Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

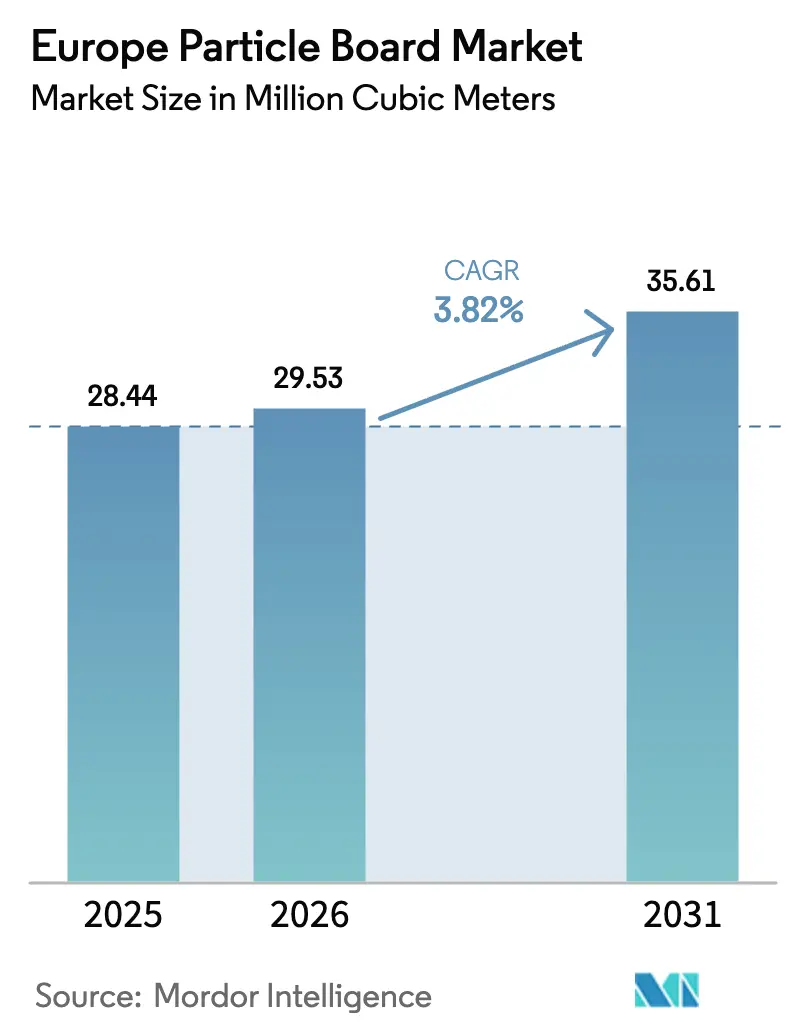

| Base Year Market Size (2025) | 28.44 Million cubic meters |

| Market Volume (2026) | 29.53 Million cubic meters |

| Market Volume (2031) | 35.61 Million cubic meters |

| Growth Rate (2026 - 2031) | 3.82% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Particle Board Market Analysis by Mordor Intelligence

The Europe Particle Board Market size is projected to expand from 28.44 million cubic meters in 2025 and 29.53 million cubic meters in 2026 to 35.61 million cubic meters by 2031, registering a CAGR of 3.82% between 2026 to 2031. Mandatory low-VOC (Volatile Organic Compound) rules, recycled-wood mandates, and carbon-pricing of urea adhesives are redefining cost structures, prompting vertically integrated leaders to accelerate recycling hubs and bio-based binder pilots. Germany anchors demand with serial timber-housing programs, while Nordic mills leverage forest ownership and combined-heat-and-power plants to cushion feedstock and energy risk. AI-optimized press lines from Siempelkamp and Dieffenbacher deliver double-digit efficiency gains, but mills lacking EUR 10-15 million automation budgets face widening operating-cost gaps. Tight sawdust supply, exacerbated by pellet-mill demand and CLT (Cross-Laminated Timber) off-cut diversion, continues to lift Austria’s spot price above EUR 120/ton, spurring experiments with agricultural residues as substitute fibers.

Key Report Takeaways

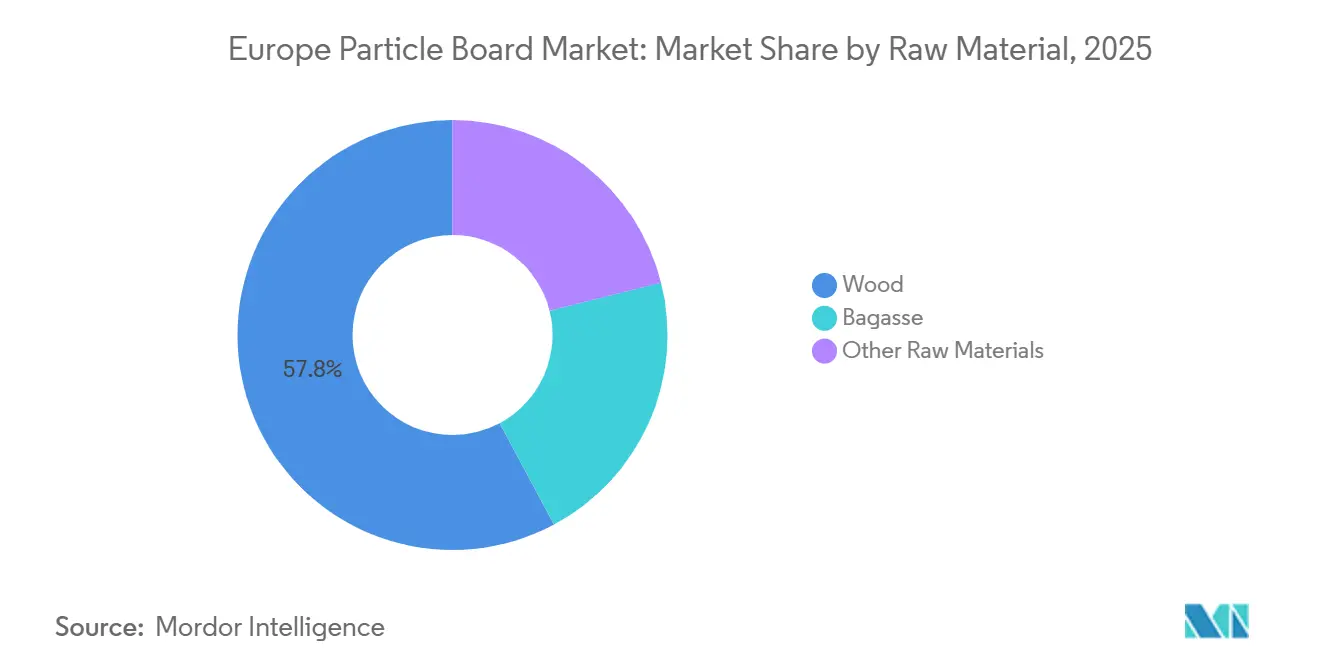

- By raw material, wood commanded 57.83% of the Europe Particle Board market share in 2025, while bagasse is expanding at a 4.23% CAGR during the forecast period (2026-2031).

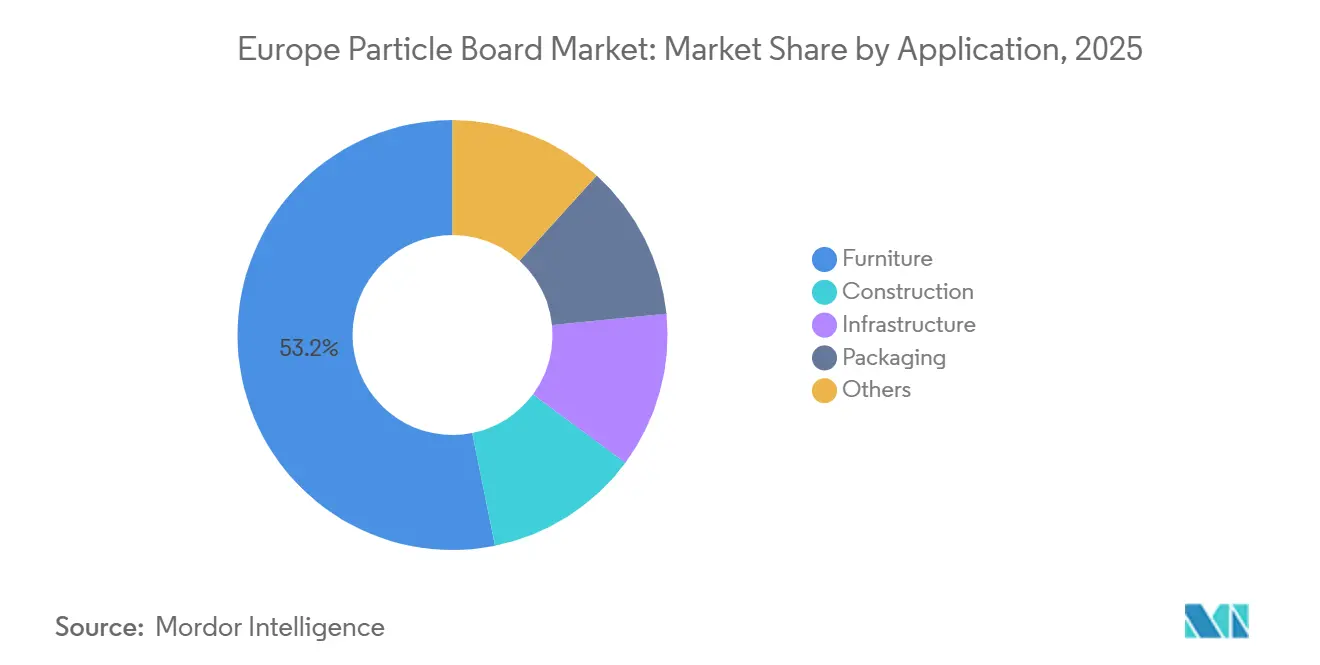

- By application, furniture captured 53.16% of the volume in 2025 and is forecasted to advance at a 4.46% CAGR during the forecast period (2026-2031).

- By country, Germany held 48.92% of the Europe Particle Board market size in 2025 and is growing at a 4.51% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Particle Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening EU formaldehyde limits | +0.9% | EU27, UK (early in Germany, Austria, Nordics) | Medium term (2-4 years) |

| Recycled-wood capacity expansions | +0.7% | Germany, Austria, Poland, Iberia | Medium term (2-4 years) |

| Prefabricated timber housing uptake | +1.1% | Netherlands, Germany, Austria, Nordics | Long term (≥ 4 years) |

| EU CBAM credits for low-carbon panels | +0.5% | EU27 (strongest in Germany, France, Benelux) | Short term (≤ 2 years) |

| AI-optimized press lines | +0.6% | Germany, Austria, Italy, Spain (large integrated producers) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening EU Formaldehyde Limits Driving Ultra-Low-VOC Boards

EU Regulation 2023/1464 fixes a 0.062 mg/m³ ceiling for emissions from wood-based panels effective August 6, 2026, compelling adhesive reformulations or market exit[1]European Chemicals Agency, “Questions & Answers on Formaldehyde Limits,” echa.europa.eu. Germany adopted DIN EN 16516 back in 2020, giving domestic mills a six-year validation lead time, whereas many Southern and Eastern counterparts now rush to install test chambers and attain EN 717-1 certification. ECHA (European Chemicals Agency) guidelines published in May 2025 mandate chamber testing over supplier declarations, adding EUR 50,000-80,000 to SME (Small and Medium Enterprises) compliance per product line. Lignin-modified resins piloted at Metsä Fibre’s Äänekoski demo plant remain 15-20% costlier than urea-formaldehyde, yet the promise of formaldehyde-free boards continues to attract R&D (research and development) budgets.

Capacity Expansions Using Recycled-Wood Feedstock

Sonae Arauco valorised 809,000 tons of recycled wood in 2024, achieving 33% incorporation, and targets 75% in selected mills by end-2025[2]Sonae Arauco, “Sustainability Report 2024,” sonaarauco.com. EGGER’s EUR 200 million Markt Bibart hub, supplied by Timberpak’s urban-collection network, started recycling operations in summer 2025, while Kronospan Luxembourg produced the first 100% recycled-wood board in June 2024. Municipal tenders for demolition wood across Germany and Austria intensify competition; mills without contracts risk shortages as beetle damage and drought curb virgin spruce supply.

Prefabricated Timber Housing and Off-Site Construction Uptake

The Netherlands recorded a 21.2% prefab housing share in 2025, with output expected to expand to near 16,100 units in 2026. Germany’s Nokera plant targets 30,000 units annually, Gropyus invested EUR 300 million in Richen, and Binderholz’s b-solution line adds 130,000 m² of modules a year. Off-site plants specify thinner, CNC (Computer Numerical Control)-friendly boards produced under tighter tolerances, challenging mills operating legacy presses.

EU CBAM Credits Favouring Low-Embodied-Carbon Panels

The Carbon Border Adjustment Mechanism, active January 1, 2026, adds EUR 40-60 per ton surcharges on imported urea, lifting adhesive cost 10-12% for panel makers tied to non-EU supply. Vertically integrated resin producers can badge “CBAM-neutral” panels for public projects that require full life-cycle accounting per EN 15804+A2 and Germany’s QNG (Qualitätssiegel Nachhaltiges Gebäude/Quality Seal for Sustainable Buildings) scheme. Kronospan’s Luxembourg site runs three CHP plants that offset Scope 2 emissions and earn carbon credits, lowering its CBAM (Carbon Border Adjustment Mechanism) burden.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-price volatility squeezing margins | -0.6% | Germany, Italy, Spain, Poland (high gas dependence) | Short term (≤ 2 years) |

| CLT/LVL residue diversion from particleboard | -0.5% | Austria, Germany, Sweden, Finland (CLT hubs) | Medium term (2-4 years) |

| Mandatory EPD disclosure boosting SME costs | -0.3% | EU27, UK (highest pressure on Southern and Eastern SMEs) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Energy-Price Volatility Squeezing Press-Line Margins

German pellet prices climbed 19% month-on-month to EUR 363.21 t in February 2025, raising press energy cost on boards that already consume 150-200 kWh/m³. Energy now accounts for up to 18% of production cost, trimming EBITDA by two to three points for mills unable to hedge contracts.

CLT/LVL Demand Diverting Wood Residues

CLT factories in Austria and Germany increasingly pelletise their off-cuts, paying premiums that pull sawdust away from board mills; Austria’s index hit 409 (base 2001 = 100) in March 2025. Stora Enso’s Oulu board line secures 1 million m³ of chips via the Junnikkala sawmill acquisition, signalling vertical-integration moves to safeguard residue supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Recycled Wood Reshapes Feedstock Economics

Wood-based feedstock retained 57.83% of volume in 2025, but the Europe Particle Board market is pivoting toward recycled streams. Sonae Arauco’s 33% recycled share in 2024 and EGGER’s Markt Bibart hub demonstrate scaling momentum. Bagasse occupies a niche yet is forecast at 4.23% CAGR during the forecast period (2026-2031), as Mediterranean mills trial sugarcane residue blends at press temperatures below 150°C. Brewer’s spent grain volumes near 6.4 million tons/year offer further optionality, although high moisture and logistics hurdles persist. Virgin spruce scarcity, exacerbated by bark-beetle outbreaks, keeps Austria’s sawdust above EUR 120 per ton, underpinning recycled-wood premiums.

Producers capturing post-consumer wood streams gain hedge value as Europe Particle Board market size expansion tightens residue supply. Fraunhofer IAP’s ReSpan project proved binder-free, 100% waste-wood boards feasible, hinting at a future in which mills decouple from virgin fiber and urea entirely. Operators that secure municipal demolition-wood tenders or commercialize agri-fiber recipes will lock in a margin advantage as circular-economy quotas tighten.

By Application: Furniture Dominance Meets Construction Disruption

Furniture retained a 53.16% share in 2025 and is set for a 4.46% CAGR during the forecast period (2026-2031) as IKEA shifts fully to FSC-certified, low-formaldehyde boards and direct-to-consumer brands demand transparent chains. Construction ranks second and benefits from prefab mandates; German megafactories add over 400,000 m² of annual modular capacity. These plants require thinner, CNC-ready grades, steering Europe Particle Board market innovation toward tighter tolerance and lower-density panels.

Infrastructure and packaging remain smaller outlets, but e-commerce parcel growth supports lightweight board demand for ready-to-assemble shelving. Producers that toggle presses between EN 312 furniture and EN 13986 construction specs with rapid changeovers will win bundled contracts as buyers shrink supplier rosters.

Geography Analysis

Germany’s 48.92% volume share in 2025 and 4.51% CAGR during the forecast period (2026-2031) underscore regulatory foresight and integrated capacity. DIN EN 16516 early adoption accelerates low-VOC rollouts, while QNG and DGNB (Deutsche Gesellschaft für Nachhaltiges Bauen/German Sustainable Building Council) frameworks embed life-cycle criteria into public procurement. EGGER’s Markt Bibart, Sonae Arauco’s Beeskow line, and elka-Holzwerke upgrades cluster near prefab hubs, minimizing logistics, which can consume 30% of project budgets.

West Fraser’s South Molton closure in 2023 trimmed United Kingdom capacity, but Scottish mills pivot to niche decorative grades. France’s RE2020 regulation pushes domestic sourcing, while Italy and Spain ride furniture export momentum. Nordic mills marry forest ownership with biomass energy; Stora Enso harvested 10.5 million m³ from its own and contracted forests in 2024, insulating Finnish and Swedish plants from residue price spikes.

Austria’s six mills lifted utilization in 2025 on strong softwood flows, yet pellet-mill competition forced temporary sawdust purchase halts. Eastern European SMEs risk market loss without EPDs; consolidation is accelerating as Western groups acquire mills to meet Digital Product Passport compliance before 2026.

Competitive Landscape

The Europe Particle Board market is moderately consolidated. EGGER, Kronospan, Swiss Krono, Sonae Arauco, and Pfleiderer strengthen positions through recycling networks, CHP plants, and in-house resin. Laggards are SMEs unable to fund EUR 50,000-80,000 EPDs or EUR 10-15 million smart-press retrofits; visible casualties include Xilopan’s 2025 shutdown in Italy. Opportunities emerge in agricultural-residue blends and ultra-thin boards for prefab interiors, niches best served by mills willing to re-engineer furnish recipes.

Europe Particle Board Industry Leaders

EGGER

Kronoplus Limited

Sonae Arauco

Pfleiderer

SWISS KRONO Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: In the Lyudinovsky district of Russia's Kaluga Special Economic Zone, Ultradecor inaugurated a new DSP particleboard plant. This facility boasts an annual production capacity of 900,000 m³ of particleboard and 72 million m² of laminated products.

- March 2025: Xilopan, an Italian manufacturer of particleboard, halted production, citing uncompetitiveness in today's economic landscape. Established in 1969 and situated in the Po Valley near Milan, Xilopan specializes in chipboard panel products, producing both raw and melamine-faced panels, primarily from poplar.

Europe Particle Board Market Report Scope

Particle board, commonly known as chipboard or low-density fiberboard, is an engineered wood product that is pressed and extruded from wood chips and synthetic resin or other suitable binders. Particle board is less expensive, denser, and more uniform than traditional wood and plywood.

The Europe Particle Board market is segmented by raw material, application, and geography. By raw material, the market is segmented into wood, bagasse, and other raw materials. By applications, the market is segmented into construction, furniture, infrastructure, packaging, and other applications. The report covers the market size and forecast for the European particle board market in 6 countries across the European region. For each segment, the market sizing and forecasts have been provided based on volume (cubic meters).

By Raw Material

| Wood |

| Bagasse |

| Other Raw Materials |

By Application

| Furniture |

| Construction |

| Infrastructure |

| Packaging |

| Others |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| NORDIC Countries |

| Rest of Europe |

| By Raw Material | Wood |

| Bagasse | |

| Other Raw Materials | |

| By Application | Furniture |

| Construction | |

| Infrastructure | |

| Packaging | |

| Others | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe |

Key Questions Answered in the Report

How large will Europe’s particleboard consumption be by 2031?

Demand is forecast to reach 35.61 million cubic meters by 2031, growing at a 3.82% CAGR from 2026 to 2031.

Which end-use sector drives the most volume?

Furniture holds 53.16% of 2025 volume and is set to expand at a 4.46% CAGR through 2031, keeping it the dominant outlet.

Why are German mills outperforming the region?

Early compliance with DIN EN 16516, aggressive prefab housing programs, and large-scale recycling investments give German plants both regulatory and cost advantages.

How is recycled wood changing feedstock strategy?

Integrated producers already exceed 30% recycled content and aim for 75%, securing urban demolition wood to hedge against scarce and expensive virgin residues.

What technology shift is most impactful for cost control?

AI-driven press-control suites from Siempelkamp and Dieffenbacher cut energy use by up to 15% and lift throughput without new presses, offering rapid payback amid volatile power prices.

Page last updated on: