Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.84 Billion |

| Market Size (2026) | USD 1.95 Billion |

| Market Size (2031) | USD 2.59 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France Adhesives Market Analysis by Mordor Intelligence

The France Adhesives Market size is projected to be USD 1.84 billion in 2025, USD 1.95 billion in 2026, and reach USD 2.59 billion by 2031, growing at a CAGR of 5.83% from 2026 to 2031. The France adhesives market is riding a renovation-led construction rebound, accelerating substitution toward water-borne and bio-based chemistries that comply with REACH and RE2020 mandates while buffering the hit from a 60-year low in domestic vehicle production. Volume growth is strongest in thermal-insulation tapes, tile adhesives, and structural glazing sealants used in the nation’s EUR 32.2 billion energy-retrofit pipeline, yet raw-material inflation and titanium-dioxide costs remain 70% higher than pre-2020, keeping margins tight. At the same time, electric-vehicle (EV) assembly lines are pulling demand toward high-performance epoxy and polyurethane bonds that cut weight and extend battery range, with an average EV already using nearly 8 lb of adhesives and sealants in its battery pack and motor interfaces. Competitive intensity is rising as global strategics execute bolt-on deals. Arkema bought Dow’s packaging-lamination line in December 2024, and Henkel signed to acquire ATP in January 2026, to lock in low-VOC portfolios and deeper access to renovation projects.

Key Report Takeaways

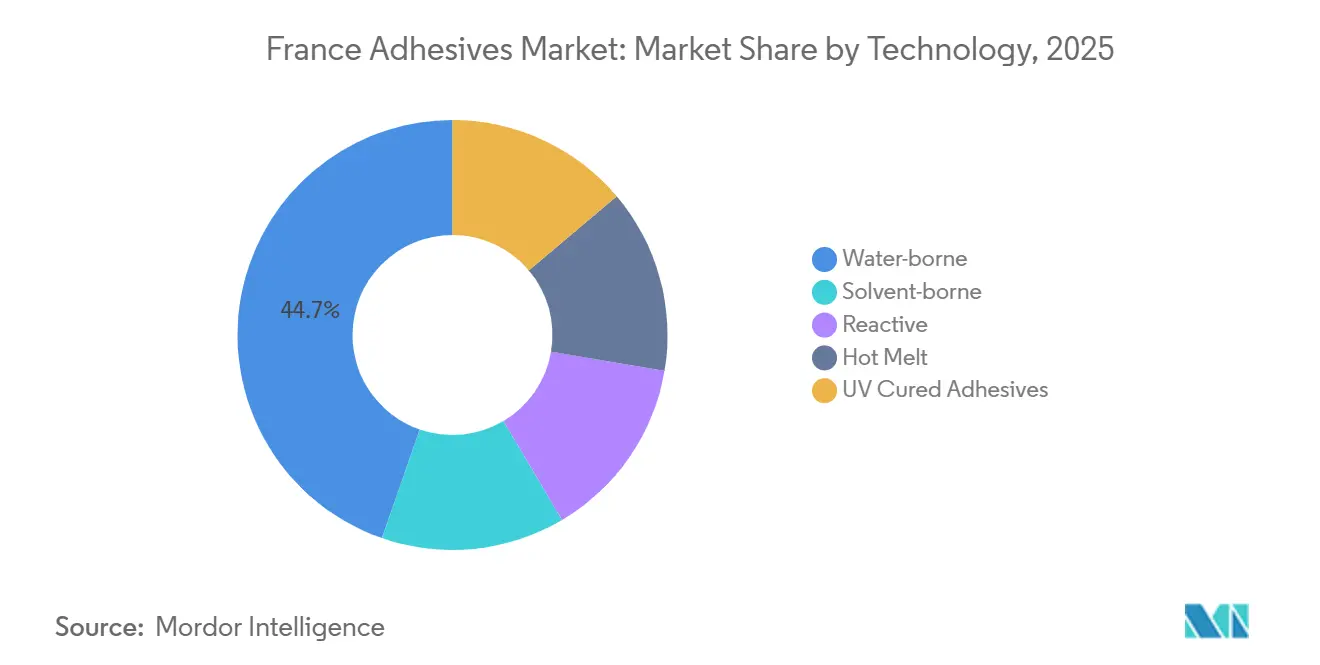

- By technology, water-borne systems led with a 44.68% share of the France Adhesives market in 2025, while hot-melt platforms are projected to expand at a 6.74% CAGR through 2031.

- By resin, acrylics commanded 28.78% of the France Adhesives market size in 2025, whereas VAE/EVA copolymers are poised for the fastest 6.43% CAGR during 2026-2031.

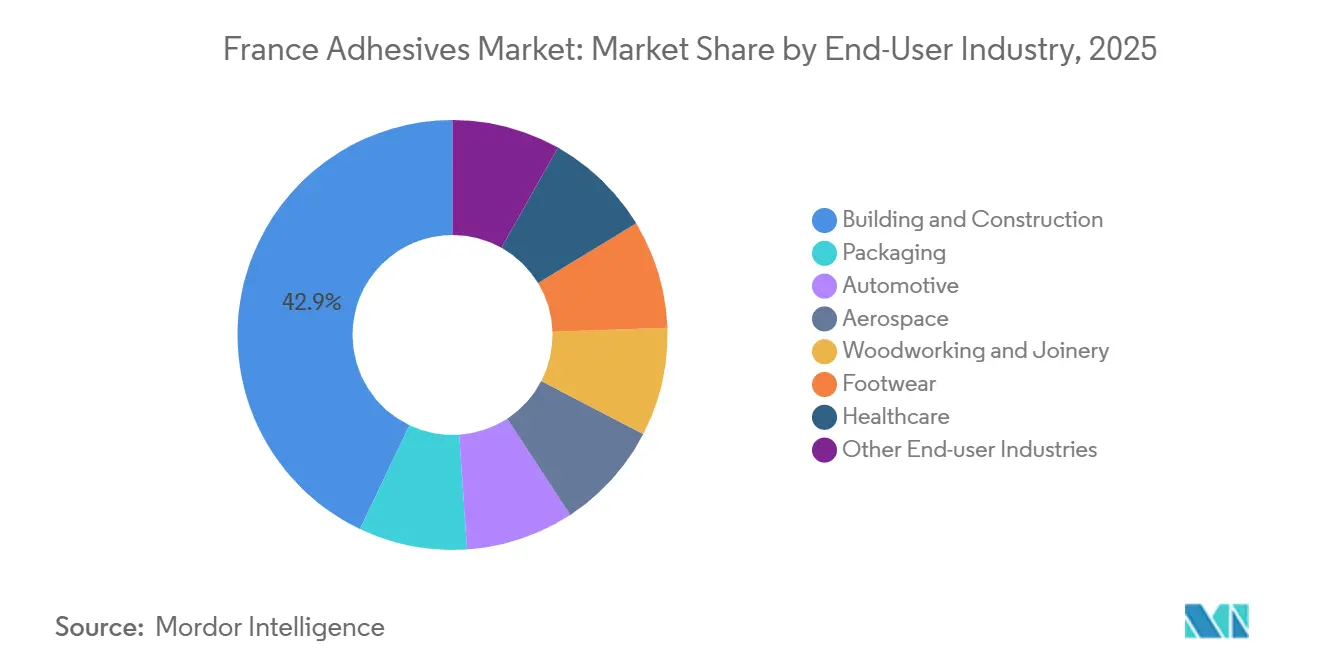

- By end-user, building and construction held 42.89% of the France Adhesives market share in 2025, yet automotive applications are advancing at a 6.39% CAGR as EV adoption gains traction.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

France Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation and energy-efficiency construction demand | +1.8% | National, with concentration in Île-de-France, Auvergne-Rhône-Alpes | Medium term (2-4 years) |

| Automotive lightweighting and EV assembly needs | +1.2% | National, with spillover to European automotive corridors | Long term (≥ 4 years) |

| Rising demand for water-borne/low-VOC systems | +1.0% | National, aligned with EU REACH and RE2020 compliance zones | Short term (≤ 2 years) |

| EU green-taxonomy incentives for bio-based formulas | +0.7% | EU-wide, early adoption in France and Germany | Long term (≥ 4 years) |

| Paris-2024 retrofits and heritage-building restorations | +0.4% | Île-de-France and UNESCO heritage sites nationally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Renovation and Energy-Efficiency Construction Demand

Energy-retrofit incentives, led by MaPrimeRénov’, disbursed EUR 1.95 billion to 505,126 projects in 2023 and generated EUR 32.2 billion of cumulative works between 2020 and mid-2024, driving sustained pull for low-VOC sealants, airtightness tapes, and bio-based panel adhesives. Embodied-carbon caps under RE2020 are tightening from 640 kg CO₂e/m² in 2022 to 415 kg CO₂e/m² by 2031, pushing formulators to swap UF and phenolic resins for bio-sourced alternatives. Continuous-insulation systems using 160 mm mineral wool, prefabricated CLT walls, and vapor-barrier membranes all rely on adhesives with superior freeze-thaw stability and low emissions. Funding from Certificats d’Économies d’Énergie hit EUR 4.15 billion in 2024, further accelerating retrofit activity. Factory-built elements already cut on-site waste by roughly 30%, increasing demand for fast-curing panel bonds that keep assembly lines moving.

Automotive Lightweighting and EV Assembly Needs

Electric-vehicle programs depend on structural epoxy and polyurethane adhesives that distribute loads, bond dissimilar metals to composites, and survive 180-250°C paint-bake cycles[1]Adhesive and Sealant Council, “EV Adhesive Usage Statistics,” ascouncil.org. Stellantis invested over USD 40 million in a Turin battery technology center aiming to halve battery weight by 2030, a goal linked directly to replacing rivets and welds with adhesives that avoid brittle intermetallics. Hybrid joints, adhesive plus rivet, are becoming the new norm in battery housings, providing peel resistance plus sealing. Although France’s vehicle output slumped to a six-decade low in 2024, the long-run shift to EVs is expected to restore volume. Short-run softness in automotive trim and interior adhesives, down 4.5% in 2024, masks a structural upswing in high-value battery applications primed to lift the France Adhesives market over the forecast horizon.

Rising Demand for Water-Borne/Low-VOC Systems

Tighter solvent rules and brand sustainability pledges are steering converters toward water-borne acrylic and VAE emulsions that meet 0.1% isocyanate caps and deliver low-VOC profiles. Solvent-free adhesive migration tests show primary aromatic amines well below EU food-contact limits, shortening print-to-lamination cycles in flexible packaging. Henkel teamed with Swedish bio-chemical supplier Sekab to swap fossil ethyl acetate for bio-based grades in French adhesive plants, cutting cradle-to-gate carbon footprints without altering line settings. PPG’s EUR 9 million expansion of OEM water-borne capacity in Europe signals cross-fertilization of raw-material streams from coatings to adhesives. Overall, water-borne systems already account for 44.68% of national volume and remain the backbone of paper, board, and tile-adhesive lines that anchor the France Adhesives market.

EU Green-Taxonomy Incentives for Bio-Based Formulas

EU funding is scaling fermentation-based phenolic resins and polylysine binders that cut greenhouse-gas footprints by 30-60% relative to fossil counterparts. The EUR 28 million BioImpulse project completed pilot runs at 200 m³ and validated plywood sheets, now nearing commercial launch. SUSBOARD’s 100% bio-based MDF adhesives promise to match UF cost while eliminating formaldehyde off-gassing. Panneaux de Corrèze commercialized Green Ultimate panels with 60% lower bonding emissions, giving furniture makers plug-and-play options for E0 compliance. Casein-flax boards met EN 15197 class 2 with an internal bond strength of 0.20 N/mm² while improving fire resistance, opening specialty doors for heritage carpentry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| REACH tightening on isocyanates and solvents | -0.9% | EU-wide, with heightened enforcement in France and Germany | Short term (≤ 2 years) |

| Escalating compliance cost for SME converters | -0.6% | National, concentrated among converters with <50 employees | Medium term (2-4 years) |

| Laser-welding substitution in selected auto parts | -0.3% | National automotive corridors, spillover to European OEM supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

REACH Tightening on Isocyanates and Solvents

Since August 24, 2023, industrial use of polyurethane adhesives with more than 0.1% free diisocyanate requires certified worker training, documentation, and periodic renewals[2]SOPREMA, “Guide pratique REACH diisocyanates,” soprema.fr . Small converters shoulder disproportionate compliance costs as they retrofit lines or reformulate into “micro-emission” grades. Reformulations often span a full year, delaying product launches and tying up research and development budgets. The rule covers MDI, TDI, HDI, and IPDI across structural, flooring, and flexible-packaging segments. Although ECHA forecasts 3,000 fewer asthma cases annually, near-term disruption clips volume growth in the France Adhesives market until exempt blends gain scale.

Escalating Compliance Cost for SME Converters

Titanium-dioxide prices remain 70% above pre-2020 levels, while anti-dumping duties on Chinese epoxy resins add further cost to a raw-material basket that already drives 50% of adhesive production expense. SMEs lack the breadth to amortize extended-producer-responsibility fees, Triman labeling redesigns, and lifecycle-assessment software mandated by RE2020. The adhesives, mastics, and sealants segment shrank 3.2% in 2024, and industry federation Fipec does not expect a rebound before 2026. Early liquidations in the coatings supply chain and deferred capital spend signal that smaller players could lose share to multinationals better able to finance compliance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Borne Dominance Meets Hot-Melt Acceleration

Water-borne platforms retained the largest 44.68% France adhesives market share in 2025 due to their compliance with VOC legislation and compatibility with cementitious substrates in tile adhesives and paper lamination. Hot-melt systems are forecast to expand at a 6.74% CAGR, lifting their slice of the France Adhesives market size as packaging lines invest in fast-setting, pressure-sensitive grades that reduce clamp time and energy use. Demand for ultra-low-monomer polyurethane hot melts is rising in flexible food packaging because they meet 0.1% isocyanate thresholds without curing delays. On the commodity end, water-borne acrylics cover bookbinding, labeling, and interior wood panels where E0 emissions rules apply. Reactive epoxies and polyurethanes occupy structural niches, EV battery packs, wind turbine blades, and aircraft interiors, where lap-shear strengths of 20-35 MPa justify premium pricing.

Hot-melt suppliers are deepening vertical ties with equipment OEMs so converters can run at line speeds above 400 m/min, critical for e-commerce corrugated plants upgrading box-on-demand cells. Water-borne formulators invest in high-solid dispersion tech that boosts solids to 65% without viscosity spikes, improving coat-weight economics. UV-cured volumes, though niche, post double-digit growth in electronics and medical devices where sub-second cure avoids thermal stress. Solvent-borne usage continues to shrink as converters phase out toluene carriers in shoe and furniture lines. Combined, technology shifts underpin medium-term upswing in the France adhesives market despite cyclical bumps.

By Resin: Acrylic Leadership Challenged by VAE/EVA Surge

Acrylics led with 28.78% France adhesives market size in 2025, buoyed by clarity, UV resistance, and frost flexibility down to -40°C in automotive trim and label stock. VAE/EVA copolymers are winning share at a 6.43% CAGR, leveraging freeze-thaw stability and alkali resistance in cement mortars, breathable roofing membranes, and flexible laminates. BASF’s ISCC PLUS-certified biomass-balance polyether polyols launched in March 2026 bring drop-in sustainability gains to polyurethane adhesives used in EV battery bonding, footwear, and thermal-insulation foams. Epoxies remain the backbone of structural aerospace and wind-blade joints, where tensile strengths exceed 80 MPa and cure shrinkage stays below 5%. Cyanoacrylates serve precision medical devices, though moisture sensitivity caps outdoor adoption.

Silicones hold niche but strategic positions in solar-panel edge bonding and automotive gaskets that call for -55°C to +200°C resilience. Bio-based proteins, lignin, and tannins migrate from lab to pilot scale as formulators seek lower-carbon panel binders. Collectively, resin innovation keeps the France Adhesives market differentiated and lets suppliers tailor performance to increasingly granular end-use demands.

By End-User Industry: Construction Anchors, Automotive Accelerates

The building and construction segment accounted for 42.89% France Adhesives market share in 2025, powered by continuous-insulation retrofits, window replacement, and airtightness upgrades encouraged by MaPrimeRénov’ and CEE grants. Bio-based wood-panel resins compliant with E0 formaldehyde limits are scaling as furniture retailers highlight low-emission badges. Automotive demand is projected to rise at 6.39% CAGR, with each EV integrating up to 1 kg of gap-fillers for battery thermal management plus multi-material structural bonds in closures and body-in-white. Flexible-packaging converters boost orders for solvent-less laminating adhesives aligned with circular design targets and food-contact safety.

Aerospace, rail, and marine segments, though smaller, value FST-compliant and vibration-toughened epoxies that command margins above construction grades. Woodworking adhesives enter a transition era as bio-based casein and lignin-phenolic blends meet both mechanical and emissions specifications for next-generation interior panels. Healthcare and electronics keep pulling small but high-value batches of medical-grade cyanoacrylates and UV-cures. This end-use diversity cushions the France Adhesives market against single-sector swings.

Geography Analysis

Regional consumption skews toward Île-de-France, Auvergne-Rhône-Alpes, and Hauts-de-France, territories that collectively house over half of the national retrofit pipeline and most automotive assembly plants. Île-de-France alone absorbs a disproportionate share of thermal-insulation tapes and floor-levelling compounds as homeowners tap Paris climate budget subsidies. Cross-border flows of hot-melt slugs and VAE dispersions travel from production hubs in Germany and Belgium into northeastern France, aided by proximity to packaging clusters.

The Atlantic coastal belt, anchored by Nouvelle-Aquitaine’s aerospace composites valley, sees above-average uptake of flame-retardant epoxies and silicone sealants certified under EN 45545 for rail interiors. Occitanie’s wind-blade factories near Port-la-Nouvelle source marine-grade epoxies and polyurethane gels that resist salt spray, feeding incremental demand in southwestern corridors. In the southeast, Provence-Alpes-Côte d’Azur’s maritime refit yards consume specialty methacrylate adhesives used for composite superstructures on luxury yachts.

Rural regions dominated by timber and panel mills, such as Bourgogne-Franche-Comté, increasingly trial bio-phenolic and tannin blends aligned with EU taxonomy rules. Alpine ski-resort refurbishments trigger seasonal spikes for low-temperature curing polyurethanes that bond insulation at sub-zero jobsite temperatures. Overall, geographic granularity underscores why broad national averages mask pockets of high growth that suppliers target to outpace the aggregate France adhesives market forecast.

Competitive Landscape

The France Adhesives Market is moderately consolidated. Start-ups experiment with reversible bonds for circular construction, while multinationals push ultra-low-monomer polyurethanes exempt from costly REACH training. Digital twins for cure-profile simulation and online viscosity sensors improve first-pass yield, lifting profitability even as raw-material inflation eats into gross margin. The push-pull between regulation-driven portfolio shifts and cost-containment defines competitive moves, shaping how value is captured across the France Adhesives market.

France Adhesives Industry Leaders

-

Arkema Group

-

H.B. Fuller Company

-

Henkel AG & Co. KGaA

-

Sika AG

-

Dow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Scott Bader forged a partnership with Sandtech, entrusting them with the distribution of its resins, gelcoats, and structural adhesives throughout France.

- December 2025: UPM revealed its decision to halt label materials production at its Nancy, France, facility. However, the Nancy site was decided to function as a slitting and distribution terminal, ensuring timely service for UPM Adhesive Materials’ clientele.

France Adhesives Market Report Scope

Adhesives, including glue, cement, and paste, bond two surfaces together, preventing their separation. Available in forms like liquid, paste, or tape, these substances are defined by their stickiness, allowing them to adhere to materials such as wood, metal, or skin.

The France Adhesives Market is segmented by technology, resin, and end-user industry. By Technology, the market is segmented into water-borne, solvent-borne, reactive, hot melt, and UV-cured adhesives. By Resin, the market is segmented into polyurethane, epoxy, acrylic, cyanoacrylate, VAE/EVA, silicone, and other resins. By End-user Industry, the market is segmented into building and construction, packaging, automotive, aerospace, woodworking and joinery, footwear, healthcare, and other end-user industries. The market sizes and forecasts are provided in terms of value (USD).

By Technology

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot Melt |

| UV Cured Adhesives |

By Resin

| Polyurethane |

| Epoxy |

| Acrylic |

| Cyanoacrylate |

| VAE/EVA |

| Silicone |

| Other Resins |

By End-user Industry

| Building and Construction |

| Packaging |

| Automotive |

| Aerospace |

| Woodworking and Joinery |

| Footwear |

| Healthcare |

| Other End-user Industries |

| By Technology | Water-borne |

| Solvent-borne | |

| Reactive | |

| Hot Melt | |

| UV Cured Adhesives | |

| By Resin | Polyurethane |

| Epoxy | |

| Acrylic | |

| Cyanoacrylate | |

| VAE/EVA | |

| Silicone | |

| Other Resins | |

| By End-user Industry | Building and Construction |

| Packaging | |

| Automotive | |

| Aerospace | |

| Woodworking and Joinery | |

| Footwear | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the adhesives market.

- Product - All adhesive products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms