France Geospatial Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

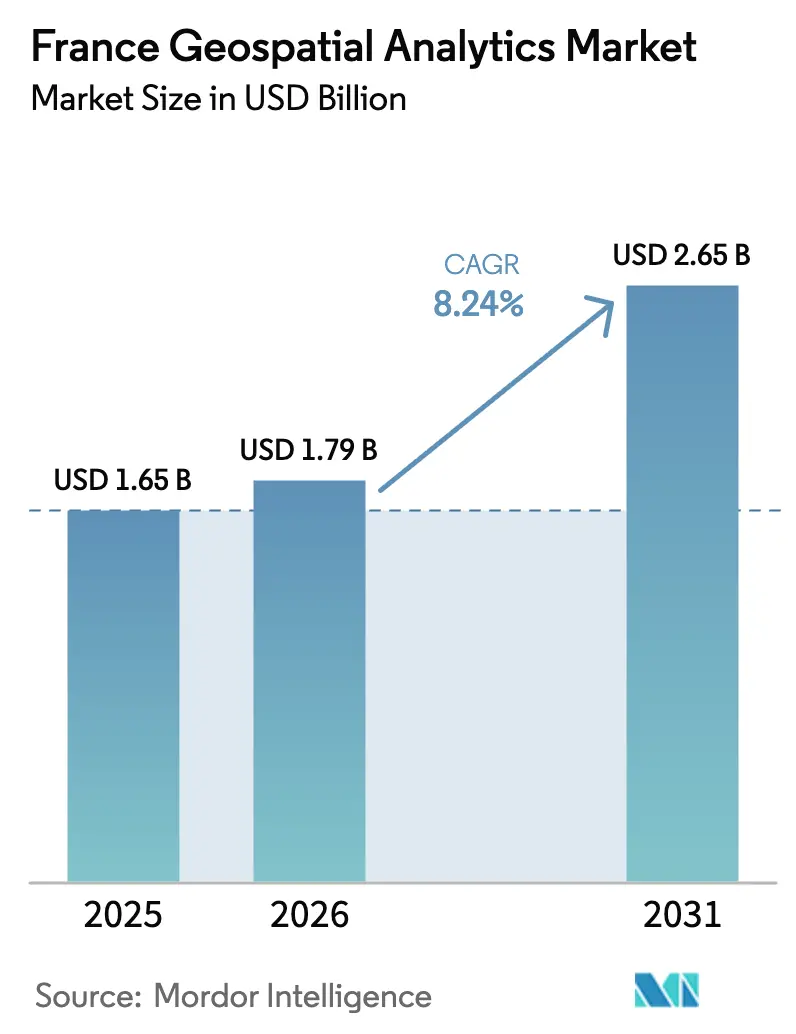

| Base Year Market Size (2025) | USD 1.65 Billion |

| Market Size (2026) | USD 1.79 Billion |

| Market Size (2031) | USD 2.65 Billion |

| Growth Rate (2026 - 2031) | 8.24% CAGR |

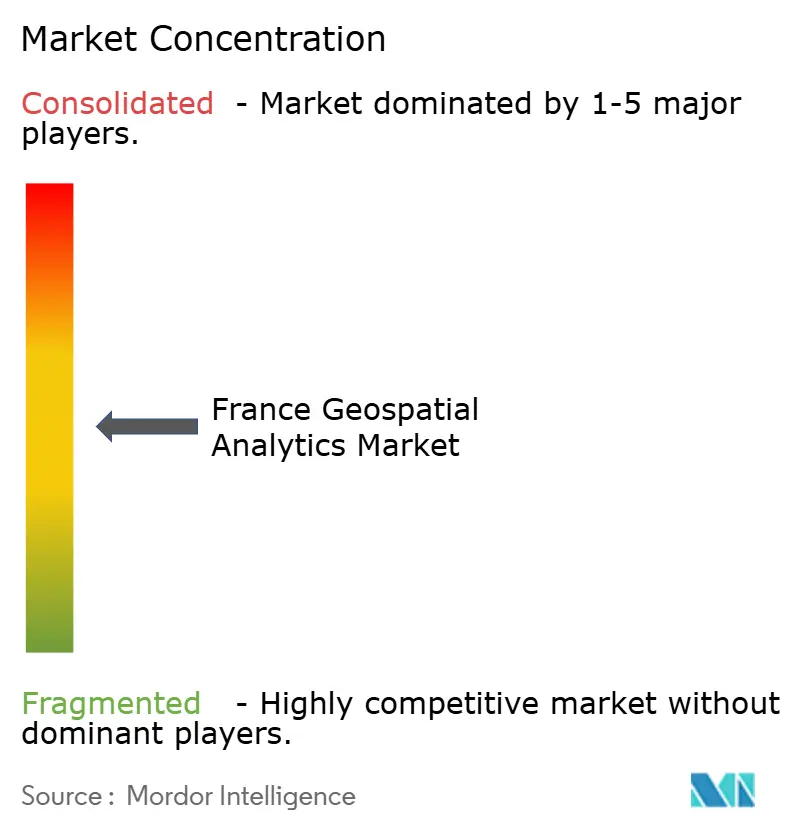

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Geospatial Analytics Market Analysis by Mordor Intelligence

The France Geospatial Analytics Market size is expected to grow from USD 1.65 billion in 2025 to USD 1.79 billion in 2026 and is forecast to reach USD 2.65 billion by 2031 at 8.24% CAGR over 2026-2031.

France benefits from a long-standing space pedigree, deep public funding and strict digital-sovereignty rules that direct spending toward domestic suppliers. The launch of the CSO-3 military observation satellite in March 2025 strengthens national imagery independence while expanding high-resolution data licensing opportunities to European allies.[1]Airbus Communications, “CSO-3 Successfully Enters Orbit,” airbus.comMeanwhile, the EUR 2 billion Fonds vert drives demand for spatial monitoring tools that validate project eligibility, especially in sectors required to file biodiversity impact reports from 2026.[2]Government of France, “Fonds vert Budget Allocation 2025,” gouvernement.fr Rapid 5G rollout under the “Réseaux du Futur” program pushes the France geospatial analytics market toward real-time sensor fusion, and the digital-twin initiative led by IGN and Cerema encourages city governments to embed location intelligence inside every urban-planning workflow. Capital injections and an export-friendly satellite fleet give local vendors an edge as the country positions itself as a continental hub for sovereign spatial intelligence.

Key Report Takeaways

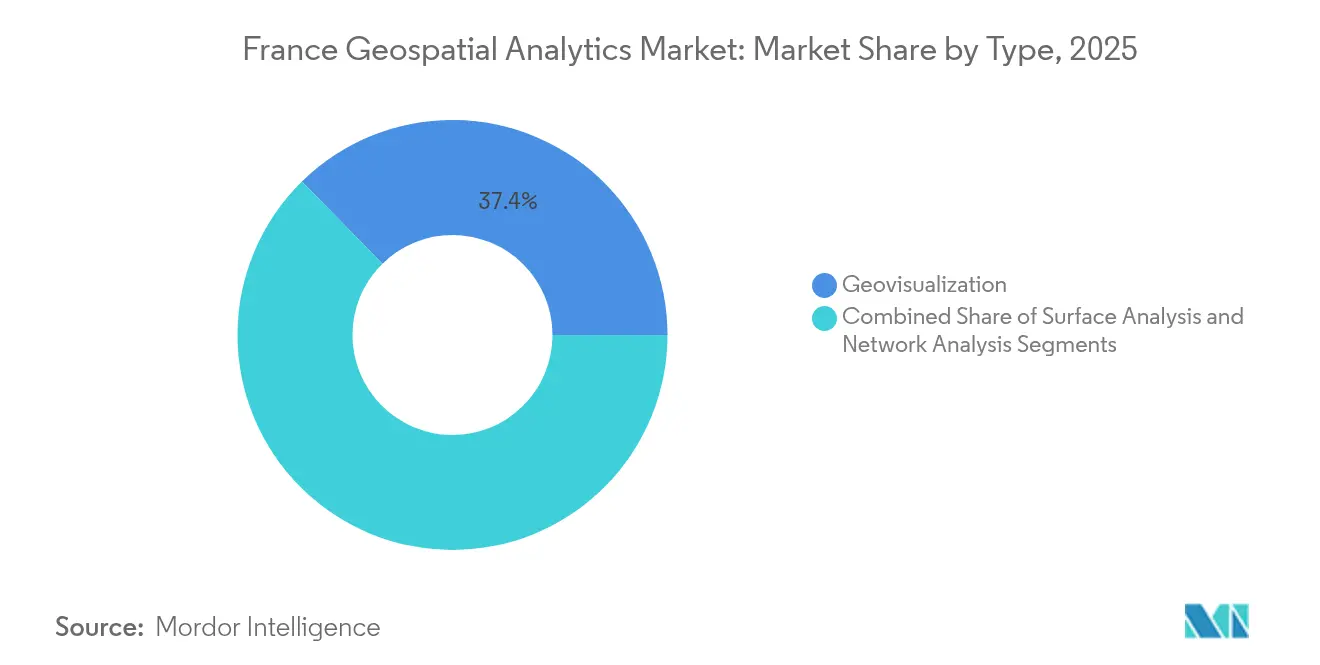

- By type, geovisualization led with 37.35% of France geospatial analytics market share in 2025, while network analysis is projected to grow at a 13.15% CAGR through 2031.

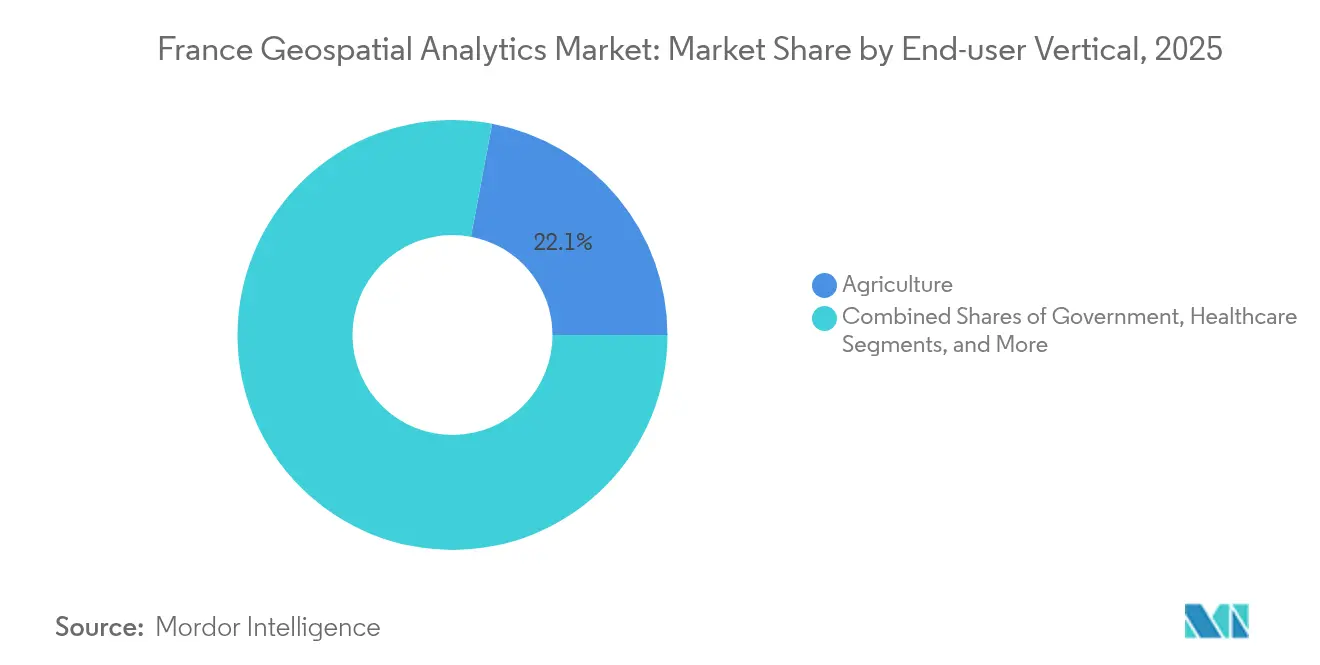

- By end-user vertical, agriculture held 22.05% of France geospatial analytics market share in 2025; automotive and transportation are forecast to expand at a 14.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Projections can easily extend beyond country and regional trends as they are defined by movement across the full international system. Mordor Intelligence's worldwide geospatial analytics market outlook captures this forward trajectory.

France Geospatial Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart city and mobility funding surge | +2.1% | National; early gains in Paris, Lyon, Marseille | Medium term (2-4 years) |

| Defense satellite constellation (CSO-3) demand | +1.8% | National; spillover to EU partners | Long term (≥ 4 years) |

| ESG and Green-Budget compliance mandates | +1.4% | National; industrial regions | Short term (≤ 2 years) |

| 5G-IoT real-time data streams | +1.2% | Urban centers; expanding rural | Medium term (2-4 years) |

| Mandatory biodiversity impact reporting (2026) | +0.9% | National; protected areas | Short term (≤ 2 years) |

| Precision-viticulture platform adoption | +0.7% | Bordeaux, Burgundy, Loire Valley | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Smart city and mobility funding surge

France is channeling EUR 475 million into road construction and a further EUR 294 million into road maintenance in 2025.[3]Sénat Budget Office, “Investissements routiers 2025,” senat.fr Municipalities receive these funds only if they can document efficiency gains, which elevates demand for geospatial dashboards that track pavement condition, traffic flow, and carbon footprint in near real time. Istres’ private 5G network demonstrates how geospatial analytics cuts municipal operating costs by 40% while improving emergency-response routing accuracy.[4]Ericsson Press Release, “Private 5G Network Deployed in Istres,” ericsson.com The national digital-twin platform, spearheaded by IGN, Cerema, and Inria, lets cities simulate flood, heat-island, and traffic scenarios, turning spatial data into predictive asset-management tools. France’s commitment to interoperability standards ensures repeatable deployments across 35,000 communes, creating durable revenue streams for vendors whose software supports the new schemas. As volumes of LiDAR, CCTV, and sensor data grow, the France geospatial analytics market will pivot from descriptive mapping to anticipatory decision support.

Defense satellite constellation (CSO-3) demand

The EUR 795 million CSO program supplies 35 cm imagery that meets NATO strategic-intelligence criteria while remaining under French command. Data commercialization clauses permit secure distribution to trusted European partners, generating an export channel that did not exist before. Ukraine’s 2025 contract with a Safran subsidiary to fuse CSO data into its defense-planning platform underscores the constellation’s market potential beyond France. Downstream, insurers, utilities and foresters gain access to a level of spatial precision previously reserved for defense. The constellation integrates with the C40S space-domain-awareness system, allowing AI algorithms to flag anomalies and send real-time alerts to both civil and military users. Each new analytic use case expands transaction volume, cementing satellite data as the backbone of the France geospatial analytics market.

ESG and Green-Budget compliance mandates

Environmental rules tighten every year. From 2026, listed companies must report biodiversity impact with georeferenced evidence. Geospatial platforms automate site-level monitoring, overlay protected-species databases and generate auditable compliance reports, cutting manual audit costs by up to 60% for large industrials. The Carb-Chaser constellation, managed by Thales Alenia Space, will deliver certified CO₂ plume measurements that regulators accept as legal proof. France also invested EUR 53 million in BRGM to map strategic minerals, a move that requires high-resolution topographic and subsurface data. These public projects reinforce commercial trust in domestic geospatial infrastructure, accelerating adoption across heavy industry and finance.

5G-IoT real-time data streams

The Réseaux du Futur program sets aside EUR 65 million for 5G-Advanced and 6G testbeds Edge-enabled antennas feed imagery, GNSS readings and sensor outputs to cloud nodes with sub-10 ms latency, letting farmers monitor soil-moisture patches and city officials track bike-lane occupancy. LTE-M deployments already support low-power devices that transmit geolocated measurements for years on a single battery. The combination of high-bandwidth backhaul and energy-efficient edge devices moves the France geospatial analytics market into continuous-monitoring business models where clients pay for streaming situational awareness rather than one-off map layers. Telecom carriers and pure-play analytics firms now partner to embed spatial AI into their service catalogs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High integration and migration cost | −1.6% | National; enterprise sector | Short term (≤ 2 years) |

| Geo-data-science talent shortage | −1.3% | National; Paris and Lyon | Long term (≥ 4 years) |

| Municipal data-standard fragmentation | −0.9% | Regional; varies by level | Medium term (2-4 years) |

| Cloud-sovereignty hosting limits | −0.7% | National; cross-border deals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High integration and migration cost

A full-stack geospatial rollout can exceed EUR 500,000 once data-ingest pipelines, sensor gateways and training programs are factored in. Many small and mid-sized firms delayed projects after construction output fell 8.4% in Q3 2024, showing the sensitivity of spatial-IT budgets to macro conditions. Legacy resource-planning software often lacks spatial fields, forcing companies to purchase middleware and hire specialist integrators. This increases total cost of ownership and makes the payback period less attractive when compared to cloud CRM or ERP investments. Until plug-and-play connectors mature, high entry costs will temper growth in the France geospatial analytics market.

Geo-data-science talent shortage

Demand for analysts who can combine satellite-imagery classifiers with GPU-based inference far outstrips supply. Universities are updating curricula, yet out-flow is limited to a few hundred graduates a year, insufficient to fill open requisitions at Paris-Saclay, Toulouse and Sophia Antipolis tech clusters. Companies like Thales run internal bootcamps, but the ramp-up time delays project launches. Scarcity drives salaries upward and pushes some projects offshore, which conflicts with data-sovereignty mandates. The talent gap therefore subtracts momentum from the France geospatial analytics market until broader STEM initiatives produce larger cohorts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Geovisualization Dominates Through Interactive Intelligence

Geovisualization held 37.35% of France geospatial analytics market share in 2025, reflecting public agencies’ need for map-centric dashboards that non-technical staff can interpret quickly. Budget officers use color-coded layers to rank infrastructure risk, while vineyard managers monitor plant stress on a mobile heatmap. The France geospatial analytics market size for geovisualization is projected to grow at 7.12% CAGR as 3D engines and browser-based point-cloud renderers remove workstation limits. Vendors embed accessibility features such as voice navigation and contrast toggles, supported by research from Université Claude Bernard Lyon 1 that demonstrated mobile geovisualization benefits for users with visual impairments.

Network analysis is the fastest-growing sub-segment at a 13.15% CAGR through 2031. This surge aligns with expanded electric-vehicle-charger deployment, where planners evaluate optimal station spacing and grid impact. Surface analysis continues to have steady demand from precision-agriculture and mining clients who require terrain-aware fertilizer plans or blast-risk contours. The combined momentum across sub-segments signals that the France geospatial analytics market will broaden from static map production toward analytical workflows that integrate routing, proximity and elevation parameters inside a single interface.

By End-user Vertical: Agriculture Leads While Automotive Accelerates

Agriculture accounted for 22.05% of France geospatial analytics market size in 2025. Viticulture projects use multi-spectral imagery plus IoT soil probes to fine-tune irrigation, saving water and improving grape quality. Farmers in Bordeaux and Burgundy link plot-level NDVI trends to yield forecasts, then price futures more accurately on commodity exchanges. Aerial spraying firms load prescription maps into autonomous drones, demonstrating how geospatial analytics now influences both upstream crop decisions and downstream trade functions.

The automotive and transportation vertical will experience a 14.21% CAGR between 2026 and 2031. High-definition base maps, centimeter-grade GNSS corrections, and roadside-unit telemetry underpin advanced driver-assistance systems and robotaxi pilots. The France geospatial analytics market size for automotive players benefits from public smart-road budgets and stringent EU safety targets. Utilities, telecom, and defense applications also expand as 5G coverage and the CSO program reduce latency and uplift imagery resolution. As demand disperses across verticals, suppliers diversify SaaS offerings to minimize reliance on any single industry.

Geography Analysis

The France geospatial analytics market is heavily domestic, tapping EUR 2.5 billion in AI and EUR 1.8 billion in quantum allocations under France 2030. Aerospace and defense use cases cluster around Toulouse and Paris, while agri-tech firms anchor in Bordeaux, Dijon and Montpellier. Digital-sovereignty policies require sensitive datasets to reside on SecNumCloud-certified infrastructure, rewarding local providers and complicating joint ventures with non-EU hyperscalers.

At the same time, European integration expands the addressable demand. France spearheads the EU’s destination-Earth digital-twin pilot, exporting methodology and software templates to partner states. CSO-3 imagery sales to allied governments add external revenue while bolstering regional security ties. Ukraine’s 2025 licensing deal illustrates how defense-grade data can enter commercial supply chains under proper export controls.

Beyond Europe, French satellite primes explore Africa and Middle-East markets, offering monitoring packs for pipeline security and desertification watch. They leverage export-credit insurance from Bpifrance to de-risk foreign deals. Domestic sovereign requirements plus selective cross-border alliances place the France geospatial analytics market on a dual-track strategy: protect critical assets at home while monetizing value-added services abroad.

The geospatial analytics market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Africa and Middle East. This is complemented by country-specific insights for United Kingdom, Italy, Nigeria, Israel, Canada, United Arab Emirates, and South Korea, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The market exhibits moderate fragmentation. Thales Alenia Space and Airbus Defence and Space Intelligence lead high-capex orbital segments, securing multiyear defense contracts and dominating the optical-satellite fleet airbus.com. Software-centric challengers exploit AI and cloud to erode incumbents’ margin in analytics layers. Safran’s EUR 220 million purchase of Preligens in 2024 injected automated object-detection into its offering, illustrating the shift from hardware to AI platforms.

Midsize firms such as Mytraffic and Geoblink combine mobile footfall data with geospatial clustering to guide retail location decisions, signalling growth in B2B SaaS niches. Academic spin-offs commercialize geospatial knowledge graphs, protected by recent patent filings that map spatial entities to semantic triples. Cloud-native architectures win bids where public agencies demand elastic scalability and SecNumCloud certification, pressuring legacy desktop GIS vendors to refactor codebases.

Strategic moves include joint data-distribution portals between Airbus and CNES, 3D point-cloud streaming solutions from Hexagon and digital-twin alliances among IGN, Cerema and Inria. Competitive intensity is expected to rise as telcos bundle geospatial analytics into private-5G offerings, expanding the field from specialists to network operators. The ability to couple sovereign hosting with automated insight generation will determine future share capture in the France geospatial analytics market.

France Geospatial Analytics Industry Leaders

Trimble Geospatial

Bentley Systems, Inc

Esri France

CLS Groupe

Intermap Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Airbus launched the CSO-3 Earth-observation satellite aboard Ariane 6, completing France’s reconnaissance trio with 35 cm resolution capability.

- March 2025: Hexagon AB announced plans to spin off its Safety, Infrastructure & Geospatial business into an independent entity valued at EUR 1.448 billion.

- February 2025: Bentley Systems reported full-year 2024 revenue of USD 1.353 billion, highlighted by its acquisition of 3D geospatial firm Cesium.

- January 2025: ACWA Robotics raised EUR 4.8 million to scale inspection robots that map underground water networks, supporting the national 10% water-withdrawal-reduction target.

France Geospatial Analytics Market Report Scope

Geospatial analytics is the process of acquiring, manipulating, and displaying imagery and data from the geographic information system (GIS), such as satellite photos and GPS data. The specific identifiers of a street address and a zip code are used in geospatial data analytics. They are used to create geographic models and data visualizations for more accurate trends modeling and forecasting.

The France geospatial analytics market is segmented by type (surface analysis, network analysis, geovisualization), by end user vertical (agriculture, utility and communication, defence and intelligence, government, mining and natural resources, automotive and transportation, healthcare, real estate, and construction). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Surface Analysis |

| Network Analysis |

| Geovisualization |

| Agriculture |

| Utility and Communication |

| Defense and Intelligence |

| Government |

| Mining and Natural Resources |

| Automotive and Transportation |

| Healthcare |

| Real Estate and Construction |

| Other End-user Verticals |

| By Type | Surface Analysis |

| Network Analysis | |

| Geovisualization | |

| By End-user Vertical | Agriculture |

| Utility and Communication | |

| Defense and Intelligence | |

| Government | |

| Mining and Natural Resources | |

| Automotive and Transportation | |

| Healthcare | |

| Real Estate and Construction | |

| Other End-user Verticals |

Key Questions Answered in the Report

What is the current size of the France geospatial analytics market?

The France geospatial analytics market size stands at USD 1.79 billion in 2026.

How fast will the market grow through 2031?

The market is projected to post an 8.24% CAGR, reaching USD 2.65 billion by 2031.

Which application segment is the largest today?

Agriculture leads with 22.05% of France geospatial analytics market share in 2025 due to widespread precision-farming adoption.

What drives rapid growth in the automotive vertical?

Demand for autonomous-vehicle mapping and smart-road planning propels a 14.21% CAGR in automotive and transportation use cases.

How does CSO-3 benefit commercial users?

The satellite supplies 35 cm imagery that civil sectors can license under controlled agreements, improving urban planning, insurance and environmental-monitoring accuracy.

Why is talent scarcity a restraint?

Universities produce too few graduates skilled in both spatial analytics and AI, delaying project rollouts and raising salary costs for specialized roles.

Page last updated on: