Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

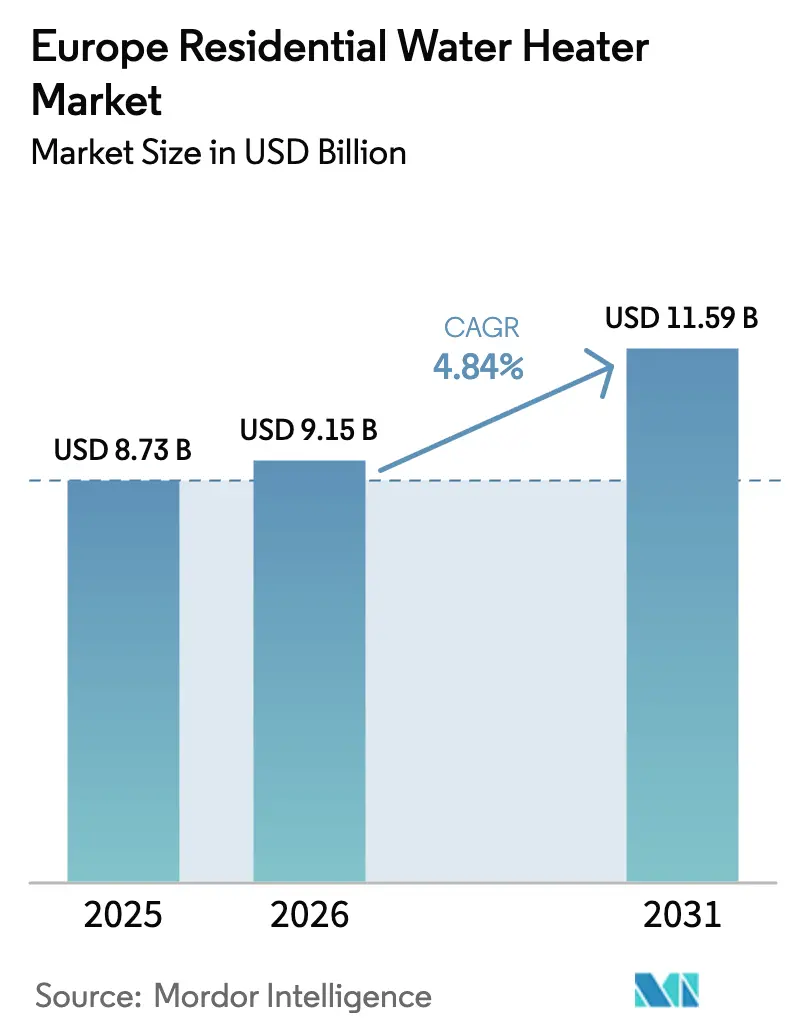

| Base Year Market Size (2025) | USD 8.73 Billion |

| Market Size (2026) | USD 9.15 Billion |

| Market Size (2031) | USD 11.59 Billion |

| Growth Rate (2026 - 2031) | 4.84% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Residential Water Heater Market Analysis by Mordor Intelligence

The Europe Residential Water Heater Market size was valued at USD 8.73 billion in 2025 and estimated to grow from USD 9.15 billion in 2026 to reach USD 11.59 billion by 2031, at a CAGR of 4.84% during the forecast period (2026-2031).

The growth reflects stringent decarbonization mandates, rising electrification, and incentive programs that rapidly replace fossil-fuel appliances. Demand strengthens as consumers shift toward connected units that integrate with building energy management systems, enabling demand-response participation and lowering lifetime operating expenses. Competitive activity centers on natural-refrigerant heat pump launches, software-driven optimization features, and supply-chain localization that mitigates component shortages. Regulatory timelines differ by country, yet manufacturers with pan-regional product platforms that meet EU Ecodesign 2024/1781 standards are positioned to capture disproportionate gains.

Key Report Takeaways

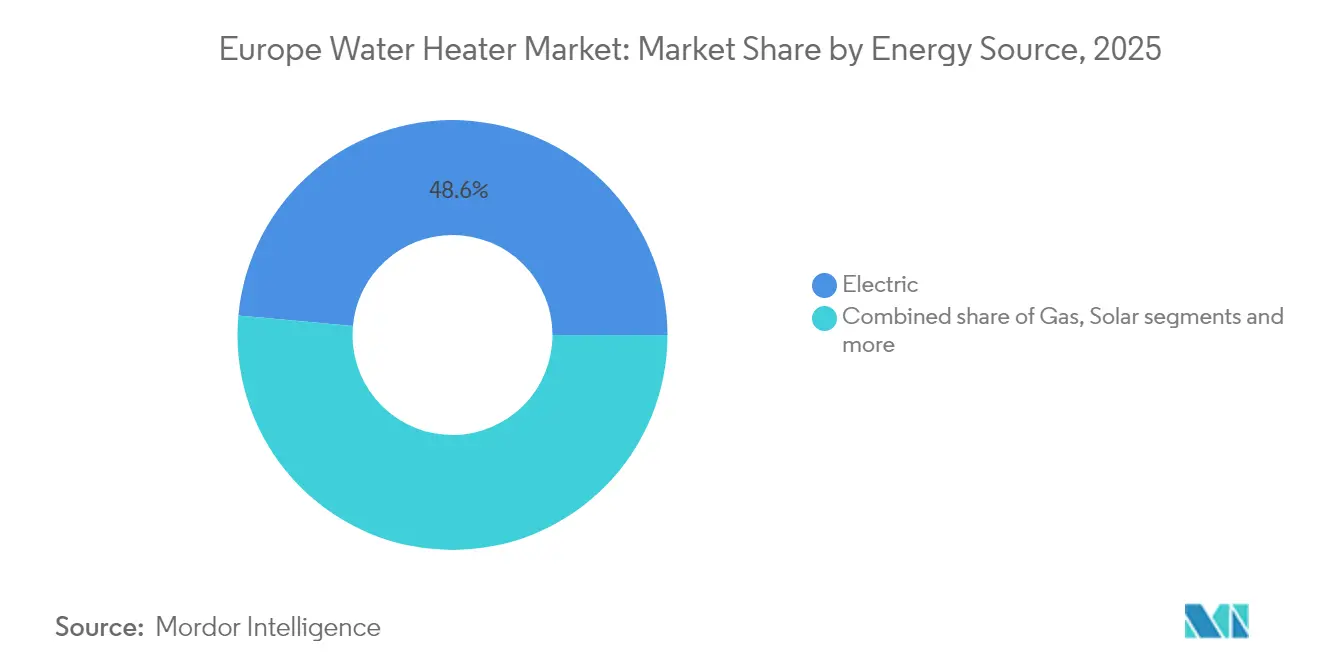

- By energy source, electric heaters captured 48.55% of Europe residential water heater market share in 2025, while solar units are forecast to grow at a 5.52% CAGR from 2026-2031.

- By product type, storage systems held 67.10% revenue share of the Europe residential water heater market in 2025; instantaneous models are expected to advance 5.48% through 2031.

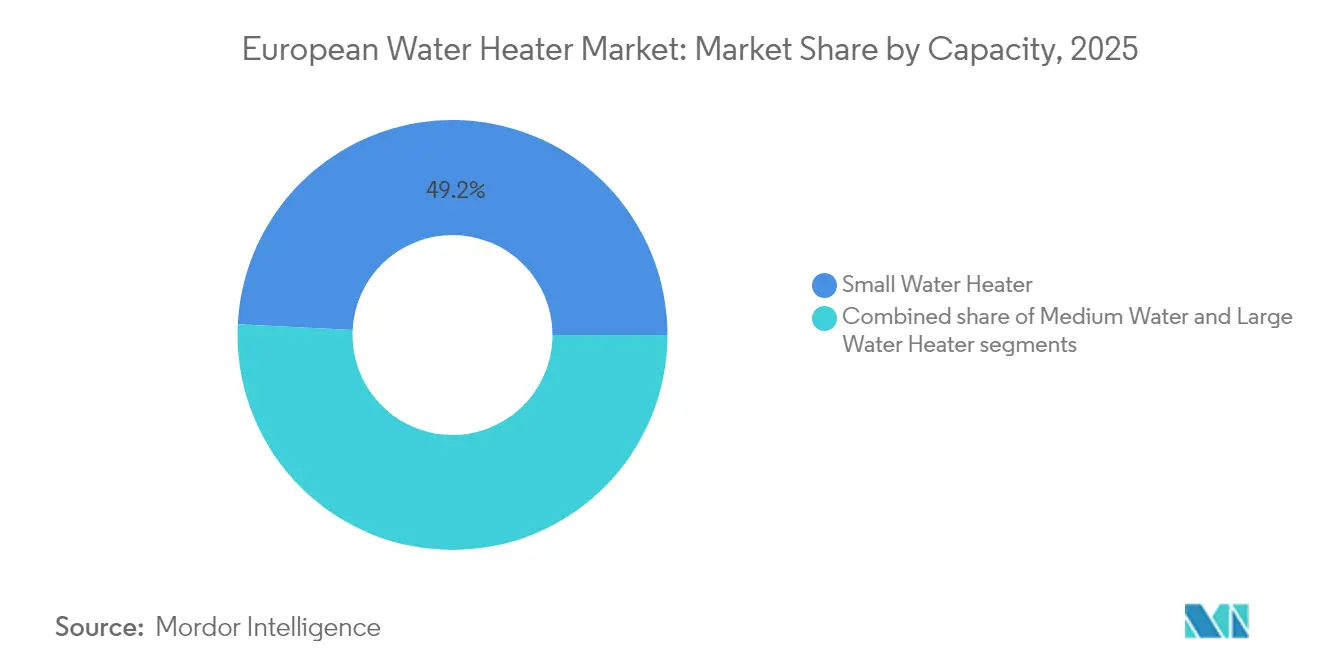

- By capacity, small (<100 L) systems represented 49.20% of the Europe residential water heater market size in 2025, yet medium units are projected to expand 5.24% between 2026-2031.

- By distribution channel, multi-brand retail outlets maintained a 45.05% share of the Europe residential water heater market in 2025, whereas online platforms should record a 6.46% CAGR.

- By country, Germany accounted for 18.20% of the Europe residential water heater market in 2025, but BENELUX is set to outpace all peers at a 5.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Residential Water Heater Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Eco-design & Energy-Labelling tightening | +1.2% | EU-wide, with early implementation in Germany, Netherlands | Medium term (2-4 years) |

| Renovation-wave replacements of ageing boilers | +1.0% | Germany, UK, France, with spillover to Eastern Europe | Long term (≥ 4 years) |

| Accelerated heat-pump WH uptake for decarbonisation | +0.9% | BENELUX, Nordic countries, with expansion to Southern Europe | Medium term (2-4 years) |

| Electrification subsidies & VAT exemptions | +0.8% | Spain, Italy, UK, with varying implementation across EU | Short term (≤ 2 years) |

| Peer-to-peer energy communities using WHs as thermal batteries | +0.4% | Germany, Netherlands, Denmark with pilot programs | Long term (≥ 4 years) |

| Plug-and-play monobloc heat-pump retrofit kits | +0.3% | France, Germany, UK focusing on apartment buildings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Concentration of market share being high in few countries like Germany,France and Italy

The 2024/1781 regulation prohibits low-efficiency models, creating immediate white-space for A-rated units that achieve top performance bands[1]European Commission, “Renovation Wave for Europe,” ec.europa.eu. Natural-refrigerant heat pumps benefit most because their life-cycle global-warming potential is sharply lower than HFC systems, unlocking green-finance eligibility for manufacturers. Stricter label visibility directs consumers toward premium devices even at higher ticket prices, strengthening margins for firms that pair efficiency with connected features. Smaller producers lacking R&D bandwidth confront rising compliance costs, accelerating consolidation as larger brands acquire distressed rivals. Market entrants emphasizing digital controls and demand-response interfaces gain added leverage because smart functionality now boosts label scores under revised testing protocols.

Renovation-Wave Replacements of Aging Boilers

Roughly 100 million residential boilers exceed 20 years of service across the EU, and renovation mandates compel their phased removal. Germany’s Gebäudeenergiegesetz stipulates renewable-ready replacements, England’s Future Homes Standard requires ≥75% CO₂ cuts, and France layers cash bonuses on fossil-fuel change-outs. These policies expand addressable volume for the European water heater market, giving manufacturers predictable multi-year demand visibility. Financing support through national green-loan schemes further accelerates the switch, enabling bundled upgrades that include heat-pump water heaters, insulation, and rooftop PV. Service providers respond with turnkey packages that merge equipment, installation, and performance guarantees, locking in annuity-style revenue streams.

Accelerated Heat-Pump Uptake for Decarbonization

Heat-pump water heaters deliver coefficients of performance above 4.0 in moderate climates and maintain efficiency via variable-speed compressors in sub-zero regions. Unit costs continue to fall as compressor output scales and European gigafactories ramp electronic-module supply. The BENELUX bloc illustrates upside: Dutch heat-pump sales are set to rebound 41% in 2025 after regulatory clarity restored consumer confidence. Utilities integrate these assets into virtual-power-plant programs, paying owners for peak-shaving contributions and trimming payback periods to 3-5 years. Ecosystem compatibility with rooftop solar allows prosumers to convert midday surplus into stored hot water, reinforcing heat-pump value propositions.

Electrification Subsidies & VAT Exemptions

Zero-rate VAT on UK heat-pump installations plus £7,500 grants remove 40-60% of upfront cost barriers[2]Gov.uk, “Boiler Upgrade Scheme Statistics 2024,” gov.uk. Spain’s municipal programs add 50% IBI property-tax discounts and 95% ICIO fee cuts for heat-pump adopters, shifting total ownership economics decisively toward electric units. Italy’s Conto Termico 3.0 earmarks EUR 900 million annually, reimbursing up to 65% of project costs and smoothing cash-flow hurdles for households. Sales spikes often precede incentive sunset dates, so producers hold buffer inventory and flexible staffing to address demand surges. Cross-border installers exploit subsidy gaps, prompting regulators to tighten residency checks to sustain local economic benefits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront price of low-carbon systems | -0.8% | EU-wide, particularly affecting price-sensitive segments in Eastern Europe | Short term (≤ 2 years) |

| Fuel-price volatility blurring payback visibility | -0.6% | Germany, UK, Netherlands with high energy price sensitivity | Short term (≤ 2 years) |

| Installer skill gap for next-gen technologies | -0.4% | Germany, UK, France with acute skilled labor shortages | Medium term (2-4 years) |

| EU cybersecurity mandate for connected heaters | -0.3% | EU-wide, with early compliance requirements in Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Price of Low-Carbon Systems

Residential heat-pump water heaters cost EUR 2,000-4,000 more than resistive or gas analogs once installation upgrades are tallied[3]Italian Ministry of Economic Development, “Conto Termico 3.0 Guidelines,” mise.gov.it. Emergency replacement buyers prioritize speed, pushing like-for-like swaps that delay efficiency gains. Installation labor shortages inflate quotes 15-25%, particularly in dense urban zones. Leasing models and energy-service contracts partially offset sticker shock through monthly payments funded by utility savings. Mass-market cost parity hinges on modular retrofit kits and simplified refrigerant charging that trim labor hours without compromising safety.

Fuel-Price Volatility Blurring Payback Visibility

Fluctuating retail electricity versus gas prices complicate household ROI calculations despite the mechanical efficiency advantages of heat pumps[4]Eulerpool, “German Heat Pump Sales 2024 Report,” eulerpool.com. Consumers react to energy-price news cycles, creating erratic purchase timing and channel switching. Governments experiment with price caps and tariff reforms that favor electrification, yet policy-driven volatility remains a perception risk. Manufacturers counter with integrated monitoring apps that present real-time savings, reinforcing value transparency. Wider adoption of fixed-rate green-electricity contracts promises to stabilize long-term economics and reassure hesitant buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Energy Source: Electric Strength, Solar Momentum

Electric residential heaters held a 48.55% share of the Europe residential water heater market in 2025, reflecting ample renewable electricity and straightforward installation. Solar units, buoyed by record-low PV panel costs, are poised for a 5.52% CAGR to 2031, carving new space in the Europe residential water heater market. Gas models remain in retreat as carbon-pricing schemes erode competitiveness. Electric-heat-pump designs qualify for EU Green Taxonomy lending, cutting capital costs by up to 75 bps. Hybrid solar-assisted pumps bridge cloudy-day performance gaps, maximizing self-consumption ratios.

Storage-focused electric heaters double as thermal batteries, letting utilities curtail wind-curtailment waste by scheduling night-time charging. Solar-thermal collectors integrate with buffer tanks, cutting compressor runtime by 20-25%. Natural-refrigerant compliance future-proofs portfolios against tighter F-Gas caps entering force in 2027, sustaining product relevance within the Europe residential water heater market. Gas-booster hybrids linger in some retrofit-challenged multifamily dwellings but lose share annually. Future growth hinges on solar-PV+heat-pump packages bundled under a single permit to streamline homeowner paperwork.

By Product Type: Storage Dominance, Instantaneous Uptick

With a 67.10% revenue, storage heaters dominate, keeping the Europe water heater market resilient because they buffer peak draws and align with dynamic tariffs. Instantaneous units, the fastest segment at 5.48% CAGR, resonate in space-starved apartments that typify urban cores. Storage models leverage phase-change insulation that curbs standby loss below 0.8 kWh/day, approaching tankless efficiency. Tankless heaters upgrade with modulating burners and PLC-based flow sensors, eliminating scald-risk fluctuations.

Premium storage tanks integrate legionella-protection cycles and Wi-Fi diagnostics that alert installers before failure, strengthening aftermarket revenue. Tankless systems win DIY favor; however, the required 3-phase wiring can offset installation savings. Hybrid configurations emerge, storing 40-60 L while deploying on-demand boosts for shower spikes, blending benefits across the Europe residential water heater market. Regulation-driven hydraulic balancing in multifamily retrofits slightly tilts the share back to tanks, as central buffer solutions ease pipe-run redesign complexity.

By Capacity: Small Units Lead, Medium Rise

In 2025, small heaters (those under 100 L) accounted for 49.20% of shipments, a trend driven by the prevalence of single-bath dwellings and studios in European cities. These compact units are particularly favored in urban areas where space constraints are significant, offering an efficient solution for limited living spaces. Meanwhile, medium units (ranging from 100-200 L) are projected to grow at a CAGR of 5.24% through 2031. This growth is attributed to the rise in household hot-water demands from teleworking and the increasing adoption of heat pumps, which benefit from larger buffers to maintain their Coefficient of Performance (COP). Medium units are also gaining traction in suburban homes, where families require a balance between capacity and energy efficiency.

Vacuum-insulated panels, compact cylinders can fit into 60 cm cabinetry, making them ideal for renovation constraints. These features cater to the growing trend of modernizing older European buildings, where space optimization is critical. Medium heat-pump systems are now equipped with smart dividers, allowing independent service to the shower, dishwasher, and laundry zones. This innovation enhances comfort while minimizing energy waste, aligning with the region's focus on energy efficiency and sustainability. Large cylinders are integrating multi-coil architectures, enabling connections to solar, boiler, and immersion-backup loops, thus future-proofing them for complex sites. These systems are particularly suited for multi-family residences and commercial establishments that require versatile and reliable hot water solutions.

By Distribution Channel: Retail Stronghold, Online Surge

Multi-brand stores held 45.05% channel share in 2025, backed by installer loyalty, immediate stock availability, and physical demos that reassure end-users. Online outlets will climb 6.46% annually as transparent pricing, product comparators, and doorstep delivery sway younger homeowners. Exclusive-brand boutiques target premium segments seeking curated advice and after-sales service, while wholesale distributors dominate bulk orders for property developers. The Europe residential water heater market leverages omnichannel tactics, meshing e-commerce convenience with brick-and-mortar expertise through click-and-collect models. Augmented-reality apps let shoppers simulate heater footprints, narrowing choice before store visits.

Click-and-collect marries web convenience with physical pickup, cutting last-mile costs by 30%. Retailers bundle finance and certified installation to combat e-commerce erosion. E-tailers answer by offering virtual-reality product demos and installer-matching algorithms, reducing friction for heat-pump projects. Omnichannel loyalty programs track serial numbers, enabling predictive-maintenance upsells that enlarge lifetime value inside the Europe residential water heater market.

Geography Analysis

Germany accounted for 18.20% of the Europe residential water heater market size in 2025, drawing on its advanced manufacturing base and progressive building codes. Heat-pump sales dipped 21% in 2024 during political debates over the Gebäudeenergiegesetz, but policy clarity and federal grants covering up to 70% of project costs are expected to revive demand in 2025. Local champions Vaillant and Viessmann continue investing in R&D, with Vaillant opening an electronics line in Remscheid to de-risk semiconductor supply. Grid-interactive pilot projects in Bavaria demonstrate revenue stacking, where heat-pump water heaters earn virtual-power-plant payments that shorten payback periods. German technical standards often become de facto templates for continental certification regimes.

The BENELUX bloc is poised to post a 5.76% CAGR through 2031, the fastest inside the Europe residential water heater market, on the back of aggressive decarbonization laws and subsidy depth. Dutch proposals mandating hybrid or all-electric heating for new builds after 2026, plus revolving-loan funds that cover installer training, spur rapid channel expansion. Belgium supplements federal incentives with regional grants, allowing homeowners to reclaim up to 70% of capital outlays. Luxembourg leverages high disposable income to push premium heat-pump penetration beyond 60% of new sales by 2027. Manufacturers view BENELUX as a testbed for ultra-high-efficiency prototypes before broader EU rollouts.

The United Kingdom, France, Spain, and Italy collectively represent a critical growth cluster for the Europe residential water heater industry. Britain’s Boiler Upgrade Scheme experienced a 75% application jump in 2024 after grant values rose to £7,500, underpinning robust 2025 order books. France offers aggregate incentives up to EUR 11,000 per household via MaPrimeRénov’ and gas-boiler scrappage bonuses, accelerating fossil-fuel exits. Spain bars boilers from municipal incentives starting 2025 while layering 50% IBI tax relief, catalyzing immediate replacement cycles. Italy’s Conto Termico 3.0 channels EUR 900 million annually to renewable heaters, ensuring sustained medium-term momentum. Nordic nations already boast high penetration, yet still upgrade to R290 refrigerants and smarter controls, maintaining a stable replacement market.

Competitive Landscape

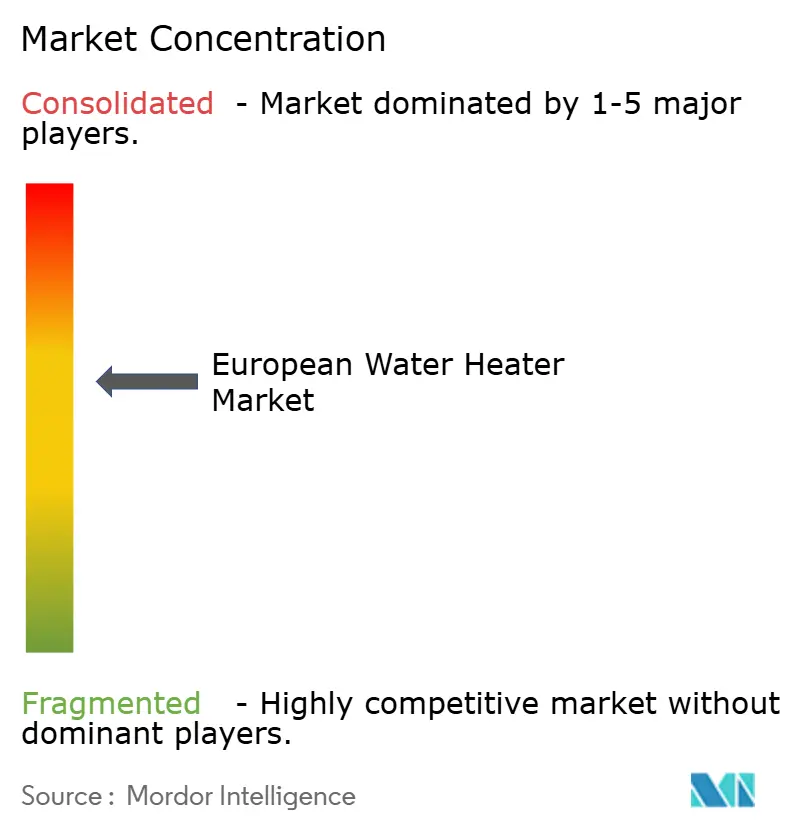

The Europe residential water heater market shows moderate concentration, with the top five suppliers holding major market share in 2024 revenues. Players' acquisition of Viessmann Climate Solutions scales up Carrier's operations and enhances brand integration, particularly in the premium heat-pump segment. Vaillant is integrating electronics and compressors, a move aimed at insulating itself from component price fluctuations. Meanwhile, Ariston is pushing boundaries with software ecosystems, capitalizing on after-sales optimization subscriptions. Disruptors like EcoFlow are shaking things up with direct-solar water heating, prompting established players to hasten their hybrid PV-plus-heat-pump offerings. Today, competitive advantage is increasingly derived from connected-service platforms, which secure customers through proprietary monitoring and maintenance contracts.

Strategic alliances proliferate: Viessmann partners with IBM for AI-based fault prediction, Ariston collaborates with Enel X on demand-response aggregation, and Bosch Thermotechnology pilots blockchain-verified energy-sharing communities. Natural-refrigerant adoption differentiates Europe brands from many Asian rivals still reliant on HFC blends, conferring regulatory head-start advantages. Manufacturers offering end-to-end installer academies mitigate the regional skills shortage, creating captive channel ecosystems that favor their product lines. White-label OEM deals expand reach into budget tiers without diluting flagship branding. Financial strength enables larger players to pre-buy semiconductors and heat-exchanger alloys, sustaining production during supply shocks.

Product roadmaps converge on three pillars: R290 refrigerants, grid-ready communications, and modular design for retrofit agility. Vaillant’s 2025 ISH launch revealed plug-in electronic boards that auto-configure refrigerant charge, lowering commissioning time by 30%. Ariston’s cloud dashboard provides hourly tariff optimization and water-usage analytics, enhancing stickiness and upsell potential for energy services. Carrier invests in shared component platforms across its multi-brand portfolio to exploit purchasing economies and shorten engineering cycles. EcoFlow champions direct-sales social-media tactics, cultivating a prosumer community that crowdsources feature updates. Price competition remains muted in upper-efficiency tiers where warranty, service network, and digital add-ons justify premium positioning.

Europe Residential Water Heater Industry Leaders

-

Ariston Holding N.V.

-

Robert Bosch GmbH (Bosch Thermotechnology)

-

Vaillant Group

-

Groupe Atlantic

-

Viessmann Werke GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: : Vaillant Group presented a full R290 heat-pump line at ISH 2025, integrating iQconnect electronics for app-based commissioning and remote performance tuning.

- February 2025: Viessmann Climate Solutions, incorporated into Carrier, launched the System Profi installer-certification program to harmonize training across Viessmann, Carrier, Riello, and Beretta brands.

- February 2025: Carrier debuted its Domestic Hot Water Air-to-Water Heat Pump at the International Builders’ Show, achieving a COP of up to 4.9 and showcasing technology transfer prospects for the European water heater market.

- January 2025: Samsung expanded its EHS air-to-water heat-pump platform to North America after deployment in 40+ European countries, featuring AI Home integration and SmartThings connectivity.

Europe Residential Water Heater Market Report Scope

Hot water heaters are appliances used to heat water and to keep it at a more or less constant elevated temperature. A complete background analysis of the Europe Residential Water Heaters Market, which includes an assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and logistics spending by the end-user industries, is covered in the report. Europe Residential Water Heaters Market is segmented By Product Type(Storage Water Heaters, Non-Storage Water Heaters and Hybrid Water Heaters), By Energy Source Type(Electric, Gas, Solar and Others), By Capacity(Small Water Heater, Medium Water Heater and Large Water Heater), By Distribution Channel (Multi-Branded Stores, Exclusive Stores, Online Stores and Other Distribution Channels) and By Geography (United Kingdom, Germany, France, Italy,Russia and Rest of Europe).

By Energy Source

| Electric |

| Gas |

| Solar |

| Other Energy Sources |

By Product Type

| Instantaneous Water Heaters |

| Storage Water Heaters |

| Hybrid Water Heaters |

By Capacity

| Small Water Heater |

| Medium Water Heater |

| Large Water Heater |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Country

| Europe |

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, and Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) |

| Rest of Europe |

| By Energy Source | Electric |

| Gas | |

| Solar | |

| Other Energy Sources | |

| By Product Type | Instantaneous Water Heaters |

| Storage Water Heaters | |

| Hybrid Water Heaters | |

| By Capacity | Small Water Heater |

| Medium Water Heater | |

| Large Water Heater | |

| By Distribution Channel | Multi-Brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| By Country | Europe |

| United Kingdom | |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

How large will the European water heater market be in 2031?

It is projected to reach USD 11.59 billion, reflecting a 4.84% CAGR.

Which technology currently leads sales?

Electric models account for 48.55% of 2025 revenue, driven by grid-decarbonization targets.

Why are heat-pump water heaters increasingly popular?

COP ratings above 4.0, generous subsidies, and VPP revenue opportunities shorten payback to 3-5 years.

Which region is the fastest-growing?

BENELUX should expand at a 5.76% CAGR through 2031, outpacing all other European sub-markets.

How are online channels influencing purchases?

E-commerce is the fastest-growing channel at 6.46% CAGR because buyers value transparent pricing and home delivery.

What refrigerant trend dominates new launches?

R290 propane is becoming standard to satisfy low-GWP rules under the latest Ecodesign framework.

Page last updated on: