Europe Tumble Dryers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.85 Billion |

| Market Size (2026) | USD 2.96 Billion |

| Market Size (2031) | USD 3.39 Billion |

| Growth Rate (2026 - 2031) | 2.75% CAGR |

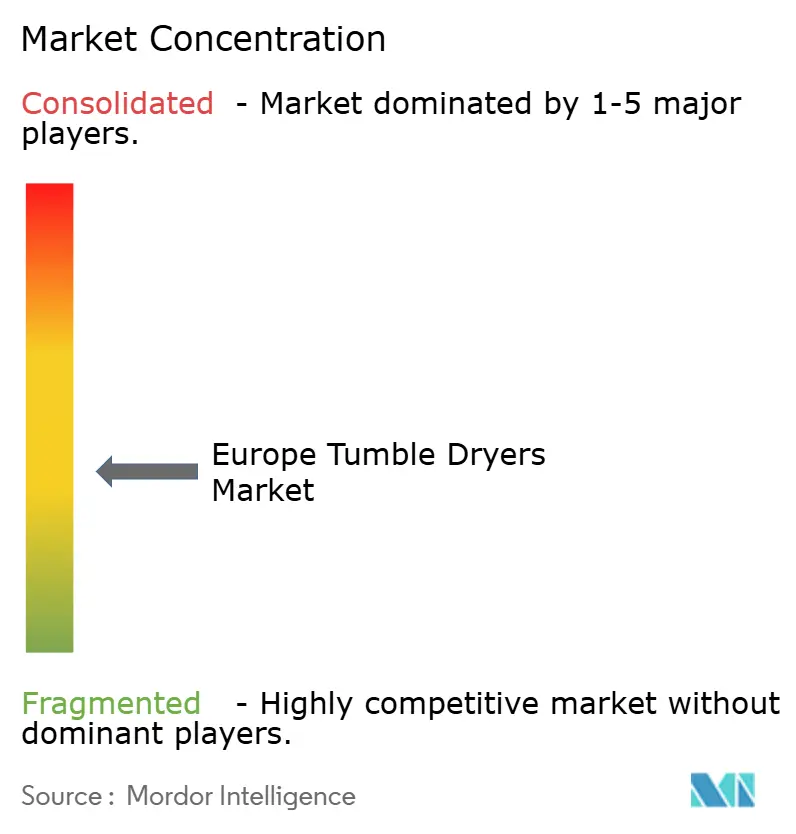

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Tumble Dryers Market Analysis by Mordor Intelligence

The Europe tumble dryers market size is projected to be USD 2.85 billion in 2025, USD 2.96 billion in 2026, and reach USD 3.39 billion by 2031, growing at a CAGR of 2.75% from 2026 to 2031. The upgrade cycle is being shaped by the EU ecodesign mandate that took effect on July 1, 2025, which effectively ended market placement of vented and entry-level condenser dryers and set A-class ratings as exclusive to heat-pump models, concentrating technology choices for new placements[1]Directorate General for Energy, “New Measures for More Energy Efficient Household Tumble Dryers from 1 July,” European Commission, ec.europa.eu . The new A to G energy label format with QR-code access to EPREL data is steering buyers toward high-efficiency units as vendors emphasize transparency on energy and condensation performance. Persistently elevated household electricity prices since the energy crisis, together with the EU’s 2030 climate goals, continue to reinforce the value proposition for heat-pump adoption in both consumer and professional settings across the Europe tumble dryers market. Competitive activity is coalescing around a small group of integrated brands that are scaling heat-pump manufacturing, connectivity, and lifecycle compliance features to meet EU requirements and service emerging utility-aligned use cases in the Europe tumble dryers market.

Key Report Takeaways

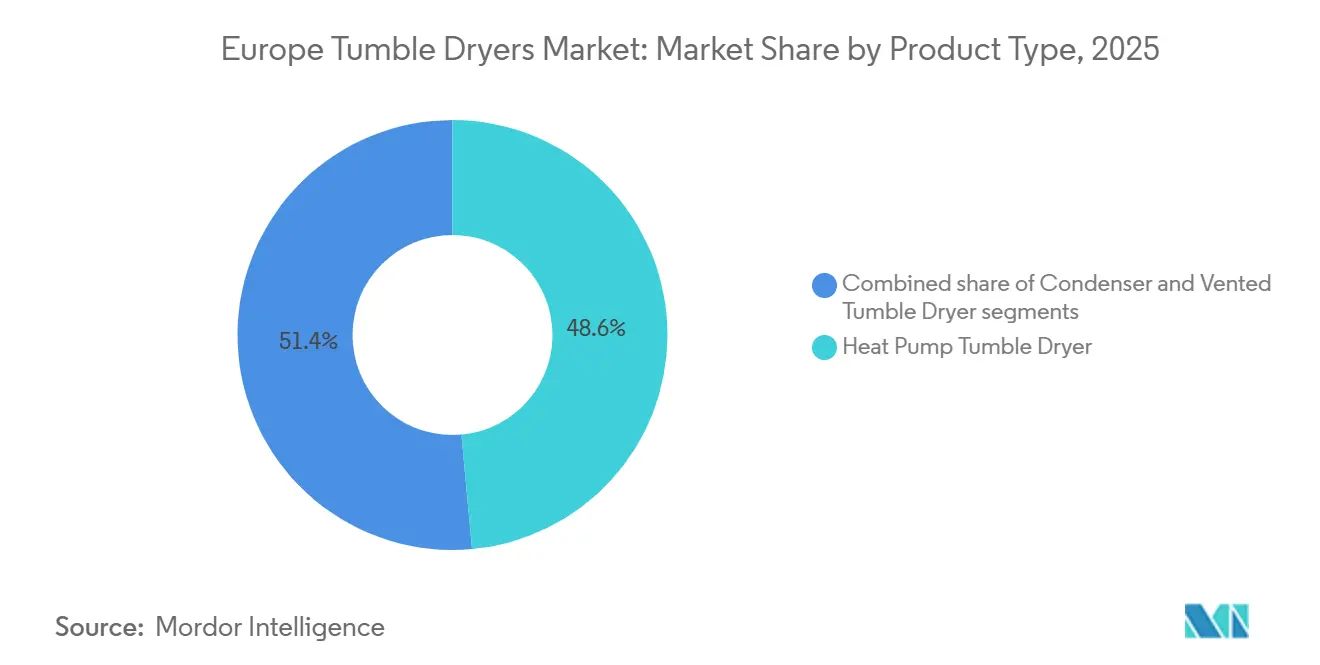

- By product type, heat-pump dryers led with 48.56% revenue share in 2025 and are projected to expand at a 4.12% CAGR through 2031, outpacing the overall category after the 2025 ecodesign enforcement.

- By end-user, residential held 77.96% value share in 2025, while commercial is forecast to record the highest growth at a 7.12% CAGR through 2031 on ESG-led fleet refreshes.

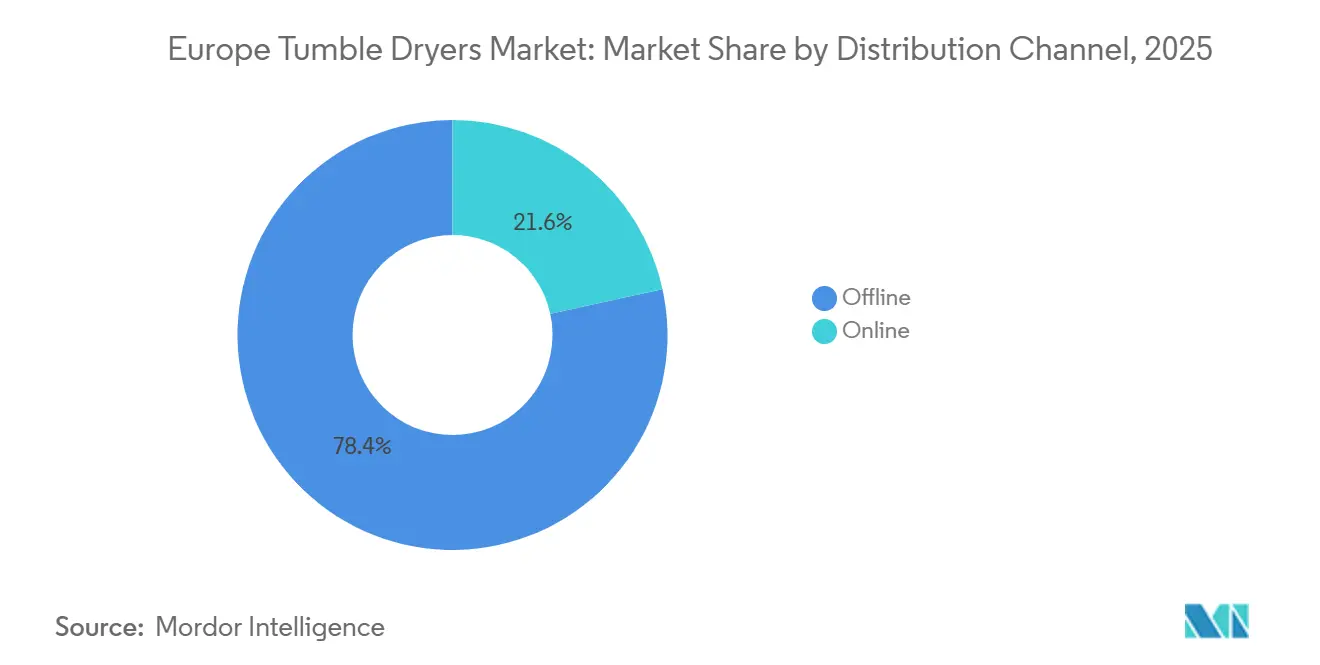

- By distribution channel, offline accounted for 78.41% share in 2025, while online is set to grow at a 4.52% CAGR to 2031 with service bundling and digital product data integration.

- By geography, Germany led with 23.22% revenue share in 2025, and Spain is projected to be the fastest-growing country with a 3.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Tumble Dryers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU 2025 ecodesign and rescaled labels | +1.8% | Germany, Netherlands, Nordics, pan‑EU | Medium term (2-4 years) |

| Energy-efficiency focus and high power costs | +1.2% | EU‑5, BENELUX | Long term (≥ 4 years) |

| Omnichannel expansion and digital discovery | +0.9% | United Kingdom, Germany, France, Southern Europe | Short term (≤ 2 years) |

| Replacement shift to premium, connected care | +0.7% | Urban EU cores, Germany, Netherlands, Nordics | Medium term (2-4 years) |

| Italy’s vouchers and Bonus Mobili | +0.4% | Italy, spillover to France, Spain | Short term (≤ 2 years) |

| Utility demand-response and smart scheduling | +0.3% | Nordics, Germany, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU 2025 Ecodesign and Rescaled Energy Labels Accelerating Heat-Pump Dryer Adoption

The July 1, 2025, enforcement of EU ecodesign rules elevated minimum energy performance and effectively removed air-vented and resistive-element condenser dryers from new market placements, making heat pump architectures the compliant path for household units above defined size thresholds. The rescaled A to G energy label and EPREL QR code transparency make A-class ratings exclusive to heat pump models and give buyers direct access to consumption, condensation efficiency, and noise metrics at the point of decision. Higher household electricity tariffs in markets such as Germany sharpen the lifetime savings case for heat pump units and compress payback horizons relative to legacy condenser products, reinforcing adoption in the Europe tumble dryers market. Spare parts and product information availability requirements, together with label transparency and repairability measures, align with circularity aims that promote better lifecycle economics and support long-term confidence in compliant models. Early pilots integrating smart home standards and demand response protocols show how connected dryers can align with time of use tariffs and utility programs, creating new value pools as grid services mature in the late decade. Component transitions to propane-based refrigerants and retooling for R290 supply add near-term friction, yet integrated manufacturers are positioned to absorb volatility and safeguard continuity across the European tumble dryers market.

Energy-Efficiency Focus Amid High Electricity Costs and Sustainability Goals

EU household electricity prices averaged EUR 28.72 (USD 33.78) per 100 kWh in H1 2025, a marginal 0.5% decline from H2 2024 yet still elevated relative to pre-2022 crisis baselines, with taxes and levies expanding from 24.7% to 27.6% of bills as government relief measures phase out[2]Eurostat, “Household Electricity Prices in 1st Half of 2025: -0.5%,” Eurostat, ec.europa.eu . The EU’s climate framework toward 2030 targets a 55% reduction in net greenhouse gas emissions, and energy efficiency is a primary lever, which positions heat pump laundry as an accessible route to reduce residential energy demand in the European tumble dryers market. Product-level energy transparency through rescaled labels and EPREL helps buyers quantify usage and align decisions with household energy budgets, which supports steady mix shift into A-class models. Industry leaders frame efficiency credentials as part of broader decarbonization efforts, a stance that increasingly influences B2B procurement in hospitality, social housing, and institutional settings. National price differentials across the EU shape payback horizons, which drive faster adoption in high tariff countries and a more gradual ramp in markets with lower electricity prices. These economics, combined with sustainability goals and regulatory certainty, continue to reinforce premium energy-efficient choices across the European tumble dryers market.

Omnichannel Expansion and Digital Discovery Elevating Category Conversion

Distribution is rebalancing as online channels grow faster than store-based formats, while offline remains dominant for high involvement purchases that require installation and hands-on evaluation. Online channels captured 27% of Major Domestic Appliance sales in H1 2025 as retailers standardize delivery, removal, and warranty bundles that reduce risk and improve convenience for buyers in the Europe tumble dryers market[3]NIQ, “Home Appliances Outlook 2026: Western Europe - NIQ,” NIQ, nielseniq.com. Connectivity and digital product data embedded via QR code links to EPREL and device apps help customers compare lifetime energy use and noise characteristics, which, in turn, shortens decision cycles. Digital Product Passports planned under EU initiatives will further surface repairability and parts availability, raising the profile of compliant, connected models in public and private procurement. Store networks continue to act as advisory hubs for premium tiers, while omnichannel checkout flows that combine online discovery with in-home services build confidence for four-figure outlays in the European tumble dryers market. As retailers deepen service integration and after-sales support, attach rates for installation and maintenance are rising, which adds recurring value to the category’s digital shift.

Replacement-Driven Base Shifting to Premium, Connected Fabric-Care Propositions

Aging installed bases and replacement windows post 2025 favor premium energy efficient upgrades, especially as households prioritize lifetime cost savings and reliable performance in the Europe tumble dryers market. Premium brands are using service guarantees to differentiate, such as Miele’s extended motor warranty for laundry machines in Germany, which signals lifecycle confidence and helps justify higher price points[4]Miele Press Office, “Miele Presents at the Altenpflege Trade Fair 2026,” Miele, miele.de . Interoperability with smart home ecosystems is advancing as vendors adopt standards that simplify setup and allow remote diagnostics, energy dashboards, and predictive maintenance within a uniform app experience. Product launches that apply AI to optimize drying and fabric protection are reinforcing premium value as users see tangible energy and time benefits surfaced in easy-to-read dashboards in the European tumble dryers market. Public procurement and professional buyers are prioritizing durable, connected platforms that streamline service across large fleets, which strengthens the case for dual consumer professional product architectures among leading OEMs. As affordability remains a constraint in some regions, brands are also testing lower-priced heat pump configurations that retain core efficiency features while moderating aesthetic customization to compress costs, a move that broadens reach across the European tumble dryers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront prices vs condenser/vented | -1.4% | Eastern and Southern Europe | Short term (≤ 2 years) |

| Longer cycle times of heat‑pump models | -0.8% | Pan‑EU, stronger in dense urban markets | Medium term (2-4 years) |

| Elongated replacement cycles | -0.6% | EU‑5 saturated markets | Long term (≥ 4 years) |

| Right‑to‑repair and refurbished channels | -0.4% | France, Belgium, Germany, EU-wide rollout | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Prices of Heat Pump Dryers Versus Condenser/Vented

Heat pump dryers typically carry a three-digit to four-digit euro price premium over condenser and vented units, which compresses adoption in price-sensitive markets and raises the need for financing or incentives in the European tumble dryers market. The effective payback period varies by electricity price, and lower tariff countries see slower upgrades because lifetime savings accrue more gradually relative to the upfront premium. Retailers’ clearance of non-compliant inventory post July 2025 created temporary arbitrage opportunities between discounted condenser units and new heat pump SKUs, which deferred some upgrades until closeouts ended. Municipal cash back schemes and national tax deductions help narrow the premium in select locations, though coverage remains uneven across the EU. As vendors scale R290 compressor supply and streamline designs, entry variants are expected to moderate price gaps over time in the European tumble dryers market.

Longer Cycle Times for Heat Pump Models Affecting User Acceptance

Heat pump dryers run at lower operating temperatures to protect fabrics, which increases average cycle time versus vented designs and challenges evening throughput in busy urban households. Moisture sensing and drum innovations are shortening cycles relative to first-generation heat pump units, but still lag the fastest vented baselines that some users are accustomed to. Perceived “damp feel” upon cycle end can occur due to lower exit temperatures, which sometimes requires consumer education so that fabric care benefits are understood as intentional rather than as incomplete drying. Cross-appliance synchronization features now help pre-optimize dryer settings based on washing machine data to compress the total laundry workflow window in the European tumble dryers market. These improvements ease acceptance, yet throughput sensitivity will remain a consideration for dual-income households and small apartments where laundry timing is tight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Heat-Pump Dominance Accelerates Under Regulatory Mandate

Heat pump units held 48.56% of the 2025 value and are projected to grow at a 4.12% CAGR through 2031, a trajectory supported by the July 2025 ecodesign enforcement and reinforced by rescaled labels that reserve A class ratings for heat pump systems in the European tumble dryers market. Condenser models, which held the balance of sales in 2025, are expected to phase down as post-enforcement inventory clears and as buyers favor the long-run savings of heat pump efficiency in the European tumble dryers industry. Leading brands have positioned new heat pump portfolios at multiple price points and with connectivity and self-cleaning features that reduce manual maintenance, a combination that supports a premium mix and attachment of service plans. Flagship lines now demonstrate top-tier energy classes with annual consumption levels far below older condenser baselines, which strengthens the product narrative around efficiency and fabric care.

As interoperability standards expand across home ecosystems, connected heat pump dryers are aligning with smart home platforms and utility programs that increase the perceived value beyond energy savings alone in the European tumble dryers market. Refrigerant transitions, retooling, and supplier ramp-ups introduce short-term constraints, yet integrated manufacturers are offsetting volatility through scale and multi-plant capacity in Europe. Premium lines from incumbents emphasize silent operation, drum engineering for delicate care, and app-based scheduling, which anchor higher average selling prices while expanding use cases in apartments and dense urban settings. These design and compliance vectors combine to concentrate product type growth within the heat pump segment as the Europe tumble dryers market moves further from legacy vented and condenser technologies.

By End-User: Residential Dominance Sustained, Commercial Momentum Builds on ESG Criteria

Residential users represented 77.96% of the 2025 value and are set to grow at a 2.98% CAGR through 2031 as households replace aging stock with A-class heat pump models and respond to label transparency and lifetime cost savings in the European tumble dryers market. Commercial buyers, including hospitality and social housing operators, are expected to expand faster at a 7.12% CAGR, driven by operating expense reduction goals and ESG-linked procurement that favors connected, durable platforms. Across both segments, the shift to heat pump systems benefits from EPREL label clarity, which helps procurement teams validate claims and compare products against consistent metrics. Budget and energy price dynamics pace residential replacement decisions, while professional buyers often prioritize total cost of ownership, cycle throughput, and remote diagnostics.

Commercial fleets increasingly specify propane-based refrigerant compressors and high-duty cycles that deliver strong energy savings, and these configurations spread into institutional laundry rooms as well as premium multi-family residences in the European tumble dryers market. Residential demand shows greater sensitivity to installation services and after-sales support, pushing retailers to increase attach rates for delivery, removal, and warranty plans that simplify ownership. Connectivity, predictive maintenance, and user-friendly dashboards shorten onboarding time and make it easier for families to optimize energy use, which broadens perceived value beyond the purely functional aspects of drying. These behavioral and procurement trends support a sustained residential majority while enabling faster relative growth in commercial settings that anchor the high efficiency transition in the European tumble dryers market.

By Distribution Channel: Online Share Climbs as Services and Data Reduce Friction

Offline channels held 78.41% of value in 2025 and remain central to premium transactions that require installation, product demonstrations, and immediate service coordination in the European tumble dryers market. Online channels are projected to grow at a 4.52% CAGR through 2031 and are on track to surpass 40% penetration before the decade ends as platforms standardize delivery, removal, and multi-year warranty bundles. Retailers and brands leverage EPREL data and QR code labels to surface energy and noise information that helps shoppers compare SKUs quickly and creates a seamless path from research to purchase. The European tumble dryers market size for online channels is set to benefit from attach rates on services that de-risk delivery and setup, which are now embedded in checkout flows across major retailers.

As consumer comfort with large ticket online orders increases, more shoppers use hybrid journeys that begin with digital discovery and finish with in-home services, which raises conversion and average order values in the European tumble dryers market. Connectivity and app support carry through post-purchase and make visible the energy savings that motivated the initial selection, which reduces regret and strengthens brand advocacy in both offline and online channels. Over time, the offline online balance will tilt further toward digital as service logistics and reverse logistics become more predictable and as EU product information policies normalize expectations for data transparency across the Europe tumble dryers market. This progression favors omnichannel leaders that can match installation quality with digital convenience while sustaining high service standards at scale.

Geography Analysis

Germany led with 23.22% of the 2025 value and is projected to maintain leadership as high electricity prices and premium brand loyalty support a steady shift to connected heat pump models in the European tumble dryers market. Smart meter infrastructure and emerging dynamic tariffs increase the relevance of smart scheduling features and support the economics of A-class dryer adoption in German households. Product portfolios from local champions emphasize energy class A performance, silent operation, and low maintenance, which fits the preferences of a mature installed base that weighs lifetime value over initial price in the Europe tumble dryers market. These conditions are likely to keep Germany at the center of connected, ecodesign-aligned product launches and pilot programs tied to evolving grid services.

France and the United Kingdom follow as large contributors, each with distinct policy and consumer behavior signals that influence replacement timing and product selection in the Europe tumble dryers market. France’s durability and repairability emphasis sits alongside label transparency, which encourages buyers to balance reliability, energy, and price during upgrades. In the United Kingdom, social housing and retrofit programs intersect with product standards policy to prioritize higher efficiency appliances in public tenders, which provides a steady B2B baseline for compliant heat pump fleets. Across both markets, connectivity and service assurances reduce friction for premium choices and support gradual mix shifts to A-class models in the European tumble dryers market.

Spain is the fastest-growing major geography at a projected 3.41% CAGR to 2031, as late adoption of heat pump dryers combines with rising incomes and expanding new home installations, while Italy’s policy support through Bonus Mobili accelerates renovation-linked upgrades in the European tumble dryers market. BENELUX and the Nordics reinforce the case for connected appliances with smart meter reach and tariff models that reward off-peak scheduling, which bolsters the economics of smart dryers. Eastern European markets see a more gradual shift as affordability and lower power prices lengthen payback timelines, yet digital discovery and service bundling will help close gaps as entry-level heat pump offers expand in the European tumble dryers market. Over the forecast, regional variations in energy prices, policy incentives, and home renovation activity will continue to shape adoption arcs across the continent.

Competitive Landscape

The European tumble dryers market is led by major manufacturers such as BSH Hausgeräte, Beko Europe, Electrolux AB, Haier Europe, and Miele, which together account for a significant share of the market, although their combined share remains below 50%. BSH’s 2025 IFA portfolio for Bosch and Siemens emphasized energy class A performance, self-cleaning condensers, fabric‑care options for delicates, and expanded Home Connect capabilities that reinforce premium value. Miele’s professional and consumer showcases highlight propane-based refrigerant use, compact high-performance stacks, and time-saving cycles, which extend advantages into institutional settings while promoting durable, service-friendly designs in the European tumble dryers market.

Electrolux leans on Scandinavian design and professional‑laundry depth, positioning heat‑pump platforms that meet high-duty-cycle requirements and reduce operating expense for hospitality and care facilities. Connectivity, energy dashboards, and predictive maintenance features are becoming standard among premium lines, with interoperability moves, such as early Matter rollouts in adjacent appliance categories, signaling a clear direction for laundry platforms in the European tumble dryers market. Integrated brands with vertically aligned manufacturing and supplier relationships are better positioned to manage refrigerant transitions and scale production efficiently under post-2025 regulatory realities.

Category leaders are also activating circular economy models to support right-to-repair policies and to serve budget-sensitive segments with certified refurbished units, which sustain brand presence and reduce environmental footprints in the European tumble dryers market. Public tenders and social‑housing initiatives increase the importance of serviceability scores, spare‑parts logistics, and data transparency, which reward vendors that design for ease of repair and long lifecycles. As utility-aligned features gain relevance, brands that make demand‑response capabilities native and easy to use will hold an advantage in B2B competitions and connected‑home ecosystems across the European tumble dryers market.

Europe Tumble Dryers Industry Leaders

BSH Hausgeräte GmbH (Bosch, Siemens)

Miele & Cie. KG

Electrolux AB

Beko Europe B.V.

Haier Europe

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Beko won four iF DESIGN AWARDS 2026, including recognition for its Intelligent Guidance (UX) feature within the HomeWhiz app, which provides instant, intuitive assistance for appliance support covering washing machines, dishwashers, refrigerators, and dryers, offering notifications, step-by-step guidance, proactive care recommendations, and one-click access to maintenance products. This system aims to simplify maintenance and help appliances maintain performance throughout their lifespan.

- February 2026: Miele showcased five laundry innovations at the Altenpflege trade fair 2026 (April 21–23, Essen, Germany), including a new dryer stack composed of two 'Little Giants' series heat pump dryers, offering compact, high-performance drying with energy consumption about 50% lower than vented dryers and using environmentally friendly propane as refrigerant. The stack can handle two 8 kg loads in 77 minutes for professional laundry applications.

- January 2026: Samsung Electronics Europe and Instacart unveiled AI Vision-enabled refrigerators supporting in-app grocery ordering in France, Germany, and the United Kingdom, while Samsung Germany expanded its Certified Re-Newed program for smartphones to France and the United Kingdom, signaling strategic moves toward connected appliances and circular-economy business models. These initiatives reflect broader trends in smart home integration and sustainability.

- November 2025: The European Commission introduced a repairability scale (rated A to E) for household tumble dryers to be displayed on new energy labels starting July 1, 2025, with mandatory inclusion for all household tumble dryers placed on the market from January 1, 2027. This initiative addresses declining product lifespans (from 14 to 12 years) and aims to reduce energy consumption and waste by promoting easier-to-repair products.

Europe Tumble Dryers Market Report Scope

A tumble dryer is an appliance that dries clothes by putting them in hot air. The appliance ensures that clothes get dried almost instantly and saves electricity and cost for the user over time with its efficiency features. The product is made available in different capacities, with automatic and semi-automatic products being offered by the manufacturers.

The Europe tumble dryers market is segmented by product type, end-user, distribution channel, and geography. By product type, the market is sub-segmented into heat pump tumble dryer, condenser tumble dryer, and vented tumble dryer. By end-user, the market is sub-segmented into residential and commercial. By distribution channel, the market is sub-segmented into offline and online. By geography, the market is sub-segmented into Germany, France, the United Kingdom, Italy, Spain, BENELUX, NORDICS, and the Rest of Europe. The report offers market size and forecasts for the Europe tumble dryers market in value (USD Billion) for all the above segments.

| Heat Pump Tumble Dryer |

| Condenser Tumble Dryer |

| Vented Tumble Dryer |

| Residential |

| Commercial |

| Offline |

| Online |

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| BENELUX |

| NORDICS |

| Rest of Europe |

| By Product Type | Heat Pump Tumble Dryer |

| Condenser Tumble Dryer | |

| Vented Tumble Dryer | |

| By End-User | Residential |

| Commercial | |

| By Distribution Channel | Offline |

| Online | |

| By Country | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| BENELUX | |

| NORDICS | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size and growth outlook for the Europe tumble dryers market?

The Europe tumble dryers market size is projected to be USD 2.85 billion in 2025, USD 2.96 billion in 2026, and reach USD 3.39 billion by 2031, growing at a CAGR of 2.75% from 2026 to 2031.

Which product type is leading and which is growing the fastest?

Heat‑pump dryers lead with 48.56% share in 2025 and are the fastest‑growing segment at a 4.12% CAGR through 2031 due to the EU’s 2025 ecodesign enforcement.

How are distribution channels evolving across the region?

Offline retains a 78.41% share for complex, premium purchases, while online is set to surpass 40% penetration before 2031 on a 4.52% CAGR supported by bundled delivery, removal, and warranty services.

Which country leads and which is the fastest growing?

Germany leads with 23.22% of the 2025 value, while Spain is forecast to grow the fastest at a 3.41% CAGR over 2026 to 2031.

What policy changes most affect new product sales?

The EU’s July 1, 2025, ecodesign and rescaled energy labels steer new placements to heat‑pump technology and elevate A-class transparency through EPREL QR codes on the label.

What features are differentiating premium models today?

Energy class A performance, lower noise, self-cleaning condensers, interoperable connectivity, and app-based scheduling are leading differentiators among premium heat‑pump dryers.

Page last updated on: