Market Overview

| Study Period | 2020 - 2031 |

|---|---|

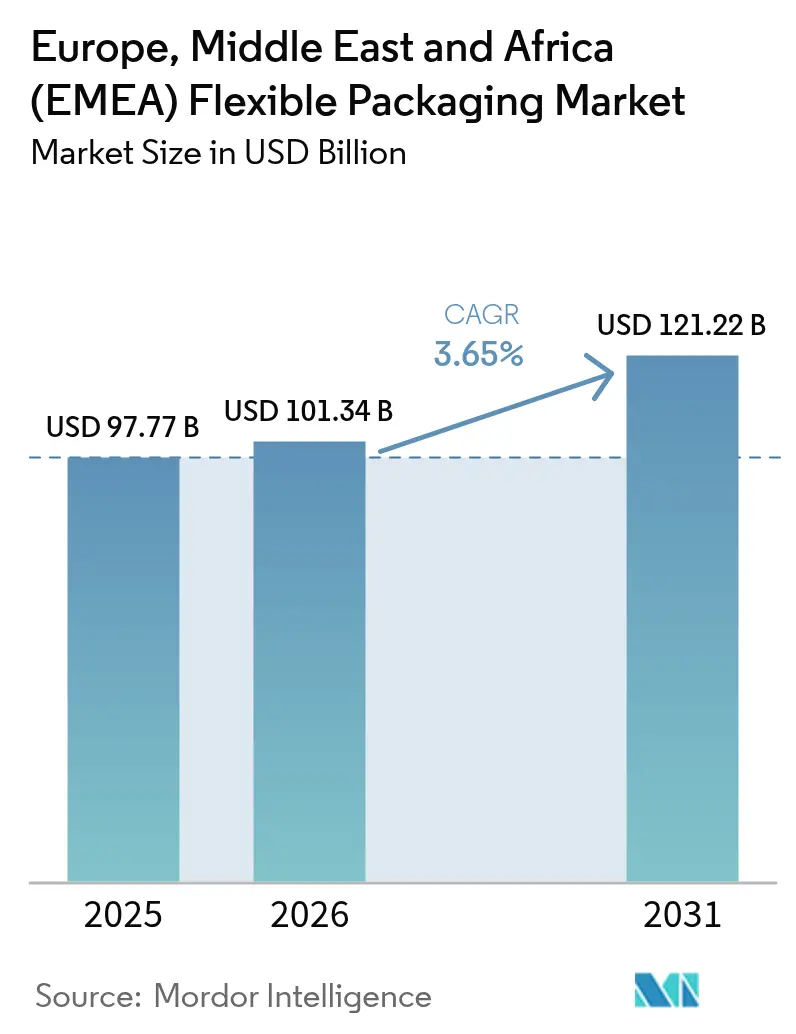

| Base Year Market Size (2025) | USD 97.77 Billion |

| Market Size (2026) | USD 101.34 Billion |

| Market Size (2031) | USD 121.22 Billion |

| Growth Rate (2026 - 2031) | 3.65% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe, Middle East And Africa (EMEA) Flexible Packaging Market Analysis by Mordor Intelligence

The Europe, Middle East And Africa (EMEA) flexible packaging market size in 2026 is estimated at USD 101.34 billion, growing from 2025 value of USD 97.77 billion with 2031 projections showing USD 121.22 billion, growing at 3.65% CAGR over 2026-2031. A mix of regulatory mandates, shifts in consumer lifestyles and technology‐enabled customization is steering this steady advance. Europe’s 83.48% revenue share in 2024 gives the region unrivalled scale, yet new capacity and policy support in the Middle East and Africa (MEA) make those sub-regions the fastest-growing at 4.87% CAGR to 2030. Material substitution is accelerating: plastics still accounted for 68.12% share in 2024 but bioplastics and compostables are tracking a 5.11% CAGR as converters pursue circularity targets. Meanwhile, volatile resin prices, margin pressure and the need for technology upgrades are spurring high-profile deals such as the Amcor–Berry integration and Constantia Flexibles’ sale to One Rock Capital Partners, signalling a pivot toward scale efficiencies and digital print competencies.

Key Report Takeaways

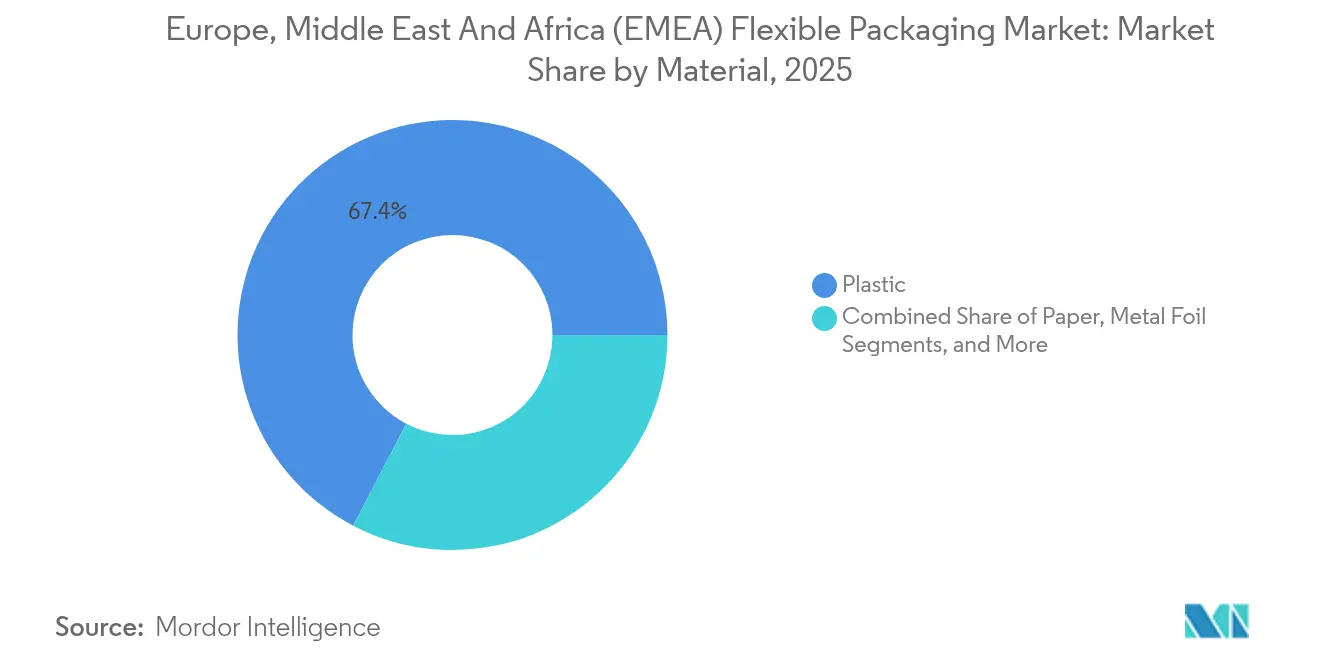

- By material, plastics commanded 67.35% of the EMEA flexible packaging market size in 2025, while bioplastics and compostable substrates are projected to rise at a 4.88% CAGR through 2031.

- By product type, bags and pouches led with 47.05% share of the EMEA flexible packaging market size in 2025, while sachets and stick packs are positioned for a 4.43% CAGR through 2031.

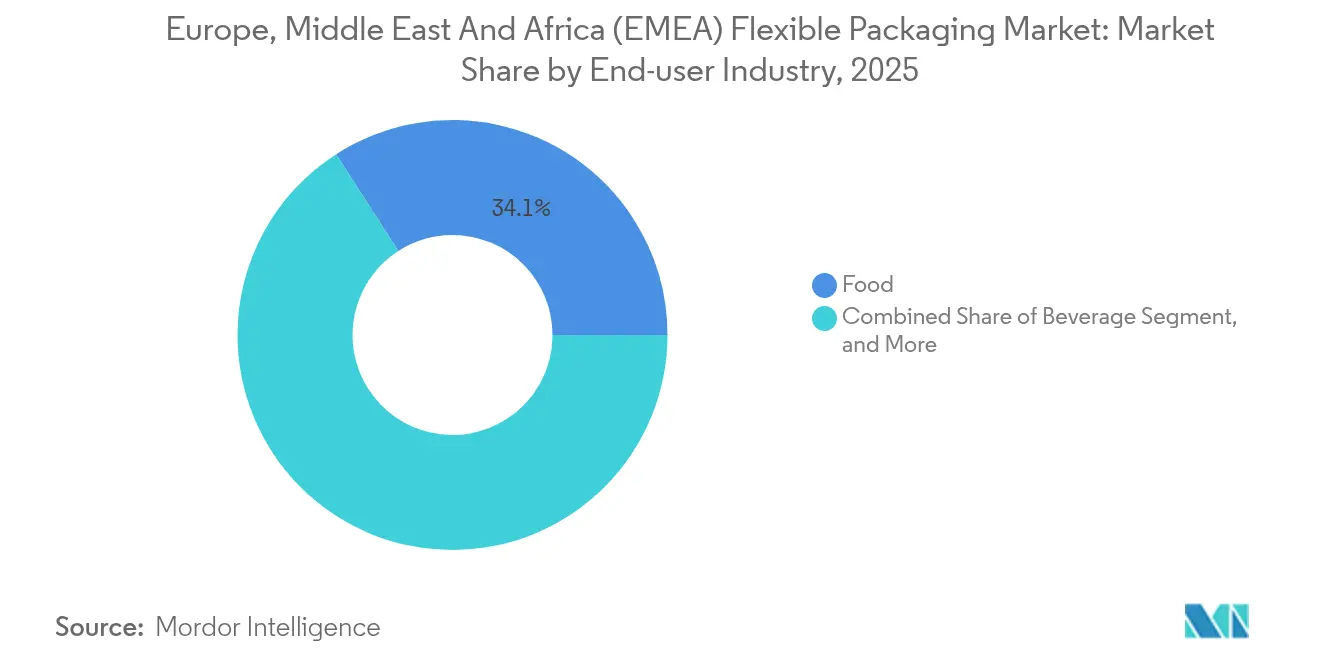

- By end-user industry, food applications claimed 34.10% revenue share in 2025; personal care and cosmetics is set to climb at a 4.65% CAGR to 2031.

- By printing technology, flexography dominated with 45.20% of the EMEA flexible packaging market share in 2025, yet digital printing is pacing ahead at a 4.79% CAGR to 2031.

- By geography, Europe held 82.95% of the EMEA flexible packaging market share in 2025, whereas the Middle East and Africa recorded the fastest CAGR at 4.63% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe, Middle East And Africa (EMEA) Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Processed and convenience food demand | +0.8% | Europe, Middle-East urban centers | Medium term (2-4 years) |

| Regulatory push for recyclable formats | +1.2% | Europe-led, MEA follow-through | Long term (≥ 4 years) |

| Lightweighting for logistics savings | +0.5% | Europe, global supply chains | Short term (≤ 2 years) |

| Rapid e-commerce expansion | +0.7% | Europe, GCC cities, emerging Africa | Medium term (2-4 years) |

| Pharma cold-chain growth | +0.4% | Europe, Gulf states | Long term (≥ 4 years) |

| Digital print for low-MOQ SKUs | +0.3% | Europe core, Middle-East uptake | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Steady Rise in Demand for Processed and Convenience Foods

Urban migration is reshaping meal habits, prompting retailers and foodservice operators to favor lightweight, shelf-stable packs that protect freshness during extended distribution cycles. Cost-effective bags and pouches displace rigid alternatives, lowering freight bills and CO₂ footprints. Converters introduce grab-and-go designs such as ProAmpac’s RotiBag, a leak-resistant format able to carry hot foods without outer cartons. [1]Brett Parker, “ProAmpac’s Rotibag Provides Sustainable Solution for Grab-and-Go Food,” packagingstrategies.com Combined with HACCP and ISO 22000 compliance, these performance upgrades increase baseline volume for film substrates and zipper closures across the EMEA flexible packaging market.

Regulatory Push for Recyclable and Sustainable Packaging

The EU Packaging and Packaging Waste Regulation 2025/40 enforces 65% recyclable content by 2030 and bans PFAS barrier chemistries, triggering broad redesign of legacy multi-layer laminates. R&D centers now prioritize mono-PE or mono-PP structures with compatibilizers that preserve oxygen and moisture barrier while allowing mechanical recovery. BASF’s compostable coatings and Südpack’s chemically recycled polyamide layers show how innovation is aligning with PPWR milestones. Brand owners standardize global SKUs around EU-level compliance, giving bioplastic suppliers and fiber-based converters new share-gain avenues in the EMEA flexible packaging market.

Lightweighting for Logistics-Cost Reduction

Carbon taxes and fuel surcharges amplify the benefits of thinner gauges and downgauged barrier webs. Innovations such as Coveris’ MonoFlex BP trays cut material use by nearly 30% versus traditional mixed-material formats without sacrificing puncture strength. Gauge-reduction initiatives cascade across frozen food, pet-food and detergent refills, helping brand owners shave transport emissions and warehouse space. E-commerce operators reward compact dimensions through lower dimensional weight fees, extending the driver’s reach into corrugated-replacement films and shrink bundles.

Rapid E-commerce Growth Across EMEA

Online retail volumes escalated in 2024-2025, prompting fulfillment centers to standardize flexible mailers, cushioning films and tamper-evident strip pouches compatible with automated sortation lines. Amazon’s robotics roll-outs in European hubs influenced converters to design tear-resistant LDPE mailers with easy-open perforations and bold graphics printed digitally for seasonal promotions. In Gulf markets, ambient temperatures above 45 °C necessitate barrier upgrades against odor ingress and seal failures, driving demand for high-performing laminated sachets ready for last-mile courier networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Polymer resin price volatility | −0.9% | Europe, global supply networks | Short term (≤ 2 years) |

| Margin squeeze from competition | −0.6% | Europe, mature GCC markets | Medium term (2-4 years) |

| Limited film-recycling infrastructure | −0.3% | Middle East and Africa | Long term (≥ 4 years) |

| PFAS and mineral-oil migration rules | −0.4% | Europe, global compliance | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Polymer Resin Prices

Crude-oil swings and Europe’s higher energy tariff structure distort input costs for PE and PP grades, forcing converters to renegotiate customer contracts every quarter. Integrated players hedge exposure through multi-year feedstock deals, but small and mid-scale firms face margin erosion that curtails CapEx on new presses and rewinders. The net effect tempers replacement cycles and slows innovation adoption in price-sensitive portions of the EMEA flexible packaging market.

Intensifying Competitive Landscape Squeezing Margins

Wave after wave of M&A is building super-regional champions with deeper purchasing leverage and broader technology portfolios. Independent converters reply by specializing in short-run jobs and investing in colour-accurate digital print lines, yet customer procurement teams pit suppliers against one another, hammering profit spreads on commodity bread bags and frozen-veg pouches. While volumes keep expanding, EBITDA compression restricts R&D budgets, delaying next-generation recyclable structures across much of the EMEA flexible packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Bioplastics Drive Sustainability Transition

Plastics retained 67.35% of the EMEA flexible packaging market share in 2025, anchored by cost advantages, high mechanical strength and well-established supply chains. Yet bioplastics and compostables are gaining ground-advancing at 4.88% CAGR-because regulatory stringency and brand commitments lean toward renewable content. EU-funded pilots, such as AIMPLAS’ PHA-from-waste initiative, illustrate institutional support that de-risks scale-up. Converters now run parallel extrusion lines for seaweed, PHA or PLA films alongside traditional LDPE, a dual-track approach that hedges compliance risks while servicing early-adopter brands. The EMEA flexible packaging market size for bio-based substrates is set to breach the USD 5.28 billion mark by 2031, a material share jump underpinned by supply-chain co-location and rising consumer visibility of compostability logos.

To prevent performance compromises, hybrid laminates blend chemically recycled PP with virgin-free PET tie layers, hitting both recycled-content quotas and downgauge objectives. Such innovations are timely because the PPWR places the onus on converters to prove recyclability through EU-accepted protocols-a compliance ceiling that plastics incumbents must clear or surrender share to emerging cellulosic webs.

By Product Type: Sachets Capture Portion Control Demand

Bags and pouches still dominated 47.05% of the EMEA flexible packaging market size in 2025, a position grounded in versatility from cereals to detergents. Yet sachets and stick packs are enjoying headline-grabbing momentum with a 4.43% CAGR through 2031, driven by single-serve coffee, electrolyte powders and dermatology creams. Personal-care multinationals deploy digitally printed sachets to trial scents or SPF formulas in subscription boxes, harnessing variable graphics to spark social media engagement. The format’s low‐material footprint slots neatly into convenience stores where shelf space commands a premium. Edible alginate sachets displayed at IFFA 2025 push the envelope further by erasing secondary waste streams altogether.

Consumer demand for precise dosing and on-the-go use aligns with national nutrition labeling schemes that discourage oversized servings. Consequently, the EMEA flexible packaging market is retooling form-fill-seal lines for faster lane counters, micro-perforation systems and hermetic edge seals that withstand courier networks. Sachet adoption also dovetails with cold-chain pharmaceutical requirements, where foil-barrier four-side seals protect hygroscopic APIs during regional transport.

By End-user Industry: Personal Care Drives Premium Growth

Food remained the backbone, capturing 34.10% share in 2025 due to volume sales of bakery, meat and snack staples. Nevertheless, personal care and cosmetics posted the strongest trajectory at 4.65% CAGR, reflecting premiumization and a consumer tilt toward planet-friendly packaging. Brands such as Beiersdorf integrate refill-ready stand-up pouches that meet ISO 22716 cosmetic GMP while cutting plastic tonnage, a move that enables storytelling around waste reduction in glossy ad campaigns. High-gloss varnishes, soft-touch films and metallic accents-once hallmarks of rigid jars-are now feasible on multilayer PE structures, widening the aesthetic vocabulary of the EMEA flexible packaging market.

Pharmaceutical and healthcare packs, though smaller in revenue, command superior margins because of regulatory validation and barrier precision. Here, foil/PET/PP tri-laminates persist despite recyclability headwinds because moisture ingress tolerances are unforgiving. Agricultural films, fertiliser sachets and horticulture pouches represent niche but resilient off-take, sustained by Africa’s blossoming greenhouse sector and EU Common Agricultural Policy subsidies for bio-mulch adoption.

By Printing Technology: Digital Printing Enables Customization

Flexography retained 45.20% of the EMEA flexible packaging market share in 2025, synonymous with long-run snack bags and detergent refill spouts. Yet digital presses are rewriting the economics of short runs, expanding at 4.79% CAGR. HP Indigo’s 2024 roll-outs enable surface-print on PE with food-safe inks, liberating order sizes to sub-1,000 units for targeted campaigns. Converters recalibrate production floors: hybrid lines combine digital for variable data and inline flexo for heavy ink coverage, maximising OEE.

Digital workflows also slash waste-no plates, minimal make-ready-and open richer data capture via serialized QR codes. The resulting transparency underpins anti-counterfeiting solutions prized by nutraceutical and cosmetic players. As the technology scales, cost parity with mid-length flexo jobs draws nearer, accelerating its penetration across the wider EMEA flexible packaging market.

Geography Analysis

Europe’s entrenched position stems from decades of innovation, stringent policy and a dense network of recyclers, film extruders and package designers. Germany’s engineering houses supply multilayer blown-film lines capable of processing chemically recycled feedstock, while France and Spain field consortiums trialling cellulose barrier papers. The bloc’s 82.95% grip on the EMEA flexible packaging market share in 2025 masks internal churn: energy-price volatility pushes converters to relocate energy-intensive lamination stages to lower-cost Poland or Turkey, trimming expense without exiting EU regulatory oversight.

The Middle East harnesses petrochemical feedstock proximity and sovereign investment vehicles to incubate mega-plants. Saudi Arabia’s USD 2 billion livestock city integrates downstream meat processing, enlarging demand for MAP trays and high-barrier thermoforms. UAE-based Hotpack’s USD 100 million U.S. site signals ambition to leverage GCC manufacturing know-how on the trans-Atlantic stage. Across the Gulf, high disposable incomes and e-commerce adoption accelerate adoption of print-rich pouches for premium confectionery, perfumery and halal-certified nutraceuticals.

Africa’s potential is vast though uneven. South Africa leads in collection and recycling, yet Nigeria and Kenya exhibit faster consumption growth thanks to urban influx, retail modernization and mobile money penetration that fuels e-commerce. Weak logistics and intermittent power in parts of sub-Saharan Africa compel converters to design packs tolerant to wide humidity and temperature swings. Multinational CPGs test refill sachet schemes in Nairobi and Lagos-programs that dovetail with community-level take-back initiatives supported by NGOs. Over the outlook window, the EMEA flexible packaging market is expected to allocate more working capital to in-continent extrusion, slashing lead times and mitigating FX swings.

Competitive Landscape

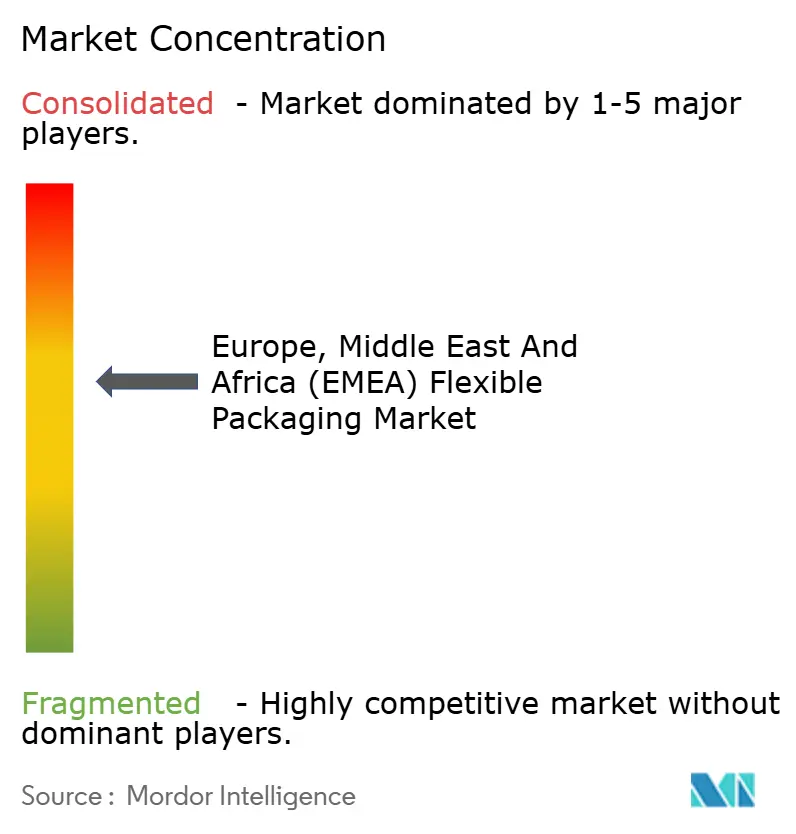

The EMEA flexible packaging market stands in a medium-consolidated posture: the top five groups control roughly 50% of regional turnover, giving the arena a concentration score of 6. High-profile transactions-Amcor closing its Berry healthcare unit acquisition and Constantia Flexibles joining One Rock-underline the scramble for scale synergies and R&D muscle. Consolidators chase a trifecta of goals: balanced geographic portfolios, material science pipelines and digital print competences.

Strategic themes are converging. First, sustainability differentiation-Amcor, Huhtamäki and Mondi race to commercialize recycle-ready mono-PE laminates tested for PPWR compliance. Second, vertical integration-polymer giants invest in chemical recycling and in-house label printing to secure feedstock certainty. Third, geographic reach-European incumbents acquire niche converters in Saudi Arabia or Egypt to gain tariff-free access and leverage low-cost energy. New-age entrants like B’ZEOS and AIMPLAS operate at the material frontier, licensing bio-based resins or coatings that incumbents may license or buy outright. Patent filings cluster around epoxy-free adhesive systems, silica-based barrier layers and in-line plasma treatments-all engineered to deliver PPWR-ready recyclability without sacrificing shelf life.

Price competition intensifies in bread bags, dry pasta and powdered milk, where buyer consolidation arms supermarket groups with stronger negotiating power. To combat commoditization, converters diversify into personal-care sample sachets, premium pet treats and medical device pouches that reward high print fidelity and tight dimensional tolerances. Digital print capacity becomes a bargaining chip: converters promise 10-day lead times and multichannel artwork management, swaying brand owners who run flash promotions on TikTok and Instagram.

Europe, Middle East And Africa (EMEA) Flexible Packaging Industry Leaders

Amcor plc

Constantia Flexibles Group GmbH

Mondi plc

Huhtamäki Oyj

ProAmpac Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Coveris released BarrierFresh board MAP trays that trim plastic by 90% and support 21-day protein shelf life.

- May 2025: Hotpack announced a USD 100 million U.S. manufacturing hub, marking its first North American investment.

- April 2025: Südpack, BASF and Werz unveiled chemically recycled meat packs using Ultramid Ccycled polyamide, meeting PPWR mandates.

- January 2025: ProAmpac introduced ProActive PCR flexible packs for food, cutting virgin resin use by 35%.

Europe, Middle East And Africa (EMEA) Flexible Packaging Market Report Scope

Flexible packaging is one of the most prominent packaging techniques used by major vendors across a diverse range of end-user verticals. This is due to its superior quality, such as its extended shelf life. Further, it is one of the most economical packaging methods to distribute and preserve food, beverage, pharmaceutical products, and other consumables.

The study analyzes the demand for the flexible packaging industry across Europe, Middle-East, and Africa, based on the following segments:

Resin Type - Polyethene (PE), Biaxially Oriented Polypropylene (BOPP), Cast Polypropylene (CPP), Polyvinyl Chloride (PVC), PET and Other Material Types (EVOH, EVA, PA)

Product Type - Pouches, Bags, Films, and other Product Types.

End-user industry - Food, Beverage, Healthcare and Pharmaceuticals, Cosmetics and Personal Care and Other End-User Verticals

By Material

| Plastics | Polyethylene (PE) |

| Biaxially Oriented Polypropylene (BOPP) | |

| Cast Polypropylene (CPP) | |

| Other Plastics | |

| Paper | |

| Metal Foil | |

| Bioplastics and Compostable Materials |

By Product Type

| Bags and Pouches |

| Films and Wraps |

| Sachets and Stick Packs |

| Other Product Types |

BY End-user Industry

| Food | Baked Goods |

| Snacks | |

| Meat, Poultry and Seafood | |

| Confectionery | |

| Pet Food | |

| Other Food Products | |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Agriculture and Horticulture | |

| Other End-Use Industries |

By Printing Technology

| Flexography |

| Rotogravure |

| Digital Printing |

| Other Printing Technologies |

By Geography

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Material | Plastics | Polyethylene (PE) | |

| Biaxially Oriented Polypropylene (BOPP) | |||

| Cast Polypropylene (CPP) | |||

| Other Plastics | |||

| Paper | |||

| Metal Foil | |||

| Bioplastics and Compostable Materials | |||

| By Product Type | Bags and Pouches | ||

| Films and Wraps | |||

| Sachets and Stick Packs | |||

| Other Product Types | |||

| BY End-user Industry | Food | Baked Goods | |

| Snacks | |||

| Meat, Poultry and Seafood | |||

| Confectionery | |||

| Pet Food | |||

| Other Food Products | |||

| Beverage | |||

| Healthcare and Pharmaceutical | |||

| Personal Care and Cosmetics | |||

| Agriculture and Horticulture | |||

| Other End-Use Industries | |||

| By Printing Technology | Flexography | ||

| Rotogravure | |||

| Digital Printing | |||

| Other Printing Technologies | |||

| By Geography | Europe | United Kingdom | |

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big will flexible packaging spending be across Europe, the Middle East and Africa by 2031?

Spending is projected to reach USD 121.22 billion by 2031, expanding from USD 97.77 billion in 2025.

Which material category is gaining share fastest in the EMEA flexible packaging space?

Bioplastics and compostables are the fastest-growing, progressing at a 4.88% CAGR through 2031 on the back of PPWR compliance.

What region is expanding quickest inside EMEA?

The Middle East and Africa sub-region leads with a 4.63% CAGR as infrastructure and food-security projects multiply.

Why are converters investing in digital printing lines?

Digital presses allow low-minimum-order runs, variable data and rapid artwork changeovers, suiting short-lived e-commerce promotions and reducing plate costs.

How are new regulations affecting barrier materials?

The PPWR bans PFAS barriers and pushes for 65% recyclable content by 2030, accelerating the shift to mono-material PE and PP laminates and chemically recycled nylons.

What recent M&A deal illustrates market consolidation?

Amcor’s acquisition of Berry Global’s healthcare packaging business exemplifies the scale-building trend among top converters.

Page last updated on: