Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

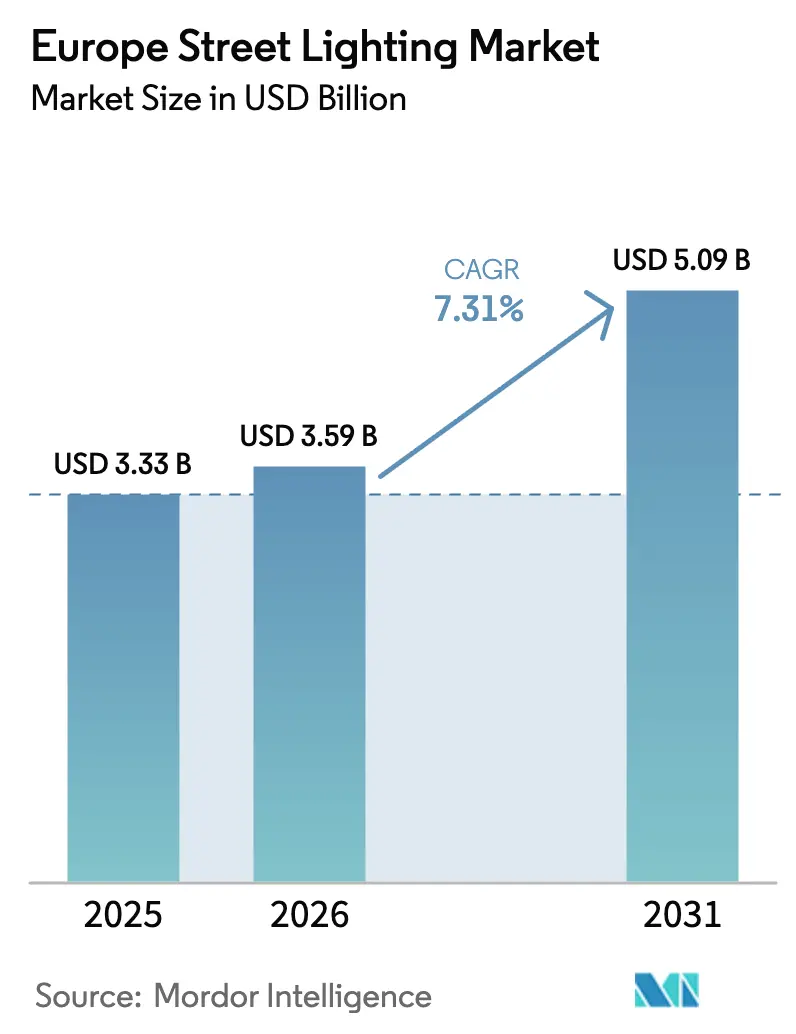

| Base Year Market Size (2025) | USD 3.33 Billion |

| Market Size (2026) | USD 3.59 Billion |

| Market Size (2031) | USD 5.09 Billion |

| Growth Rate (2026 - 2031) | 7.31% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Street Lighting Market Analysis by Mordor Intelligence

The Europe street lighting market size is projected to be USD 3.33 billion in 2025, USD 3.59 billion in 2026 and reach USD 5.09 billion by 2031, growing at a CAGR of 7.23% from 2026 to 2031. Energy-efficiency mandates, the 2024 fluorescent-lamp ban and a widening secondary-replacement wave for first-generation LEDs are accelerating tenders across the region. Municipalities are shifting focus from simple lamp swaps to networked platforms that support adaptive dimming, traffic analytics and pole-mounted 5G small cells, thereby turning lighting assets into multi-service gateways. Hardware continues to dominate spending, yet the fastest growth is migrating to software and services as cities favor subscription models that bundle cybersecurity and analytics. Competitive intensity remains elevated as incumbent luminaire makers, connectivity specialists and telecom vendors converge on the same procurement cycles, while smaller towns struggle with up-front capital outlays despite expanded European Investment Bank technical assistance.

Key Report Takeaways

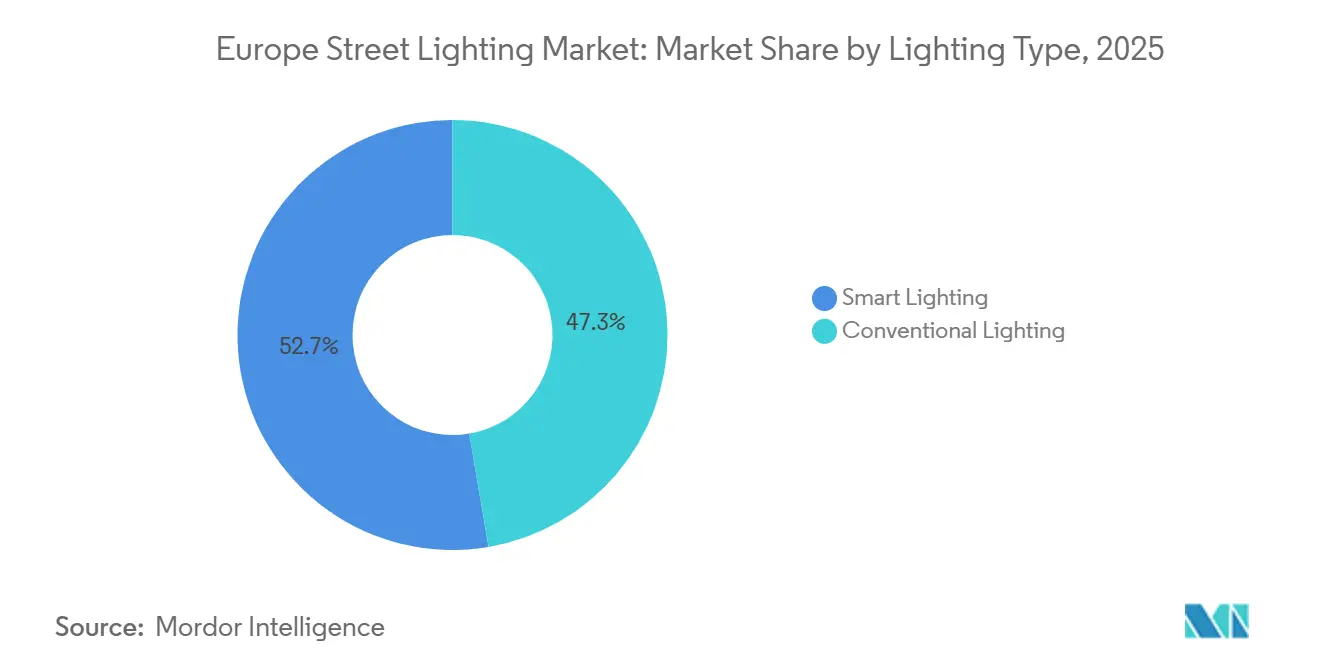

- By lighting type, smart lighting held 52.67% of the Europe street lighting market share in 2025 and is advancing at an 8.12% CAGR through 2031.

- By light source, LEDs accounted for 86.58% of the Europe street lighting market size in 2025 and are expanding at an 8.33% CAGR to 2031.

- By offering, hardware commanded 67.12% of 2025 revenue, while software and services record the highest projected CAGR at 9.04% over 2026-2031.

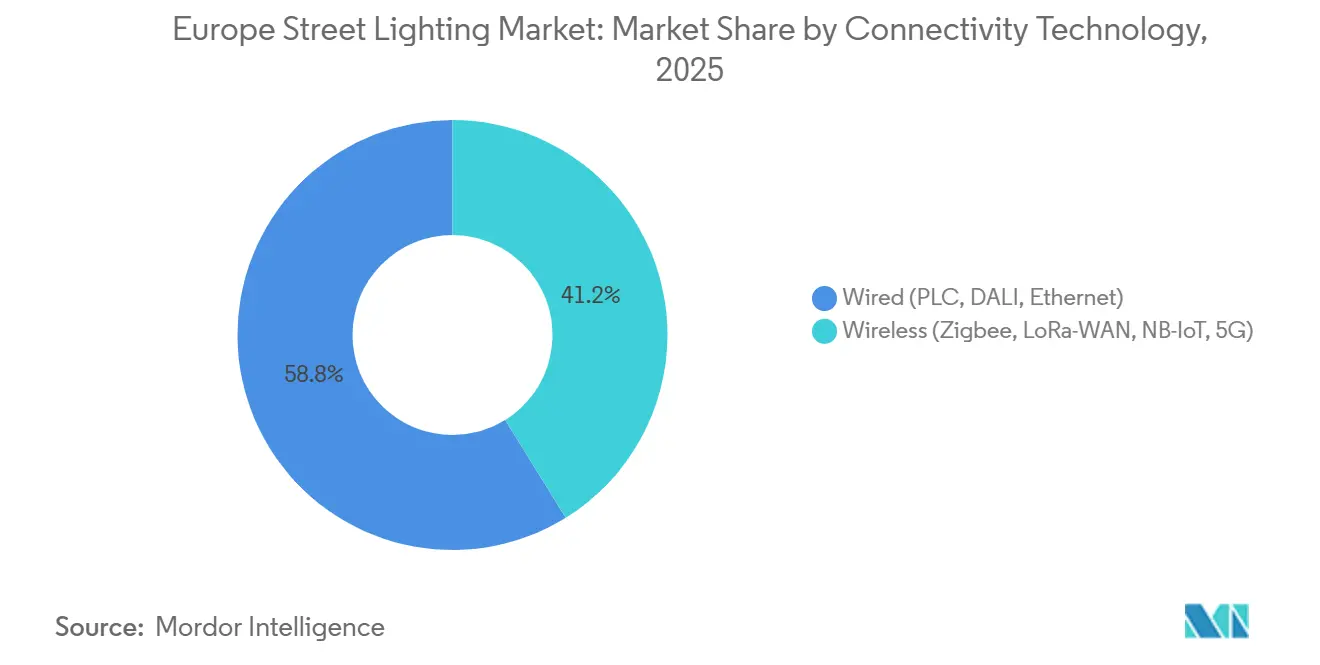

- By connectivity, wired solutions led with 58.83% share in 2025, yet wireless protocols are on track for an 8.93% CAGR through 2031.

- By installation type, retrofit and secondary replacement represented 71.73% of 2025 projects and are forecast to grow at 8.36% to 2031.

- By country, Germany captured 28.73% share in 2025; Italy is forecast to register the fastest national CAGR at 7.97% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Street Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Ban on Fluorescent Lamps and Stricter Ecodesign Targets | +1.8% | EU-wide, with accelerated adoption in Germany, France, Netherlands | Short term (≤ 2 years) |

| Smart-City Stimulus and Pilot Replication Momentum | +1.5% | Germany, France, Italy, Spain, Nordic countries | Medium term (2-4 years) |

| Declining Total Cost of Ownership for LED and Connectivity | +1.4% | EU-wide, with early gains in municipalities >50,000 population | Medium term (2-4 years) |

| EU Recovery and Resilience Facility E-Mobility Corridors | +1.2% | Trans-European Transport Network corridors, priority in Italy, Spain, Eastern Europe | Long term (≥ 4 years) |

| Secondary-Replacement Wave for First-Gen LEDs (2024-2030) | +1.0% | Germany, UK, France, Benelux (early LED adopters 2012-2018) | Medium term (2-4 years) |

| Street-Light Poles Monetised as Edge-IoT Real-Estate | +0.8% | Urban centers in Germany, France, UK, Nordic capitals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Ban on Fluorescent Lamps and Stricter Ecodesign Targets

The European Commission’s Mercury Regulation 2024/1849 mandates a complete phase-out of compact fluorescent lamps by December 2025 and linear fluorescent lamps by December 2026, closing the final loophole for mercury-containing sources. Compliance deadlines have triggered a surge in tender releases as municipalities rush to replace obsolete inventories and retrain crews on LED diagnostics. France has tied EUR 1.5 billion (USD 1.61 billion) of municipal grants to adherence, accelerating take-up in smaller towns. Obsolete ballast write-offs and mandatory recycling add near-term budget pressure, yet they open multiyear demand for connected LED systems that meet updated Ecodesign efficacy thresholds.

Smart-City Stimulus and Pilot Replication Momentum

Horizon Europe labeled 103 cities as climate-neutral demonstrators in 2024 and allocated EUR 41 million (USD 43.9 million) for integrated pilots where lighting forms the digital backbone.[1]European Commission, “EU Recovery and Resilience Facility,” ec.europa.eu Germany’s EUR 10 billion (USD 10.7 billion) climate fund reimburses up to 50% of retrofit costs when projects embed traffic sensing and air-quality nodes, spurring replication in mid-sized municipalities. The RESONANCE project is scaling LoRaWAN-based architectures proven to cut energy use 35% and truck-rolls 42% in Iceland. Funding consistency and published best-practice playbooks continue to shrink decision cycles, propelling the Europe street lighting market toward platform models.

Declining Total Cost of Ownership for LED and Connectivity

Between 2020 and 2024, average LED luminaire prices dropped 20% and narrowband-IoT modules fell below EUR 10 per node, making smart capability almost cost-neutral. A Smart Cities Marketplace audit shows that replacing a 100 W high-pressure sodium lamp with a 40 W LED saves 26,280 kWh over its life, paying back within 3.2 years at prevailing tariffs. Predictive diagnostics cut maintenance labor 30-40%, further widening the lifecycle gap. Italy’s EUR 2.2 billion (USD 2.35 billion) PNRR funding enables bundling with EV chargers, diluting per-pole capital outlays.

EU Recovery and Resilience Facility E-Mobility Corridors

The Recovery and Resilience Facility earmarks street-light upgrades along TEN-T corridors to support fast EV charging, awarding Bulgaria EUR 76 million (USD 81.3 million) in 2024. The United Kingdom’s GBP 1.1 billion (USD 1.39 billion) LEVI fund applies identical photometric standards to on-street chargers. Corridor projects demand higher lumen packages, adaptive dimming and ruggedized enclosures, channeling premium demand toward suppliers with highway-grade portfolios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front CAPEX for Smart Retrofits in Small Municipalities | -1.2% | Southern Europe, Eastern Europe, rural municipalities <10,000 population | Short term (≤ 2 years) |

| LED Driver Reliability and Thermal Ageing Failures | -0.9% | EU-wide, particularly in high-ambient-temperature zones (Southern Europe) | Medium term (2-4 years) |

| Cyber-Security and GDPR Compliance Burden | -0.7% | Germany, France, Nordic countries with stringent data-protection enforcement | Medium term (2-4 years) |

| Semiconductor-Component Supply Volatility | -0.6% | EU-wide, with acute impact on custom-control systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Up-Front CAPEX for Smart Retrofits in Small Municipalities

A networked LED unit costs EUR 300-500 versus EUR 150 for a non-connected replacement, a hurdle for towns with annual budgets under EUR 5 million (USD 5.93 million).[2]European Investment Bank, “ELENA Program,” eib.org While the ELENA facility has mobilized EUR 1.1 billion (USD 1.31 billion) for technical assistance since 2009, coverage remains uneven in Southern and Eastern Europe. France’s France 2030 plan bundles lighting with broader infrastructure upgrades, effectively sidelining stand-alone bids from cash-strapped communes. Cyclic grant windows further delay adoption, constraining early volume in the Europe street lighting market.

LED Driver Reliability and Thermal Ageing Failures

Field data show 15-20% failure rates in first-generation LED drivers after eight years, far earlier than the promised 15-year life, with Mediterranean pavement temperatures pushing junctions beyond 70 °C. Premature outages erode lifecycle savings and fuel skepticism during second-wave procurements. Research now recommends silicon-carbide devices and liquid-cooled heat sinks, but municipalities remain wary, slowing conversion in Spain, Italy and Greece.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Lighting Type: Smart Platforms Capture Majority Share

Smart platforms accounted for 52.67% of 2025 revenue, demonstrating that the Europe street lighting market is steadily migrating from commodity lamp replacement to network intelligence. Remote diagnostics and adaptive dimming lower lifecycle costs, while pole-mounted radios support add-on services such as traffic analytics and environmental monitoring. Municipal bundling with 5G small cells opens incremental lease income, reinforcing platform economics. Conventional lighting retains relevance in rural zones where debt capacity is limited, yet declining component prices and widening grant access are set to narrow its addressable pocket by 2030.

Continued stimulus from Horizon Europe and evidence from pilots such as LORIOT’s 6,000-node Iceland deployment have validated energy and maintenance savings, shortening payback periods below four years. As cities publish open-data dashboards powered by lighting networks, civic appetite for sensor integration is rising, anchoring future procurement specifications firmly in favor of smart infrastructure.

By Light Source: LEDs Dominate with Accelerating Growth

LEDs commanded an 86.58% share in 2025 and are advancing at an 8.33% CAGR to 2031 as the Europe street lighting market size shifts wholesale toward solid-state sources. Mercury Regulation 2024/1849 makes the purchase of fluorescent lamps illegal after 2026, while high-pressure sodium remains in slow retirement due to poor dimming compatibility. Secondary replacement of early LED vintages further lifts unit volumes without adding new poles.

Advances in chip-scale packaging and silicon-carbide drivers are extending usable life under high-ambient conditions, directly addressing the primary restraint of thermal driver failures. As ballast inventories and technician skill sets for legacy lamps vanish, post-2026 tenders are expected to specify LED-only solutions, cementing the technology’s near-total dominance.

By Offering: Software and Services Expand Fastest

Hardware maintained a 67.12% share in 2025 because every retrofit begins with a luminaire and controller. Even so, software and services are on track for a 9.04% CAGR as municipalities shift toward lighting-as-a-service, rolling cybersecurity updates and data analytics subscriptions. The EU Cyber Resilience Act obliges ongoing patch support, catalyzing multi-year platform contracts and stable recurring revenue streams.

Signify’s Interact and Telensa’s PLANet platforms illustrate the pivot, offering APIs for traffic flow or air-quality modules that can be turned on without swapping the fixture. Hardware margins compress as Asian vendors commoditize LED engines, further motivating incumbents to upsell analytics and value-added services.

By Connectivity Technology: Wireless Protocols Gain Ground

Power-line communication and DALI-over-mains kept wired systems at a 58.83% share in 2025, but cellular narrowband-IoT, LoRaWAN and early 5G are accelerating at an 8.93% CAGR as the Europe street lighting market embraces radio links to avoid conduit digs. Wireless units are particularly appealing in historical city centers where trenching is prohibited or in sprawling suburbs where pole spacing exceeds 50 m.

EN 303 645 V3.1.3 from ETSI created a clear security baseline, reducing risk-perception barriers. Early concerns about latency and interference are subsiding as pilot data confirm stable performance and over-the-air firmware updates. Wired systems remain favored for highway corridors requiring deterministic latency and for municipalities with existing broadband-over-power infrastructure, yet wireless momentum is unmistakable.

By Installation Type: Retrofit Dominates Amid Secondary-Replacement Wave

Retrofits represented 71.73% of 2025 activity, underscoring the vast aging installed base and the onset of second-cycle replacements for first-generation LEDs. Mandatory fluorescent phase-out dates and EU financing windows converge to keep retrofit volumes high through 2031. New installations are confined to highway expansions and greenfield developments concentrated in Eastern Europe, resulting in lower share despite solid CAGR.

Complexity in retrofit projects drives demand for modular fixtures with tool-free driver swap capability, trimming truck time and extending asset value. The learning curve from first-wave LED rollouts informs tighter procurement specifications on thermal management, cybersecurity and open APIs.

Geography Analysis

Germany led with 28.73% of 2025 revenue, anchored by USD 10.7 billion in federal climate and transformation funds and mature energy-performance contracting know-how. Early LED adopters now face wide-scale driver failures, spurring secondary replacements that almost always include smart controls and sensor docks. The United Kingdom and France follow, each leveraging national EV-charging funds and renewable microgrid incentives that mandate compliant lighting upgrades.[3]Gouvernement Français, "France 2030 Investment Plan," gouvernement.fr

Italy is projected as the fastest climber at a 7.97% CAGR to 2031, propelled by USD 2.35 billion in PNRR urban mobility allocations. Historically low LED penetration leaves ample room for catch-up, and bundled e-mobility corridor projects along the Autostrada network are accelerating award volume. Spain, Portugal and Greece confront harsher thermal stress and tighter municipal budgets, tilting demand toward cost-optimized LED replacements unless multilateral funding is secured.

Nordic countries exhibit the highest per-capita spend on smart lighting due to steep electricity tariffs and progressive climate goals, reinforcing premium demand for advanced analytics. Eastern European member states benefit from Recovery and Resilience Facility corridors, yet smaller municipalities still depend heavily on ELENA technical assistance to navigate complex procurement formats and performance contracts.

Competitive Landscape

The Europe street lighting market is moderately concentrated around global incumbents such as Signify, Zumtobel Group and Schréder that combine broad luminaire portfolios with vertically integrated optics, drivers and control stacks. Signify leverages its Interact platform and BrightSites pole-monetization model to sell outcome-based contracts, while Zumtobel emphasizes architectural optics for heritage districts and Schréder targets ruggedized highway fixtures.

Controls specialists including Telensa, Itron and Cisco Systems decouple software intelligence from luminaire hardware, allowing municipalities to upgrade algorithms without ripping out fixtures. Systems integrators and energy-service companies bundle lighting with broadband, charging or surveillance networks, transferring capital risk through performance-based agreements and placing further pressure on traditional product margins.

White-space opportunities are most evident in the secondary-replacement cycle and in edge-IoT monetization. ETSI’s EN 303 645 and the EU Cyber Resilience Act give an advantage to vendors able to resource multi-year patch management, penalizing low-cost entrants that cannot sustain compliance. Thermal-management startups offering liquid-cooled heat sinks or silicon-carbide driver modules address the reliability restraint, while LoRaWAN network operators secure contracts by shouldering connectivity deployment.

Europe Street Lighting Industry Leaders

-

Signify N.V.

-

Zumtobel Group AG

-

Schréder SA

-

Eaton Corporation plc

-

OSRAM GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Signify announced a multiyear framework agreement with the City of Milan to retrofit 150,000 luminaires on an energy-performance contract that guarantees 60% energy savings and includes BrightSites small-cell readiness.

- May 2025: O2 Telefónica began nationwide 5G streetlight expansion across Germany’s 25 largest cities, marrying LED luminaires with small-cell antennas to enhance network coverage.

- April 2025: Cornerstone and Signify agreed to deploy UK-wide multi-operator wireless networks through existing street-lighting systems.

- January 2025: Signify announced CEO Eric Rondolat will step down after 13 years amid revenue pressures despite 90% LED sales.

Europe Street Lighting Market Report Scope

Street lighting is an essential infrastructural lighting form. Without proper outdoor lights, traveling at night becomes a significant challenge. Street lighting can promote security in urban areas and improve safety for drivers, riders, and pedestrians.

The Europe Street Lighting Market Report is Segmented by Lighting Type (Conventional Lighting, Smart Lighting), Light Source (LEDs, Fluorescent Lamps, HID Lamps), Offering (Hardware (Lights and Bulbs, Luminaires, Control Systems), Software and Services), Connectivity Technology (Wired (PLC, DALI, Ethernet), Wireless (Zigbee, LoRa-WAN, NB-IoT, 5G)), Installation Type (New Installation, Retrofit and Secondary Replacement), and Geography (Germany, United Kingdom, France, Italy, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Lighting Type

| Conventional Lighting |

| Smart Lighting |

By Light Source

| LEDs |

| Fluorescent Lamps |

| HID Lamps |

By Offering

| Hardware | Lights and Bulbs |

| Luminaires | |

| Control Systems | |

| Software and Services |

By Connectivity Technology

| Wired (PLC, DALI, Ethernet) |

| Wireless (Zigbee, LoRa-WAN, NB-IoT, 5G) |

By Installation Type

| New Installation |

| Retrofit, Secondary Replacement |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Rest of Europe |

| By Lighting Type | Conventional Lighting | |

| Smart Lighting | ||

| By Light Source | LEDs | |

| Fluorescent Lamps | ||

| HID Lamps | ||

| By Offering | Hardware | Lights and Bulbs |

| Luminaires | ||

| Control Systems | ||

| Software and Services | ||

| By Connectivity Technology | Wired (PLC, DALI, Ethernet) | |

| Wireless (Zigbee, LoRa-WAN, NB-IoT, 5G) | ||

| By Installation Type | New Installation | |

| Retrofit, Secondary Replacement | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe street lighting market today?

The sector generated USD 3.59 billion in 2026 and is projected to reach USD 5.09 billion by 2031.

What CAGR is forecast for European street lighting through 2031?

The market is expected to grow at a healthy 7.23% compound annual rate over 2026-2031.

Which segment is expanding fastest?

Software and services are projected to rise at 9.04% CAGR as cities adopt lighting-as-a-service models.

Why are smart platforms gaining share?

Falling connectivity costs, EU funding for smart-city pilots and new revenue from pole-mounted 5G small cells are driving adoption.

Which country will post the quickest growth?

Italy leads with a forecast 7.97% CAGR thanks to sizable PNRR mobility allocations and low prior LED penetration.

What is the main risk for municipalities deploying LEDs?

Premature driver failures under high heat conditions can raise lifecycle costs unless robust thermal management is specified.

Page last updated on: