Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

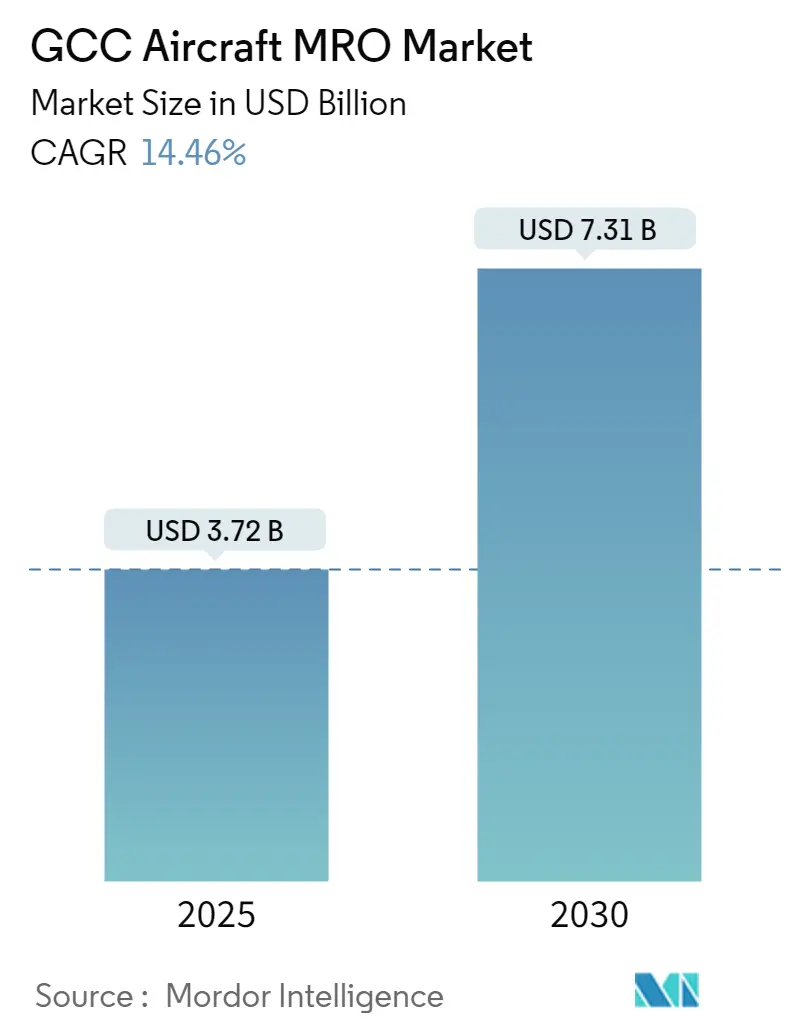

| Market Size (2025) | USD 3.72 Billion |

| Market Size (2030) | USD 7.31 Billion |

| Growth Rate (2025 - 2030) | 14.46% CAGR |

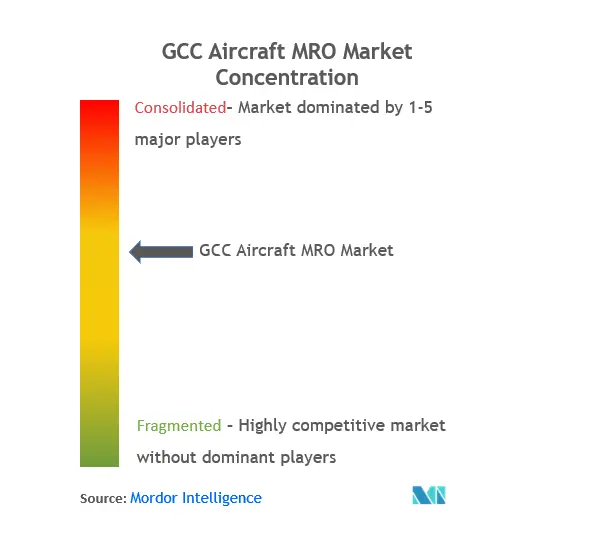

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Aircraft MRO Market Analysis by Mordor Intelligence

The GCC Aircraft MRO Market size is estimated at USD 3.72 billion in 2025, and is expected to reach USD 7.31 billion by 2030, at a CAGR of 14.46% during the forecast period (2025-2030).

The GCC aviation MRO landscape is experiencing significant transformation as regional economic powerhouses strengthen their aviation infrastructure. Emirates Engineering, one of the region's largest aircraft maintenance providers, currently operates 12 hangars and supports a fleet of 255 aircraft while serving over 30 international airlines through third-party aircraft maintenance services contracts. This extensive infrastructure development reflects the broader trend of GCC nations establishing themselves as global aviation maintenance hubs. The region's strategic geographical location between Europe, Asia, and Africa has catalyzed investments in advanced MRO facilities, with major players expanding their technical capabilities to handle next-generation aircraft.

The industry is witnessing a surge in strategic partnerships between local and international MRO providers, enhancing technical capabilities and service offerings. A notable example is the recent collaboration between Sanad Aerotech and Emirates Engine Maintenance Centre, which aims to elevate regional aviation MRO services through shared knowledge and technology transfer. The UAE's Etihad Engineering has demonstrated this evolution by developing state-of-the-art additive manufacturing capabilities, including the region's first EASA-certified design and production facility featuring advanced polymer systems for cabin parts manufacturing.

Infrastructure development continues to be a key focus area, with major facilities expanding their capabilities. Saudia Aerospace Engineering Industries (SAEI) operates 11 aircraft hangars and 27 aircraft component maintenance shops, making it one of the largest aerospace maintenance providers in the Middle East & Africa. The company's expansion plans include accommodating A380 aircraft, reflecting the industry's adaptation to serving larger aircraft types. Qatar Airways' maintenance facility spans 162,000 square meters and can simultaneously accommodate twelve aircraft, including five A380s, demonstrating the scale of regional MRO infrastructure.

Technical workforce development has emerged as a critical focus area for sustaining the industry's growth trajectory. Lufthansa Technik Middle East, with its UAE facility, exemplifies this trend by investing in specialized training programs and advanced repair capabilities for structural and composite materials. The facility has expanded its services to include sophisticated repairs using resistance spot welding and composite bonding techniques, showcasing the industry's commitment to developing advanced technical capabilities. This focus on technical expertise is crucial as the region's MRO providers increasingly handle complex maintenance tasks for both commercial and VIP aircraft.

GCC Aircraft MRO Market Trends and Insights

Growing Fleet Size and New Aircraft Orders

The GCC aircraft MRO market is primarily driven by the substantial fleet expansion plans of major regional carriers, evidenced by several significant aircraft orders in recent years. Qatar Airways demonstrated this trend with its massive USD 72 billion worth of orders for approximately 250 Airbus and Boeing aircraft as of March 2023, representing one of the largest commercial aviation commitments globally. This expansion is further complemented by other regional carriers, such as FlyDubai's December 2023 agreement with Boeing for 30 B787-9 aircraft, indicating the robust growth trajectory of the region's aviation sector.

The continuous fleet modernization initiatives by flagship carriers are creating sustained demand for comprehensive aviation maintenance, repair, and overhaul services. This is exemplified by Air Arabia Abu Dhabi's strategic move to secure 240 CFM Leap-1A engines in November 2023, which will power their future fleet, including the A321XLR aircraft. These substantial orders necessitate the development of sophisticated aircraft maintenance capabilities and infrastructure, as newer aircraft models require specialized maintenance protocols and advanced technological expertise. The increasing complexity of modern aircraft systems, particularly in new-generation aircraft, has led to a greater emphasis on preventive maintenance and the need for stronger maintenance control centers with advanced IT expertise.

Understand The Key Trends Shaping This Market

Download PDF

Infrastructure Development and MRO Facility Expansion

The strategic geographical positioning of GCC countries has catalyzed significant investments in aviation infrastructure, particularly in MRO facilities. This is exemplified by the November 2023 launch of Sanad's LEAP Engine MRO Center in Abu Dhabi, which represents a major advancement in regional maintenance capabilities with its impressive capacity to service up to 200 engines annually. The establishment of such specialized facilities demonstrates the region's commitment to developing comprehensive MRO capabilities and reducing dependence on external service providers.

The expansion of MRO infrastructure is further supported by collaborative initiatives between regional and international players. Major airlines are developing partnerships with engine OEMs and establishing state-of-the-art maintenance facilities to enhance their service portfolios. These developments are accompanied by investments in advanced technologies, such as predictive maintenance systems and sophisticated diagnostic tools, which are becoming increasingly crucial for maintaining modern aircraft fleets. The focus on infrastructure development extends beyond physical facilities to include investments in human capital and technical expertise, ensuring the region can handle the growing complexity of aviation maintenance requirements.

Rising Demand for Widebody Aircraft Services

The unique aviation landscape of the Middle East, characterized by limited domestic travel options and the presence of major international aviation hubs, has led to increased utilization of widebody aircraft, driving specialized MRO requirements. This trend is particularly evident in the operations of major carriers like Emirates and Etihad Airways, which maintain substantial widebody fleets to serve their extensive international route networks. The preference for widebody aircraft is further reinforced by the region's role as a global connection hub, necessitating aircraft capable of operating long-haul routes efficiently.

The growing widebody fleet has spurred the development of specialized maintenance capabilities and infrastructure designed specifically for larger aircraft. This includes the establishment of dedicated hangars capable of accommodating multiple widebody aircraft simultaneously and the development of specialized component repair facilities. The trend is further supported by the increasing complexity of widebody aircraft systems, which require more sophisticated maintenance protocols and specialized expertise in areas such as composite materials repair and advanced avionics maintenance.

Growing Low-Cost Carrier Segment

The emergence and expansion of the low-cost carrier segment in the GCC region is creating new demands for MRO services, particularly in the narrowbody aircraft category. This trend is exemplified by the establishment of Air Arabia Abu Dhabi, which marked a significant milestone as the UAE capital's first low-cost carrier. The growth of LCCs has led to increased demand for efficient and cost-effective maintenance solutions, particularly for narrowbody aircraft that form the backbone of low-cost operations.

The LCC segment's expansion is driving innovations in MRO service delivery, with a focus on reducing maintenance turnaround times and optimizing cost efficiency. This has led to the development of specialized maintenance programs tailored to the unique requirements of LCC operations, including quick-turn line maintenance and optimized check schedules. The trend is further supported by strategic partnerships between LCCs and MRO providers, aimed at developing maintenance capabilities that align with the high-utilization business models of budget carriers while maintaining competitive operating costs.

Segment Analysis: By MRO Type

Engine Segment in GCC Aircraft MRO Market

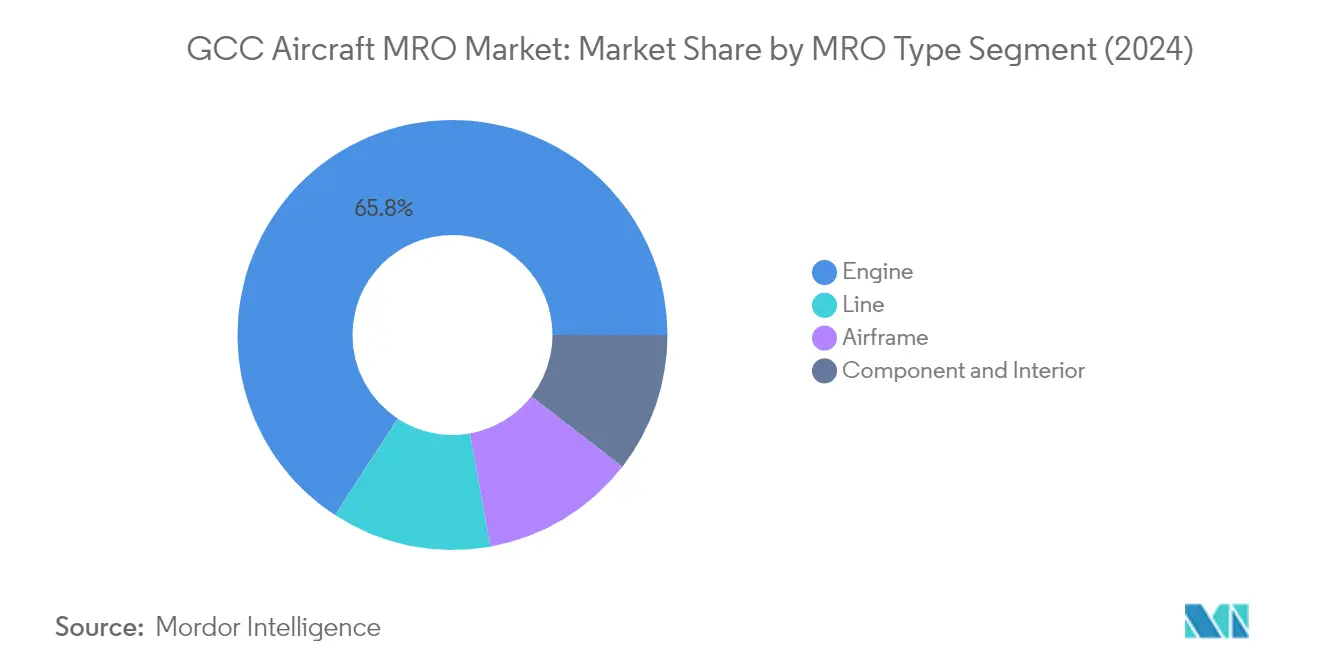

The engine segment dominates the GCC Aircraft MRO market, accounting for approximately 66% of the total market share in 2024. Aircraft engine maintenance represents the most critical and expensive component of aircraft maintenance, driven by the increasing complexity of engine parts and the critical need to prevent engine-related failures. In the engine MRO sector, OEMs control roughly half of the market, with the remaining share split between independent and airline overhaul shops. The segment's prominence is further reinforced by operators frequently outsourcing engine maintenance through comprehensive MRO-support programs. Major airlines in the region have established strategic partnerships with leading engine manufacturers like GE Aviation and Rolls-Royce to enhance their engine maintenance capabilities, while facilities like Abu Dhabi Aircraft Technologies (ADAT) have emerged as world-class maintenance centers for next-generation engines such as the GEnx.

Engine Segment in GCC Aircraft MRO Market

The engine segment is also projected to be the fastest-growing segment in the GCC Aircraft MRO market, with an expected growth rate of approximately 19% during 2024-2029. This rapid growth is driven by several factors, including the increasing adoption of new-generation aircraft in the region requiring specialized maintenance services. The segment's growth is supported by significant investments in advanced maintenance facilities and technologies across the GCC region. For instance, Sanad Aerotech has expanded its capabilities to become the only certified GEnx MRO partner in the Middle East and North Africa region. The increasing complexity of new engine technologies, coupled with stringent safety regulations and the need for regular maintenance regardless of aircraft utilization, continues to drive demand for aircraft engine maintenance services.

Remaining Segments in GCC Aircraft MRO Market

The airframe, component and interior, and line maintenance segments collectively form significant portions of the GCC Aircraft MRO market. The airframe maintenance segment focuses on heavy maintenance visits and structural modifications, benefiting from the increasing use of advanced technologies and composites in new-generation aircraft. The aircraft component maintenance and interior segment provides comprehensive services for avionics systems, cabins, and various aircraft parts, with providers implementing innovative solutions like predictive maintenance technologies. The line maintenance segment offers critical support for routine checks and immediate maintenance needs, with most major carriers maintaining in-house capabilities at their primary hubs while partnering with third-party providers for other locations. Additionally, the market for aircraft overhaul and aircraft base maintenance is expanding as airlines seek to optimize their fleet performance and longevity.

GCC Aircraft MRO Market Geography Segment Analysis

GCC Aircraft MRO Market in United Arab Emirates

The United Arab Emirates dominates the GCC aircraft MRO landscape, commanding approximately 50% of the total market share in 2024. The country's prominence is anchored by world-class MRO facilities like Emirates Engineering and Etihad Engineering, which have established themselves as regional centers of excellence. The UAE's strategic geographical location, coupled with its advanced aviation infrastructure, has made it a preferred destination for both regional and international carriers seeking aircraft maintenance services. The country's MRO capabilities span comprehensive airframe maintenance, engine overhaul, component repairs, and aircraft line maintenance operations. The presence of state-of-the-art facilities equipped with advanced technologies, including additive manufacturing capabilities and digital maintenance solutions, further strengthens its position. The UAE's MRO sector also benefits from strong partnerships with global OEMs and continuous investments in expanding service capabilities for next-generation aircraft.

GCC Aircraft MRO Market in Kuwait

Kuwait's aircraft MRO market is experiencing remarkable growth, projected to expand at approximately 27% CAGR from 2024 to 2029. The country's MRO sector is undergoing significant transformation driven by ambitious fleet expansion plans of local carriers and increasing demand for sophisticated aviation MRO services. Kuwait's strategic focus on developing its aviation infrastructure has attracted substantial investments in MRO capabilities. The country is actively expanding its maintenance facilities to handle various aircraft types, from narrow-body to wide-body aircraft. Local MRO providers are increasingly adopting advanced technologies and forming strategic partnerships with international players to enhance their service offerings. The government's supportive policies and commitment to aviation sector development have created a conducive environment for MRO growth. Kuwait's emergence as a regional MRO hub is further supported by its geographical advantage and growing emphasis on technical training and skill development programs.

GCC Aircraft MRO Market in Saudi Arabia

Saudi Arabia's aircraft MRO market demonstrates robust development, supported by the kingdom's ambitious aviation sector transformation plans. The country's MRO landscape is characterized by significant investments in expanding maintenance capabilities and infrastructure development. Saudia Aerospace Engineering Industries (SAEI) leads the market with its extensive facility network and comprehensive service portfolio. The kingdom's focus on localizing MRO services aligns with its Vision 2030 objectives, promoting domestic capabilities and reducing dependence on foreign aviation repair services. Saudi Arabia's MRO sector benefits from strong government support, strategic partnerships with international players, and continuous technological advancement initiatives. The market's growth is further driven by the expansion of domestic airlines' fleets and increasing demand for specialized aircraft maintenance services. The kingdom's commitment to developing a skilled local workforce through various training programs ensures sustainable growth in the MRO sector.

GCC Aircraft MRO Market in Qatar

Qatar's aircraft MRO market showcases impressive development, backed by the country's strong aviation sector and commitment to technical excellence. The market benefits from Qatar Airways' extensive fleet operations and its state-of-the-art maintenance facilities. The country's MRO capabilities encompass a wide range of services, including heavy maintenance, component repairs, and specialized technical solutions. Qatar's focus on adopting cutting-edge technologies and implementing efficient maintenance practices has enhanced its competitive position in the regional MRO landscape. The country's MRO providers have established strong partnerships with global aerospace manufacturers and technology providers, ensuring access to the latest maintenance solutions. Qatar's investment in training and development programs has created a skilled workforce capable of handling complex aircraft repair operations. The market's growth is further supported by the country's strategic location and its role as a major aviation hub.

GCC Aircraft MRO Market in Other Countries

The aircraft MRO markets in Bahrain and Oman contribute significantly to the GCC's overall MRO landscape, each offering unique advantages and specialized services. Bahrain's MRO sector benefits from its established aviation infrastructure and strategic partnerships with international maintenance providers. The country's focus on developing specialized maintenance capabilities, particularly in engine maintenance and component repairs, has strengthened its position in the regional market. Meanwhile, Oman's MRO sector leverages its strategic location and growing aviation sector to expand its maintenance capabilities. Both countries are actively investing in infrastructure development, workforce training, and technology adoption to enhance their MRO service offerings. Their markets are characterized by increasing collaboration with global players, a focus on service quality improvement, and a commitment to meeting international maintenance standards. These smaller but dynamic markets play a crucial role in providing comprehensive aircraft maintenance coverage across the GCC region.

Competitive Landscape

Top Companies in GCC Aircraft MRO Market

The GCC aircraft MRO market features prominent players like Emirates Engineering, Saudia Aerospace Engineering Industries, Rolls-Royce, Raytheon Technologies, and Etihad Airways Engineering leading the sector. Companies are increasingly focusing on technological advancement through investments in additive manufacturing, predictive maintenance, aircraft health monitoring systems, and composite repair capabilities. The integration of artificial intelligence and big data analytics has become a key trend as MRO providers aim to streamline operations and enhance service efficiency. Strategic partnerships between local and international players have accelerated knowledge transfer and capability enhancement, particularly in specialized services like engine maintenance and component repairs. Facility expansions and modernization initiatives across the GCC region demonstrate the industry's commitment to building comprehensive service portfolios and reducing dependency on external providers.

Local Champions Dominate Regional MRO Services

The GCC aviation maintenance market exhibits a unique structure where local players, particularly airline-affiliated maintenance providers, hold significant market share alongside global MRO specialists. The market has transformed from having a few standalone providers to becoming highly fragmented, with intense competition driving service quality improvements and technological adoption. The entry of foreign players through joint ventures and partnerships has reshaped the competitive dynamics, leading to enhanced service offerings and expanded capabilities across airframe, engine, component, and line maintenance segments. The presence of major airlines' in-house MRO divisions has created a robust ecosystem that serves both regional and international customers.

The industry has witnessed increased consolidation through strategic alliances and partnerships, particularly between regional providers and global OEMs. These collaborations have enabled local MRO providers to access advanced technologies and expand their service capabilities while helping international players establish a stronger regional presence. The market structure continues to evolve with airlines developing their in-house airline maintenance capabilities to reduce operational costs and enhance control over critical maintenance functions, while simultaneously maintaining partnerships with specialized service providers for specific technical requirements.

Innovation and Flexibility Drive Future Success

Success in the GCC aviation engineering services market increasingly depends on providers' ability to adapt to technological advancements and changing customer requirements. MRO companies must invest in digital transformation initiatives, including predictive maintenance capabilities and automated inspection systems, while building expertise in handling next-generation aircraft components. The development of local talent through partnerships with educational institutions and training programs has become crucial for sustainable growth, as has the ability to offer flexible service packages that accommodate varying customer needs and fleet types.

Market participants need to focus on building comprehensive service portfolios while maintaining cost competitiveness through operational efficiency improvements. The increasing use of composite materials and advanced avionics systems requires continuous capability enhancement and certification updates. Regulatory compliance and safety standards remain critical success factors, with providers needing to maintain multiple international certifications to serve a diverse customer base. The ability to offer rapid turnaround times while maintaining high-quality standards will continue to differentiate successful providers in this competitive landscape, particularly as airlines focus on minimizing aircraft downtime and optimizing maintenance costs.

GCC Aircraft MRO Industry Leaders

Emirates Engineering (Emirates Group)

RTX Corporation

Etihad Airways Engineering L.L.C.

Rolls-Royce plc

Saudia Aerospace Engineering Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2023: Emirates signed a contract with GE Aerospace for 202 GE9X engines and spares to power its upcoming Boeing B777X aircraft. The agreement also includes a detailed long-term service commitment.

- November 2023: GAL AMMROC and Pannesma formed a partnership to provide advanced aircraft maintenance, upgrade, and overhaul services for rotary and fixed-wing aircraft.

GCC Aircraft MRO Market Report Scope

Aircraft MRO encompasses activities that maintain an aircraft and its components' airworthiness. Service providers conduct overhauls, inspections, replacements, defect rectifications, and modifications in line with airworthiness directives. This study focuses on MRO services for commercial fixed-wing and general aviation aircraft in the GCC region.

The GCC aircraft MRO market is segmented by MRO type and geography. By MRO type, the market is segmented into the airframe, engine, component and interior, and line. The report also offers the market size and forecasts for six countries across the region. For each segment, the market size is provided in terms of value (USD).

By MRO Type

| Airframe |

| Engine |

| Component and Interior |

| Line |

By Geography

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Oman |

| Kuwait |

| Bahrain |

| By MRO Type | Airframe |

| Engine | |

| Component and Interior | |

| Line | |

| By Geography | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Oman | |

| Kuwait | |

| Bahrain |

Key Questions Answered in the Report

How big is the GCC Aircraft MRO Market?

The GCC Aircraft MRO Market size is expected to reach USD 3.72 billion in 2025 and grow at a CAGR of 14.46% to reach USD 7.31 billion by 2030.

What is the current GCC Aircraft MRO Market size?

In 2025, the GCC Aircraft MRO Market size is expected to reach USD 3.72 billion.

Who are the key players in GCC Aircraft MRO Market?

Emirates Engineering (Emirates Group), RTX Corporation, Etihad Airways Engineering L.L.C., Rolls-Royce plc and Saudia Aerospace Engineering Industries are the major companies operating in the GCC Aircraft MRO Market.

What years does this GCC Aircraft MRO Market cover, and what was the market size in 2024?

In 2024, the GCC Aircraft MRO Market size was estimated at USD 3.18 billion. The report covers the GCC Aircraft MRO Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the GCC Aircraft MRO Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: