Europe Lithium-ion Battery For Electric Vehicle Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

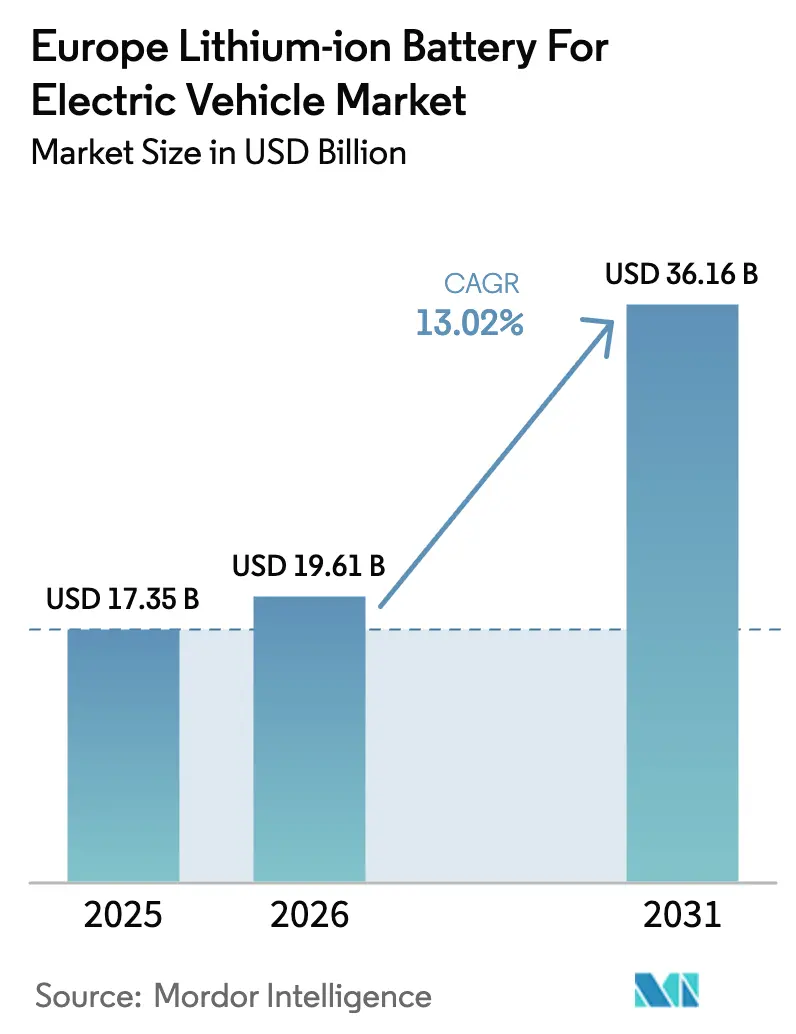

| Base Year Market Size (2025) | USD 17.35 Billion |

| Market Size (2026) | USD 19.61 Billion |

| Market Size (2031) | USD 36.16 Billion |

| Growth Rate (2026 - 2031) | 13.02% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Lithium-ion Battery For Electric Vehicle Market Analysis by Mordor Intelligence

Europe Lithium-ion Battery For Electric Vehicle Market size in 2026 is estimated at USD 19.61 billion, growing from 2025 value of USD 17.35 billion with 2031 projections showing USD 36.16 billion, growing at 13.02% CAGR over 2026-2031.

Battery-electric vehicles keep driving most pack demand, accounting for 85.4% of 2024 propulsion volume, while a wave of gigafactory announcements is reducing freight costs and shortening lead times across the region. Pouch-cell incumbency is strong, but prismatic designs that integrate directly into vehicle structures are scaling faster and pulling through iron-phosphate chemistries that reduce reliance on cobalt and nickel. Germany anchors production with 28.6% 2024 revenue, yet Spain now attracts the largest share of new capacity as energy prices and targeted subsidies undercut Northern European sites.(1)European Commission, “EU Battery Regulation,” europa.euRapid truck electrification, stricter carbon-intensity rules, and expanding second-life revenue streams all converge to keep regional demand on an upward path despite higher European power and labor costs than in North America or Asia.

Key Report Takeaways

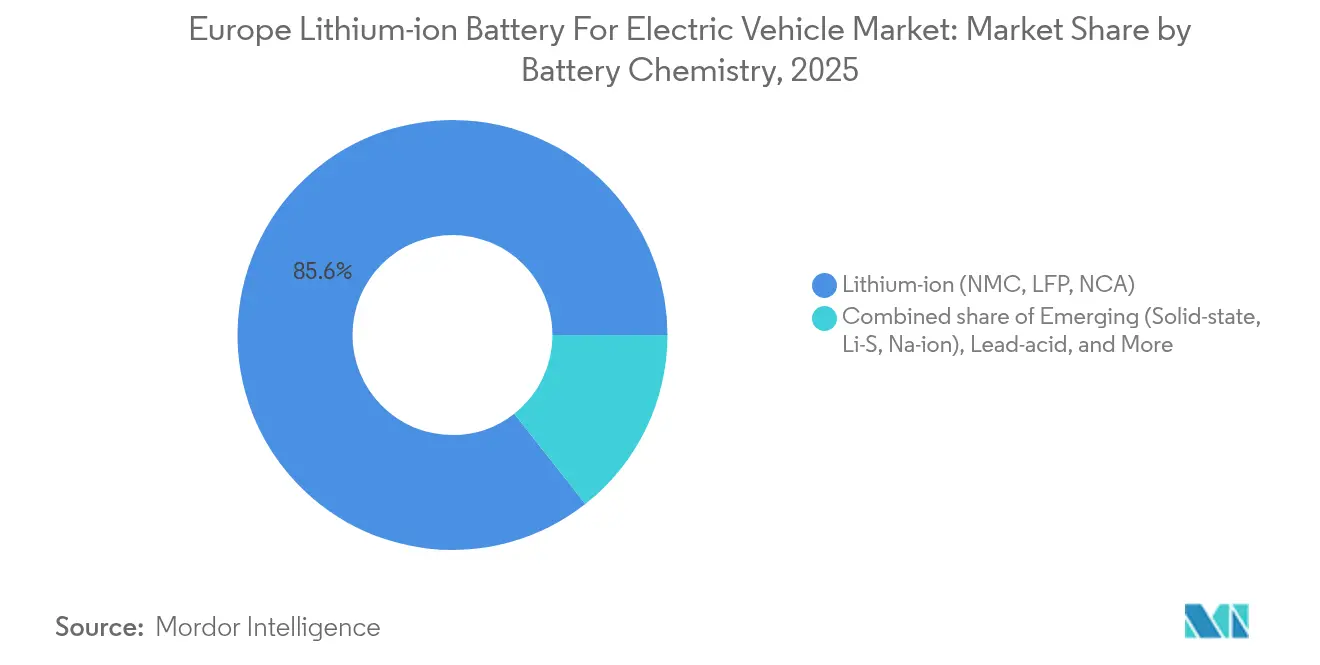

- By battery chemistry, lithium-iron-phosphate captured 38.65% revenue share in 2025 and remains the fastest expanding chemistry at 16.2% CAGR to 2031 within the lithium-ion family.

- By cell format, pouch cells commanded 47.45% of the European lithium-ion battery for electric vehicle market share in 2025, whereas prismatic cells are projected to grow at a 18.9% CAGR through 2031.

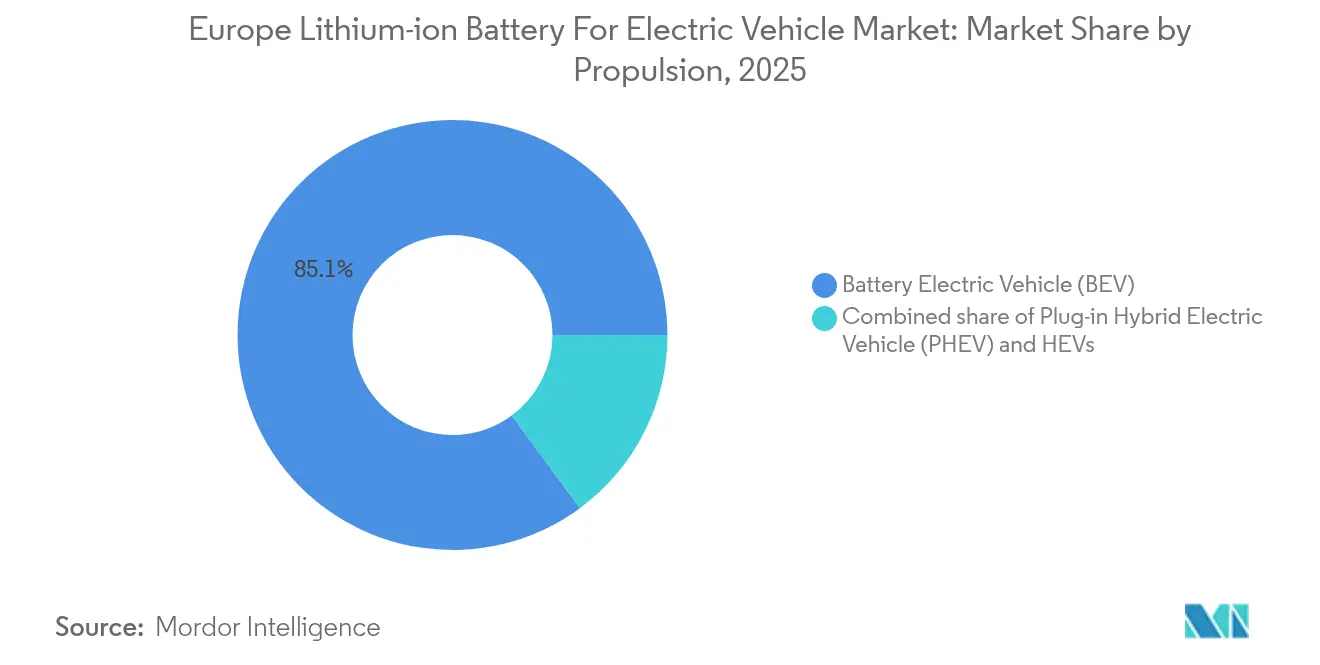

- By propulsion, battery-electric vehicles led with 85.10% revenue share in 2025, while medium and heavy trucks recorded the highest projected 21.1% CAGR through 2031.

- By vehicle type, passenger cars held 92.10% share of the European lithium-ion battery for electric vehicle market size in 2025, and the truck segment is forecast to expand at 21.1% CAGR to 2031.

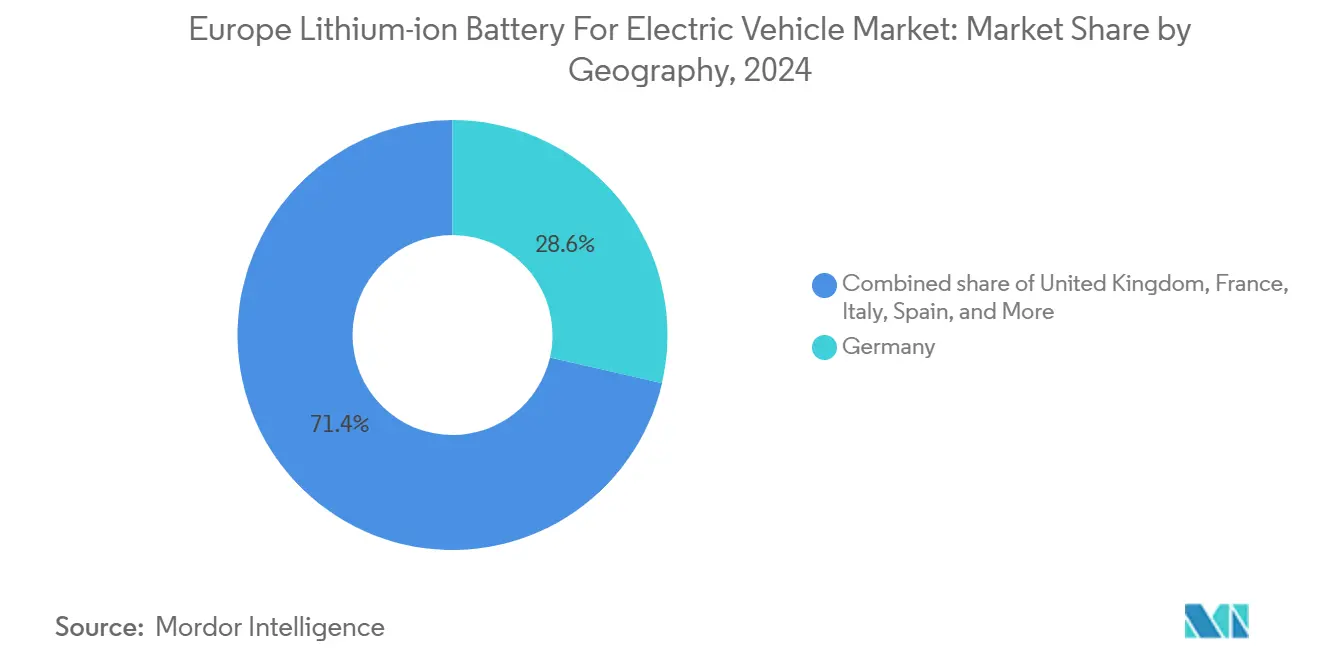

- By geography, Germany contributed 28.10% of 2025 revenue, yet Spain is set to lead growth with an 18.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Future direction is shaped by developments occurring across multiple regions, with Europe contributing to the overall trajectory. The outlook on worldwide lithium-ion battery for electric vehicle market reflects how these are expected to evolve collectively.

Europe Lithium-ion Battery For Electric Vehicle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining lithium-ion battery prices | +2.80% | Germany, France, Spain | Medium term (2-4 years) |

| Rapid growth in electric-vehicle registrations | +3.50% | Germany, UK, Nordic countries | Short term (≤ 2 years) |

| EU Green Deal and Battery Regulation | +2.10% | EU-27, led by France, Netherlands, Belgium | Long term (≥ 4 years) |

| Scale-up of EU gigafactories | +1.90% | Germany, France, Spain, Italy, Hungary | Medium term (2-4 years) |

| Roll-out of EU digital Battery Passport | +1.20% | EU-27, early movers Germany and Netherlands | Long term (≥ 4 years) |

| Second-life EV-battery revenue models | +0.90% | Germany, UK, Nordic countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Lithium-ion Battery Prices

Pack costs fell to USD 115 per kWh in 2024 after cathode suppliers negotiated larger volume rebates, helping original-equipment manufacturers launch 80 kWh to 100 kWh packs that deliver 500 km to 600 km real-world range. Iron-phosphate designs, which removed cobalt and nickel from the bill of materials, drove much of the savings and already account for 38% of regional cell demand. The price curve is not linear because lithium-carbonate spot values rebounded 22% in early 2025 when Chinese production tightened, pushing sub-USD 100 per kWh pack expectations beyond 2026. Automakers that locked multi-year offtake deals, such as BMW with Ganfeng Lithium, are insulated against sudden spikes.

Rapid Growth in Electric-Vehicle Registrations

Europe registered 2.1 million new battery-electric cars during 2024, up 21% year on year, with Norway, the Netherlands, and Germany taking 54% of volume. Corporate fleets represented 43% of deliveries because total lifetime operating cost swings in favor of electric drivetrains once annual mileage exceeds 25,000 km. Tightening European Union fleet CO₂ rules impose penalties of EUR 95 per gram per kilometer above target, pushing every manufacturer to prioritize zero-tailpipe sales.(2)European Commission, “EU Battery Regulation,” europa.eu High fleet penetration changes cell requirements because operators care more about cycle life and fast-charge behavior than peak energy density, which in turn favors lithium-iron-phosphate chemistries that retain 80% capacity after 3,000 cycles. Spot cell availability shrinks as brands sign multi-year contracts, lifting contract prices 8% to 12% above 2023 levels.

EU Green Deal and Battery Regulation Incentives

EU legislation that entered force in February 2024 obliges battery manufacturers to disclose full life-cycle carbon footprint by 2025 and to meet minimum recycled-content thresholds by 2031. Fully traceable packs qualify for favorable procurement scores from automakers, as shown by Northvolt’s Revolt unit, which recovered 1,200 metric tons of black mass in 2024 at >99.5% purity and secured premium contracts as a result. A blockchain-anchored digital passport becomes mandatory from 2027 and adds around EUR 20 per pack in software cost, yet permits differentiated pricing for low-carbon cells that can command a 3% to 5% premium. Early adopters, including ACC, are embedding passport data into manufacturing execution systems, erecting entry barriers for smaller assemblers. These rules collectively lift long-run demand and protect high-value domestic capacity.

Scale-up of EU Gigafactories

Announced European cell capacity climbed to 789 GWh by year-end 2024, with 312 GWh already online. Locating cell plants near final assembly slashes inbound freight by EUR 10 per kWh compared with trans-Pacific supply chains. Volkswagen’s PowerCo Valencia site sits 50 km from Martorell and Pamplona assembly, cutting lead time from six weeks to 10 days REUTERS.COM. Utilization risk remains because Northvolt Ett ran at only 28% of its nameplate in 2024 when BMW and Volvo delayed orders. Even so, the network effect still raises medium-term growth expectations for the European lithium-ion battery for electric vehicle market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Critical-mineral supply-chain dependence | -1.80% | Germany, France, Poland | Short term (≤ 2 years) |

| Competing next-generation chemistries | -0.90% | Germany, France, UK | Long term (≥ 4 years) |

| High industrial energy and labor costs | -1.40% | Germany, France, Italy, Belgium | Medium term (2-4 years) |

| Recycling-capacity bottlenecks after 2028 | -0.70% | Southern and Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Critical-Mineral Supply-Chain Dependence

Europe imports 98% of its lithium, 93% of its cobalt, and all natural graphite, while China controls most mid-stream refining, leaving the region exposed to shocks such as the 19% rise in neodymium prices after Beijing tightened export rules in January 2024. The Critical Raw Materials Act caps single-supplier reliance at 65% by 2030, yet domestic mines in Portugal and Germany will cover less than 8% of forecast lithium demand. Long-term fixed-price contracts help, as illustrated by LG Energy Solution’s 2024 cobalt precursor deal in China, but diversification remains aspirational. Lithium-iron-phosphate and manganese-rich chemistries ease cobalt exposure, although their lower energy density limits uptake in premium cars.

Competing Next-Generation Chemistries

Solid-state batteries promise 400 Wh/kg density and fast charging, but showed yields below 60% in 2024 pilot lines, while sodium-ion cells cut costs by 25% yet remain confined to low-range applications. Eight EU-funded consortia share EUR 925 million of Horizon grants, which accelerates lab work but fragments intellectual property and slows standard-setting. If solid-state reaches cost parity by 2028, existing liquid-lithium plants risk early write-offs, especially pouch lines that cannot easily retrofit ceramic separators. Near-term uncertainty keeps some automakers cautious about long-term offtake commitments, tempering capital spending in traditional formats.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: Diverse Pathways Shape Competitive Positioning

Lithium-ion chemistries accounted for 85.60% of 2025 demand, with the European lithium-ion battery for electric vehicle market size skewed toward nickel-manganese-cobalt mixes in premium models. Lithium-iron-phosphate gained a 38.65% share because it cuts cobalt and nickel out of the bill of materials and shows 3,000-cycle durability that aligns with commercial fleet needs. Producers use cell-to-pack layouts to offset the chemistry’s lower gravimetric density and still achieve 400 km to 450 km range. Solid-state, lithium-sulfur, and sodium-ion options are forecast to grow at a 25.1% CAGR as Horizon grants push lab projects toward pilot scale. The European lithium-ion battery for electric vehicle market share mix will adjust as next-generation formats clear 80% manufacturing yield and sub-USD 120 per kWh thresholds.

Over the forecast period, automakers will balance near-term cost reduction with longer-term density targets. Lithium-iron-phosphate packs already meet mass-market requirements and avoid supply-chain concentration in the Democratic Republic of Congo. Nickel-rich chemistries stay dominant in performance cars until solid-state reaches commercial maturity. Sodium-ion will secure low-speed urban microcars and stationary storage niches thanks to its cost advantage. The European lithium-ion battery for electric vehicle market will see incremental share gains for each alternative rather than a single disruptive swing.

By Cell Format: Prismatic Designs Capture the Growth Upside

Pouch cells controlled 47.45% of 2025 deliveries, but prismatic units are poised to expand at a 18.9% CAGR to 2031, driven by blade batteries that integrate directly into vehicle underbodies. The European lithium-ion battery for electric vehicle market size linked to prismatic formats rises as CATL and BYD offer structural designs that cut bill-of-materials cost by EUR 8 per kWh. Cylindrical cells retained a 28.35% share on the back of Tesla's Berlin plant, where 4680 tabless designs allow 4C charging without early thermal runaway. Pack makers converge on higher energy density by stacking electrodes, a technique that narrows the classic gap between pouch flexibility and prismatic rigidity.

As utilization ramps, format choice will hinge on platform standardization and locked-in supply contracts rather than intrinsic cell geometry. Prismatic cells' mechanical robustness suits commercial vehicles that face higher shock loads, while pouch cells stay attractive for compact cars needing flexible footprints. Cylindrical output will remain tied to manufacturers that own fast-winding lines. Blade and cell-to-pack systems skip the module layer entirely and help bring production time down from 4.5 hours to 2.1 hours per pack. All formats keep converging, ensuring the European lithium-ion battery for the electric vehicle market benefits from healthy competition and incremental efficiency gains.

By Propulsion: Battery-Electric Takes Center Stage

Battery-electric vehicles held 85.10% of 2025 demand and will grow at a 14.25% CAGR as charging points reach one fast charger for every eight battery cars across key markets. The European lithium-ion battery for electric vehicle market size linked to plug-in hybrids shrinks because subsidy regimes phase out incentives for combustion-engine hybrids. PHEVs captured 11.60% of 2025 lithium-ion volume, but real-world fuel economy gains disappointed regulators after telematics showed inconsistent charging habits. Hybrids that rely on tiny nickel-metal-hydride packs will erode further as automakers consolidate around pure electric platforms to reduce capital intensity.

Fleet and corporate buyers push BEV demand as their total operating cost per kilometer is 43% lower than diesel at 200,000 km lifetime when electricity is EUR 0.35 per kWh. European Union fleet targets compel manufacturers to sell more BEVs to dodge stiff penalties, embedding growth momentum. PHEV residual values soften as future urban restrictions tighten on combustion engines, reinforcing buyer preference for full electric. The European lithium-ion battery for electric vehicle market, therefore, remains anchored in pure electric propulsion, with hybrids serving a transitional niche only.

By Vehicle Type: Commercial Segments Enter High-Gear Growth

Passenger cars delivered 92.10% of 2025 battery volume, yet medium and heavy trucks show the steepest expansion at 21.1% CAGR as zero-emission zones proliferate in major cities. Daimler Truck’s eActros 600 uses a 600 kWh pack and has already logged 1,400 pre-orders, illustrating how fleet operators now view range as sufficient for regional haul. The European lithium-ion battery for electric vehicle market share for light commercial vans will keep growing as parcel delivery giants electrify urban fleets to meet sustainability targets. Buses follow a predictable duty cycle that simplifies depot charging and will maintain steady demand for long-life iron-phosphate cells.

Two-wheelers and micro-mobility see rapid unit growth but small absolute pack volumes because battery capacities remain modest. Trucks benefit from the CharIN Megawatt Charging System that replenishes 300 kWh in 15 minutes and pulls through high-cycle-life cells suited to heavy daily usage. By 2027, total-cost-of-ownership parity will extend to long-haul trucking routes above 120,000 km per year, unlocking a significant incremental demand bump. The diversified customer mix spreads risk and supports the sustained expansion of the European lithium-ion battery for electric vehicle market through 2031.

Geography Analysis

Germany generated 28.10% of 2025 revenue and remains the anchor for premium cylindrical output from Tesla’s Grünheide plant plus early volumes from ACC’s Kaiserslautern site. Industrial power above EUR 0.15 per kWh and rising wage costs threaten Germany’s cost base, but dense automotive supply chains and strong engineering talent keep the country competitive for high-value nickel-rich cells. An expanding domestic recycling network, led by BASF and Northvolt, supports compliance with the 2031 recycled-content mandate and provides feedstock security.

Spain is the breakout growth story with an 18.2% forecast CAGR as Volkswagen’s EUR 10 billion Sagunto complex scales to 40 GWh by 2026. Industrial electricity charges run 18% below Germany, and exemptions from the 7% electricity-generation levy lower costs by another EUR 0.011 per kWh, improving competitiveness. PowerCo co-locates cell production within 50 km of Martorell and Pamplona assembly, cutting logistics lead times and inventory lock-up. Coupled with proximity to Moroccan lithium projects, Spain positions itself as the cost leader for prismatic iron-phosphate cells aimed at mass-market cars.

France, the United Kingdom, and the Nordic countries round out the next tier, collectively contributing about 39.70% of 2025 demand. France benefits from ACC’s Billy-Berclau hub and Verkor’s Dunkirk project, both backed by Important Projects of Common European Interest funding that covers up to 25% of capital outlay. The United Kingdom must meet rules of origin thresholds that rise to 55% in 2027, prompting Envision AESC’s 38 GWh Sunderland expansion. Nordic capacity anchors around Northvolt Ett, which, despite a 2024 restructuring, still holds 16 GWh operational output and leverages abundant renewable energy to lock in long-term low-carbon contracts. Central and Eastern Europe attract cost-focused investments such as CATL’s 100 GWh Debrecen plant that supplies BMW’s Neue Klasse platform. This east-west bifurcation provides buyers with diverse sourcing options and underpins the overall resilience of the European lithium-ion battery for the electric vehicle market.

Analysis of the lithium-ion battery for electric vehicle market by Mordor Intelligence spans multiple other regional evaluations across Asia, Middle East and Africa, and South America, supported by country-level insights for France and United Kingdom, wherein local market conditions keep varying from one country to another.

Competitive Landscape

Asian suppliers hold scale advantages that let them price 8% to 12% below European peers, yet regional champions rely on recycling integration and low-carbon credentials to secure strategic offtake deals. The top five players, CATL, LG Energy Solution, Samsung SDI, Northvolt, and Panasonic, controlled about 68% of 2024 shipments, which positions the European lithium-ion battery for the electric vehicle market as moderately concentrated. CATL’s blade battery cuts pack assembly cost by EUR 20 per kWh, helping it win multi-year supply agreements with BMW and Stellantis. LG Energy Solution leverages JV structures to lock demand at utilization rates above 75%.

Northvolt’s Chapter 11 process lowered debt to USD 3.1 billion and refocused cash on its Skellefteå plant, where Revolt recycling now feeds nickel, cobalt, and lithium back into new cells at >99.5% purity. Automotive Cells Company, backed by Stellantis, Mercedes-Benz, TotalEnergies, and Saft, secured EUR 4.4 billion financing in 2024 and already shipped the first 8 GWh of high-nickel cells from Kaiserslautern in January 2025. Technology road maps differentiate suppliers: Tesla’s 4680 cylindrical design enables 4C charging in Berlin, BYD’s cell-to-pack supports 160 Wh per liter volumetric density, and ProLogium targets 400 Wh per kilogram solid-state outputs in Dunkirk by 2026.

Smaller disruptors such as Verkor, FREYR, Faradion, and Morrow focus on niche chemistries or regional security of supply. Verkor’s 16 GWh Dunkirk site will feed Renault’s 800-volt architecture, FREYR locked EUR 120 million of Norwegian support to build a 32 GWh plant aimed at storage and marine clients, and Faradion pairs with Reliance Industries to commercialize sodium-ion batteries for urban microcars in the United Kingdom. Recycling is emerging as a durable moat because the EU Battery Regulation will require 12% cobalt and 4% lithium recycled content by 2031, favoring firms that own a full loop. BASF’s Schwarzheide precursor plant pairs with a hydrometallurgical unit next door, and ACC embeds in-house recovery to secure compliance. Supply-chain localization, digital passports, and circular-economy integration, therefore, define the coming competitive playbook and sustain the medium-term growth of the European lithium-ion battery for the electric vehicle market.(4)Financial Times, “Blade Batteries Arrive in Europe,” ft.com

Europe Lithium-ion Battery For Electric Vehicle Industry Leaders

Contemporary Amperex Technology Co. Ltd (CATL)

LG Energy Solution Ltd

North Volt AB

Faradion Limited (U.K.)

Panasonic Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Automotive Cells Company began commercial output at its Kaiserslautern gigafactory, delivering 8 GWh of high-nickel NMC cells to Mercedes-Benz and activating a digital Battery Passport that meets the 2027 EU mandate.

- December 2024: Northvolt exited Chapter 11 after securing USD 245 million debtor-in-possession financing led by Volkswagen and Goldman Sachs, trimming debt to USD 3.1 billion and focusing on the Skellefteå plant.

- November 2024: Volkswagen’s PowerCo inaugurated its 40 GWh Valencia cell plant that will supply ID.4, ID.7, and Cupra Born platforms, benefiting from Spain’s lower energy costs.

- October 2024: CATL approved a EUR 2.1 billion expansion of its Debrecen, Hungary site to 135 GWh, including a blade-battery line for European structural-pack programs.

Europe Lithium-ion Battery For Electric Vehicle Market Report Scope

A lithium-ion battery for electric vehicles (EVs) is a rechargeable battery commonly used to power electric cars and other electric vehicles. Lithium-ion batteries comprise cells containing an anode, cathode, separator, and electrolyte. These batteries offer a high power-to-weight ratio, excellent energy efficiency, and reduced self-discharge compared to other rechargeable batteries, making them a preferred choice for modern electric vehicles.

The European Lithium-ion Battery for Electric Vehicles Market is Segmented by Battery Chemistry, Cell Format, Propulsion Type, and Vehicle Type. By Battery Chemistry, the Market is Segmented by Lithium-ion (Nmc, Lfp, Nca), Emerging (Solid-state, Li-S, Na-ion), Lead-acid, and Nickel-metal-hydride. By Cell Format, the Market is Segmented Into Cylindrical, Prismatic, and More. By Propulsion Type, the Market is Segmented Into BEV, PHEV, and HEV. By Vehicle Type, the Market is Segmented Into Passenger Cars, Light Commercial Vehicles, Medium and Heavy Trucks, Buses and Coaches, and Two and Three-wheelers.

By geography, the market is segmented into Germany, the United Kingdom, France, Italy, Spain, the NORDIC Countries, the Netherlands, Russia, Rest of Europe. The report also covers the market sizes and forecasts in terms of value (USD) for all the above segments.

| Lithium-ion (NMC, LFP, NCA) |

| Emerging (Solid-state, Li-S, Na-ion) |

| Lead-acid |

| Nickel-metal-hydride |

| Cylindrical |

| Prismatic |

| Pouch |

| Blade/Cell-to-Pack |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Trucks |

| Buses and Coaches |

| Two and Three-wheelers |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| NORDIC Countries |

| Netherlands |

| Russia |

| Rest of Europe |

| By Battery Chemistry | Lithium-ion (NMC, LFP, NCA) |

| Emerging (Solid-state, Li-S, Na-ion) | |

| Lead-acid | |

| Nickel-metal-hydride | |

| By Cell Format | Cylindrical |

| Prismatic | |

| Pouch | |

| Blade/Cell-to-Pack | |

| By Propulsion | Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) | |

| Hybrid Electric Vehicle (HEV) | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium and Heavy Trucks | |

| Buses and Coaches | |

| Two and Three-wheelers | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Netherlands | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe lithium-ion battery for electric vehicle market in 2026?

It is valued at USD 19.61 billion and is forecast to reach USD 36.16 billion by 2031.

What is the expected CAGR for lithium-ion EV batteries in Europe to 2031?

The market is projected to grow at a 13.02% CAGR over 2026-2031.

Which chemistry is growing fastest inside European EV batteries?

Lithium-iron-phosphate cells are expanding the quickest, advancing 16.2% per year within the lithium-ion category.

Why is Spain emerging as a European battery hotspot?

Spain offers lower industrial power prices, large Volkswagen investments, and policy incentives that cut operating costs.

How will EU Battery Regulation affect suppliers?

It forces carbon-footprint disclosure, minimum recycled content, and digital passports, favoring vertically integrated manufacturers that control recycling.

What segment drives the highest future growth?

Medium and heavy trucks show the strongest forecast at 21.1% CAGR as fleet operators electrify to meet new emission rules.

Page last updated on: