Burn Care Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 2.88 Billion |

| Market Size (2030) | USD 3.96 Billion |

| Growth Rate (2025 - 2030) | 6.56% CAGR |

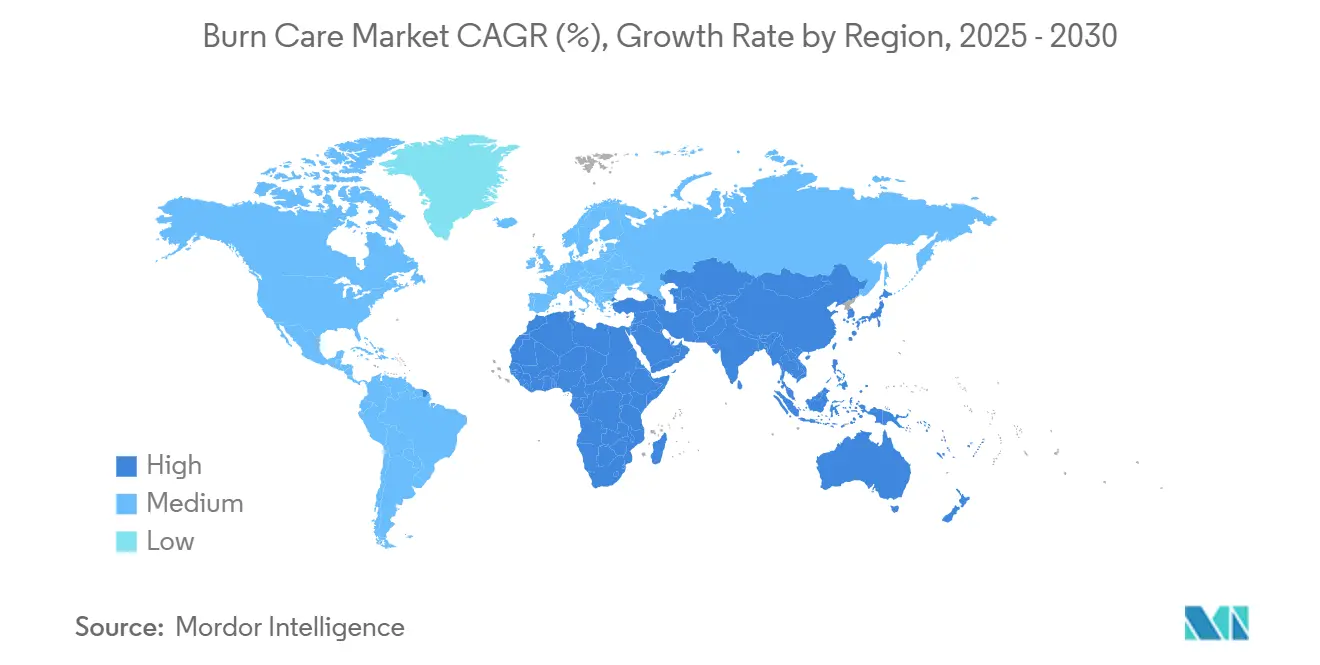

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Burn Care Market Analysis by Mordor Intelligence

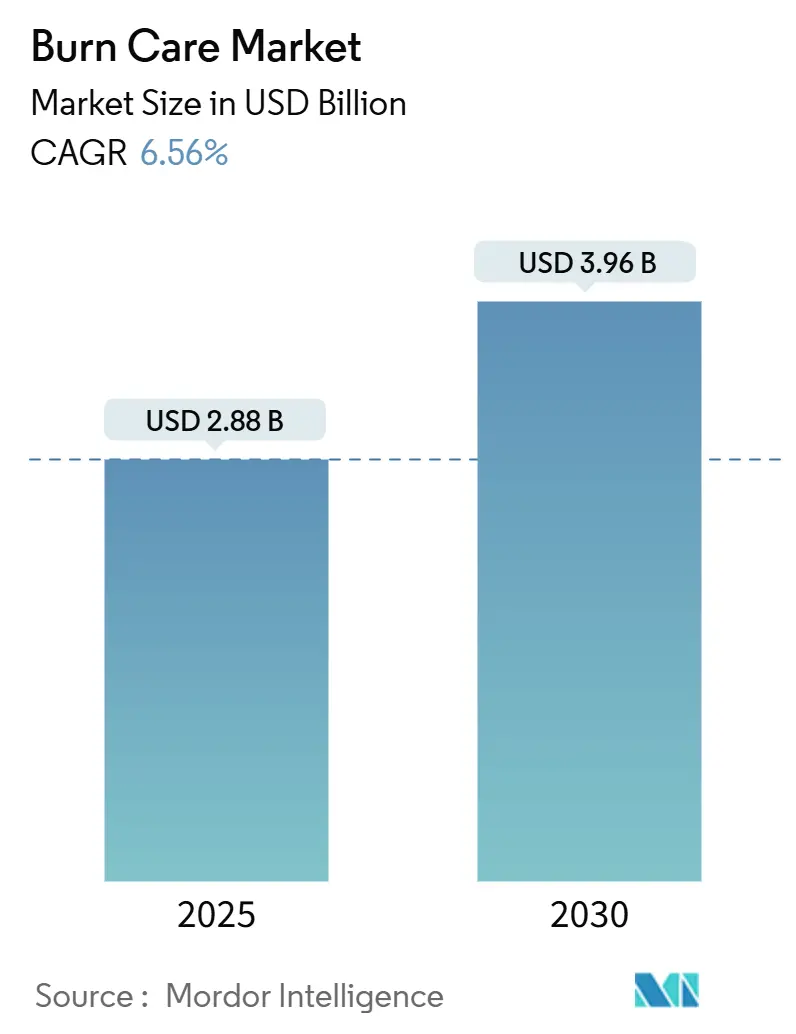

The Burn Care Market size is estimated at USD 2.88 billion in 2025, and is expected to reach USD 3.96 billion by 2030, at a CAGR of 6.56% during the forecast period (2025-2030).

Severe weather events, electric-vehicle battery fires, and industrial accidents continue to elevate the global incidence of burn injuries, sustaining demand for advanced dressings, biologics, and portable negative-pressure therapy systems. Reimbursement reforms in the United States, Europe, and selected Asia-Pacific economies support wider adoption of sophisticated wound technologies. Meanwhile, ambient-intelligence tools such as smart bandages and bioelectronic monitors shorten healing times and reduce readmissions, driving hospital cost-containment strategies. Strategic investments from public research programs and military agencies accelerate translation of laboratory breakthroughs into commercial products.

Key Report Takeaways

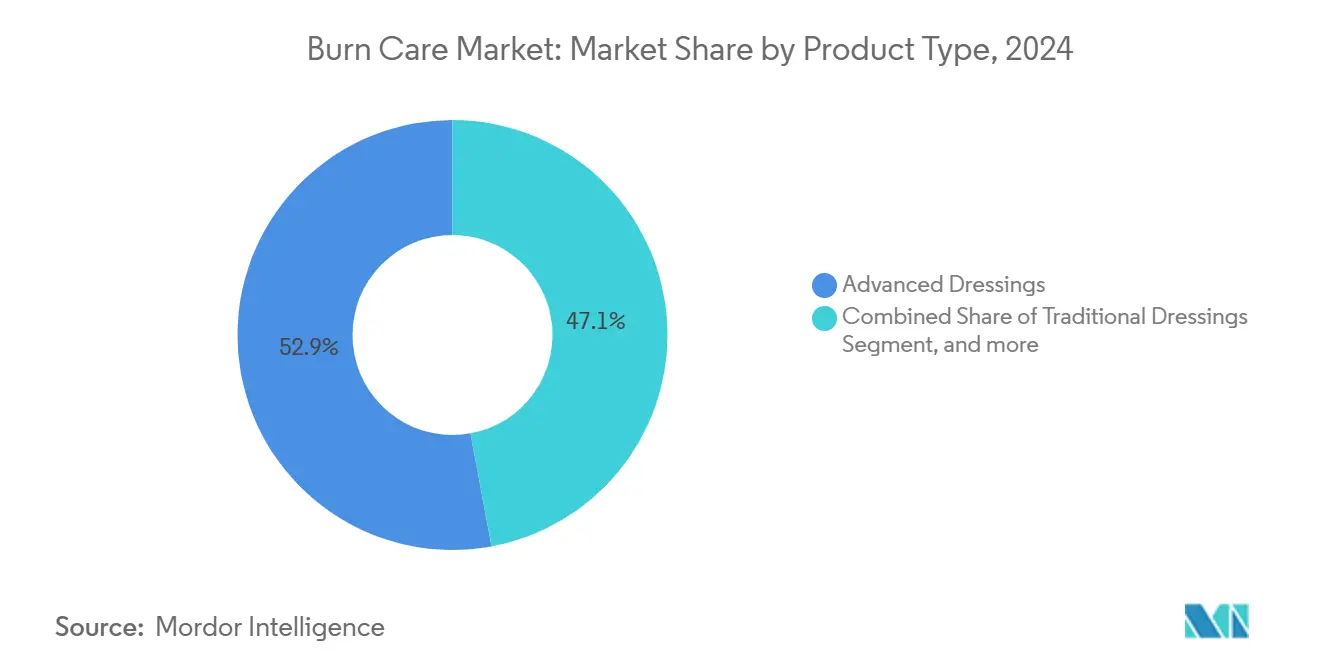

- By product type, advanced dressings led with 52.87% burn care market share in 2024, while biologics recorded the fastest 9.83% CAGR through 2030.

- By depth of burn, partial-thickness cases accounted for 43.94% of the burn care market size in 2024, whereas full-thickness burns are projected to expand at an 8.73% CAGR.

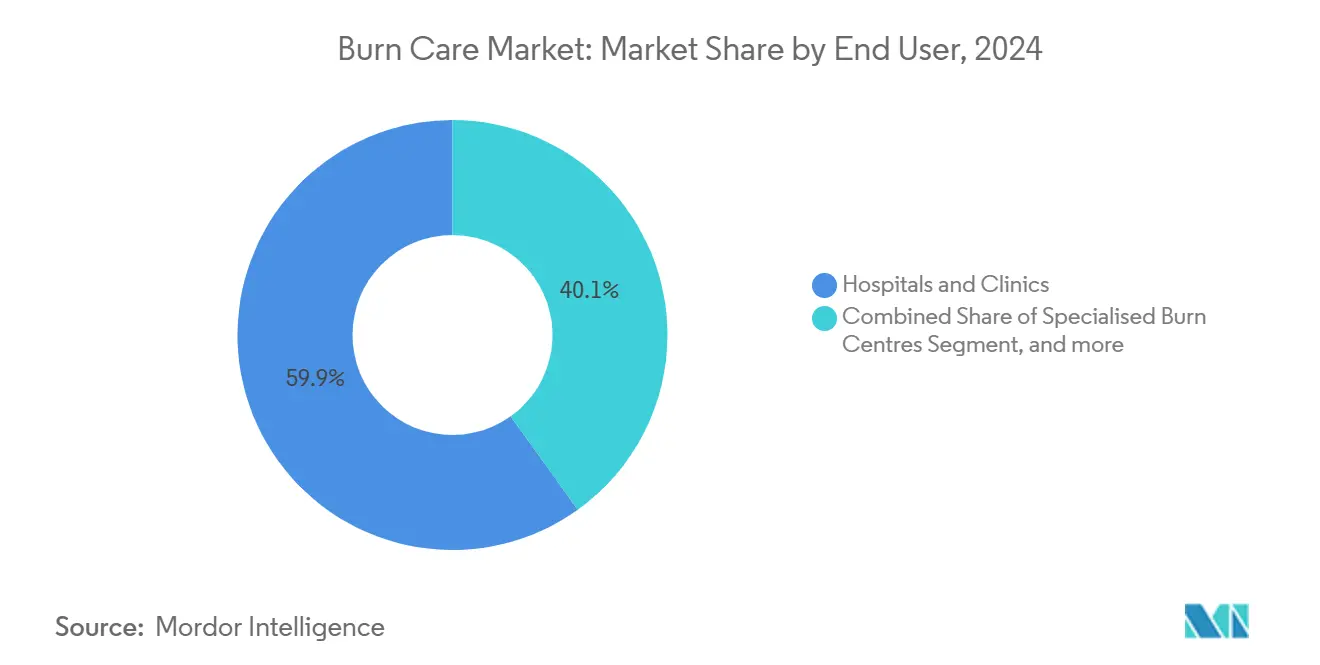

- By end user, hospitals and clinics held 59.92% revenue in 2024; ambulatory surgery centers are forecast to grow 10.19% annually to 2030.

- By geography, North America dominated with 39.74% of 2024 sales, and Asia-Pacific is expected to grow at an 8.16% CAGR through 2030.

Global Burn Care Market Trends and Insights

Drivers Impact Analysis

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High incidence of burn injuries worldwide | +1.2% | Global wildfire-prone zones | Long term (≥ 4 years) |

| Adoption of advanced wound dressings and skin grafts | +1.8% | North America & Europe spreading to Asia-Pacific | Medium term (2-4 years) |

| Rapid technological advances in NPWT, antimicrobial hydrogels, 3-D bioprinting | +2.1% | Worldwide led by North America & Europe | Short term (≤ 2 years) |

| Favourable reimbursement and government safety initiatives | +0.9% | North America, Europe, selected Asia-Pacific | Medium term (2-4 years) |

| Rising electric-vehicle and lithium-battery fire incidents | +0.3% | North America, Europe, China | Short term (≤ 2 years) |

| Climate-linked wildfire frequency | +0.7% | US West Coast, Australia, Mediterranean Europe | Long term (≥ 4 years) |

Source: Mordor Intelligence

High Incidence of Burn Injuries Worldwide

Wildfires in Central Canada burned 2.7 million hectares in 2025 and forced 33,000 evacuations, pushing emergency departments to an eightfold surge in burn-related visits. The January 2025 Los Angeles fires destroyed 16,250 structures and exposed 41,000 residents, illustrating the escalating clinical burden.[1]United Nations University, “Wildfire Losses and Health Impacts 2025,” unu.edu Chronic wound management, including burns, carries an annual economic load surpassing USD 20 billion in the United States. Pediatric trials with non-thermal plasma cut skin-graft needs from 40% to 10%.[2]Y. Chen et al., “Plasma Therapy in Pediatric Burns,” mdpi.com These data point toward sustained allocation of resources across global health systems.

Increasing Adoption of Advanced Wound Dressings & Skin Grafts

Smith+Nephew posted 3.8% underlying growth in its Advanced Wound Management unit during Q1 2025, reflecting robust demand for foams and NPWT devices. The Red Dot-awarded RENASYS EDGE system addresses the needs of 8.2 million American chronic-wound patients at a USD 33 billion financial burden. Silver-nanoparticle and collagen matrices achieve 50-95% healing rates across diverse cohorts. Solventum’s V.A.C. Peel & Place cut application time by 61% and costs by 41% while supporting seven-day wear. Healthcare purchasers therefore continue to favour clinically proven dressings that also reduce total cost of care.

Rapid Technological Advances (NPWT, Antimicrobial Hydrogels, 3-D Bioprinting)

Caltech’s iCares smart bandage delivers real-time diagnostics and machine-learning-based healing predictions with expert accuracy.[3]Science Translational Medicine, “Smart Bandage for Burn Healing,” caltech.edu Three-dimensional bioprinted nanofiber scaffolds show improved adhesion and controlled degradation for full-thickness wounds. Conductive hydrogels containing deep-eutectic solvents stimulate tissue repair through low-intensity electrical fields. MedStar Health paired dynamic thermography with laser Doppler imaging to anticipate wound conversion, enabling earlier intervention. Such tools shorten healing times and limit infection-related readmissions.

Favourable Reimbursement & Government Safety Initiatives

CMS reclassified skin substitutes as wound-care management products in April 2025, expanding application limits and introducing new documentation standards. The 2025 Physician Fee Schedule added caregiver training codes G0541-G0543, supporting telehealth engagement. The Military Burn Research Program committed USD 650 million to triage and treatment technologies designed for austere settings. Compliant suppliers gain advantage under the updated rules.

Restraints Impact Analysis

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced products and biologics | -1.4% | Global emerging markets | Medium term (2-4 years) |

| Limited reimbursement and skilled staff | -0.8% | Asia-Pacific, Latin America, Africa | Long term (≥ 4 years) |

| Stringent biologic regulatory pathway | -0.6% | North America, Europe, selected Asia-Pacific | Medium term (2-4 years) |

| Raw-material supply volatility | -0.4% | Global manufacture hubs | Short term (≤ 2 years) |

Source: Mordor Intelligence

High Cost of Advanced Burn-Care Products & Biologics

Medicare investigations into inflated skin-substitute pricing spotlight financial barriers in the burn care market. Integra LifeSciences saw Tissue Technologies revenue fall 15.3% in Q1 2024 due to production outages, underscoring supply risk. DOJ action against Vohra Wound Physicians accentuates compliance pressure. Accountable Care Organizations advocate stricter controls to safeguard budgets. High sticker prices thus temper biologic uptake, especially outside high-income economies.

Limited Reimbursement & Skilled Staff in Emerging Economies

Asia-Pacific still shows the fastest trajectory yet faces gaps in certified wound nurses, hindering the burn care market. Home-health teams struggle with complex dressing protocols, and limited insurance hampers broad technology deployment. A regional consensus on standardized burn assessment called for investment in professional development and telehealth infrastructure. Solutions such as WoundConnect reduced in-person visits while keeping clinical outcomes stable. Nevertheless, progress remains uneven across developing regions.

Segment Analysis

By Product Type: Advanced Dressings Retain Leadership Amid Biologic Surge

Advanced dressings held 52.87% market share, of the burn care market in 2024. Iterative upgrades in hydrofiber foams, antimicrobial silver layers, and moisture-handling backings maintain clinician confidence and secure reimbursement. Smith+Nephew expanded its foam line in 2024, reinforcing stickiness within hospital formularies. Traditional dressings persist in budget-sensitive outpatient settings, sustaining baseline demand. Therapy devices, notably portable NPWT units, speed patient discharge and bolster outpatient revenue models. Topical antimicrobial gels remain standard prophylaxis for minor wounds.

Biologics, while smaller in absolute value, recorded 9.83% CAGR from 2025 to 2030, the highest across product categories. FDA clearance of AVITA Medical’s Cohealyx dermal matrix in December 2024 widens indications and triples the firm’s total addressable population. Bioengineered skin delivers outcomes similar to autografting without donor-site morbidity. However, the burn care market size for biologics stays curtailed by high manufacturing cost and complex cold-chain logistics. As payers refine coverage criteria, vendors that generate robust comparative-effectiveness data will gain share.

Note: Segment shares of all individual segments available upon report purchase

By Depth of Burn: Prevalence of Partial-Thickness Dominates as Full-Thickness Gains Momentum

Partial-thickness injuries comprised 43.94% of the burn care market in 2024, benefiting from established moist-healing protocols and outpatient care pathways. Patients typically receive hydrogel or silicone dressings that minimize trauma on changes, reducing infection risk and scarring. Minor wounds, often treated at home or in urgent-care settings, drive demand for accessible dressings and analgesic sprays. Clinician familiarity, predictable healing times, and lower material cost sustain steady revenue.

Full-thickness burns, although fewer in case volume, will rise at an 8.73% CAGR to 2030. The January 2025 Los Angeles fires exposed tens of thousands of residents, highlighting the need for highly specialized reconstruction. Advanced dermal matrices from Integra anchor staged reconstruction algorithms that now achieve higher survival rates. Growth accelerates as critical-care capabilities improve outside traditional burn centers, expanding geographical availability of complex surgeries. The burn care market size for these severe presentations therefore shows disproportionate revenue contribution compared with case count.

By End User: Hospitals Dominate While Ambulatory Centers Expand

Hospitals and clinics accounted for 59.92% of 2024 revenue in the burn care market. Level I burn centers integrate intensive care, surgical suites, and rehabilitation teams to manage complex trauma. The USD 650 million Military Burn Research Program funds innovations such as deployable resuscitation units, reinforcing hospital capabilities. Emergency departments also function as gatekeepers, initiating NPWT or graft placement before step-down to outpatient settings.

Ambulatory surgery centers are expected to register a 10.19% CAGR through 2030 as portable NPWT and advanced dressings enable same-day procedures. Smart bandages like iCares permit real-time monitoring outside hospital walls, giving clinicians confidence to shorten inpatient stays. Reimbursement incentives for site-of-service shifts, together with patient preference for home recovery, support ambulatory adoption. Vendors tailoring packaging and staff training for outpatient workflows will capture incremental opportunities in the burn care market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America held 39.74% of global revenue in 2024. Federal investments, including the USD 650 million Military Burn Research allocation, promote basic and translational science. CMS updates on skin-substitute coverage effective April 2025 further incentivize technology uptake. The Los Angeles wildfires exposed 41,000 people and demonstrated the region’s vulnerability. Canadian wildfires affected 2.7 million hectares and sent smoke toward 117 million Americans, indicating cross-border healthcare contingencies.

Europe combines strict regulatory oversight with rising wildfire activity around the Mediterranean. Healthcare systems focus on cost-effectiveness, prompting hospitals to adopt dressings that reduce total hospitalization days. Joint EU research programs foster collaboration between academic groups and device makers, accelerating approvals of smart hydrogel dressings.

Asia-Pacific is projected to achieve an 8.16% CAGR to 2030. Policymakers prioritize universal health coverage and invest in trauma infrastructure, creating strong tailwinds in the burn care market. A region-wide consensus issued new burn-assessment guidelines and emphasized workforce training. Private-equity interest grows as healthcare providers consolidate and seek digital-health partnerships.

Middle East & Africa and South America remain nascent yet show steady uptake of portable NPWT and silver dressings. Governments modernize emergency services to meet climate-related disaster demands. Multilateral aid and public-private collaborations introduce telehealth solutions for remote burn triage, gradually expanding the burn care market footprint in underserved regions.

Competitive Landscape

The competitive arena features diversified multinationals and agile biotech entrants. Smith+Nephew generated USD 5.5 billion sales in 2023 and leverages scale to bundle foams, infection-control products, and surgical tools. 3M separated its healthcare assets into Solventum, inheriting USD 340 million in federal contracts for NPWT systems. Integra LifeSciences anchors its USD 1.6 billion regenerative portfolio with AI-enabled wound analytics that guide graft decisions.

Disruptors target niche opportunities. Caltech’s iCares smart bandage integrates sensors and predictive algorithms, offering hospitals a data-rich alternative to conventional dressings. Start-ups in 3-D bioprinting supply custom scaffolds for full-thickness reconstructions. Patent filings on conductive hydrogels and polymer nanofibers accelerate as firms seek defensible IP. Heightened DOJ action over false claims raises compliance costs, favouring players with robust governance.

Strategic moves include partnerships with telehealth providers to track outpatients, licensing of antimicrobial coatings, and regional acquisitions that add distribution scale. Vendors also explore value-based contracts where reimbursement ties to documented healing outcomes, aligning incentives with payers and accountable-care organizations in the burn care industry.

Burn Care Industry Leaders

-

Johnson & Johnson

-

Mölnlycke Health Care AB

-

3M Company

-

Smith & Nephew plc

-

Cardinal Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Caltech researchers launched the iCares smart bandage system capable of real-time wound monitoring and machine-learning-driven healing predictions, with clinical trials in 20 human patients demonstrating expert-level accuracy in predicting healing outcomes. The breakthrough technology received support from multiple health and research organizations and findings were published in Science Translational Medicine.

- April 2025: The Centers for Medicare & Medicaid Services implemented comprehensive updates for skin substitutes effective April 13, 2025, expanding application limits and introducing new documentation requirements while reclassifying these products as 'wound care management products' to streamline coding and payment under the Physician Fee Schedule.

- April 2025: The 2025 Military Burn Research Program allocated USD 650 million through the Congressionally Directed Medical Research Program, focusing on prevention, triage, and treatment innovations for austere environments with funding opportunities ranging from USD 200,000 to USD 1.7 million.

- January 2025: ConvaTec welcomed the postponement of Local Coverage Determinations on skin substitutes in the United States, potentially impacting the availability and reimbursement of these products in the burn care market.

Global Burn Care Market Report Scope

As per the scope of the report, burn care products are specially formulated to heal burn wounds. Burn can cause skin cells to die and a painful burning sensation to the skin. Immediate emergency care must be provided in case of serious burns to avoid complications or even death. Burn care products help relieve discomfort and prevent scarring. The Burn Care Market is Segmented By Product Type (Advanced Dressing, Traditional Dressing, Biologics, and Other Product Types), Depth of Burn (Minor Burns, Partial Thickness Burns, Full Thickness Burns), End User (Hospitals & Clinics, Ambulatory Surgery Center, Others) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| By Product Type | Advanced Dressings | Foam Dressings | |

| Hydrocolloid Dressings | |||

| Hydrogel Dressings | |||

| Alginate Dressings | |||

| Antimicrobial Silver Dressings | |||

| Collagen & Silicone Dressings | |||

| Traditional Dressings | |||

| Biologics | |||

| Therapy Devices | |||

| Topical Agents | |||

| Other Product Types | |||

| By Depth of Burn | Minor Burns | ||

| Partial-Thickness Burns | |||

| Full-Thickness Burns | |||

| By End User | Hospitals & Clinics | ||

| Specialised Burn Centres | |||

| Ambulatory Surgery Centres | |||

| Home-Care Settings | |||

| Military & Emergency Services | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Advanced Dressings | Foam Dressings |

| Hydrocolloid Dressings | |

| Hydrogel Dressings | |

| Alginate Dressings | |

| Antimicrobial Silver Dressings | |

| Collagen & Silicone Dressings | |

| Traditional Dressings | |

| Biologics | |

| Therapy Devices | |

| Topical Agents | |

| Other Product Types |

| Minor Burns |

| Partial-Thickness Burns |

| Full-Thickness Burns |

| Hospitals & Clinics |

| Specialised Burn Centres |

| Ambulatory Surgery Centres |

| Home-Care Settings |

| Military & Emergency Services |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size of the burn care market?

The burn care market stood at USD 2.88 billion in 2025 and is projected to reach USD 3.96 billion by 2030.

Which product category dominates revenue?

Advanced dressings accounted for 52.87% of 2024 revenue, making them the leading product segment.

Which region is growing fastest?

Asia-Pacific is forecast to expand at an 8.16% CAGR between 2025 and 2030 because of rising healthcare investment and standardized treatment protocols.

Why are ambulatory surgery centers important for future growth?

Portable NPWT devices and smart bandages enable complex wound management outside hospitals, driving a 10.19% CAGR for ambulatory centers through 2030.

How are technology advances shaping burn care?

Real-time sensors, conductive hydrogels, and 3-D bioprinting accelerate healing, reduce infections, and shorten inpatient stays, shifting budgets toward data-enabled solutions.

What challenges limit adoption of biologics?

High manufacturing costs, stringent regulatory pathways, and reimbursement scrutiny in emerging markets constrain widespread biologic uptake despite strong clinical performance.

Page last updated on: July 1, 2025