Flue Gas Desulfurization (FGD) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 27.61 Billion |

| Market Size (2031) | USD 37.03 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flue Gas Desulfurization (FGD) Market Analysis by Mordor Intelligence

The Flue Gas Desulfurization Market size in 2026 is estimated at USD 27.61 billion, growing from 2025 value of USD 26.03 billion with 2031 projections showing USD 37.03 billion, growing at 6.05% CAGR over 2026-2031.

A tightening regulatory landscape, expanding industrial retrofits, and early integration with carbon-capture equipment sustain growth even as coal capacity retreats worldwide. Power utilities remain the primary adopters, yet cement, iron, steel, and shipping fuel have incremental demand. Suppliers able to bundle wet and dry systems with data-driven services and carbon-capture modules are positioned to capture addressable revenue pools widening across Asia-Pacific, Europe, and selective North American industrial clusters. Coupled with a rising trade in high-purity synthetic gypsum and widening maritime scrubber deployment, the flue gas desulfurization market continues demonstrating durable resilience.

Key Report Takeaways

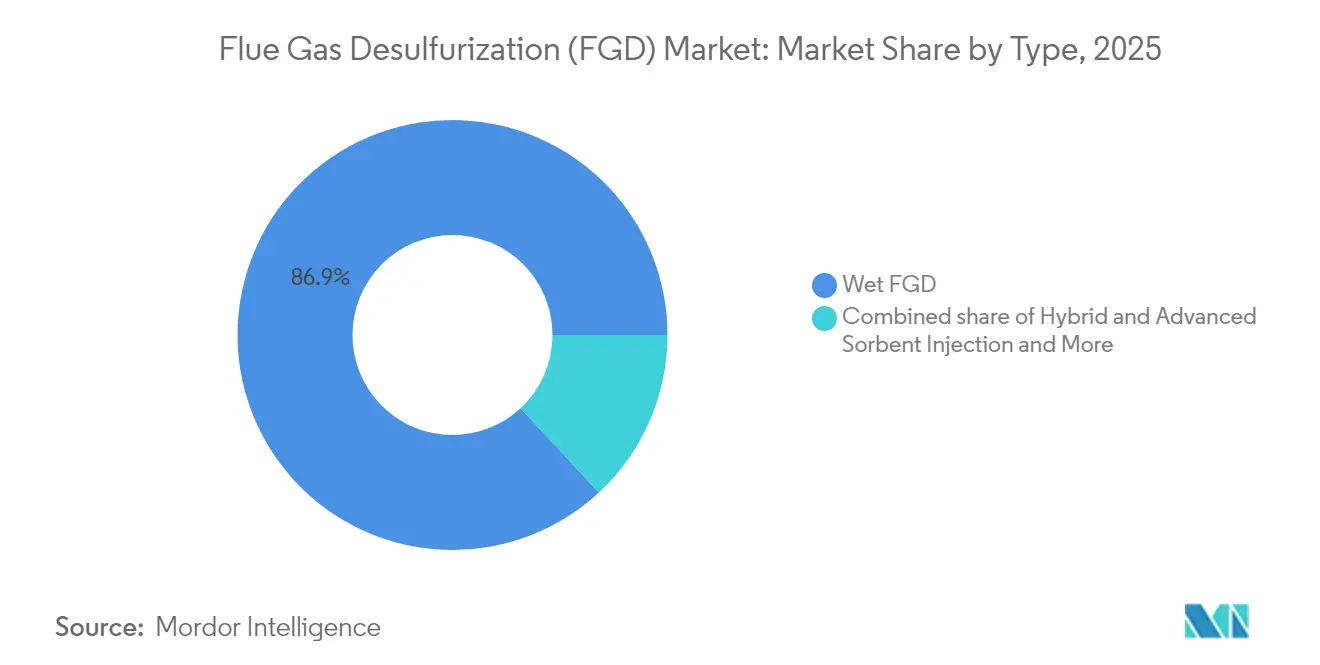

- By type, wet FGD captured 86.92% of the flue gas desulfurization market share in 2025; hybrid and sorbent-injection configurations are forecast to lead growth at 9.65% CAGR through 2031.

- By reagent, limestone commanded 62.95% share of the flue gas desulfurization market size in 2025, whereas sodium-based sorbents are poised to deliver an 8.22% CAGR to 2031.

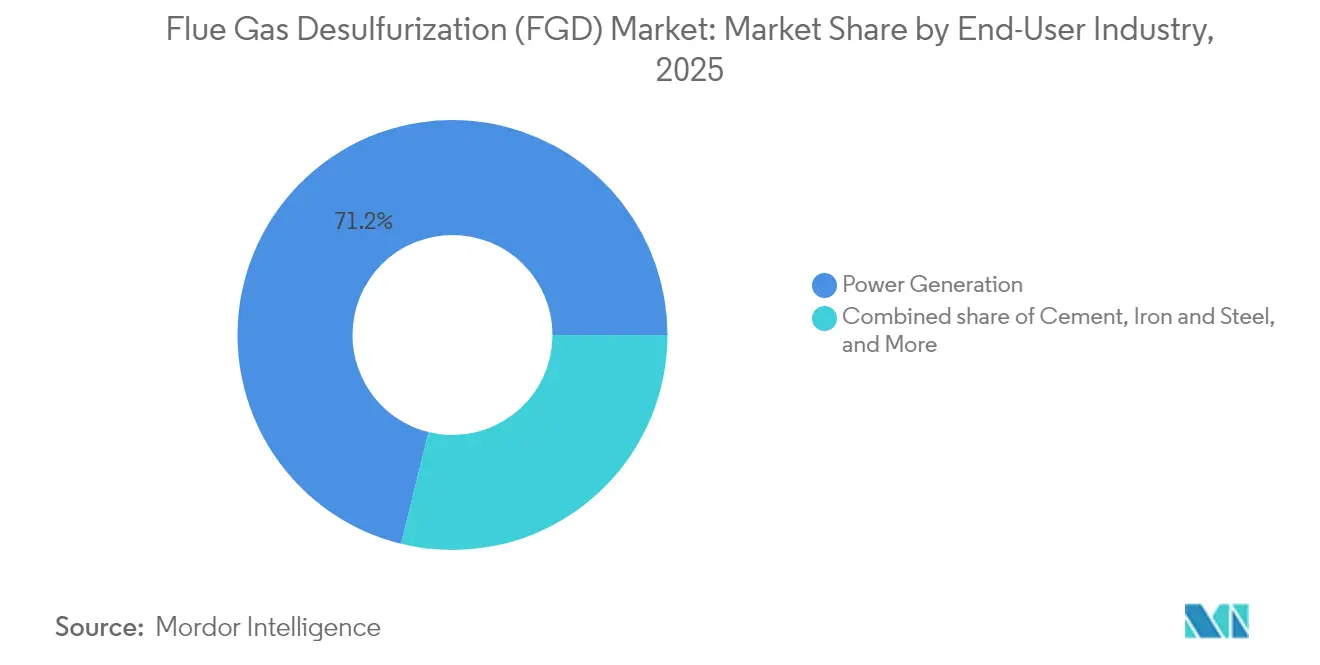

- By end-user, power generation accounted for 71.15% of the flue gas desulfurization market size in 2025, while the cement segment is projected to post the fastest 7.86% CAGR to 2031.

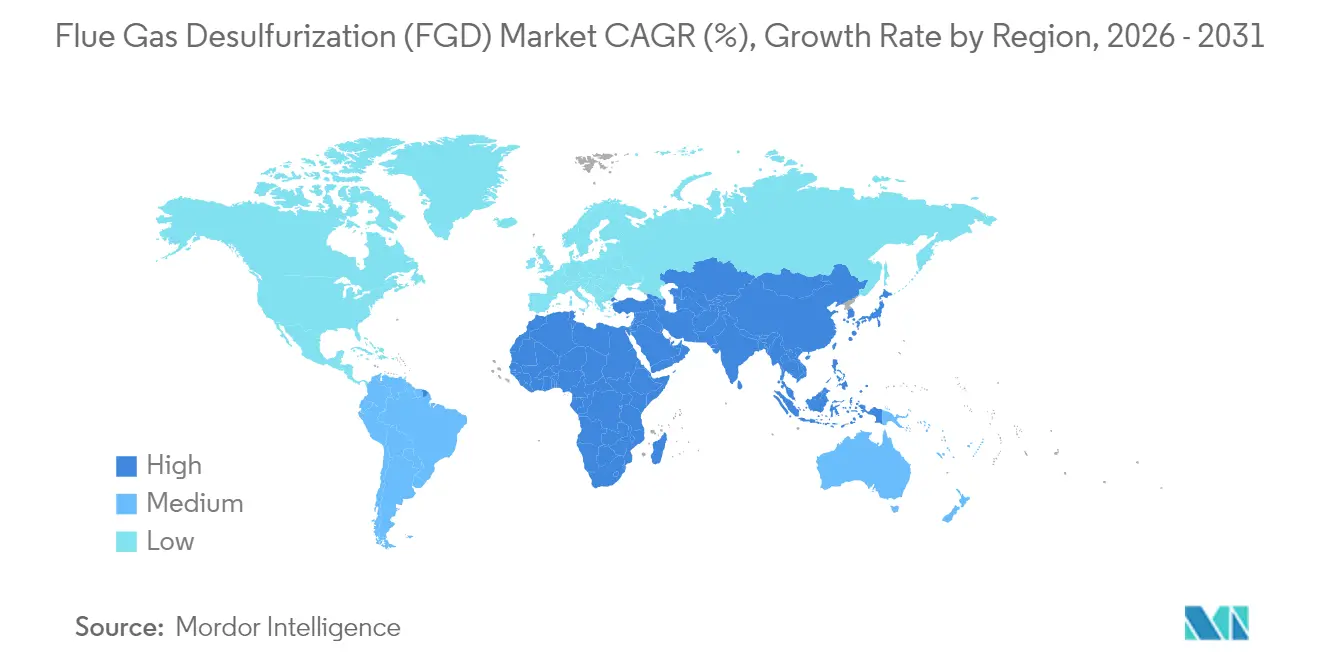

- By geography, Asia-Pacific held 61.70% revenue share of the flue gas desulfurization market in 2025; Europe is set to expand at a 6.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Flue Gas Desulfurization (FGD) Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent SO₂-emission caps in coal-fired power plants | +2.10% | China, EU, North America | Medium term (2-4 years) |

| Mandatory retrofits of aging industrial boilers & kilns | +1.80% | APAC core, Europe, North America | Long term (≥ 4 years) |

| Rising demand for FGD-derived synthetic gypsum | +1.20% | North America, Europe | Short term (≤ 2 years) |

| Integration of FGD with carbon-capture retrofits | +0.90% | Europe, North America opening to APAC | Long term (≥ 4 years) |

| IMO rules driving high-sulfur marine fuel scrubbers | +0.70% | Global maritime corridors | Medium term (2-4 years) |

| Predictive-maintenance analytics lowering OPEX | +0.50% | OECD markets, spreading to emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent SO₂-Emission Caps in Coal-Fired Power Plants

Global alignment on sulfur-oxide limits is reshaping procurement calendars. China’s ultra-low emission code caps SO₂ at 35 mg/Nm³ and achieves 99% capture through limestone-gypsum loops. The EU’s revised Industrial Emissions Directive imposes tighter benchmarks for large combustion plants, compelling upgrades across legacy fleets.[1] European Commission, “Revision of the Industrial Emissions Directive,” eur-lex.europa.eu The US Environmental Protection Agency finalized a 2024 rule obligating residual coal units to meet stringent hourly sulfur ceilings, catalyzing retrofits in Midwest and Appalachian stations.[2]US Environmental Protection Agency, “Effluent Limitation Guidelines 2024 Update,” epa.gov In Poland, mandated installations lifted limestone use from negligible in 1994 to 3.4 million t/y by 2019 as capture efficiencies passed the 90% mark. Compliance accelerators such as automatic reagent optimization, modular absorber sections, and dual-alkali loops reduce downtime, reinforcing a replacement cycle that lengthens the economic life of installed reactors even as coal dispatch inches downward.

Mandatory Retrofits of Aging Industrial Boilers & Kilns

Industrial point sources below 50 MW thermal capacity now fall under the EU Medium Combustion Plant Directive, multiplying the addressable base by thousands of lignite dryers, kilns, and refinery heaters. Cement plants reveal favorable economics because flue moisture can be reused for raw-meal conditioning, offsetting utility costs. Heidelberg Materials’ USD 500 million Mitchell upgrade in Indiana targets a 2 million t/y CO₂ capture plateau, pairing amine absorption with a new FGD pretreatment train. Similar archetypes materialize in non-ferrous smelters, where elemental-sulfur recovery couples revenue streams with compliance credit sales. Retrofits therefore gravitate toward multi-contaminant kits delivering incremental mercury and NOₓ abatement, making the flue gas desulfurization market a cross-sector platform for integrated pollution control.

Rising Demand for FGD-Derived Synthetic Gypsum

Coal retirements shrink gypsum output even as wallboard and soil conditioner demand rise in North America and parts of Europe. FGD gypsum’s uniform particle size and low radionuclide trace align with green-building protocols, allowing wallboard plants to displace natural mined feedstock and cut logistics expenditure. Producers monetize the by-product by installing dewatering presses that yield 96% solids and marketable granules. Transportation radius remains the limiting factor, pressing operators to forge local offtake pacts and enhance bulk-terminal handling. Consequently, waste-treatment costs decline, raising the internal rate of return for limestone-gypsum facilities and cushioning the flue gas desulfurization market against fuel-mix volatility.

Integration of FGD with Carbon-Capture Retrofits

FGD absorbers and carbon-capture columns share fans, ducts, and mist-elimination gear; repurposing hardware can shave 12–18% from combined capital outlays. Norway’s Brevik CCS project demonstrates synergy: an existing absorber front-ends a 400,000 t/y solvent train, exploiting waste heat for regeneration. Mitsubishi Heavy Industries' CO₂MPACT™ modules capture 1–200 t CO₂/d and bolt onto limestone-gypsum loops without major civil works, targeting cement, steel, and waste-to-energy sites. Proof points spur utilities to future-proof units by oversizing fans and piping to accommodate later carbon capture connections, extending revenue certainty under evolving decarbonization legislation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX & disposal costs of wet FGD sludge | –1.4% | Emerging economies | Short term (≤ 2 years) |

| Coal-to-renewables shift curbing new installations | –1.1% | OECD power markets | Long term (≥ 4 years) |

| Limestone supply-chain bottlenecks & price volatility | –0.8% | Regional high-demand pockets | Medium term (2-4 years) |

| Zero-liquid-discharge rules inflating water-use costs | –0.6% | North America, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX & Disposal Costs of Wet FGD Sludge

Installation expenses near INR 12 million/MW hinder India’s rollout, prompting advisory panels to question blanket mandates. Disposal charges escalate where sludge requires thermal drying or leachate sealing, lifting the levelized cost of electricity by up to USD 3/MWh in emerging grids. Zero-liquid-discharge prescriptions magnify water treatment capital; Pennsylvania’s Homer City power station invested USD 750 million in a compliant evaporator crystallizer train before closing in 2024. As a result, dry sorbent injection garners interest despite lower capture efficiency, creating a price ceiling for the flue gas desulfurization market in capital-constrained regions.

Coal-to-Renewables Shift Curbing New Installations

US utilities will retire 8.1 GW of coal in 2025, sliding to 145 GW by 2028. An average unit age of 50 years dampens retrofit appetite because payback periods exceed remaining asset lives, steering managers toward accelerated closure. European operators follow a similar path, retiring over 10 GW since 2023 as carbon prices surge. Yet India’s USD 33 billion slate of new coal builds, coupled with Indonesia’s 30 GW pipeline, offsets OECD softness, reallocating the growth center of the flue gas desulfurization market eastward.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Wet Systems Dominate Despite Hybrid Innovation

Wet limestone-gypsum reactors represented 86.92% of the flue gas desulfurization market share in 2025, cemented by >95% SO₂ capture efficiencies under ultra-low emission codes in China. At a flue gas desulfurization market size of USD 22.63 billion, the type thrives on established vendor ecosystems and stable sorbent supply chains. Hybrid and sorbent-injection variants, while accounting for a modest revenue slice, clocked a 9.65% CAGR and attracted industrial retrofits where space or water scarcity constrains wet designs.

Operators favor proven wet loops for high-sulfur, high-volume stacks, yet innovation accelerates around circulating fluidized bed scrubbers that fold in particulate removal, cutting electrostatic precipitator capital outlay. Tri-Mer’s SorbSaver system, for example, integrates dry sorbent dispersion with low-energy baghouses and lowers reagent overdosing by up to 40%, aligning with budgets in sub-25 MW industrial boilers. The coexistence of established and novel designs expands supplier addressable revenue as users layer hybrid kits onto legacy absorbers, sustaining healthy competition within the flue gas desulfurization market.

By Reagent/Sorbent: Limestone Leads While Sodium Systems Accelerate

Limestone captured 62.95% of the flue gas desulfurization market size in 2025, reflecting abundant reserves and low delivered cost in major coal belts. Premium 53% CaO grades fetch higher prices in steelmaking regions, yet utilities typically secure multi-year quarry supply, stabilizing OPEX. Lime, seawater alkalinity, and magnesium hydroxide fill niche duty cycles, particularly along coastal refineries.

Sodium-based sorbents are growing at an 8.22% CAGR as maritime and small industrial users prioritize compact, simple hardware. Hitachi Zosen Inova’s Xerosorp dry reactor posts 94% SO₂ capture on sodium bicarbonate, requiring minimal water input and producing a salable reacted salt cake. Comparative research shows sodium bicarbonate achieves lower residual emissions than limestone under low-temperature spray conditions. Thus, reagent diversification mitigates supply shocks and gives plant owners a menu of sorbents calibrated to site logistics, a trend reshaping future competitive positioning across the flue gas desulfurization market.

By End-User Industry: Power Generation Stable While Cement Surges

The power sector retained 71.15% of 2025 revenue, underpinned by mandatory retrofits in India, Indonesia, and Vietnam. Although coal dispatch wanes in OECD grids, integration with carbon-capture systems sustains retrofit appetite where capacity remains indispensable for grid inertia. Cement kilns, however, post the sharpest 7.86% CAGR as direct-process emissions necessitate stack scrubbing regardless of fuel mix. The segment’s flue gas desulfurization market size is projected to double by 2030 as producers pair SO₂ removal with CO₂ capture to hedge future carbon fees.

Steelmakers rank next, with sinter plants and hot-strip mills installing wet scrubbers that dovetail with limestone flux logistics. Chemicals and petrochemicals adopt corrosion-resistant alloys and dual-alkali designs that withstand chlorine and sulfuric acid traces, extracting higher average selling prices for vendors. Collectively, industrial diversification lessens reliance on the utility cycle, reinforcing stable mid-single-digit expansion across the flue gas desulfurization market.

Geography Analysis

Asia-Pacific commands 61.70% of 2025 revenue and will tack on a 6.98% CAGR through 2031, anchored by China’s >95% wet-system penetration and India’s multi-gigawatt pipeline despite intermittent policy debate. Vietnam, Indonesia, and the Philippines incentivize SO₂ control upgrades via concessional lending, adding density to regional vendor service networks. Japan and South Korea specialize in marine scrubber supply, leveraging shipyard ecosystems to export turnkey kits across global fleets.

Europe enforces the world’s strictest emission ceilings, spurring retrofits in small-to-medium industrial plants. Germany, Belgium, and Poland invest heavily in absorber upgrades linked to carbon-capture pilots under the EU Innovation Fund, positioning the region as a technology incubator. Nordic maritime regulations accelerate the adoption of closed-loop scrubbers, export regulatory templates worldwide, and sustain European equipment backlogs.

North America experiences structural attrition in utility coal capacity, yet industrial adopters buoy order intake. Cement plants in the United States advance with USD 500 million-plus CCUS retrofits that assume FGD bleeds for solvent protection. Canada tightens sulfur limits in oil-sands boilers, stimulating fresh package-plant bids, while Mexican utilities outline modernization roadmaps aligning with updated NOM-085-SEMARNAT limits. South America and the Middle East & Africa contribute single-digit revenue shares but deliver sporadic large orders tied to refinery expansions, fertiliser complexes, and copper smelters, offering long-cycle prospects for globally active OEMs.

Competitive Landscape

The flue gas desulfurization market presents a moderately concentrated structure where the top five suppliers control 55–60% of installed capacity revenues. Mitsubishi Heavy Industries recorded a record ¥7,071.2 billion order intake in FY 2024, buoyed by turbine upgrades and CCUS-ready scrubbers.[4]Mitsubishi Heavy Industries, “MHI Report 2024,” mhi.com ANDRITZ’s USD 100 million acquisition of LDX Solutions in February 2025 broadens its wet electrostatic and thermal oxidizer lineup, strengthening cross-sell potential into pulp, mining, and power segments.[5]ANDRITZ AG, “Acquisition of LDX Solutions,” andritz.com

GE Vernova collaborates with Svante on carbonate looping and is studying exhaust-gas recirculation under a US Department of Energy grant, signaling convergence of sulfur and carbon mitigation on modular skids GEVernova.com. Alfa Laval and Wärtsilä dominate maritime scrubbers, leveraging thousands of reference installations and robust global service stations. Chinese heavy-machinery integrators such as Dongfang Boiler and Babcock & Wilcox Beijing supply cost-optimized wet loops that secure domestic share yet increasingly bid on Southeast-Asian tenders.

Competitive levers hinge on lifecycle support, digital twins, and reagent-optimization software that reduce operating expense rather than headline capex alone. Suppliers with a wide portfolio spanning wet, dry, and hybrid designs and carbon-capture attachments enjoy a hedge against changing fuel mixes and regulatory escalations.

Flue Gas Desulfurization (FGD) Industry Leaders

Mitsubishi Heavy Industries Environmental & Chemical Engg.

GE Vernova (incl. Alstom legacy)

Babcock & Wilcox Enterprises Inc.

Fujian Longking Co. Ltd

Andritz AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: ANDRITZ AG finalized the USD 100 million purchase of LDX Solutions, adding over 2,000 installed environmental systems and 250 specialists to its North American footprint.

- January 2025: Cemex Knoxville won USD 101 million in DOE backing for a carbon-capture test center in partnership with the University of Illinois Urbana-Champaign.

- October 2024: Cemex secured EUR 157 million from the EU Innovation Fund for a 1.3 million t CO₂ capture project at Rüdersdorf, Germany, employing HISORP technology.

- September 2024: Mitsubishi Heavy Industries unveiled a modular CO₂MPACT overhaul enabling mass-produced units sized 1–200 t CO₂/d for cement, steel, and waste-to-energy stacks.

Global Flue Gas Desulfurization (FGD) Market Report Scope

The flue gas desulfurization (FGD) market report include:

| Wet FGD | Limestone/Gypsum Wet Scrubbers |

| Seawater Scrubbers | |

| Dry and Semi-Dry FGD | Spray-Dry Absorbers |

| Circulating Fluidized-Bed Dry Scrubbers | |

| Hybrid and Advanced Sorbent Injection |

| Limestone |

| Lime |

| Seawater |

| Sodium-based and Other Alkalis |

| Power Generation |

| Cement |

| Iron and Steel |

| Chemical and Petrochemical |

| Non-Ferrous Metals |

| Waste-to-Energy and Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Wet FGD | Limestone/Gypsum Wet Scrubbers |

| Seawater Scrubbers | ||

| Dry and Semi-Dry FGD | Spray-Dry Absorbers | |

| Circulating Fluidized-Bed Dry Scrubbers | ||

| Hybrid and Advanced Sorbent Injection | ||

| By Reagent/Sorbent | Limestone | |

| Lime | ||

| Seawater | ||

| Sodium-based and Other Alkalis | ||

| By End-User Industry | Power Generation | |

| Cement | ||

| Iron and Steel | ||

| Chemical and Petrochemical | ||

| Non-Ferrous Metals | ||

| Waste-to-Energy and Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the flue gas desulfurization market by 2031?

The flue gas desulfurization market size is forecast to reach USD 37.03 billion by 2031.

Which region currently dominates revenue?

Asia-Pacific held 61.70% of global revenue in 2025 due to expansive Chinese and Indian coal fleets and growing industrial retrofits.

Why are wet limestone-gypsum systems still preferred?

They deliver >95% SO₂ removal, meet ultra-low emission codes, and benefit from mature supply chains, ensuring predictable lifecycle costs.

How fast is the cement segment growing?

Cement applications are advancing at an 7.86% CAGR through 2031 as plants pair SO₂ removal with CO₂-capture retrofits.

Will carbon-capture integration change FGD specifications?

Yes. New absorbers are often oversized and equipped with corrosion-resistant alloys to accommodate future CO₂ solvent systems, lowering total retrofit costs.

What factors may restrain new installations?

High capital costs, sludge disposal expenses, and accelerated coal retirements in OECD markets act as primary headwinds.

Page last updated on: