Europe Quinoa Seeds Market Analysis by Mordor Intelligence

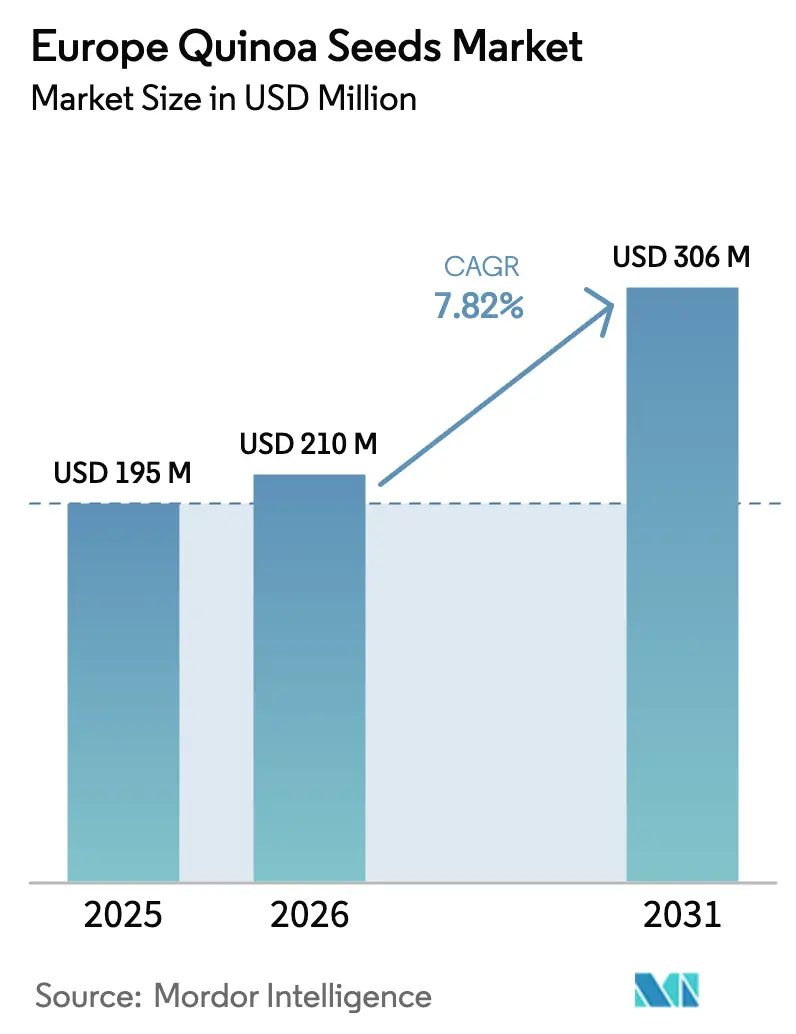

The Europe quinoa seed market size was valued at USD 195 million in 2025 and is estimated to grow from USD 210 million in 2026 to reach USD 306 million by 2031, at a CAGR of 7.82% during the forecast period (2026-2031). Structural diversification away from wheat and barley, policy incentives for alternative proteins, and the rapid uptake of gluten-free diets are shifting acreage toward quinoa across core-producing zones in France, Germany, and the United Kingdom. Price premiums for certified organic grain, averaging 35–45%, continue to outweigh higher input and de-saponization costs, supporting farmer margins even when South American imports pressure conventional grades. Ready-meal manufacturers have elevated demand by integrating quinoa into chilled and frozen lines sold through discount retailers, while aquaculture feed trials in Spain and Norway reveal non-food industrial potential that could unlock incremental volumes. The Europe quinoa seed market is also benefiting from the Common Agricultural Policy’s eco-scheme payments, which reward crop rotation diversity and partially offset growers’ learning-curve risks.

Key Report Takeaways

By Geography, France captured 29.4% of the Europe quinoa seeds market share in 2025, while Germany is advancing at an 11.7% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Quinoa Seeds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer demand for plant-based proteins | +1.8% | France, Germany, Netherlands, and United Kingdom | Medium term (2–4 years) |

| Growth in organic and gluten-free product sectors | +1.5% | Germany, France, United Kingdom, and Scandinavia | Medium term (2–4 years) |

| Government incentives for crop diversification | +1.2% | France, Germany, Spain, and Italy | Short term (≤ 2 years) |

| Expanding use in ready-meal manufacturing | +1.0% | Germany, United Kingdom, and Netherlands | Medium term (2–4 years) |

| Aquaculture feed integration of quinoa | +0.7% | Spain, Norway, and Scotland | Long term (≥ 4 years) |

| Heat-tolerant cultivars enabling southern Europe farming | +0.6% | Spain, Italy, and Southern France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand for Plant-Based Proteins

Flexitarian diets are shifting protein intake toward plant sources as urban millennials and Generation Z seek low-carbon food choices. Quinoa’s complete amino acid profile positions it as an attractive meat substitute in meal kits and quick-service food chains, especially in Germany, where plant-based protein consumption rose 18% in 2025, and quinoa captured 9% of that category [1]Source: BMEL, “Crop Production,” bmel.de. Institutional buyers reinforce volume stability. France’s school-lunch mandate requiring 50% plant-based proteins created a predictable domestic offtake. Suppliers that secure multi-year contracts with foodservice distributors can lock in premiums while South American cargoes continue to clear on volatile spot markets.

Growth in Organic and Gluten-Free Product Sectors

Organic quinoa commands 35–45% premiums over conventional grades, prompting acreage expansion in Germany as certified production continues to rise [2]Source: Organic Europe, “Annual Statistics,” organic-europe.net. European Union gluten-free sales reached EUR 3.8 billion (USD 4.1 billion) in 2025, advancing 12% annually as diagnoses of celiac disease and non-celiac gluten sensitivity rise [3]Source: European Commission, “Health Topics,” health.ec.europa.eu. Quinoa’s gluten-free status enables processors to avoid cross-contamination risks common to oats and wheat, and harmonized labeling under Regulation 828/2014 simplifies compliance across member states.

Government Incentives for Crop Diversification

The 2023–2027 Common Agricultural Policy earmarked EUR 387 billion (USD 418 billion) for eco-schemes that reward farmers adopting rotations with pseudocereals such as quinoa. France’s Ecophyto III program disburses EUR 150 (USD 162) per hectare for quinoa in low-input zones, while Spain funds seed subsidies through regional agencies. These incentives reduce Europe’s 14 million-metric-ton protein deficit and confer first-mover advantages on growers who master quinoa agronomy early.

Expanding Use in Ready-Meal Manufacturing

European ready-meal revenue reached EUR 28 billion (USD 30 billion) in 2025, and processors now value quinoa for rapid cook times and freeze-thaw stability. German firms such as Frosta and Apetito added quinoa bowls to chilled ranges sold through Aldi and Lidl, while United Kingdom producer Bakkavor lifted quinoa salad output 30% by relying on British Quinoa Company’s local harvests. Local sourcing not only compresses lead times but also shields processors from freight spikes such as those seen during the 2024 El Niño shipping crunch.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited agronomic know-how among farmers | -1.1% | France, Germany, Spain, and Italy | Short term (≤ 2 years) |

| Competition from low-priced South American imports | -0.9% | Netherlands, Germany, and United Kingdom | Medium term (2–4 years) |

| Stringent European Union pesticide-residue regulations | -0.6% | All member states | Medium term (2–4 years) |

| Saponin allergen concerns in infant foods | -0.4% | Germany, France, and Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Agronomic Know-How Among Farmers

Quinoa remained under 5,000 hectares in Europe during 2025, compared with 180,000 hectares in Peru and Bolivia. Photoperiod sensitivity requires precise planting windows, and Wageningen University trials showed yields decline 30–40% when sowing drifts two weeks from optimal dates. High-saponin varieties deter birds but require mechanical de-saponization, adding USD 216–324 per metric ton in processing costs, eroding returns. Limited extension capacity is slowing the diffusion of best practices, constraining acreage gains.

Stringent European Union Pesticide-Residue Regulations

The European Union policy will tighten maximum residue limits for chlorpyrifos and glyphosate in 2025. Compliance testing is expected to add USD 35–50 per metric ton to costs, posing a significant burden for small growers who lack the scale to distribute laboratory expenses. This increase in compliance costs may lead to reduced competitiveness for smaller players, potentially forcing some out of the market. Although the policy aims to protect consumer health by ensuring safer agricultural products, it inadvertently creates a higher financial barrier for new entrants. In contrast, larger, integrated firms with in-house quality laboratories are better positioned to absorb these costs, further consolidating their market advantage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

France dominates with 29.4% of the European quinoa seed market in 2025, with its maritime climate, subsidies under the Common Agricultural Policy (CAP), and cooperative de-saponization capabilities. Agricolor Quinoa's network consolidates smallholder production, reduces processing costs, and supplies grain to Carrefour's national distribution network. Imports are projected to grow significantly through 2031, indicating a persistent supply gap that Andean exporters and emerging European producers are anticipated to compete to address.

Germany’s consumption value is advancing at an 11.7% CAGR through 2031, reflecting the country’s dual role as a high-growth producer and a central logistics hub in Europe. The Europe quinoa seed market size in Germany is expanding quickly as organic premiums sustain farmers' incomes, and federal funding of USD 54 million over four years for protein crops accelerates research on photoperiod-insensitive varieties, re-exports of organic flakes and flour position German processors as regional price setters, especially toward Scandinavia.

The Netherlands remains the re-export gateway, but its arbitrage model faces two pressures include retailers demanding direct traceability and Andean exporters forging direct contracts with large chains. The United Kingdom, Spain, and Italy are cultivating regional niches. Andalusia’s quinoa cluster supports 30 pilot farms, while Emilia-Romagna trials quinoa in rotations with tomatoes and vegetables. Remaining European regions depend on imports, with climate risk and limited extension support delaying local scale-up.

Competitive Landscape

The competition in the European quinoa seed market is moderate and fragmented. South American exporters, including Andean Naturals, lead bulk commodity segments, leveraging scale and favorable exchange rates. European contract growers such as British Quinoa Company and Quinoa Marchfeld meet niche organic demand where consumers pay for transparent provenance. Vertically integrated processors, including Quinola and Ekibio, manage genetics, farming, processing, and retail packaging, insulating margins from import price swings.

Technology investment differentiates leaders. British Quinoa Company’s satellite-guided variable-rate seeding lifted yields 12% by matching plant density to soil moisture maps. Naturkost Übelhör installed optical sorters and nitrogen flushing in 2025, extending shelf life to 24 months and supporting exports to cold-chain-limited regions. European Union Intellectual Property Office (EUIPO) patent filings for heat tolerance and protein enhancement rose to 14 in 2025, signaling a trend toward defensible genetics.

Non-traditional entrants drive demand growth as Spanish aquaculture company Avramar is testing quinoa meal as a substitute for fishmeal, aiming to explore sustainable and cost-effective alternatives in aquaculture feed. Similarly, Dutch plant-based meat start-up Redefine Meat is utilizing quinoa protein isolate to enhance the texture of its products, addressing consumer demand for improved plant-based meat alternatives. Suppliers capable of providing ingredient-grade specifications can tap into higher-margin B2B channels, enabling them to diversify their revenue streams beyond traditional retail grain sales and cater to the evolving needs of innovative industries.

Recent Industry Developments

- September 2025: Whitworths introduced the Nutty Kitchen Supermince range, a plant-based meat alternative featuring red quinoa as a primary ingredient, along with walnuts and lentils. This launch aligns with the increasing demand for quinoa and other plant-based ingredients in alternative food products, emphasizing "unprocessed," high-fiber, and high-protein meat-free options.

- September 2025: Research initiatives, such as the Quinoa for Future Diversified Farming Systems (Q4F) project in Germany, aim to develop quinoa varieties suited to European climates. The objectives include enhancing domestic seed performance, increasing yields, and reducing reliance on imports.

- July 2025: Nature Bio Foods, a subsidiary of LT Foods specializing in organic products, has opened a new Business-to-Consumer (B2C) organic food facility in Maasvlakte, Rotterdam. The facility is designed to strengthen the company's position in the European organic market, with a focus on products such as quinoa, pulses, and oilseeds. It includes advanced packaging capabilities, storage capacity for 15,000 pallets, and supports a "Farm to Fork" supply chain model.

Europe Quinoa Seeds Market Report Scope

Quinoa is a cereal crop primarily cultivated for its edible seeds, which are naturally gluten-free, high in protein, and a good source of dietary fiber. The Europe quinoa seed market report is segmented by geography into the France, Germany, United Kingdom, Spain, and Italy. The report includes production analysis (volume), consumption analysis (value and volume), export analysis (value and volume), import analysis (value and volume), wholesale price trend analysis and forecasts, regulatory framework, list of key players, logistics and infrastructure, and seasonality analysis. Market forecasts are provided in terms of value (USD) and volume (metric tons).

By Geography

| France | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Germany | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| United Kingdom | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Spain | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis | |

| Italy | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |

| Wholesale Price Trend Analysis and Forecast | |

| Regulatory Framework | |

| List of Key Players | |

| Logistics and Infrastructure | |

| Seasonality Analysis |

| By Geography | France | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Germany | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| United Kingdom | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Spain | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Italy | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

Key Questions Answered in the Report

How big is the Europe Quinoa Seed Market?

The Europe quinoa seed market is projected to reach USD 210 million in 2026 and USD 306 million by 2031.

What is the current Europe Quinoa Seed Market size?

In 2025, the Europe quinoa seed market is estimated at USD 195 million

How fast is demand for quinoa growing in Europe?

Consumption value across Europe is advancing at an 11.7% CAGR in Germany and high single-digit rates elsewhere, driven by flexitarian diets and institutional foodservice mandates.

What makes European quinoa more expensive than South American grain?

Smaller farm scale, higher labor costs, stringent residue testing, and de-saponization expenses lift European production costs 20–30% above Andean imports.

Page last updated on: