rising fastest at 20.45% CAGR.

- By geography, Saudi Arabia retained 33.67% revenue share in 2024, while Qatar is set to grow at an 18.01% CAGR between 2025 and 2030.

GCC Drone Pilot Training Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory mandate for commercial UAV licensing | +4.2% | GCC-wide, strongest in UAE and Saudi Arabia | Short term (≤ 2 years) |

| Rising demand for aerial inspection services in oil and gas | +3.8% | Saudi Arabia, UAE, Qatar, Kuwait | Medium term (2-4 years) |

| Government smart-city and gigaproject initiatives | +3.5% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| Tourism-driven cinematography boom | +2.9% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Defense offset-funded scholarship programs | +2.1% | Saudi Arabia, UAE | Long term (≥ 4 years) |

| Female-only training cohorts aligned with Vision 2030 | +1.8% | Saudi Arabia, UAE | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory mandate for commercial UAV licensing

Harmonized frameworks now require every commercial pilot in the GCC drone pilot training market to obtain formal certification. The UAE issues Unmanned Aircraft Operator Authorizations, Saudi Arabia’s General Authority of Civil Aviation (GACA) grants Remote Pilot Certificates for craft above 250 g, and Qatar demands permits even for non-commercial flyers.[1]General Authority of Civil Aviation, “Remotely Piloted Aircraft Systems Regulation,” gaca.gov.sa Uniform rules eliminate informal coaching and funnel trainees to accredited schools, yet partial license recognition between states still forces some crews to recertify when crossing borders.

Rising demand for aerial inspection services in oil and gas

Digitization programs at Saudi Aramco and ADNOC push operators toward beyond-visual-line-of-sight (BVLOS) flights and AI-driven analytics. Pilots now need advanced thermal imaging, payload integration, and data processing skills, encouraging premium courses within the GCC drone pilot training market.[2]Energy Robotics GmbH, “Automated Drone Inspection Case Study,” energy-robotics.com Limited instructor pools for these specialised modules hold pricing power for academies that can meet strict safety and compliance standards.

Government smart-city and gigaproject initiatives

NEOM’s USD 500 billion master plan in Saudi Arabia, Dubai’s SkyDome corridor, and Qatar’s Vision 2030 projects rely on autonomous aircraft for construction monitoring, logistics, and passenger transport. Demand therefore shifts toward hybrid VTOL and eVTOL syllabi covering urban-air-traffic management, multi-drone coordination, and emergency protocols, broadening the GCC drone pilot training market beyond traditional photography roles.

Tourism-driven cinematography boom

Destination-marketing agencies in Dubai, Riyadh, and Doha commission high-definition aerial footage, pushing media houses to hire locally certified pilots who understand cultural norms and restricted zones. Cinematography courses include creative flight paths, camera control, and post-production workflows, generating stable enrolment and frequent up-skilling cycles inside the GCC drone pilot training market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified Arabic-speaking instructors | -2.8% | GCC-wide, acute in Saudi Arabia and Kuwait | Short term (≤ 2 years) |

| High insurance premiums for flight schools | -2.1% | UAE, Qatar, Bahrain | Medium term (2-4 years) |

| Restrictive no-fly zones around pilgrimage sites | -1.5% | Saudi Arabia, spillover effects in UAE | Long term (≥ 4 years) |

| Delays in harmonising GCC license reciprocity | -1.2% | GCC-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of certified Arabic-speaking instructors

The pool of trainers who can deliver high-level technical content in Arabic remains far smaller than the demand from public-sector scholarship programmes and Vision 2030 workforce targets. Academies that secure bilingual staff, such as FalconViz, routinely win government contracts because ministries insist on native-language instruction for safety briefings, examinations, and recordkeeping.[3]FalconViz, “Government Training Services,” falconviz.com Scarcity has pushed instructor salaries well above regional airline first-officer scales, raising tuition fees and eroding price competitiveness for smaller schools that cannot match these wage premiums. The imbalance also lengthens course start dates, forcing students to wait months for seat availability and compelling some enterprises to defer drone-service rollouts. Attempts to import expatriate instructors only partially solve the gap because most foreign trainers lack the Arabic fluency required for regulatory sign-off, leaving domestic capacity as the largest bottleneck in scaling the GCC drone pilot training market.

High insurance premiums for flight schools

All GCC states oblige training providers to hold third-party liability coverage. Yet, the UAE sets the highest floor at AED 3.67 million (USD 1 million), a figure insurers often double when underwriting courses that include beyond-visual-line-of-sight drills.[4]STA Law Firm, “Unmanned Aircraft Liability in the UAE,” stalawfirm.com Underwriters cite limited actuarial history and potential crowd risk in urban airspace, so they apply aviation-grade loss assumptions that inflate annual premiums far above those for comparable light-aircraft academies. Large institutions absorb the cost through volume, but independent operators must raise tuition or reduce simulator hours, weakening their competitive appeal. High coverage also discourages entry of niche providers that could serve specialised segments such as VTOL or thermal-inspection training, slowing innovation across the ecosystem. Until insurers gain confidence from broader claims data or regulators introduce risk-based premium tiers, elevated insurance costs will continue to cap the pace at which new capacity enters the GCC drone pilot training market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Training Type: Hybrid Programs Bridge Traditional Gaps

In-person instruction retained 63.45% of GCC drone pilot training market share in 2024 because regulators mandate logged stick-time and supervised manoeuvres. Practical modules cover emergency recovery, flight-controller calibration, and airspace communication, disciplines that remain difficult to replicate online. A blended model is growing at a 17.51% CAGR and is expected to lift the GCC drone pilot training market size for hybrid programs to USD 227.9 million by 2030. Online ground school delivers air law, meteorology, and navigation theory, after which candidates attend condensed boot camps for flight checks. This structure slashes travel expenditure for regional students and appeals to corporate clients who need predictable scheduling.

Hybrid curricula also leverage cloud-based learning-management systems and AI-driven progress analytics to personalise study plans. Emirates Flight Training Academy and Skydio Academy deploy mobile apps that send quizzes and flight-log feedback, thereby tightening knowledge-retention loops. Smaller schools adopt the same framework to compete on convenience rather than facility scale, creating multiple entry paths into the GCC drone pilot training market. Nonetheless, instrument-rated programs—especially for BVLOS operations—still require extended in-person simulator time, so physical campuses remain central even as remote modules proliferate.

By Drone Class: VTOL Capabilities Drive Innovation

Rotary-wing courses dominated 69.78% of enrolments in 2024, thanks to photography, inspection, and security needs that favour multi-rotor agility. Fixed-wing craft feature in mapping and pipeline surveys where endurance eclipses manoeuvrability, but demand is modest. Hybrid VTOL classes, registering 21.56% CAGR, are poised to capture USD 148.2 million of the GCC drone pilot training market size by 2030 as eVTOL logistics corridors go live. Trainees learn dual flight-regime aerodynamics, transition-phase control logic, and redundancy management.

Academies invest in next-generation simulators that replicate tilt-rotor behaviour and urban-air-traffic scenarios. Etihad Aviation Training’s new eVTOL division, backed by partnerships with Archer Aviation, demonstrates first-mover advantage. The capital intensity of VTOL hardware and the need for type-rated instructors create high barriers for start-ups, concentrating this slice of the GCC drone pilot training market among operators with aviation-academy heritage.

By Certification Type: Military Programs Accelerate Growth

Civil and commercial licences represented 55.92% of the GCC drone pilot training market in 2024 because sectors such as media, construction, and energy remain the largest drone adopters. Government and military certificates are rising fastest at 20.35% CAGR and are projected to contribute USD 431.7 million to the GCC drone pilot training market size by 2030. Courses cover secure datalink protocols, anti-jamming manoeuvres, and electronic-warfare awareness.

Defense authorities increasingly fund local cohorts under offset agreements that require knowledge transfer. Royal Saudi Air Force initiatives now integrate drone modules within broader pilot development tracks, while the UAE Armed Forces expand unmanned systems syllabi to ground personnel. These programs typically stipulate Arabic instruction and classified network simulators, advantages that incumbent academies already holding security clearances can exploit within the GCC drone pilot training market.

By End-User Industry: Government Agencies Drive Expansion

Media and entertainment providers generated 37.89% of 2024 revenue because tourism marketing agencies and streaming studios demand cinematic footage of headline landmarks. Government and defense buyers, however, are adding the most new seats at 20.45% CAGR due to surveillance, disaster response, and border security missions. Multiple ministries now issue blanket purchase agreements with local schools, converting sporadic orders into multi-year pipelines across the GCC drone pilot training market.

Oil-and-gas operators form a sizeable second-tier customer group, commissioning thermal-inspection and gas-leak-detection endorsements that attract premium tuition. Construction conglomerates enrol crews for progress-tracking and volumetric-calculation tasks, while academic institutes roll out bachelor-level unmanned-aviation degrees that feed future instructor pools. This diversified client base cushions schools against cyclical shocks and underscores the maturity of the GCC drone pilot training industry.

Geography Analysis

Saudi Arabia led the GCC drone pilot training market with 33.67% revenue share in 2024, underpinned by NEOM’s perpetual demand for urban-air-mobility crews and Saudi Aramco’s long-term inspection mandates. Vision 2030 localization policies funnel public funding into domestic academies, and dedicated female-only cohorts further widen candidate inflows. Restrictions around pilgrimage zones impose extra air-law content, but otherwise, the Kingdom offers expansive Class G airspace that supports comprehensive field exercises.

The UAE remains a powerhouse through its established aviation ecosystem, strong regulatory clarity, and international student pull. Emirates Flight Training Academy’s USD 181,650 Airline Transport Pilot Licence (ATPL) path demonstrates consumers’ readiness to invest in world-class facilities. Dubai’s SkyDome program catalyses urban-air-traffic management modules, while partnerships with Joby Aviation and Volocopter attract global attention. Insurance thresholds are high, yet abundant venture capital offsets entry costs and sustains healthy competition within the GCC drone pilot training market.

Qatar is the fastest-growing geography at an 18.01% CAGR. The Civil Aviation Authority’s decision to license hobbyists widens the addressable population, and National Vision 2030 megaprojects need regular surveillance flights. The state’s investment in digital twins and automated port logistics fosters specialist syllabi on data-pipeline integration and beyond-visual-line-of-sight compliance, ensuring robust volume for domestic and inbound trainees. Smaller markets—Kuwait, Bahrain, and Oman—add strategic diversity. Kuwait’s Directorate General of Civil Aviation (DGCA) enforces the UAS Operator Certificate. Bahrain uses a tiered classification regime, and Oman is experimenting with U-space service providers that may become testbeds for advanced autonomy. While smaller in value, each niche encourages curriculum differentiation and maintains a regional spread of the GCC drone pilot training market.

Competitive Landscape

Competitive dynamics remain fragmented because legacy flight academies, niche drone schools, and global manufacturers all claim space. Emirates Flight Training Academy, Etihad Aviation Training, and Prince Sultan Aviation Academy repurpose existing simulators and instructor cadres to issue unmanned licences rapidly, leveraging decades-old regulator relationships. Specialist players like FalconViz and Sanad Academy compete in Arabic instruction, geospatial data processing, and sector-specific endorsements, carving profitable lanes inside the GCC drone pilot training market.

Technology is a central differentiator. Skydio Academy integrates autonomy-based scenario training, while DJI-authorised schools focus on broad platform familiarity. Providers acquire immersive-reality simulators and cloud analytics dashboards that quantify flight precision and shorten feedback loops, raising pass rates and word-of-mouth referrals. Curriculum bundling—combining regulatory theory, remote-ID configuration, payload management, and post-production editing—helps schools extract higher per-student yields in the GCC drone pilot training industry.

Partnerships also shape market power. Emirates partners directly with Diamond Aircraft for multi-engine resources, while Saudi academies sign memoranda with defense contractors to secure simulator content. Insurance alliances serve as another moat because carriers often set exclusive premium brackets for vetted academies. Instructor scarcity exerts upward wage pressure favoring deep-pocketed incumbents, though scholarship-driven demand guarantees occupancy across most reputable classrooms. The GCC drone pilot training market is moderately concentrated.

GCC Drone Pilot Training Industry Leaders

The Drone Centre

Aerodyne Geospatial Sdn. Bhd.

Gulf Air Academy

FalconViz

Makalu Ventures, LLC, d.b.a. UAV Coach

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: UAV Corp announced a USD 105 million letter of intent for DART airships and a pilot-training hangar in the UAE free zone.

- December 2024: NEOM Investment Fund partnered with GMT Robotics to automate rebar assembly, indirectly boosting demand for drone oversight training on the project site.

- February 2024: SAL Saudi Logistics Services partnered with Space Age to localize drone logistics capabilities, opening scholarship slots for cargo-drone pilots.

- October 2024: Sonoran Desert Institute launched disaster-response drone modules, a template GCC academies are assessing for civil-defense contracts.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the GCC drone pilot training market as every paid program or course that teaches individuals or teams to safely plan, fly, and maintain civil, commercial, or government unmanned aircraft operated within Saudi Arabia, the United Arab Emirates, Qatar, Kuwait, Bahrain, and Oman. Instruction methods covered include classroom, simulator, field, and blended formats that culminate in a locally valid license or certificate.

Scope exclusion: Manufacturing of flight simulators, manned aircraft flight schools, and post-licensing recurrent courses are out of scope.

Segmentation Overview

- By Training Type

- In-person Training

- Online Training

- Hybrid Training

- By Drone Class

- Fixed-wing

- Rotary-wing

- Hybrid VTOL

- By Certification Type

- Civil/Commercial Certification

- Government/Military Certification

- Recreational License

- By End-user Industry

- Government and Defense Agencies

- Enterprise and Corporate

- Educational and Research Institutes

- Media and Entertainment

- Oil and Gas and Utilities

- Construction and Real Estate

- Others (Sports, Tourism)

- By Geography

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Bahrain

- Oman

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed chief instructors at leading GCC drone schools, safety inspectors, oil and gas asset managers, and film production crew chiefs across Riyadh, Dubai, and Doha. Insights on average flight hours needed for certification, dropout rates, and equipment refresh costs filled gaps and verified secondary assumptions.

Desk Research

We started with official air navigation notices, civil aviation regulations, and drone license registers from GCAA-UAE, GACA-Saudi Arabia, Qatar CAA, and ICAO. Market fingerprints such as annual student intake and pass rates were pulled from trade associations like the Middle East Aviation Training Organization Council, along with customs data on imported multi-rotor kits. Investor presentations from listed training academies, press releases on Vision 2030 scholarship cohorts, and peer-reviewed papers on UAV safety incidents grounded the demand model. Subscription feeds from Dow Jones Factiva and D&B Hoovers added hard numbers on course pricing and school revenues. This list is illustrative; many additional sources informed validation.

Market-Sizing & Forecasting

A top-down reconstruction used country-level new license issuances, average tuition, and expected recertification cycles. Results were cross-checked through selective bottom-up spot checks of academy revenues and typical ASP x student volumes. Key variables include: 1) annual construction site drone deployment counts, 2) defense scholarship quotas, 3) cinema-grade drone rental hours, 4) insurance premium trends, and 5) instructor to trainee ratios. A multivariate regression with ARIMA overlays projected these drivers to 2030, after gap handling for countries lacking transparent license data.

Data Validation & Update Cycle

Outputs pass variance checks against historical license growth and live enrollment dashboards. Senior analysts review anomalies, and figures refresh yearly, with mid-cycle updates when major regulatory or funding shifts occur.

Why Mordor's GCC Drone Pilot Training Baseline Inspires Confidence

Published estimates naturally differ because firms choose unlike geographies, training types, and forecast cadences.

Key gap drivers are: some publishers bundle manned aircraft or global regions, others focus on a single end user such as law enforcement, and many assume static tuition despite rapid price inflation. Mordor's disciplined scope, variable tracking, and annual refresh minimize such skews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 321.7 M (2025) | Mordor Intelligence | - |

| USD 1.8 B (2024) | Global Consultancy A | Includes all civil aviation training and simulation across Middle East, not drone specific |

| USD 80 M (2024) | Regional Consultancy B | Covers only agency remote pilot courses for entire MEA region |

| USD 60 M (2024) | Trade Journal C | Focuses on law enforcement training, excludes commercial cohorts and hybrid formats |

These contrasts show that when scope and inputs align with actual GCC licensing rules and segment demand, Mordor's balanced baseline offers the most reproducible decision foundation.

Key Questions Answered in the Report

What is the current value of the GCC drone pilot training market?

The market is valued at USD 321.7 million in 2025 and is projected to reach USD 988.88 million by 2030, registering a 25.18% CAGR.

Which training format is growing fastest?

Hybrid programs that mix online theory with in-person flight sessions are climbing at a 17.51% CAGR through 2030.

Why are hybrid VTOL courses important?

Hybrid VTOL courses prepare pilots for emerging urban-air-mobility and logistics corridors, expanding at a 21.56% CAGR within the GCC drone pilot training market.

How significant is government demand?

Government and defense agencies are the fastest-growing customer segment, registering a 20.45% CAGR as ministries adopt drones for security and emergency response.

Which GCC country shows the highest growth outlook?

Qatar leads with an 18.01% CAGR because its Civil Aviation Authority licenses both hobbyist and commercial flyers, creating the broadest trainee base.

What is the main barrier facing training providers?

A shortage of certified Arabic-speaking instructors remains the top operational hurdle, shaving an estimated 2.8 percentage points from forecast CAGR growth across the region.

Page last updated on: