Europe Protein Based Sports Drinks Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

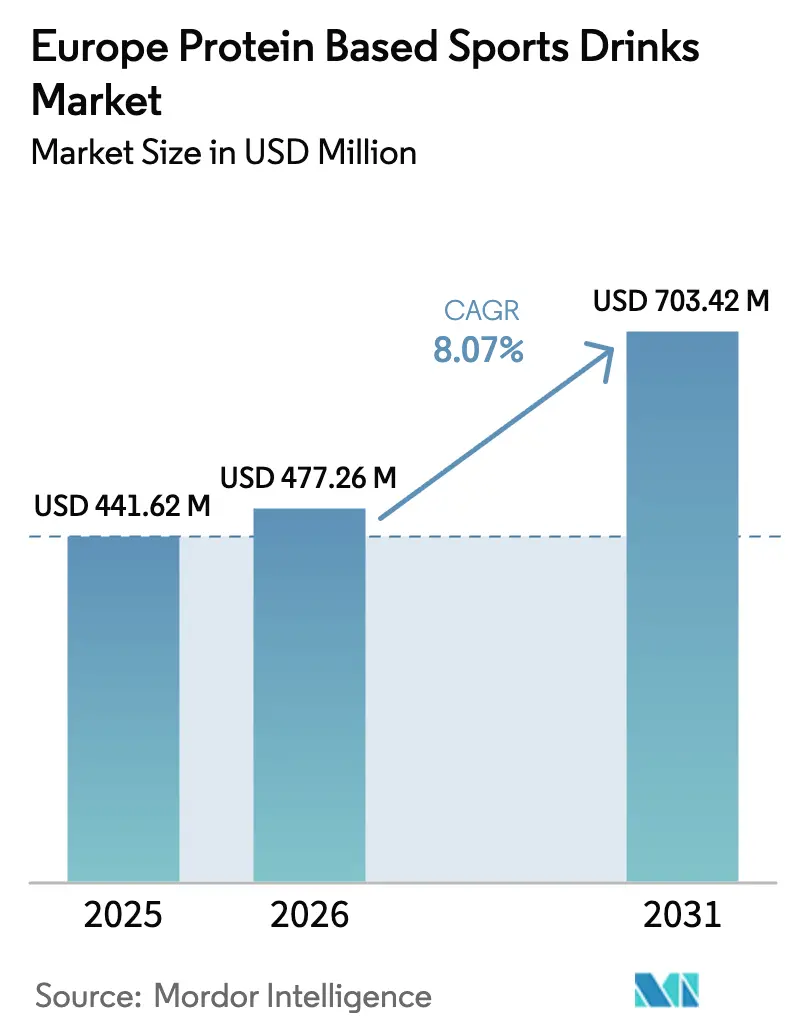

| Base Year Market Size (2025) | USD 441.62 Million |

| Market Size (2026) | USD 477.26 Million |

| Market Size (2031) | USD 703.42 Million |

| Growth Rate (2026 - 2031) | 8.07% CAGR |

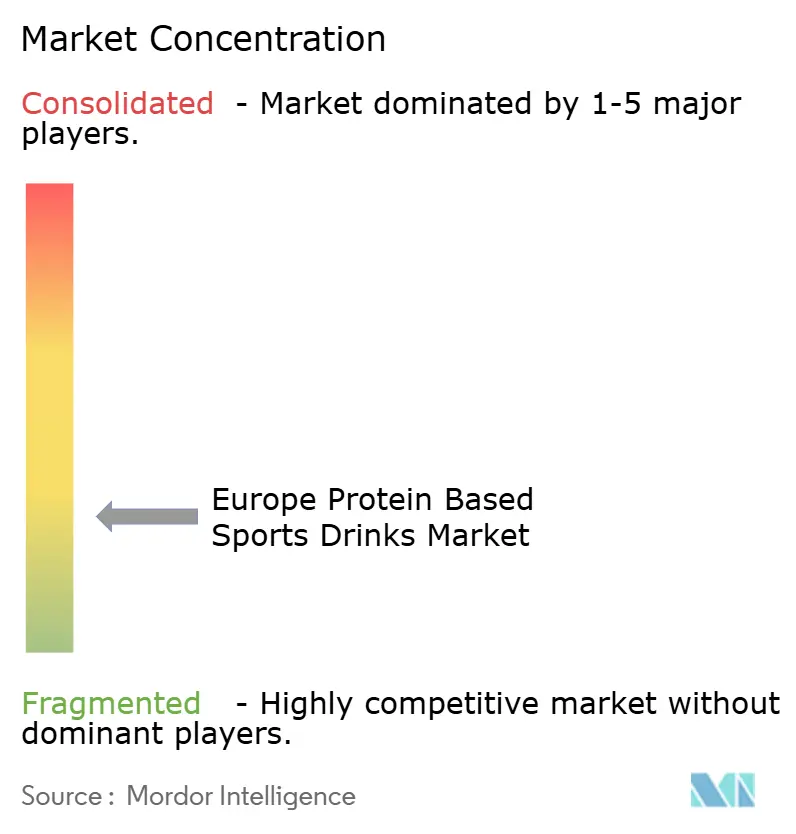

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Protein Based Sports Drinks Market Analysis by Mordor Intelligence

The European protein sports drinks market size is expected to grow from USD 441.62 million in 2025 to USD 477.26 million in 2026 and is forecast to reach USD 703.42 million by 2031 at 8.07% CAGR over 2026-2031. Demand growth reflects a lasting shift in European dietary habits, with high-protein beverages migrating from post-exercise recovery niches into everyday wellness regimes. Rising health-club density, clear European Food Safety Authority (EFSA) guidance on allowable health claims, and frictionless direct-to-consumer logistics have collectively expanded the addressable buyer pool. Women now account for the majority of protein-seeking shoppers, a reversal from the male-led profile of a decade earlier, propelled by social-media advocacy and clinical links between protein intake and metabolic resilience. Retailers are also demanding more sustainable packaging, accelerating a transition from plastic to aluminum and paper-based formats. Input-cost volatility for dairy-derived whey, however, continues to squeeze margins for brands that lack long-term supply agreements.

Key Report Takeaways

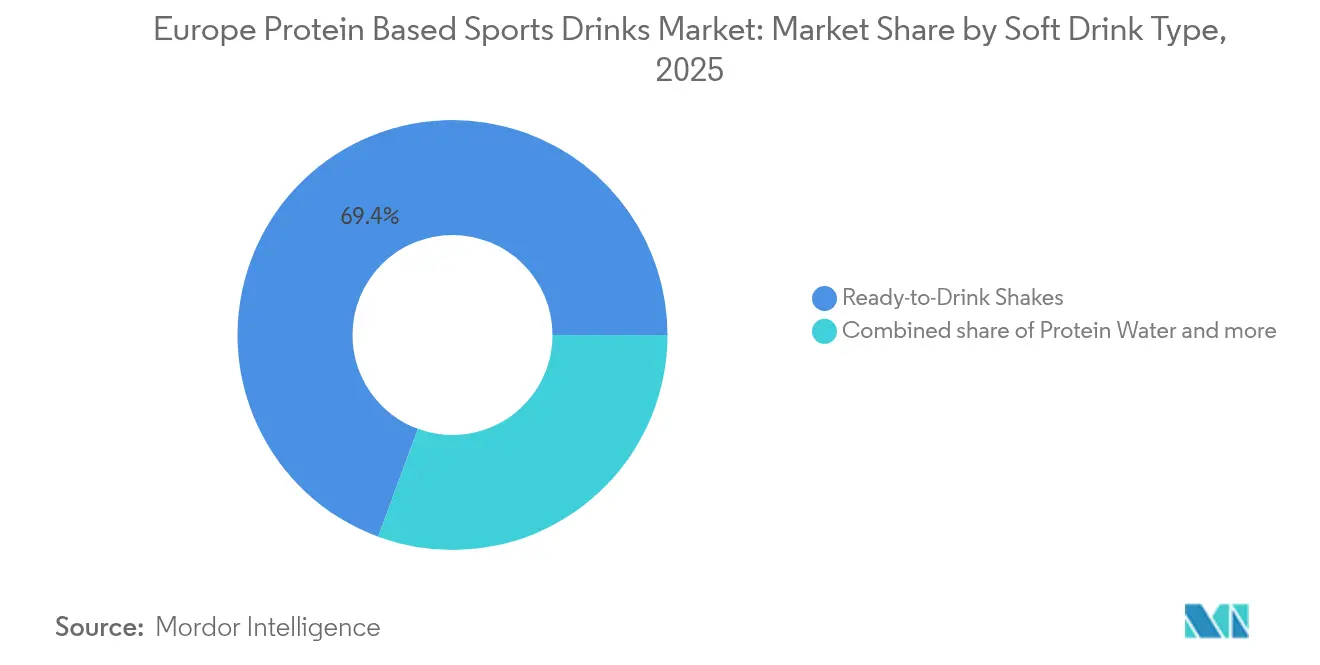

- By Soft Drink Type, ready-to-drink shakes captured 69.38% revenue in 2025 and are projected to compound at 8.92% through 2031, while clear protein waters represent the fastest-growing sub-format.

- By Source, animal-source beverages held 35.61% of the European protein sports drinks market share in 2025; plant-based alternatives are expanding at an 8.76% CAGR to 2031.

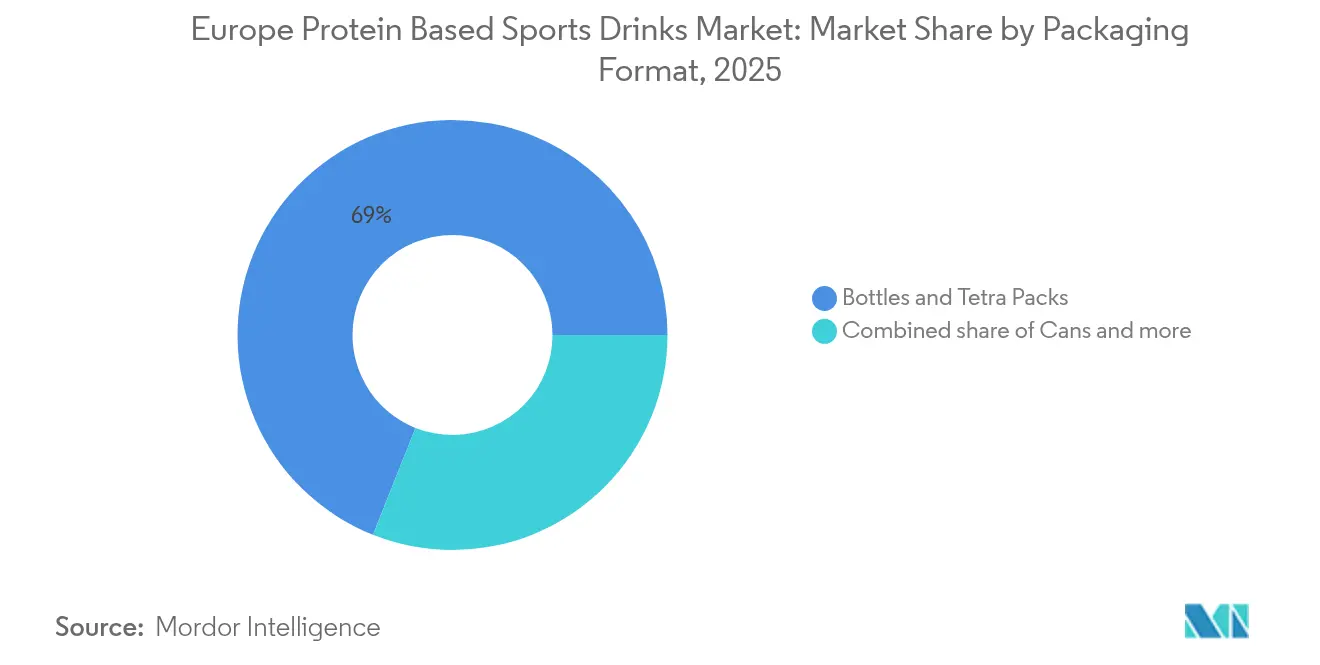

- By Packaging Format, bottles and cartons commanded 68.97% of packaging in 2025, but aluminum cans are rising at an 8.6% CAGR as retailers tighten recyclability mandates.

- By Distribution Channel, supermarkets and hypermarkets generated 42.55% of 2025 sales, yet online retail is scaling fastest, advancing at 9.74% CAGR on the back of subscription models.

- By Geography, the United Kingdom led the 2025 value at 37.28%, whereas Germany is set to grow at 9.06% CAGR, the quickest among large EU economies.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Protein Based Sports Drinks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient high-protein RTD beverages | +1.9% | Global, with the highest penetration in the United Kingdom, Germany, Netherlands | Medium term (2-4 years) |

| Expansion of fitness-centre memberships across Europe | +1.6% | Western Europe core (United Kingdom, Germany, France), spill-over to Poland, Spain | Long term (≥ 4 years) |

| E-commerce enabling direct-to-consumer distribution | +1.4% | North America and Europe, led by the United Kingdom, Germany, the Netherlands | Short term (≤ 2 years) |

| Surge in female consumer protein uptake for wellness | +1.2% | Global, particularly strong in Nordics (Sweden) and the United Kingdom | Medium term (2-4 years) |

| Growth of clear protein waters targeting hydration-plus-protein | +0.8% | Southern Europe (Spain, Italy), expanding to France | Medium term (2-4 years) |

| Precision-fermentation proteins lowering lactose allergen exposure | +0.6% | Western Europe (Germany, the Netherlands, Belgium), early regulatory approvals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient high-protein RTD beverages

In 2024, the European Journal of Clinical Nutrition published findings indicating that spreading protein intake across meals, specifically, 20 to 30 grams each, boosts muscle protein synthesis more effectively than a single dose post-workout. This insight has led European consumers to weave protein supplements into their daily lives, not just at the gym. Many now opt for ready-to-drink protein formats as meal replacements, whether during commutes or in between meetings. Responding to this shift, brands are reformulating their shakes, adding fiber, vitamins, and adaptogens, thus merging the realms of sports nutrition and functional food. For instance, Glanbia's Grenade Energy RTD, introduced in February 2024, packs 23 grams of whey isolate and 150 milligrams of caffeine, catering to office workers who often skip breakfast. Meanwhile, the European Food Safety Authority's regulatory oversight mandates that products touted as meal replacements adhere to specific micronutrient thresholds. This not only complicates product formulation but also bolsters consumer trust[1]Source: EFSA, “EU Nutrient Profiles,” efsa.europa.eu.

Expansion of fitness-centre memberships across Europe

Across Europe, the surge in fitness center memberships is fueling the growth of the protein-based sports drinks market, as consumers increasingly seek convenient post-workout nutrition. The European fitness sector, as highlighted in the EuropeActive Market Report 2025, has seen memberships soar to a record 71.6 million in 2024, a notable rise from 63.1 million in 2023[2]Source: EuropeActive, “European Health and Fitness Market Report 2024,” europeactive.eu. This uptick in active lifestyles, bolstered by government and public health campaigns advocating for regular exercise to tackle challenges like obesity, has cultivated a sizable consumer base eager for efficient muscle recovery and performance enhancement solutions. In light of this health-conscious trend, manufacturers are ramping up product innovations to cater to varied consumer tastes. Current developments are honing in on improving taste, texture, and digestibility. They're also emphasizing clean-label ingredients, functional perks (such as adaptogens and probiotics), and eco-friendly packaging (like recyclable cans), solidifying the role of these protein drinks in today's European fitness landscape.

E-commerce enabling direct-to-consumer distribution

In 2024, 77% of EU internet users made online purchases, with health supplements and sports nutrition accounting for 16% of the total online food and beverage transactions, as reported by Eurostat. Brands are increasingly adopting direct-to-consumer models, enabling them to bypass retailer margins that typically account for 30 to 35% of the wholesale price. This strategy lets brands reinvest those savings into customer acquisition, often leveraging influencers on platforms like Instagram and TikTok. Huel, a meal-replacement brand from the UK, reported revenues of GBP185 million (around USD 235 million) in 2024. Notably, 68% of its sales came from its own website and subscription service. The subscription model excels in the protein drinks sector, boasting repeat purchase rates of over 60%, in stark contrast to the 25% seen in more impulsive purchases like energy drinks. Thanks to Amazon's expansive pan-European fulfillment network, logistics costs have dropped. This shift enables smaller brands, such as UFIT, to match the delivery speeds of larger competitors without the overhead of maintaining warehouses in every country.

Surge in female consumer protein uptake for wellness

In Europe, women now account for 51% of consumers actively seeking protein. This demographic shift is largely attributed to social media campaigns that have successfully linked protein consumption to benefits like weight management, enhanced skin health, and improved metabolic resilience. In addition, the surge in popularity of GLP-1 agonist medications, such as Ozempic, has inadvertently spurred sales of protein drinks. This is because doctors are now advocating high-protein diets to help patients maintain lean muscle mass while undergoing rapid weight loss. In response, brands are pivoting their strategies, introducing lower-calorie formulations, adopting pastel packaging, and securing endorsements from wellness influencers, moving away from traditional endorsements by bodybuilders. A case in point is Danone's Alpro Sport, which debuted in March 2024. With 20 grams of plant-based protein and just 110 calories, it's specifically crafted for women aged 25 to 45, emphasizing clean labels over sheer protein density.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU labelling and health-claim regulations | -0.5% | EU-wide, with strictest enforcement in Germany and, Netherlands | Short term (≤ 2 years) |

| Price premium versus conventional sports drinks | -0.7% | Southern Europe (Spain, Italy), Eastern Europe (Poland) | Medium term (2-4 years) |

| Supply volatility of specialised whey-isolate inputs | -0.4% | Global, acute impact in Ireland, New Zealand dairy regions | Short term (≤ 2 years) |

| Consumer taste fatigue toward overly-sweet protein drinks | -0.3% | Western Europe (UK, Germany, France) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent EU labelling and health-claim regulations

In 2024, the European Commission revised Regulation 1924/2006, stipulating that any health claim associating protein with muscle maintenance or growth must be backed by a minimum of two independent clinical trials on EU populations[3]Source: European Commission, “Regulation 1924/2006 Update 2024,” europa.eu. This new stipulation has pushed product launches back by 6 to 9 months, as brands scramble to commission studies and await the European Food Safety Authority's review. Smaller manufacturers, lacking the capital for multi-site trials, find themselves at a disadvantage, leading to a market consolidation around established players like Glanbia and Abbott, who boast in-house clinical teams. In a clear message of zero tolerance for non-compliance, Germany's Federal Office of Consumer Protection issued 14 cease-and-desist orders in 2024 against brands making unapproved claims. The regulatory landscape is uneven: while all proteins are scrutinized, plant-based proteins face heightened challenges. This is largely because the EFSA has yet to define reference amino-acid profiles for pea or rice protein, compelling brands to over-formulate to maintain label accuracy.

Supply volatility of specialised whey-isolate inputs

In Q2 2024, spot prices for whey isolate jumped 18%, hitting EUR 15.20 per kilogram. This spike was driven by drought-related milk shortages in Ireland, Europe's top whey exporter, and a downturn in output from New Zealand due to bad weather. Such price fluctuations are squeezing gross margins for brands that depend on spot markets, as opposed to those with long-term contracts with dairy cooperatives. While Glanbia, with its own whey-processing facilities in Ireland, kept input costs steady, smaller brands like UFIT and PowerBar saw their margins shrink by 12 to 15%. The supply chain faces added constraints from consolidation: three cooperatives, Fonterra, Arla, and Glanbia, dominate 60% of global whey-isolate production, curbing buyers' negotiating power. Climate risks are on the rise; in 2024, heat stress led to a 4% dip in Ireland's dairy output, and analysts warn that extreme weather could cause annual price fluctuations of 10 to 15% through 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Soft Drink Type: Shakes Anchor Volume, Waters Target Premiumization

In 2025, ready-to-drink shakes seized a commanding 69.38% of the market share and are projected to expand at a robust 8.92% CAGR through 2031, solidifying their status as the category's backbone. Their leading position is attributed to matured formulations; brands have honed emulsification methods to avert protein separation, ensuring a creamy texture, and the convenience of 330-milliliter bottles, which easily slide into car cup holders and gym bags. Launched in February 2024, Glanbia's Grenade Energy RTD epitomizes this segment's progression, melding 23 grams of whey isolate with 150 milligrams of caffeine, positioning it as both a breakfast substitute and a pre-workout energizer. In Southern Europe, protein waters are gaining traction, with consumers linking opacity to heaviness and favoring transparent, fruit-infused drinks. Optimum Nutrition's Clear Protein Water, introduced in April 2024, employs enzymatic hydrolysis to transform whey into transparent peptides, subsequently infusing natural fruit extracts. Meanwhile, protein isotonic blends, merging electrolytes with 10 to 15 grams of protein, are becoming popular among endurance athletes. However, they face challenges: formulation issues can lead to protein precipitation in high-salt settings, as highlighted by the European Journal of Sport Science.

Within the "Others" category, which encompasses protein-enhanced coffees and teas, a notable 19% growth was recorded in 2024. Brands like Arla Foods tapped into this trend, debuting a cold-brew coffee infused with 20 grams of protein, specifically catering to morning commuters. The European Food Safety Authority's regulatory oversight mandates that products labeled as sports drinks adhere to specific electrolyte benchmarks. While this complicates the formulation of protein isotonic blends, it simultaneously elevates the entry barriers for new players. The segment's future trajectory is closely tied to flavor innovations; consumer feedback from Germany and the UK indicates a 20% higher refreshment rating for clear protein waters over traditional shakes, underscoring the potential of format diversification in driving premiumization.

By Source: Plant Proteins Gain Share Despite Amino-Acid Gaps

In 2025, animal-source proteins commanded a 35.61% market share, buoyed by the rapid digestion and superior amino-acid profile of whey isolate. However, plant-source proteins are on a faster trajectory, expanding at an 8.76% CAGR through 2031. This surge is fueled by the rise of flexitarian consumers and strategies to avoid allergens. Addressing the historical critique that plant proteins lack sufficient leucine for muscle protein synthesis, Danone's Alpro Sport, launched in March 2024, blends pea and rice proteins for a complete amino-acid profile. Nestlé's Garden Gourmet line, introduced in May 2024, utilizes fava-bean protein, a novel source with 30% lower carbon emissions than soy, catering to environmentally conscious consumers in Germany and the Netherlands. The plant-protein supply chain is evolving; in 2024, French ingredient supplier Roquette inaugurated a pea-protein facility in Belgium with a capacity of 20,000 metric tons. This move not only slashed input costs by 12% but also positioned brands to price plant-based drinks within 10% of their whey-based counterparts.

Within the animal-source segment, egg-white protein and collagen peptides carve out niche markets, appealing to those who eschew dairy yet desire animal-derived amino acids. In 2024, Post Holdings' Premier Protein debuted a collagen-infused shake in the UK, touting joint-health benefits for consumers aged 50 and above. The plant-versus-animal discourse remains contentious: 2024 clinical studies in the British Journal of Nutrition reveal whey protein's 18% edge over pea protein in stimulating muscle protein synthesis on a gram-for-gram basis. Yet, plant proteins boast a 70% reduction in greenhouse-gas emissions, presenting a dilemma between performance and sustainability. In response to this divide, brands are diversifying their offerings; Glanbia's Optimum Nutrition markets both the whey-based Gold Standard and its plant-based counterpart, Gold Standard Plant, side by side, empowering consumers to choose based on their values.

By Packaging Format: Aluminum Cans Rise on Sustainability Mandates

In 2025, bottles and tetra packs held a dominant 68.97% share of the packaging market, thanks to established filling infrastructures and consumer familiarity. However, cans are on an upward trajectory, boasting an 8.6% CAGR through 2031. This surge is driven by retailer sustainability mandates and the infinite recyclability of aluminum. In response to the rising demand from protein-drink brands, Ball Corporation, the globe's leading beverage-can manufacturer, ramped up its European production capacity by 15% in 2024. Retail giants Tesco and Carrefour declared in 2024 their intent to favor shelf space for aluminum or glass beverages over plastic ones by 2026, hastening the industry's shift. According to Packaging Europe, cans have a leg up: they shield contents from light and oxygen more effectively than PET bottles, extending shelf life from 9 to 12 months and curbing spoilage-related waste. In 2024, Science in Sport shifted its REGO Protein line to cans, highlighting the consumer trend towards on-the-go formats that conveniently fit in gym lockers.

In Central and Eastern Europe, where cold-chain infrastructure lags and consumers lean towards shelf-stable products, aseptic cartons, multi-layer paperboard containers designed for ambient storage, are gaining traction. Tetra Pak rolled out a protein-optimized carton in 2024, featuring an inner coating that curbs protein adhesion, leading to an 8% reduction in product loss during filling. The "Others" category, encompassing pouches and single-serve sachets favored by travelers and outdoor enthusiasts, struggles to scale up due to elevated per-unit packaging costs. The European Commission highlights that regulatory frameworks, like the EU's Packaging and Packaging Waste Directive, mandate a 90% recycling collection rate for beverage containers by 2029, with a clear preference for aluminum and glass over multi-material laminates.

By Distribution Channel: Online Retail Disrupts Traditional Shelf Allocation

In 2025, supermarkets and hypermarkets held a 42.55% share of the distribution landscape, leveraging high foot traffic and impulse purchases. However, online retail stores are growing rapidly, with a 9.74% CAGR through 2031, the fastest among all channels. This trend highlights a generational shift: consumers under 35 discover protein drinks via Instagram influencers and purchase on Amazon or brand websites, while those over 45 prefer in-store browsing and retailer loyalty programs, according to Eurostat. Huel generated GBP 185 million (USD 235 million) in 2024, with 68% of its revenue coming from its website and subscription service, bypassing traditional retail. Subscription models secure repeat purchases, Huel's annual churn rate is 12%, compared to 40% for one-time buyers, and enable brands to use customer data for personalized marketing.

Specialty and health stores, such as GNC and Holland & Barrett, are losing share as consumers shift online but remain critical for trials. Notably, 58% of first-time protein drink buyers in Europe purchase in-store and reorder online if satisfied. Amazon's pan-European fulfillment network allows smaller brands like UFIT to offer next-day delivery across 15 countries without building warehouses, leveling the playing field. The "Other Distribution Channels" category, including gyms, vending machines, and convenience stores, accounts for 17.73% of volume. In 2024, PureGym partnered with Science in Sport to install vending machines with exclusive flavors at 300 UK locations, converting trials into habitual purchases. Regulatory factors minimally impact distribution, though the EU's Digital Services Act enforces transparency on online marketplaces, ensuring consistent health claims across e-commerce platforms, according to the European Commission.

Geography Analysis

In 2025, the United Kingdom secured a dominant 37.28% share of the market, capitalizing on its early embrace of high-protein diets, a well-established network of specialty stores, and a cultural inclination towards meal-replacement beverages. On average, British consumers shell out GBP 42 (USD 53) annually for protein drinks, twice the European norm. This heightened spending is largely attributed to a robust gym membership penetration, with 16.2% of the population enrolled in 2024, and endorsements from the National Health Service, which ties protein intake to healthy aging. Huel, a Hertfordshire-based company, stands as a testament to the UK's market leadership, raking in a notable GBP 185 million (USD 235 million) in 2024 and extending its reach to 18 European nations. Meanwhile, Germany is on a rapid ascent, boasting a 9.06% CAGR through 2031, the swiftest pace among major markets. This surge is bolstered by government-endorsed fitness initiatives, notably the "Bewegt GESUND bleiben" program, which offers gym membership subsidies to citizens over 60. Additionally, there's a cultural tilt towards functional foods, especially those with transparent ingredient lists. In a notable move, German giants Aldi and Lidl introduced private-label protein drinks in 2024, pricing them at EUR 1.80 per unit. By year's end, these drinks commanded a 11.92% volume share, challenging branded counterparts to rationalize their premium pricing.

France, Italy, and Spain together accounted for 27.84% of the market value in 2025, but their growth rates lagged behind Western Europe's. This is attributed to a lower penetration of gym memberships and a cultural inclination towards whole-food protein sources, such as yogurt and cheese. Addressing local hesitations towards synthetic ingredients, Danone's Alpro Sport, rolled out in March 2024, caters specifically to French tastes with its organic certification and reduced sweetness. In Spain and Italy, the demand for clear protein waters surged by 22% in 2024, spurred by the summer heat and a cultural preference against creamy textures.

The Netherlands, Belgium, and Sweden, together making up 11.06% of the market value in 2025, have carved out a significant niche, thanks to their affluent populations and forward-thinking wellness cultures. Notably, the Netherlands boasts the highest fitness center density in Europe, with one center for every 4,200 residents. Poland, home to 4.8 million gym members in 2024, is emerging as a new frontier. International chains like FitX and McFit are setting up budget-friendly facilities in secondary cities. However, the market faces challenges, as price sensitivity limits the reach of premium products.

Competitive Landscape

In the European protein sports drinks market, major players such as Glanbia, PepsiCo, and Nestlé dominate a significant portion of the revenue. However, the market remains fragmented below the top tier, with regional specialists defending niche segments through localized flavors, sponsorship of amateur sports clubs, and direct-to-consumer models that bypass traditional retail channels. Glanbia's Optimum Nutrition and Grenade brands lead the premium segment, leveraging clinical endorsements from professional athletes. Meanwhile, PepsiCo's Gatorade Protein and Muscle Milk target mainstream consumers with supermarket distribution and competitive pricing. Nestlé focuses on plant-based innovation, exemplified by its Garden Gourmet line, launched in May 2024, which uses fava-bean protein to appeal to environmentally conscious consumers in Germany and the Netherlands. Disruptors like Huel and UFIT are capturing younger demographics through Instagram-driven marketing and subscription models, achieving customer lifetime values three times higher than one-time buyers.

Emerging opportunities in the market include precision-fermentation proteins, which provide lactose-free whey alternatives, and protein-fortified coffees, which grew by 19% in 2024. Brands like Arla Foods have capitalized on this trend, introducing cold-brew coffee with 20 grams of protein. Technological advancements are also reshaping the competitive landscape. Enzymatic hydrolysis is enabling the production of clear protein waters, eliminating the chalky texture of traditional shakes. Additionally, aseptic-filling lines are reducing cold-chain costs by 25% through ambient storage, facilitating market expansion in Southern and Eastern Europe.

Regulatory frameworks, such as the European Food Safety Authority's health-claim substantiation requirements, favor established players with in-house clinical teams, raising barriers to entry for smaller brands. Patent filings highlight strategic priorities within the market. In 2024, Glanbia filed seven patents related to protein-stabilization techniques, while Danone filed five patents focused on blending plant proteins to achieve complete amino-acid profiles. These developments underscore the competitive dynamics and innovation driving the European protein sports drinks market.

Europe Protein Based Sports Drinks Industry Leaders

Glanbia PLC

PepsiCo Inc.

Abbott Laboratories

THG plc

Mondelez International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: Danone launched Alpro Sport, a plant-based protein drink combining pea and rice protein to deliver 20 grams of protein and a complete amino-acid profile, targeting flexitarian consumers in Germany, France, and the Netherlands. The product is certified organic and priced at EUR 2.80 per 330-milliliter bottle, positioning it as a premium alternative to whey-based drinks.

- February 2024: Glanbia introduced Grenade Energy RTD, a ready-to-drink protein shake combining 23 grams of whey isolate with 150 milligrams of caffeine, marketed as a breakfast replacement and pre-workout fuel for office workers and commuters. The product launched in the UK, Ireland, and Germany, with distribution through supermarkets and online channels.

- May 2024: Nestlé expanded its Garden Gourmet line with protein drinks using fava-bean protein, which generates 30% lower carbon emissions than soy. The launch targeted environmentally conscious consumers in Germany and the Netherlands, with retail availability through Albert Heijn and Edeka supermarkets.

Europe Protein Based Sports Drinks Market Report Scope

Metal Can, PET Bottles are covered as segments by Packaging Type. Convenience Stores, Online Retail, Specialty Stores, Supermarket/Hypermarket, Others are covered as segments by Sub Distribution Channel. Belgium, France, Germany, Italy, Netherlands, Russia, Spain, Turkey, United Kingdom are covered as segments by Country.| Ready-to-Drink Shakes |

| Protein Water |

| Protein Isotonic Blends |

| Others |

| Animal Source |

| Plant Source |

| Bottles and Tetra Packs |

| Cans |

| Aseptic Cartons |

| Others |

| Supermarkets/Hypermarkets |

| Specialty and Health Stores |

| Online Retail Stores |

| Other Distribution Channels |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| Soft Drink Type | Ready-to-Drink Shakes |

| Protein Water | |

| Protein Isotonic Blends | |

| Others | |

| Source | Animal Source |

| Plant Source | |

| Packaging Format | Bottles and Tetra Packs |

| Cans | |

| Aseptic Cartons | |

| Others | |

| Distribution Channel | Supermarkets/Hypermarkets |

| Specialty and Health Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Market Definition

- Carbonated Soft Drinks (CSDs) - Carbonated soft drinks (CSDs) refer to non-alcoholic beverages that are carbonated and typically flavored, containing dissolved carbon dioxide to create effervescence. These beverages commonly include cola, lemon-lime, orange, and various fruit-flavored sodas. Marketed in cans, bottles, or fountain dispense.

- Juices - We have considered packaged juices which encompass non-alcoholic beverages derived from fruits, vegetables, or a combination thereof, processed and sealed in various packaging formats such as bottles, cartons, or pouches. Excluding fresh juices, this market segment involves commercially prepared and preserved juices, often with added preservatives and flavors.

- Ready-to-Drink (RTD) Tea and RTD Coffee - Ready-to-Drink (RTD) tea and RTD coffee are pre-packaged, non-alcoholic beverages that are brewed and prepared for consumption without further dilution. RTD tea typically includes various tea varieties, infused with flavors and sweeteners, and comes in bottles, cans, or cartons. Similarly, RTD coffee involves pre-brewed coffee formulations, often mixed with milk, sugar, or flavorings, and is conveniently packaged for on-the-go consumption.

- Energy Drinks - Energy drinks are non-alcoholic beverages formulated to provide a quick boost of energy and alertness. Whereas, sports drinks are beverages designed to hydrate and replenish electrolytes, particularly after physical exertion, exercise, or intense activity

| Keyword | Definition |

|---|---|

| Carbonated Soft Drinks | Carbonated soft drinks (CSDs) are a combination of carbonated water and flavouring, sweetened by sugar or a non-sugar sweeteners. |

| Standard Cola | Standard Cola is defined as the original flavor of cola soda. |

| Diet Cola | A cola-based soft drink containing no or low amounts of sugar |

| Fruit Flavored Carbonates | A carbonated beverage prepared from fruit juice/fruit flavor with carbonated water and containing sugar, dextrose, invert sugar or liquid glucose either singly or in combination. It may contain peel oil and fruit essences. |

| Juice | Juice is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| 100% Juice | Fruit/vegetable juice made from fruit in the form of its juice with no water added to make up the volume. It is not permitted to add sugars, sweeteners, preservatives, flavourings or colourings to fruit juice. |

| Juice Drinks (up to 24% Juice) | Fruit/vegetable juice drinks with up to 24% fruits/vegetable extract. |

| Nectars (25-99% Juice) | Juices that can have between 25 and 99% of fruit, with the minimum legal limits defined depending on the type of fruit |

| Juice concentrates | Juice Concentrates are those form of juices when most of this liquid is removed resulting in a thick, syrupy product known as juice concentrate. |

| RTD Coffee | Packaged coffee beverages that are sold in a prepared form and are ready for consumption at the time of purchase. |

| Iced Coffee | An iced coffee is a cold version of coffee, usually a combination of hot espresso and milk with ice added to it. |

| Cold Brew Coffee | Cold brew also called cold water extraction or cold pressing is made by steeping ground coffee in room-temperature water for several hours. |

| RTD Tea | Ready-to-drink (RTD) tea is a packaged tea product ready for immediate consumption without brewing or preparation |

| Iced Tea | Ice tea or iced tea is a drink made from tea without milk but with sugar and sometimes fruit flavourings, drunk cold. |

| Green Tea | Green tea is a tea beverage which promotes mental alertness, relieving digestive symptoms and promoting weight loss. |

| Herbal Tea | Herbal tea beverages are made from the infusion or decoction of herbs, spices, or other plant material in hot water. |

| Energy Drink | A type of drink containing stimulant compounds, usually caffeine, which is marketed as providing mental and physical stimulation. They may or may not be carbonated and may also contain sugar, other sweeteners, or herbal extracts, among numerous possible ingredients. |

| Sugar-free or Low-calories Energy Drinks | Sugar-free or Low-calories Energy Drinks are sugar-free, artificially sweetened energy drinks with few or no calories. |

| Traditional Energy Drink | Traditional Energy Drinks are functional soft drinks containing ingredients designed to boost the consumer's energy. |

| Natural/Oraganic Energy Drinks | Natural/Organic energy drinks are energy drinks free of artificial sweeteners and synthetic colorings. Instead, they contain naturally derived ingredients such as green tea, yerba mate, and botanical extracts. |

| Energy Shots | A small but highly concentrated energy drink that contains large amounts of caffeine and/or other stimulants. The quantity is comparatively smaller compared to energy drinks. |

| Sports Drink | Sports drinks are beverages designed specifically for the rapid supply of fluid, carbohydrates, and electrolytes before, during or after exercise. |

| Isotonic | Isotonic drinks contain similar concentrations of salt and sugar as in the human body, and are designed to quickly replace fluids lost during exercise but with an increase of carbohydrate. |

| Hypertonic | Hypertonic drinks have a higher concentration of salt and sugar than the human body. They are best drunk after exercise as it is important to replace glycogen levels quickly after exercise. |

| Hypotonic | Hypotonic drinks are designed to quickly replace fluids lost during exercise. They have very low carbohydrate content and a lower concentration of salt and sugar than the human body. |

| Electrolyte-Enhanced Water | Electrolyte water is water infused with electrically-charged minerals, such as sodium, potassium, calcium, and magnesium. |

| Protein-based Sport Drinks | Protein-based sports drinks are those sports drinks which has added protein in it that will improve performance and reduce muscle protein breakdown. |

| On-Trade | The on-trade refers to places that sell beverages for immediate consumption on the premises like bars, restaurants, and pubs |

| Off-Trade | Off-trade usually means places like liquor stores, supermarkets and other places where you don't consume the beverage right away. |

| Convenience Store | A retail business that provides the public with a convenient location to quickly purchase a wide variety of consumable products and services, generally food and gasoline. |

| Specialty store | A specialty store is a shop/store that carries a deep assortment of brands, styles, or models within a relatively narrow category of goods |

| Online Retail | Online retail is a type of eCommerce whereby a business sells goods or services directly to consumers from a website. |

| Aseptic Packaging | Aseptic packaging refers to the filling of a cold, commercially sterile product under sterile conditions into a presterilized container and closure under sterile conditions to form a seal that effectively excludes microorganisms. These includes tetra packs, cartons, pouches etc. |

| PET Bottle | PET bottle means a bottle made of polyethylene terephthalate. |

| Metal Cans | Metal containers made of aluminum or tin- plated or zinc-plated steel, which are commonly used for packaging food, beverages or other products. |

| Disposable Cups | Disposable Cup means a cup or other container designed for single use to serve beverages, such as water, cold drinks, hot drinks and alcoholic beverages. |

| Gen Z | A way of referring to the group of people who were born in the late 1990s and early 2000s. |

| Millenial | Anyone born between 1981 and 1996 (ages 23 to 38 in 2019) is considered a Millennial |

| Taurine | Taurine is an amino acid that supports immune health and nervous system function. |

| Bars & Pubs | It is a drinking establishment licensed to serve alcoholic drinks for consumption on the premises. |

| Café | It is a foodservice establishment serving refreshments (mainly coffee) and light meals. |

| On the go | It means doing / dealing with while busily engaged with something and not diverting plans in order to accommodate. |

| Internet Penetration | The Internet Penetration Rate corresponds to the percentage of the total population of a given country or region that uses the Internet. |

| Vending Machine | A machine that dispenses small articles such as food, drinks, or cigarettes when a coin or token is inserted |

| Discount store | A discount store or discounter offers a retail format in which products are sold at prices that are in principle lower than an actual or supposed "full retail price". Discounters rely on bulk purchasing and efficient distribution to keep down costs. |

| Clean Label | Clean label on the beverage market are drinks that are made from few ingredients of natural origin and are not or only slightly processed. |

| Caffeine | An alkaloid compound which is a stimulant of the central nervous system. It is mainly used recreationally, as a mild cognitive enhancer to increase alertness and attentional performance. |

| Extreme sport | Action sports, adventure sports or extreme sports are activities perceived as involving a high degree of risk. |

| High-intensity interval training | It incorporates several rounds that alternate between several minutes of high intensity movements to significantly increase the heart rate to at least 80% of one's maximum heart rate, followed by short periods of lower intensity movements. |

| Shelf life | The length of time for which an item remains usable, fit for consumption, or saleable. |

| Cream Soda | Cream soda is a sweet soft drink. Generally flavored with vanilla and based on the taste of an ice cream float |

| Root Beer | Root beer is a sweet North American soft drink traditionally made using the root bark of the sassafras tree Sassafras albidum or the vine of Smilax ornata as the primary flavor. Root beer is typically, but not exclusively, non-alcoholic, caffeine-free, sweet, and carbonated. |

| Vanilla Soda | A carbonated soft drink flavoured with vanilla. |

| Dairy-Free | A product that does not contain any milk or milk products from cows, sheep or goats. |

| Caffeine-Free Energy Drinks | Caffeine-free energy drinks rely on other ingredients to boost the energy. Popular choices include amino acids, B vitamins, and electrolytes. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated reports, custom consulting assignments, databases & subscription platforms