Europe High Voltage Switchgear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

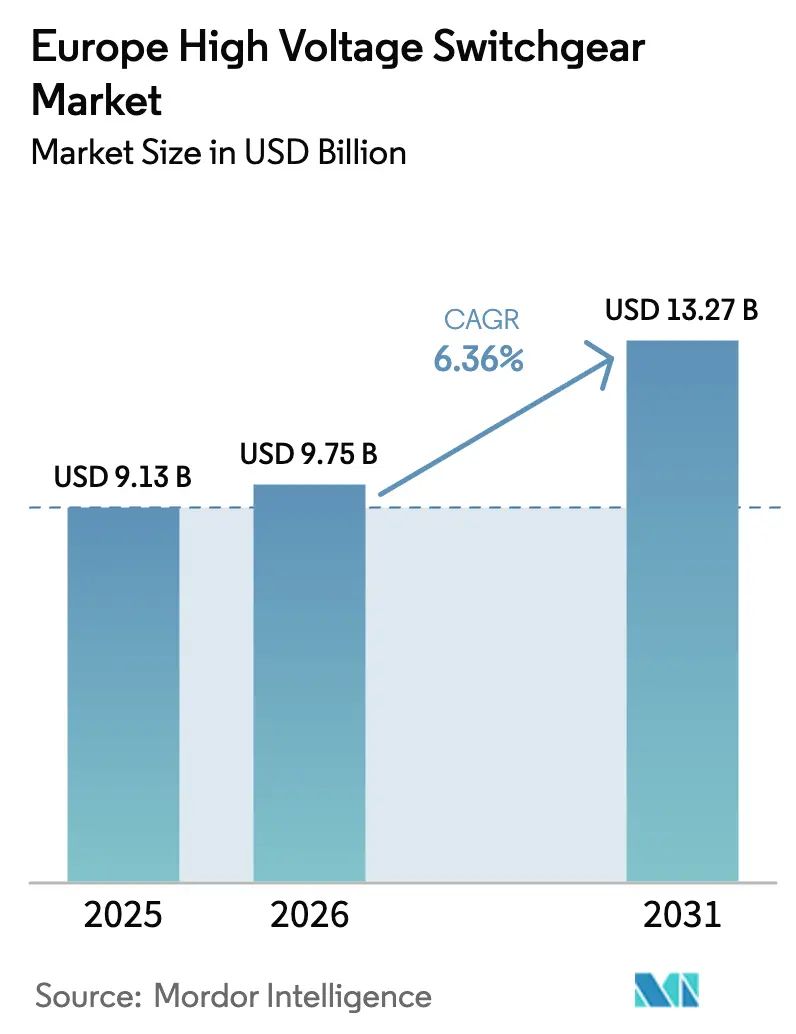

| Base Year Market Size (2025) | USD 9.13 Billion |

| Market Size (2026) | USD 9.75 Billion |

| Market Size (2031) | USD 13.27 Billion |

| Growth Rate (2026 - 2031) | 6.36% CAGR |

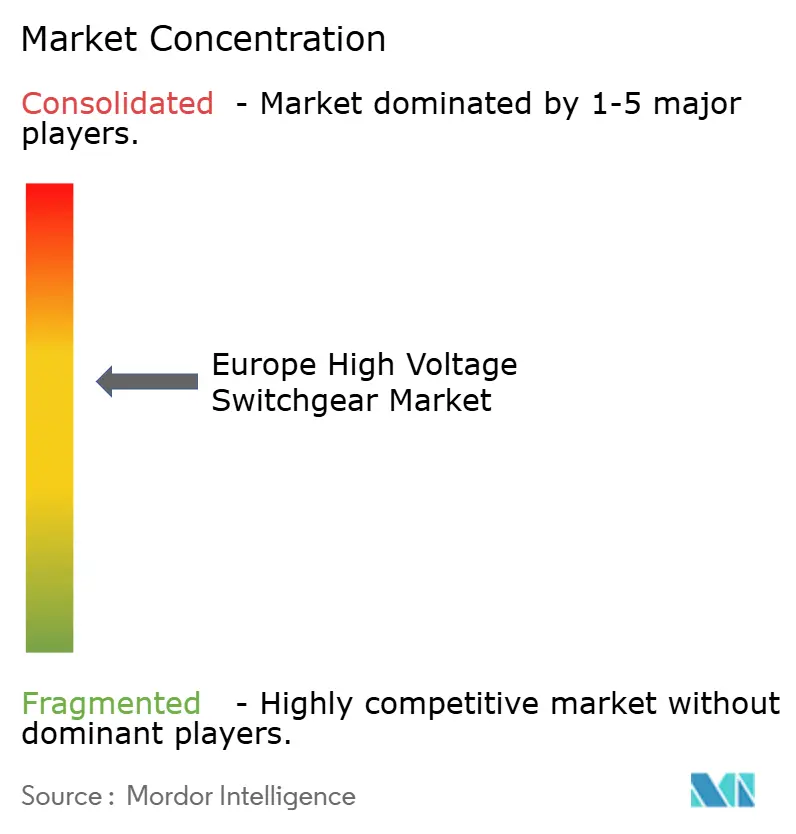

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe High Voltage Switchgear Market Analysis by Mordor Intelligence

The Europe High Voltage Switchgear Market size is projected to be USD 9.13 billion in 2025, USD 9.75 billion in 2026, and reach USD 13.27 billion by 2031, growing at a CAGR of 6.36% from 2026 to 2031.

The region’s growth rests on three pillars: stringent revisions to the EU F-gas Regulation that accelerate a pivot toward SF₆-free equipment, a once-in-a-generation overhaul of transmission assets installed during the 1970s–1980s build-out, and an expanding roster of HVDC interconnectors that anchor offshore wind and data-center loads to mainland grids. Utilities are front-loading orders to beat looming compliance deadlines, even as metal-price volatility pressures their capital budgets. In parallel, industrial players, battery gigafactories, green-hydrogen electrolyzers, and semiconductor fabs are contracting directly for factory-assembled switchgear to compress construction schedules and safeguard power quality, broadening the customer base beyond traditional network owners. Competitive dynamics are fluid: incumbents still command scale in gas-insulated switchgear, yet the rise of vacuum, clean-air, and fluoronitrile-CO₂ platforms is lowering barriers for regional specialists, reshaping supplier shortlists for new tenders.

Key Report Takeaways

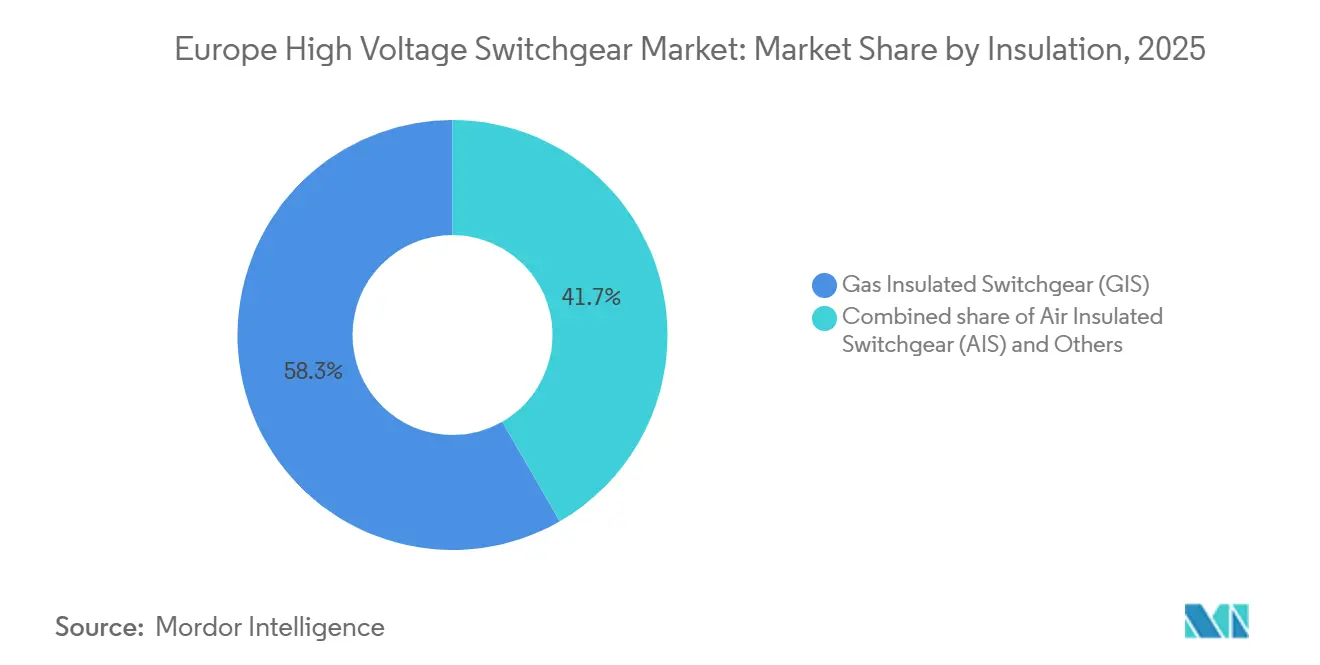

- By insulation type, gas-insulated switchgear captured 58.31% of the European high voltage switchgear market share in 2025, while SF₆-free alternatives under “Others” are forecast to advance at a 12.63% CAGR through 2031.

- By current type, AC equipment dominated with 88.17% of the European high voltage switchgear market share in 2025; DC switchgear is projected to expand at a 9.22% CAGR to 2031.

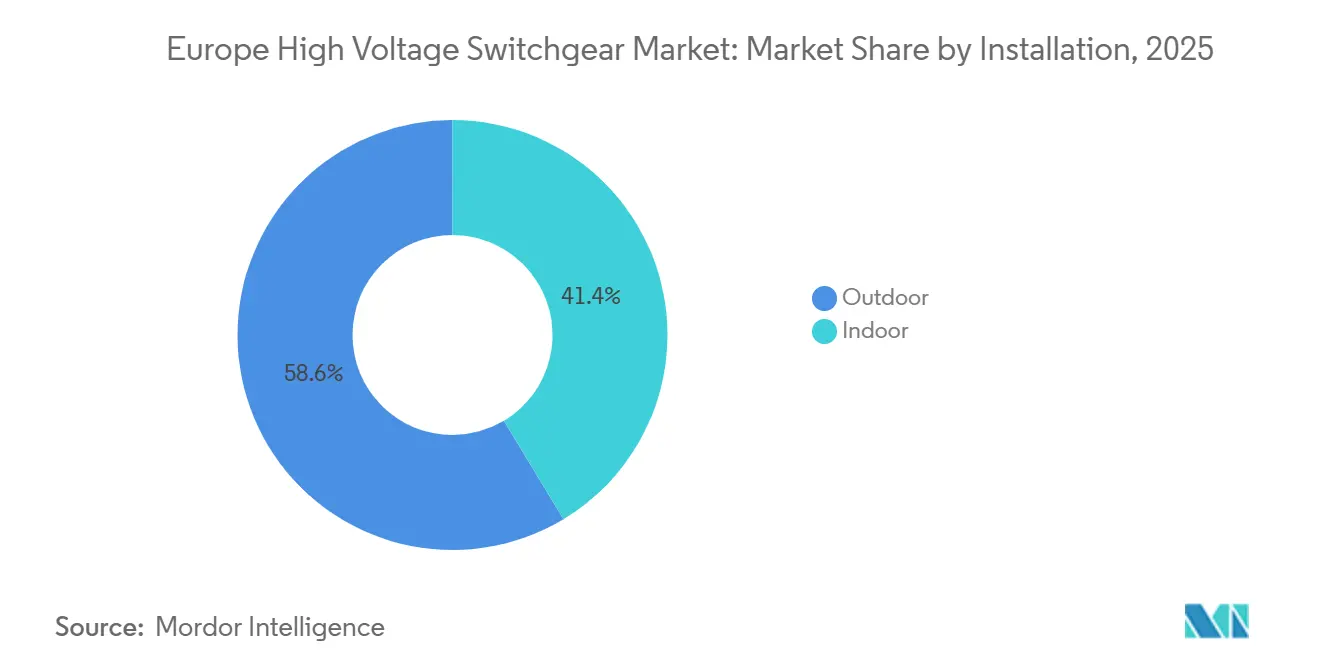

- By installation, outdoor configurations held a 58.63% slice of the European high voltage switchgear market size in 2025 and are set for 6.85% CAGR growth out to 2031.

- By end-user, utilities commanded a 67.50% share in 2025, whereas industrial customers posted the highest 8.91% CAGR forecast through 2031.

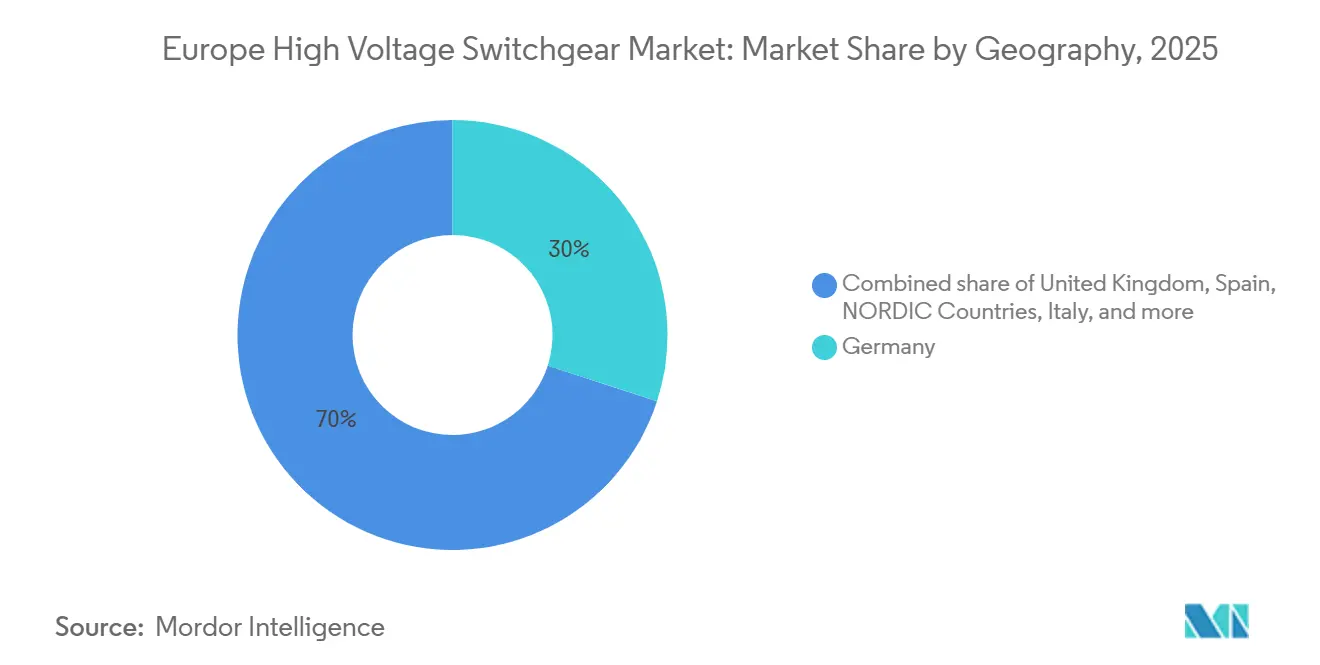

- By geography, Germany led revenue with 27.99% in 2025; the United Kingdom is the fastest riser at 9.47% CAGR for 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Proportional positioning is established by comparing regional contributions against the global total, including that of Europe. The high voltage switchgear market share in our global report expresses these relative weights.

Europe High Voltage Switchgear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-modernization capex rebound post-COVID-19 | +1.2% | Germany, UK, France, Nordic countries | Medium term (2–4 years) |

| Renewable-driven interconnector build-out | +1.8% | UK, Nordic, Germany, Spain | Long term (≥ 4 years) |

| Mandatory replacement of aging 1970–90s assets | +1.5% | Germany, France, Italy, Spain | Long term (≥ 4 years) |

| Data-center and HPC cluster electrification | +0.9% | Germany, Netherlands, Ireland, Nordic | Short term (≤ 2 years) |

| EU Green-Taxonomy loans favoring SF₆-free gear | +1.0% | EU-wide, early uptake in Germany, France, Netherlands | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Grid-Modernization Capex Rebound Post-COVID-19

Transmission system operators are spending at a pace unseen since the early 2010s, reversing a half-decade of austerity. ENTSO-E’s 2024 Ten-Year Network Development Plan earmarked EUR 584 billion for grid works to 2032, with roughly 18% devoted to high-voltage substations and switchgear.[1]ENTSO-E, “Ten-Year Network Development Plan 2024,” entsoe.eu Germany’s four TSOs alone committed EUR 110 billion for 2024–2030 upgrades, embedding large multi-year switchgear orders.[2]Bundesnetzagentur, “Netzentwicklungsplan Strom 2025,” bundesnetzagentur.de The United Kingdom cleared 26 GW of new transmission projects in 2025, implying 140 new or refurbished substations. Rising copper and aluminum prices add procurement risk, yet operators are accelerating tenders to lock in factory slots before SF₆-free production ramps stress global supply lines.

Renewable-Driven Interconnector Build-Out

Offshore wind integration is rewriting Europe’s transmission topology. The North Sea Wind Power Hub advanced a 10 GW artificial-island concept in 2025 that will host hundreds of HVDC breakers and DC switchgear modules.[3]TenneT, “North Sea Wind Power Hub Position Paper 2025,” tennet.eu The Baltic Synchronization program is deploying back-to-back converters on the Polish and Lithuanian borders, necessitating new DC yards. Spain’s second Biscay Gulf corridor, now in tender, scales to 2 GW and deepens DC hardware demand. These projects create parallel replacement demand for coastal AC assets upgraded to bidirectional power flows.

Mandatory Replacement of Aging 1970–90s HV Assets

Aging fleets are hitting end-of-life thresholds. France’s RTE reports 22% of its 400 kV and 225 kV switchgear exceeds 40 years, triggering a EUR 12 billion renewal through 2035. Italy’s Terna mapped 1,800 km of lines and 85 substations for overhaul by 2030, allocating EUR 1.8 billion for new bays. Germany is decommissioning 1980s SF₆ units to meet 2030 phase-down targets, adding complexity through live-line work and bypass circuits.

Data-Center and HPC Cluster Electrification Surge

Hyperscale campuses now draw power comparable to mid-sized cities. Ireland’s EirGrid records data centers at 21% of national consumption in 2025 and expects 1.2 GW of incremental load that needs 18 new 110 kV GIS-equipped substations.[4]EirGrid, “All-Island Generation Capacity Statement 2025,” eirgrid.ie Frankfurt added eight facilities in 2024–2025, each requiring dedicated HV feeders. The Netherlands temporarily capped new builds in 2024, underscoring grid bottlenecks linked to switchgear delivery lead times.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter SF₆-emission caps raise compliance costs | -0.7% | EU-wide, strict in Germany, France, Netherlands | Short term (≤ 2 years) |

| High GIS upfront CAPEX amid budget squeezes | -0.5% | Southern and Eastern Europe | Medium term (2–4 years) |

| Copper and aluminum volatility inflates risk | -0.4% | EU-wide, acute on mega interconnectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter SF₆-Emission Caps Raise Compliance Costs

The 2024 F-gas revision mandates a 60% SF₆ supply cut by 2030, forcing utilities to deploy leak-detection, gas-recovery, and staff-training programs that elevate ownership cost by 8–12%. Germany logged an 18% emissions drop from 2020-2024, but its 12,000 t legacy gas stock remains a decommissioning liability. Shrinking supply lifted SF₆ spot prices by 40% since 2023, sharpening the replacement case yet squeezing budgets.

High GIS Upfront CAPEX Amid Utility Budget Squeezes

GIS costs 30–50% more than AIS per bay, translating to over EUR 8 million extra on a 400 kV, 12-bay yard. Terna’s weighted average cost of capital rose to 6.2% in 2024, prompting deferral of several GIS upgrades. Red Eléctrica similarly opted for AIS life-extension schemes that save near-term cash but raise long-run maintenance risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insulation: SF₆-Free Platforms Gain Momentum

Gas-insulated technology secured 58.31% of 2025 revenue, yet the “Others” category, vacuum, air-plus, and fluoronitrile-CO₂ mixes, shows the strongest 12.63% CAGR outlook, reshaping high voltage switchgear market dynamics. The high voltage switchgear market size for SF₆-free variants is projected to exceed USD 3.2 billion by 2031 as more utilities bid clean-air platforms into urban and offshore schemes. ABB’s AirSeT landed its first 380 kV order with TenneT in 2024, signaling utility comfort with vacuum interrupters at transmission voltages. Siemens Energy’s blue GIS now spans 40+ substations across Germany and France.[5]Siemens Energy, “Blue GIS Reference Book 2025,” siemens-energy.com Early clean-air prototypes faced dielectric-strength questions in humid zones, extending commissioning times, yet iterative design and expanded factory tests are reducing field-validation hurdles.

By Current Type: DC Switchgear Accelerates

While AC equipment represented 88.17% of 2025 sales, DC hardware is projected to post a 9.22% CAGR, underpinned by 20 GW of HVDC capacity now under construction in the North Sea and Baltic corridors. Hitachi Energy’s hybrid DC breaker dominates delivered projects on NordLink and Viking Link. Solid-state prototypes by ABB and Siemens Energy promise faster clearing speeds but remain in pilot status. Hyperscale operators such as Microsoft trialed 380 V DC distribution that trimmed facility energy use by 7%, reinforcing a nascent data-center pull toward low-voltage DC switchgear. The high voltage switchgear market share for DC remains modest but rising as converter-rich networks become the norm for remote renewables.

By Installation: Outdoor Dominates

Outdoor assemblies accounted for 58.63% revenue in 2025 and are tracking a 6.85% CAGR to 2031, buoyed by land-rich rural substations that favor air-insulated footprints. Natural convection cooling curbs OPEX, though exposure to salt and industrial pollutants demands advanced coatings. ABB’s 2024 silicone-rubber insulator cut maintenance intervals by an estimated 30%. Indoor GIS, representing 41.37%, is entrenched in Berlin, London, and Amsterdam, where land trades above EUR 1,000 per m². Digital-sensor density is easier to embed in climate-controlled halls, a factor shaping urban replacement strategies.

By End-User: Industrial Segment Surges

Utilities held 67.50% of 2025 demand, yet the industrial cohort is pacing at 8.91% CAGR, the fastest within the high voltage switchgear market. Northvolt’s Ett gigafactory draws 150 MW at peak, requiring a 145 kV yard with eight GIS bays. Ørsted’s 2 GW H2RES offshore wind-to-hydrogen hub will run modular DC switchgear for electrolyzers. The high voltage switchgear market size allocated to industrial buyers is expected to double between 2025 and 2031 as battery, hydrogen, and semiconductor projects codify direct grid connections.

Geography Analysis

Germany contributed 27.99% of the 2025 turnover, channeling EUR 20 billion toward substation and switchgear refresh under Energiewende. The United Kingdom exhibits a 9.47% CAGR outlook, buoyed by a GBP 60 billion plan that earmarks 140 substations for offshore wind take-off. Nordic TSOs together pledge EUR 18 billion to hydropower links and DC corridors, lifting demand in Norway, Sweden, Denmark, and Finland. Baltic synchronization will inject EUR 1.2 billion into converter-station switchgear on the Polish-Lithuanian border. The rest of Europe cluster benefits from EU cohesion funds targeting Poland, Romania, and Bulgaria, while data-center clusters in the Netherlands and Ireland intensify local switchgear procurement.

Mordor Intelligence examines the high voltage switchgear market across diverse other regional markets as well, including North America, Middle East and Africa, and Asia.

Competitive Landscape

Europe’s supplier base is moderately concentrated. ABB, Siemens Energy, Hitachi Energy, and Schneider Electric control 55–60% of revenue, yet SF₆-free adoption is creating white-space for agile entrants. ABB booked USD 2 billion in SF₆-free orders during 2024–2025, lifting the clean-portfolio mix to 32%. Siemens Energy reported 50+ blue GIS installations and became the de facto spec in recent Dutch and German tenders. Hitachi Energy leverages HVDC know-how to front-run offshore interconnector awards. Schneider Electric monetizes its EcoStruxure digital layer, adding USD 457 million in 2024 software and services. Regional firms like Ormazabal, Lucy Electric, and Efacec are winning modular factory-built lines suited to data-center and industrial clients, where speed trumps bespoke design. Sensor-rich panels, edge computing, and IEC 61850 compliance are emerging as table stakes that deepen after-sales annuity streams.

Europe High Voltage Switchgear Industry Leaders

ABB Ltd

Siemens AG

Hitachi Energy Ltd

Schneider Electric SE

General Electric Company (GE Grid Solutions)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: HD Hyundai Electric has clinched a contract in Finland, marking its European debut of a new line of eco-friendly circuit breakers. The deal entails the supply of 14 units of 14 kV gas-insulated switchgear (GIS).

- August 2025: Siemens Energy has successfully tested its prototype, the SF₆-free 420 kV air-insulated circuit breaker (3AV2FI 420 kV), leveraging vacuum technology. The prototype tests validated the technical feasibility of employing vacuum technology for 420 kV circuit breakers. Transmission system operators RTE in France and Statnett in Norway are set to install the fully industrialised solution in the latter half of 2026.

- August 2025: Schneider Electric inked a long-term framework agreement with E.ON, a major player among Europe's energy giants. This collaboration underscores a pivotal move towards advancing sustainable and digitally-adept energy infrastructures throughout Europe.

- July 2025: Hitachi Energy, a global leader in electrification, has inked a deal with E.ON, potentially worth up to USD 700 million. This collaboration aims to supply transformers to the German energy grid, enhancing the country's energy security, resilience, and affordability.

Europe High Voltage Switchgear Market Report Scope

A high-voltage switchgear is a power system that operates at voltages greater than 36 kV, and as a result, the arcing generated during switching operation is also very high. Accordingly, higher caution should be exercised while constructing high-voltage switchgear. A switchgear system is n electrical power system that controls, regulates, and switches on or off the electrical circuit. Switchgear devices include circuit breaker devices, fuses, isolators, relays, current and potential transformers, lightning arresters, indicating instruments, and control panels.

The European high voltage switchgear market is segmented by insulation, current type, installation, end-user, and geography. By insulation, the market is segmented into gas-insulated switchgear, air-insulated switchgear, and others. By current type, the market is segmented into AC switchgear and DC switchgear. By installation, the market is segmented into indoor and outdoor. By end-user, the market is segmented into utilities, residential, commercial, and industrial. The report also covers the market size and forecasts for the switchgear market across major countries in the region. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Gas Insulated Switchgear (GIS) |

| Air Insulated Switchgear (AIS) |

| Others |

| AC Switchgear |

| DC Switchgear |

| Indoor |

| Outdoor |

| Utilities |

| Residential |

| Commercial |

| Industrial |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| NORDIC Countries |

| Russia |

| Rest of Europe |

| By Insulation | Gas Insulated Switchgear (GIS) |

| Air Insulated Switchgear (AIS) | |

| Others | |

| By Current Type | AC Switchgear |

| DC Switchgear | |

| By Installation | Indoor |

| Outdoor | |

| By End-User | Utilities |

| Residential | |

| Commercial | |

| Industrial | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the European high voltage switchgear market in 2026?

It is on track to reach USD 9.75 billion in 2026, following the 6.36% CAGR trajectory set between 2026 and 2031.

Which insulation technology is growing fastest?

SF₆-free solutions - vacuum, clean-air, and fluoronitrile-CO₂ mixes - are advancing at 12.63% CAGR, the quickest among all insulation types.

Why is DC switchgear gaining attention?

New HVDC interconnectors for offshore wind and hyperscale data-center adoption of direct-current power are lifting DC switchgear demand at a 9.22% CAGR.

What role do industrial projects play in demand growth?

Battery gigafactories, hydrogen electrolyzers, and semiconductor fabs require dedicated substations, driving the industrial segment's 8.91% CAGR.

How are EU regulations influencing technology choices?

The updated F-gas Regulation and EU Taxonomy restrict high-GWP gases, pushing utilities and lenders toward vacuum and clean-air switchgear platforms.

Which country is expanding the fastest?

The United Kingdom posts the highest regional growth, projected at 9.47% CAGR through 2031, supported by a GBP 60 billion grid-upgrade plan.

Page last updated on: