Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

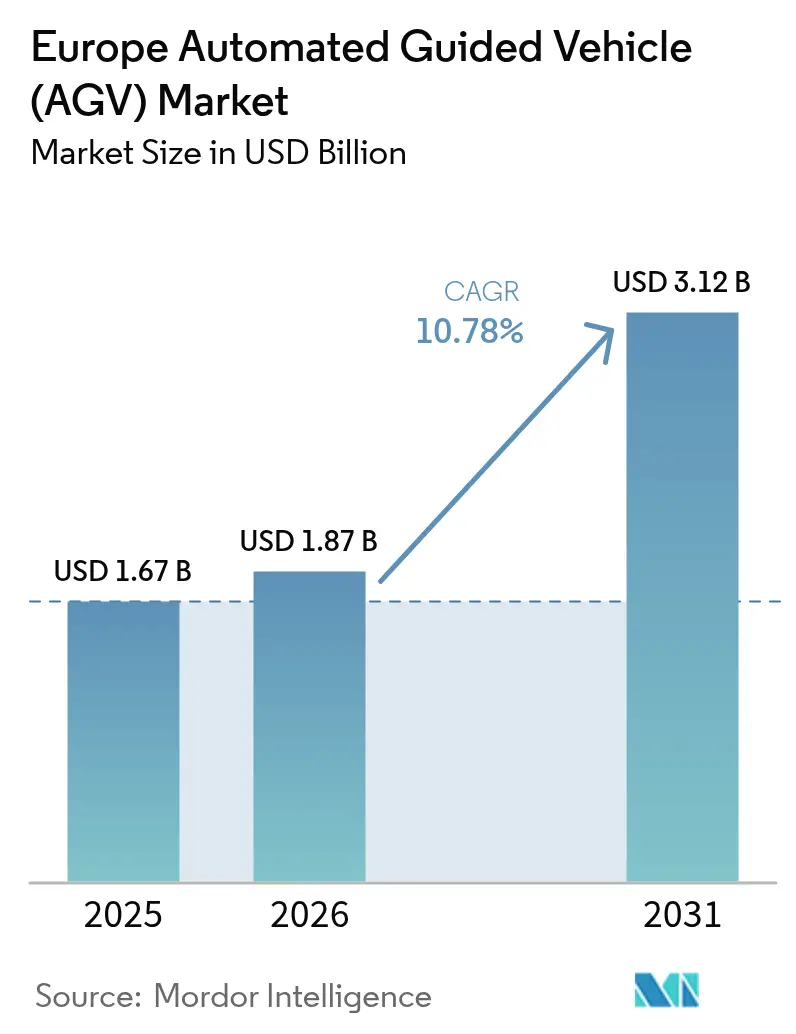

| Base Year Market Size (2025) | USD 1.67 Billion |

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 3.12 Billion |

| Growth Rate (2026 - 2031) | 10.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automated Guided Vehicle (AGV) Market Analysis by Mordor Intelligence

The Europe automated guided vehicle market size is projected to be USD 1.67 billion in 2025, USD 1.87 billion in 2026, and reach USD 3.12 billion by 2031, growing at a CAGR of 10.78% from 2026 to 2031. Robust e-commerce fulfilment expansion, wage pressures in Western Europe, and accelerating Industry 4.0 programs across automotive and pharmaceutical plants are shortening payback periods for automation. Government incentives tied to the EU Green Deal are further tilting capital budgets toward zero-emission warehouse equipment, while Horizon Europe funds speed the commercialization of swarm-intelligent traffic control and natural-feature SLAM navigation. As fixed infrastructure becomes a liability, operators favour fleets that can remap layouts overnight, leading to stronger demand for sensor-rich vehicles and unified fleet-management software.

Key Report Takeaways

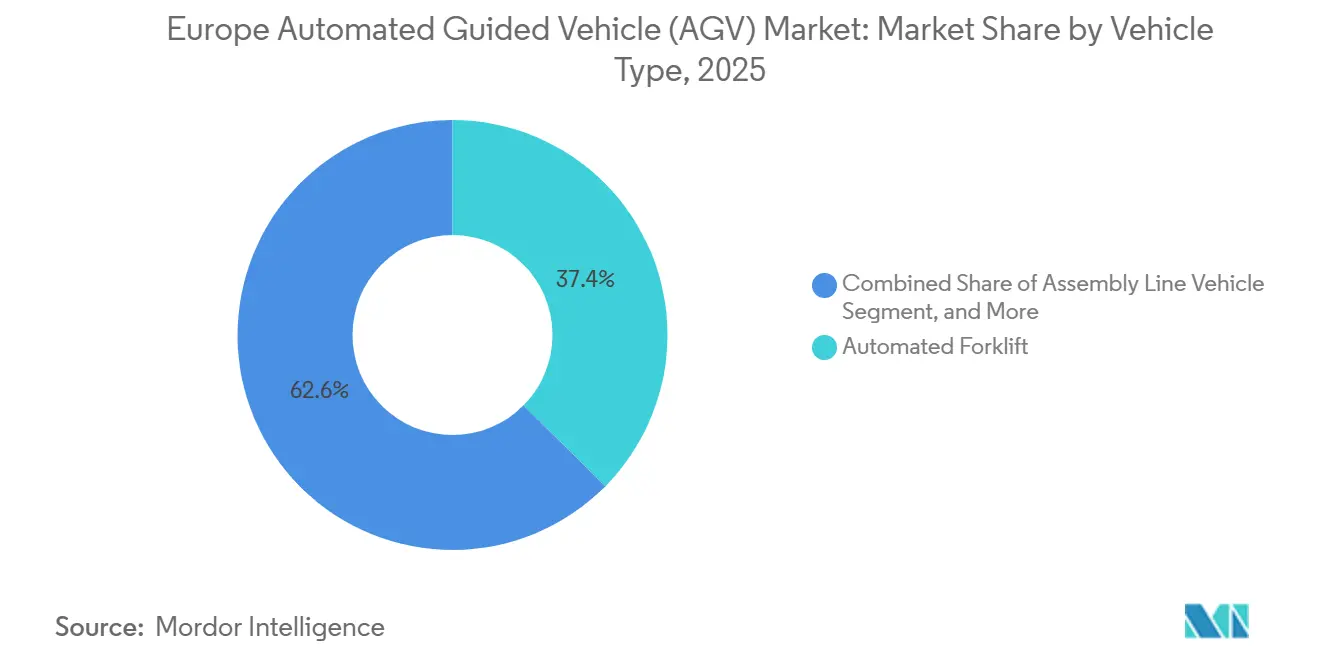

- By vehicle type, automated forklifts led with 37.41% revenue share in 2025, whereas assembly line vehicles are advancing at an 11.21% CAGR through 2031.

- By navigation, laser-guided systems retained 44.16% of the Europe automated guided vehicle market share in 2025, yet natural-feature SLAM is recording an 11.52% CAGR to 2031.

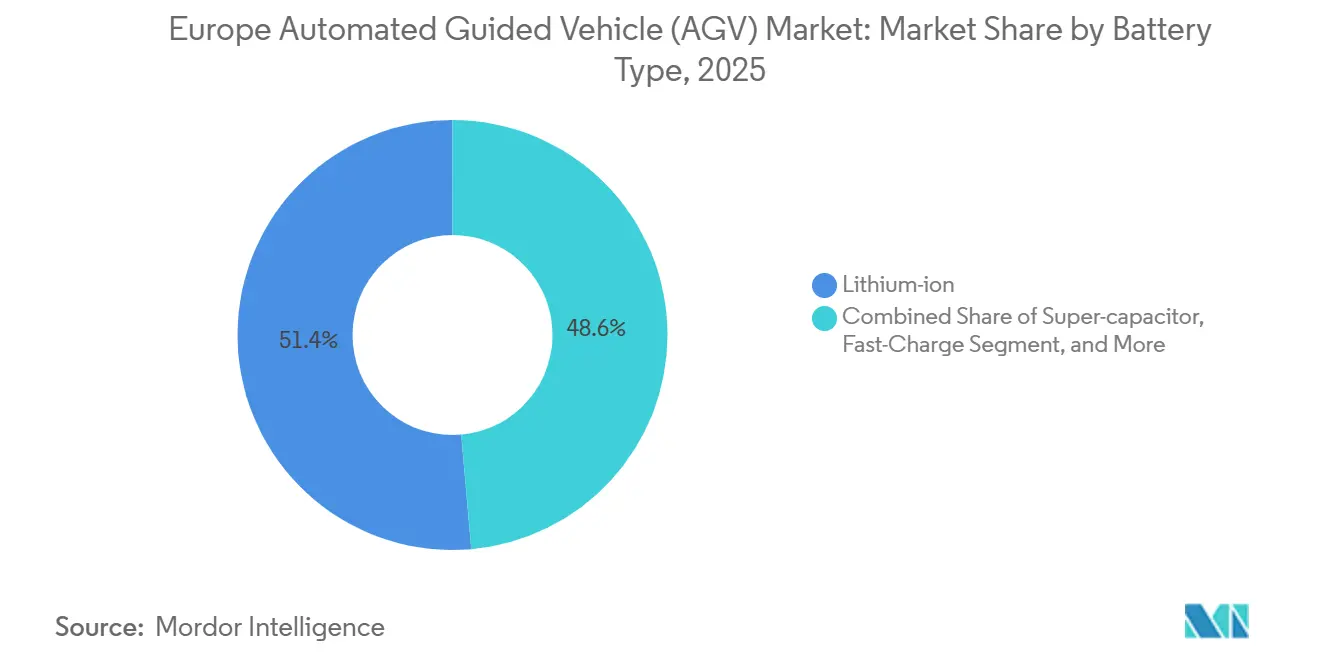

- By battery chemistry, lithium-ion accounted for 51.39% of installations in 2025 and super-capacitor fast-charge packs are set to expand at an 11.34% CAGR over 2026-2031.

- By mode, fully autonomous units accounted for 46.32% of deployments in 2025 and are forecast to grow at a 11.96% CAGR, outpacing hybrid dual-mode fleets.

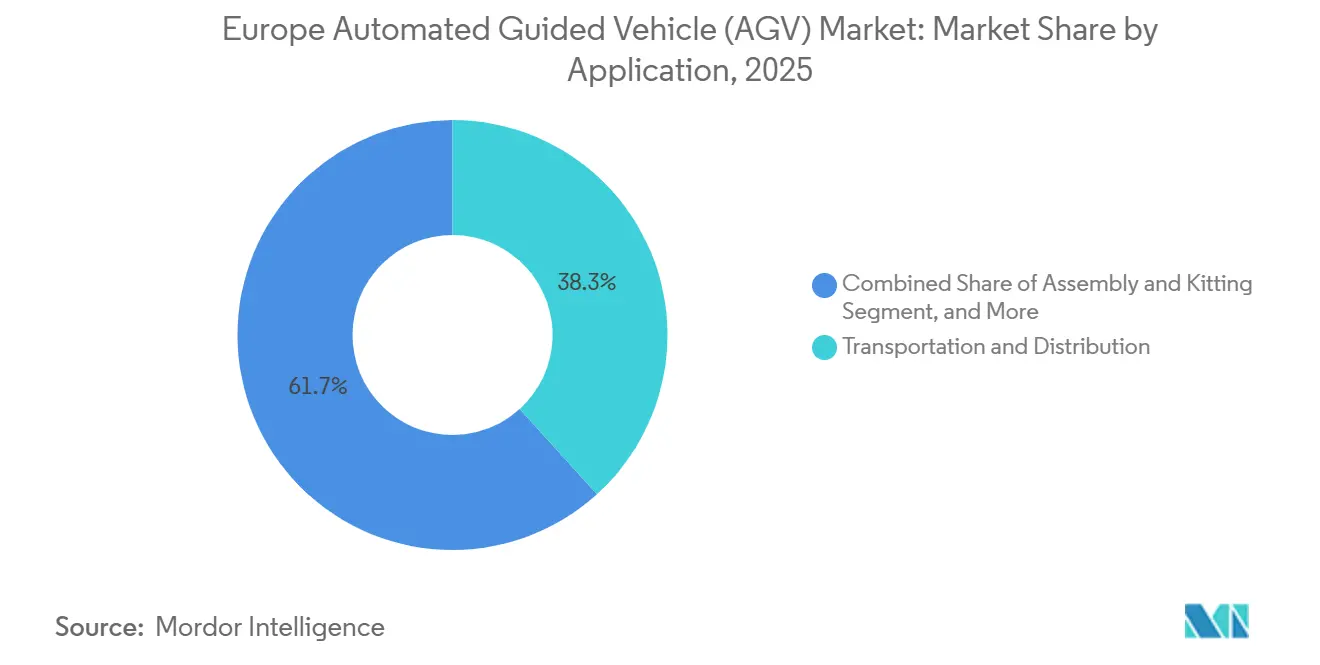

- By application, transportation and distribution commanded 38.27% revenue in 2025, while assembly and kitting posts an 11.27% CAGR to 2031.

- By end-user, automotive generated 27.91% of 2025 revenue, but pharmaceuticals is the quickest mover with an 11.82% CAGR through 2031.

- By country, Germany captured 24.54% of 2025 sales, and the Netherlands is set to expand at an 11.59% CAGR on the back of port and air-cargo automation.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Automated Guided Vehicle (AGV) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce Fulfillment Centres Surge Across Urban Europe | +2.80% | Western Europe core (Germany, UK, France, Netherlands), expanding to Poland and Czech Republic | Medium term (2-4 years) |

| Industry 4.0 Enabled Flexible Manufacturing Lines in German Automotive Plants | +2.30% | Germany dominant, spillover to France, Italy, Spain automotive corridors | Short term (≤ 2 years) |

| Labour-Cost Inflation and Demographic Shortages in Western Europe Logistics Workforce | +2.10% | Western Europe (Germany, UK, Netherlands, France), acute in Scandinavia | Long term (≥ 4 years) |

| EU Green Deal Incentives for Low-Emission Intralogistics Equipment | +1.50% | EU-27 member states, strongest uptake in Germany, Netherlands, Nordic countries | Medium term (2-4 years) |

| Port Automation Projects in Rotterdam and Antwerp Boosting Maritime AGV Adoption | +1.20% | Netherlands (Rotterdam), Belgium (Antwerp), secondary ports in Hamburg, Le Havre | Short term (≤ 2 years) |

| Horizon Europe Funding for Next-Gen Swarm Navigation Algorithms | +0.90% | Pan-European research consortia, commercialization in Germany, Netherlands, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce fulfilment Centers Surge Across Urban Europe

Online retail’s penetration climbed to 21.3% of total European sales by 2025, compressing order cycles and driving dense micro-fulfillment hubs that require compact vehicles able to navigate shared pedestrian docks. Same-day delivery promises are pushing operators to triple throughput per square meter, so high-speed unit-load carriers now shuttle inventory between mezzanine pick faces and ground-floor consolidation at over 2 m s⁻¹. Payback periods for AGVs in the Netherlands and Germany have narrowed to 18-24 months as wages escalate and overtime premiums rise.[1]BMW Group, “Sustainability Report 2025,” bmwgroup.com These conditions place the Europe automated guided vehicle market in a structural sweet spot for sustained double-digit growth.

Industry 4.0 Enabled Flexible Manufacturing Lines in German Automotive Plants

BMW and Volkswagen plants use cloud-based traffic control to reroute vehicles in real time, eliminating fixed conveyors and cutting line stoppages by 34%. Mixed-model production demands sub-10 mm positioning accuracy, prompting manufacturers to favour natural-feature SLAM over magnetic tape. The result is a rising share of assembly line vehicles within the Europe automated guided vehicle market, supported by standardized ISO 3691-4 safety logic across vendors.[2]ISO, “ISO 3691-4 Driverless Industrial Trucks,” iso.org

Labor-Cost Inflation and Demographic Shortages in Western Europe Logistics Workforce

The logistics wage index in Germany rose 8.4% in 2026, while the EU forecasts a deficit of 426,000 commercial drivers by 2030. AGVs help operators redeploy scarce labour to exception handling and maintenance, making automation financially attractive even for mid-volume warehouses. Eastern European 3PLs are adopting AGVs pre-emptively to hedge against wage convergence with Western Europe, adding further momentum to the Europe automated guided vehicle market.

EU Green Deal Incentives for Low-Emission Intralogistics Equipment

The Innovation Fund covers up to 40% of capital costs for zero-emission material-handling fleets, accelerating lithium-ion and hydrogen fuel-cell adoption.[3]European Commission, “Innovation Fund Overview,” ec.europa.eu Germany offers accelerated depreciation, and the Netherlands grants a 15% tax credit on battery systems, tipping total-cost-of-ownership in favour of electrified AGVs. Regenerative braking in lithium-ion models recovers up to 40% of kinetic energy, aligning with corporate sustainability targets and broadening the addressable base for the Europe automated guided vehicle market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-front System Integration and Customisation Costs for SMEs | -1.80% | Broad European SME base, acute in Southern Europe (Italy, Spain, Portugal) | Short term (≤ 2 years) |

| Fragmented European RF Spectrum Causing Network Latency in Dense Warehouses | -1.20% | Multi-country logistics operators, cross-border facilities in Benelux, Rhine corridor | Medium term (2-4 years) |

| Lengthy CE-Mark and ISO 3691-4 Safety Certification Lead-Times | -0.70% | EU-27 member states, new entrants and custom AGV variants | Short term (≤ 2 years) |

| Limited Availability of Skilled AGV Systems Integrators | -0.50% | Eastern Europe, Southern Europe, smaller metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front System Integration and Customization Costs for SMEs

Integration packages for a sub-20,000 m² warehouse can exceed EUR 400,000 (USD 429,000), including Wi-Fi upgrades and middleware coding. Payback stretches beyond 36 months for single-site operators, deterring many family-owned firms in Italy and Spain. Robotics-as-a-service models are emerging but remain under-penetrated where asset-based lending is less mature.[4]Balyo launched a retrofit navigation kit that autonomously converts existing forklifts, with pilot projects in Italy and Spain.

Fragmented European RF Spectrum Causing Network Latency in Dense Warehouses

Regulatory variance in 5 GHz Wi-Fi allocations forces multi-country operators to design site-specific networks, adding up to 12 weeks to commissioning schedules. Latency spikes above 200 ms can trigger emergency stops, so some automotive plants invest in private 5G, but costs run to EUR 2 million (USD 2.1 million) per facility. Until spectrum harmonizes, reliability concerns will temper adoption rates within the Europe automated guided vehicle market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Flexible Assembly Line Vehicles Gain Traction

Assembly line vehicles are registering an 11.21% CAGR as mixed-model plants demand precise, just-in-sequence delivery. Automated forklifts still account for the largest slice of the Europe automated guided vehicle market size at USD 0.62 billion in 2025, but their growth is moderating in space-constrained warehouses.

Tow tractors shuttle cart trains across automotive campuses, and unit-load carriers dominate contamination-sensitive pharmaceutical sites. Custom vehicles from coil handlers to paper-roll movers fetch premium prices yet limited volumes. The shift toward lighter footprints and cloud-orchestrated fleets indicates continuing diversification of vehicle form factors within the Europe automated guided vehicle market.

By Navigation Technology: Natural-Feature SLAM Challenges Laser Dominance

Laser guidance retained 44.16% of 2025 revenue because reflectors still deliver centimeter accuracy in high-throughput hubs. However, SLAM’s 11.52% CAGR signals that operators value the ability to re-map a floor layout overnight without moving targets or magnetic tape. The Europe automated guided vehicle market size tied to SLAM navigation is poised to double by 2031 as LiDAR sensors drop below USD 1,000 per unit.

Vision-guided and magnetic systems occupy niches such as cleanrooms, where optical occlusion or floor excavation demands specialized guidance. Horizon Europe’s SESAME swarm project further tilts the playing field toward infrastructure-free mapping and decentralized traffic arbitration.

By Battery Type: Super-Capacitors Offer 24-Hour Utilization

In 2025, lithium-ion packs powered 51.39% of fleets, bolstered by local cell production at CATL's Hungary facility. This growth is attributed to the increasing adoption of lithium-ion technology due to its higher energy density, longer lifespan, and lower maintenance requirements compared to traditional battery technologies. Super-capacitor AGVs, which recharge in just 15 seconds, are witnessing an 11.34% CAGR, making them perfect for sortation hubs with continuous shifts. These AGVs are particularly advantageous in high-demand environments, as their rapid recharging capability minimizes downtime and enhances operational efficiency. Despite a 50% higher upfront cost, their million-cycle lifespan significantly reduces lifetime expenses, making them a cost-effective solution in the long term.

Lead-acid batteries remain in use primarily where capital expenditure constraints overshadow downtime penalties, a trend notably observed in Southern Europe. However, their limited lifespan and higher maintenance needs make them less favorable for high-duty-cycle applications. As a result, super-capacitors are poised to steadily increase their share in Europe's automated guided vehicle market, particularly for high-duty-cycle applications, driven by their superior performance and cost-efficiency over time.

By Mode of Operation: Fully Autonomous Fleets Accelerate

Fully autonomous units held 46.32% of deployments in 2025 and are advancing at an 11.96% CAGR, outpacing hybrid dual-mode fleets as operators gain confidence in mature obstacle-avoidance algorithms and ISO 3691-4 safety logic. Lights-out warehouses that rely on these vehicles eliminate the 25-50% nightshift wage premium common in Germany and the Netherlands, improving return on invested capital and freeing scarce labour for value-added quality checks. The Europe automated guided vehicle market size tied to fully autonomous modes is therefore widening faster than any other operational class, especially in e-commerce hubs that process more than 50,000 orders daily.

A second adoption vector comes from automotive paint and body shops, where welding sparks and particulate matter used to force recurring manual interventions. New sealed-sensor housings and predictive path-planning now allow the same fleets to operate safely in high-heat, high-debris zones, extending runtime and reducing unscheduled maintenance windows by 18%. Vendors that pre-certify autonomous logic under ISO 3691-4 shorten commissioning by eight weeks, a decisive edge for plants facing quarterly model-change deadlines. As a result, procurement teams are shifting RFQs toward turnkey autonomous packages that bundle fleet-management software, remote diagnostics, and over-the-air updates, cementing fully autonomous operation as the default specification for greenfield projects through 2031.

By Application: Assembly and Kitting Surpass Traditional Transport

Assembly and kitting applications are expanding at an 11.27% CAGR, outpacing the overall Europe automated guided vehicle market. Transportation and distribution still contributed the largest slice of revenue in 2025 at 38.27%, yet its growth is moderating as high-volume pallet shuttling nears saturation across first-wave e-commerce hubs. Storage and retrieval usage sits in a mature niche where AGVs link automated storage and retrieval systems to floor conveyors, while packaging and palletizing vehicles find traction in food and beverage plants that require stainless enclosures and IP69K sealing. Assembly lines now rely on sub-meter positioning accuracy so that mixed-model plants can deliver battery trays, fuel tanks, or hydrogen storage modules to the same workstation without pausing the takt time. This precision need is steering procurement toward natural-feature SLAM and vision-guided units instead of magnetic tape, shrinking re-layout downtime from weeks to days and raising the Europe automated guided vehicle market size tied to flexible workflows.

The second growth lever is the migration to cloud-based fleet managers that optimize task sequencing across transport, kitting, and palletizing jobs in one platform. Operators achieve 75-80% loaded-mile ratios, trimming empty travel by 15 percentage points compared with manual forklifts and boosting labour reallocation toward exception handling. Lights-out night shifts magnify the return as vehicles keep queues balanced ahead of the morning wave of outbound parcels. In cold-storage groceries, packaging AGVs eliminate propane emissions and convert waste heat from motor drives into compartment warming, preventing frost on sensors that once stopped lead-acid forklifts. Collectively these factors widen the Europe automated guided vehicle market share of high-mix, high-throughput applications and reinforce the case for investments that bundle kitting, transport, and palletizing modules into a single payback model.

By End-User Industry: Pharmaceuticals Post the Fastest Gains

Automotive maintained 27.91% of 2025 revenue, but pharmaceuticals are posting the quickest climb with an 11.82% CAGR to 2031 as biologics, cell therapy, and vaccine plants require ISO Class 5 cleanliness and 2 °C-8 °C temperature corridors. Cleanroom-grade AGVs feature sealed wheel hubs, HEPA filtration, and electrostatic shielding so batches move between fill-finish suites and cold vaults without operator contact, satisfying good manufacturing practice audits and traceability mandates. Food and beverage facilities leverage stainless chassis and wash-down compatibility for meat, dairy, and frozen goods, although their uptake pace hinges on commodity price swings that tighten capex cycles. Retail and e-commerce centers remain volume drivers for pallet movers and tow tractors, yet wage spikes are tilting those operators toward collaborative robots that share pedestrian aisles. Electronics and electrical manufacturers deploy unit-load carriers inside dust-sensitive rooms, preventing particulate contamination that could ruin semiconductor wafers or printed circuit boards.

The Europe automated guided vehicle market size linked to pharmaceutical sites is set to double as rapid fill-finish capacity expansions across Denmark, Ireland, and Germany bake automation into greenfield layouts from day one. Automotive growth is plateauing because new electric-vehicle plants already spec AGVs in their core designs, leaving incremental gains to model-change tooling rather than wholesale retrofits. Food processors are trailing super-capacitor packs that recharge during 15-second label-print cycles, eliminating battery swaps inside minus 25 °C freezers. Retail warehouses are piloting hybrid fleets were kitting robots stage seasonal gift sets for human pickers, pushing end users toward software-centric vendor evaluation. Across sectors, early movers report 12-18% working-capital reductions from just-in-sequence delivery and 30-40% lower energy use versus diesel or lead-acid fleets, reinforcing the long-term competitiveness of AGVs and sustaining momentum in the Europe automated guided vehicle market share grabbed by regulated, hygiene-critical industries.

Geography Analysis

Germany captured 24.54% of 2025 sales thanks to dense automotive clusters, advanced robotics programs, and logistics corridors along the Rhine-Ruhr. Wage inflation of 8.4% in 2026 cut automation payback to under two years, while federal incentives accelerated the switch to lithium-ion fleets.

The Netherlands is the fastest grower at an 11.59% CAGR. Rotterdam’s fully automated APM Terminals III and Schiphol’s cargo hub illustrate how port and air-cargo nodes catalyse warehouse robotics investments. Dutch labour costs above EUR 25 h⁻¹ and a chronic driver shortage reinforce the need for 24-hour AGV utilization.

The United Kingdom, France, Italy, and Spain show mature but steady demand patterns, each anchored by either automotive or e-commerce hubs. Eastern Europe and the Nordics round out the region, leveraging lower land costs yet higher wages to justify new greenfield AGV deployments. Combined, these dynamics secure a broad runway for the Europe automated guided vehicle market through the forecast horizon.

Regulatory Landscape

Safety and conformity for the Europe AGV market rely on CE-marking requirements and harmonized standards for driverless industrial trucks. EN ISO 3691-4:2023 is used by AGV and AMR suppliers as the core harmonized safety standard to support presumption of conformity for machinery safety, influencing vehicle design parameters (speed and braking performance, protective measures, functional safety) and the validation documentation requested by end users in automotive, logistics, and pharmaceuticals.

Competitive Landscape

The market is moderately concentrated. KION Group posted EUR 11.3 billion (USD 12.1 billion) in 2023 revenue, while Jungheinrich recorded EUR 5.5 billion (USD 5.9 billion) in 2024, underscoring the scale advantage of diversified material-handling portfolios. Toyota Material Handling, Swisslog, and Dematic bundle AGVs with cranes and shuttle systems, locking customers into multi-year service contracts.

Disruptors such as AGILOX and Mobile Industrial Robots target high-mix, human-shared spaces with swarm-controlled or collaborative units that install in days instead of weeks. Balyo’s retrofit kits convert legacy forklifts at half the cost of new vehicles, appealing to SMEs seeking incremental automation. Access to Horizon Europe grants accelerates the proofs of concept these start-ups need to penetrate tier-one manufacturers.

Certification speed is emerging as a differentiator. Vendors that pre-qualify modules under ISO 3691-4 shave eight weeks off lead times, a critical edge when e-commerce peaks approach. Over the next five years, partnerships between sensor suppliers, battery makers, and software firms will further fragment the value chain, but scale players are expected to remain dominant in complex greenfield megasites.

Europe Automated Guided Vehicle (AGV) Industry Leaders

KUKA AG

Toyota Material Handling Europe AB

Jungheinrich AG

Swisslog Holding AG

Dematic (KION Group)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A transition is underway in EU machinery rules. Regulation (EU) 2023/1230 will fully apply from 20 January 2027, replacing the Machinery Directive 2006/42/EC and tightening obligations for autonomous and software-driven machinery.

Alongside this, the European Commission adopted a proposal for an Industrial Accelerator Act in March 2026 (COM(2026) 100 final). The proposal is aimed at streamlining permit-granting for industrial manufacturing projects, which could shorten deployment timelines for automation-capable facilities and reinforce their role as prime sites for AGVs.

Recent Industry Developments

- June 2026: KUKA deployed a fleet of 22 autonomous mobile robots for automated material transport at a leading European TV manufacturer in Gorzow Wielkopolski, Poland, with integration delivered by partner Saicon. The project points to demand for production-grade AMR deployments in European factories and underscores the systems integrators role in linking vehicle fleets to shopfloor processes.

- March 2026: Toyota Material Handling Europe launched Swarm Automation Transport, pairing the SAI125CB automated counterbalance stacker with the T-ONE control system to orchestrate mixed transport flows across multiple vehicle types and fit brownfield sites where humans and automation share space. This highlights operator interest in mixed-fleet control rather than single-vehicle rollouts.

- December 2025: Jungheinrich expanded Alfred Ritter GmbH & Co. KG's internal logistics automation at Dettenhausen, Germany, moving toward a scalable multi-line material-flow with integrated control systems and lithium-ion technology. The update supports ongoing attention to integrating AGVs into broader material-flow control.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers revenue generated from automated guided vehicles used for indoor material movement in Europe, including the vehicles and the navigation and power setups sold with them, across industrial and warehouse settings.

Scope exclusions: We exclude fixed automation such as conveyors and AS/RS that do not operate as vehicles, and we also exclude aftermarket parts-only sales when they are not tied to an AGV sale.

Segmentation Overview

- By Vehicle Type

- Automated Forklift

- Tow, Tractor and Tug

- Unit-Load Carrier

- Assembly Line Vehicle

- Special-Purpose, Custom

- By Navigation Technology

- Laser Guided

- Magnetic, Inductive Guided

- Vision Guided

- Natural Feature, SLAM

- By Battery Type

- Lead-acid

- Lithium-ion

- Nickel-Metal Hydride

- Super-capacitor, Fast-Charge

- By Mode of Operation

- Manual Override

- Hybrid, Dual-Mode

- Fully Autonomous

- By Application

- Transportation and Distribution

- Storage and Retrieval

- Assembly and Kitting

- Packaging and Palletising

- By End-User Industry

- Automotive

- Food and Beverage

- Retail and E-commerce

- Electronics and Electrical

- General Manufacturing

- Pharmaceuticals

- Aerospace and Defence

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public signals that can explain how fast factories and warehouses in Europe are modernizing, and what this means for AGV demand. We reviewed sources such as Eurostat for industrial production and labor indicators, EU-OSHA and national safety bodies for workplace automation context, the European Commission and national transport and industry ministries for policy direction, and customs and trade statistics for relevant material handling equipment movements.

To keep assumptions realistic, we also used company annual reports and investor presentations to understand product mix and regional exposure, along with association and event publications that describe adoption patterns in automotive, food, retail, and general manufacturing. In a few cases, we referenced paid subscriptions focused on company financials and news, patent activity, and shipment-level trade flows to cross-check timing and direction of growth. These desk sources are not exhaustive, and many other public references were used to collect data, validate inputs, and clarify open questions.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions that most often change the final number, such as typical system pricing, deployment size, replacement cycles, and adoption speed by end-user industry. We spoke with a mix of manufacturers, integrators, distributors, and large end users across major European countries so that coverage reflected both mature sites and late adopters, and then we used follow-up checks to confirm outliers before finalizing inputs.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 17% | |

| Mid tier: 48% | Functional/Unit leaders: 40% | |

| Smaller Players: 22% | Managers: 43% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand-pool approach, where manufacturing output, warehouse automation intensity, and AGV penetration by site type were used to reconstruct annual spending in Europe, and then the totals were checked through selective bottom-up approximations. Those bottom-up checks included sampled ASP ranges by vehicle type, typical fleet sizes per deployment, and channel and integrator validations that helped adjust for undercounting in smaller projects.

Key model inputs (illustrative) included new warehouse space additions and upgrades, labor cost pressure and vacancy signals, automotive and electronics production cycles, safety and uptime requirements that push automation, and the shift from lead-acid to lithium-ion that changes system pricing over time. Forecasts were built using scenario analysis, where base-case adoption curves by end-user industry were combined with expected macro and industrial output paths, and the scenario weights were refined using what interviewees shared about budget timing and project pipelines. When bottom-up data was missing for smaller countries, ratios were inferred from similar markets using industrial activity and logistics intensity, and the assumptions were then rechecked in expert follow-ups.

Data Validation & Update Cycle

Validation was done through several rounds of checks so the final number stayed consistent with real-world activity. We compared model outputs against independent signals such as industrial production direction, warehouse investment headlines, and observed pricing patterns, and then we reviewed any sharp jumps that did not match these indicators.

Before sign-off, the analysis goes through internal reviews where assumptions are challenged, and sensitivity checks are rerun to see what drives the range most. Reports are refreshed annually, and interim updates are made when material events occur that can change adoption or pricing. Right before delivery, the latest public updates are re-scanned so the view reflects the most current market conditions.

Mordor Intelligence's Europe Automated Guided Vehicles Market Size Measured Against Other Published Estimates

Published market values for Europe AGVs often do not match because the market boundary is not consistent, and the time reference can shift between shipment year, booking year, or installed base expansion. Differences also come from how firms treat related automation categories, how they model system pricing over time, and whether their assumptions are verified with on-the-ground demand signals.

Order activity seen through integrator pipeline discussions, tender and project announcements, and the observed ASP range by vehicle type are the checks that keep Mordor Intelligence tied to a Europe-only AGV revenue pool, which is why the 2025 value lands where it does in our view. When these checks are not used, estimates can drift because adoption can be overstated in sectors that are still piloting, or pricing can be carried forward without reflecting battery and navigation mix changes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.67 B (2025) | |

| Regional Consultancy A | USD 1.12 B (2024) | Uses an earlier base year and a wider country list that can shift timing, and the sizing approach appears to lean on segment listings without clearly separating AGVs from adjacent mobile robotics spend. |

| Global Consultancy B | USD 0.87 B (2026) | Starts from a later base year with a narrower definition that emphasizes selected AGV types and navigation options, which can undercount projects bundled with hybrid or custom vehicles and services in Europe. |

The spread in the table mainly comes from year selection and what is counted inside an AGV deal, especially when systems are sold as part of a broader automation project. By anchoring the total to repeatable demand indicators and then cross-checking with practical price and deployment norms, the estimate stays transparent and can be revisited cleanly when new evidence appears.

Key Questions Answered in the Report

How large will the Europe automated guided vehicle market be by 2031?

It is forecast to reach USD 3.12 billion, expanding at a 10.78% CAGR from 2026 to 2031.

Which vehicle type is growing fastest?

Assembly line vehicles, supported by flexible automotive manufacturing, are advancing at an 11.21% CAGR through 2031.

What navigation technology is gaining share?

Natural-feature SLAM is expanding at an 11.52% CAGR as operators avoid fixed infrastructure.

Why are pharmaceuticals adopting AGVs quickly?

Cold-chain mandates and GMP compliance boost demand, giving pharmaceuticals the highest end-user CAGR at 11.82%.

Which country offers the strongest growth outlook?

The Netherlands leads with an 11.59% CAGR, driven by port and air-cargo automation investments.

What is the main hurdle for SMEs?

Up-front integration costs can exceed EUR 400,000, extending payback beyond three years for single-site operators.

Page last updated on: