Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.10 Billion |

| Market Size (2026) | USD 1.11 Billion |

| Market Size (2031) | USD 1.18 Billion |

| Growth Rate (2026 - 2031) | 1.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Ceramic Tiles Market Analysis by Mordor Intelligence

The Poland ceramic tiles market size was valued at USD 1.10 billion in 2025 and estimated to grow from USD 1.11 billion in 2026 to reach USD 1.18 billion by 2031, at a CAGR of 1.23% during the forecast period (2026-2031). This measured trajectory underscores a mature landscape where demand relies on renovation activity, product innovation, and selective export gains. Rising residential retrofits, EU-backed energy-efficiency subsidies, and large-format porcelain adoption are cushioning the sector against volatile natural-gas prices that inflate up to 30% of production costs and mounting competition from LVT and SPC flooring alternatives[1]Source: Cerame-Unie, “EU Tiles Market Statistics 2025,” cerameunie.eu. Export orientation—over 40% of output ships abroad, continues to support factory utilization, while e-commerce gains, thin-tile façades, and digital printing open novel value pools that can offset slowing domestic new-build activity. Market leaders are prioritizing kiln upgrades, waste-recycling feedstocks, and AI-assisted surface design to improve margins and maintain relevance in premium segments.

Key Report Takeaways

- By application, floor coverings commanded 63.25% of Poland's ceramic tile market share in 2025, and roofing and façade systems are projected to rise at a 1.72% CAGR through 2031.

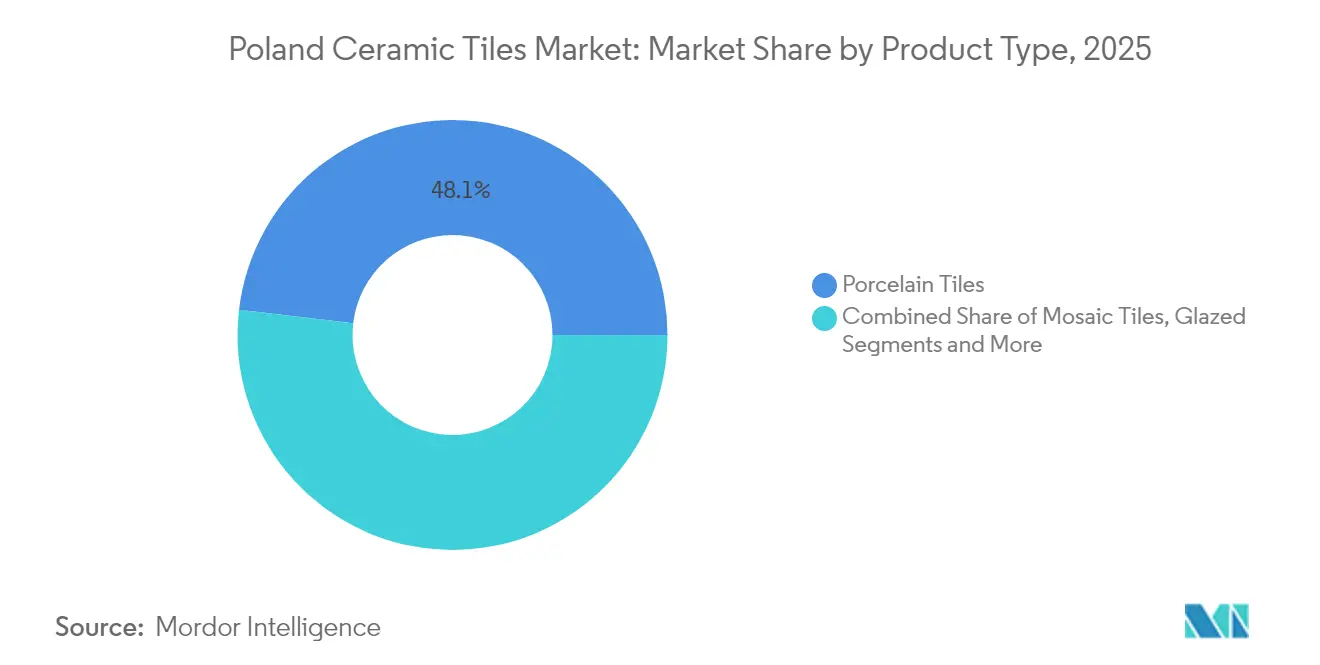

- By product type, porcelain occupied 48.12% of the Poland ceramic tiles market size in 2025, whereas mosaic tiles are advancing at a 1.05% CAGR to 2031.

- By end-user, residential held 43.85% of Poland's ceramic tiles market share in 2025, and commercial applications are set to expand at a 2.39% CAGR through 2031.

- By distribution channel, home-improvement and DIY stores secured 42.10% of Poland's ceramic tile market share in 2025, while online retail is growing at a 4.18% CAGR through 2031.

- By geography, Central Poland accounted for 28.86% of Poland's ceramic market size in 2025, whereas Northern Poland is expected to grow at a 3.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Poland Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising residential renovation & loft conversions | +0.3% | Central & Northern Poland | Medium term (2-4 years) |

| Government subsidies for energy-efficient retrofits | +0.2% | Southern & Eastern Poland | Long term (≥ 4 years) |

| Developer shift toward large-format porcelain slabs | +0.2% | Urban centers in Central & Western Poland | Medium term (2-4 years) |

| Growth of e-commerce DIY channels | +0.2% | National metro areas | Short term (≤ 2 years) |

| Digital ink-jet printing & custom designs | +0.1% | Łódź manufacturing hub | Medium term (2-4 years) |

| Thin-tile panels for façades & cladding | +0.1% | Western & Central Poland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Residential Renovation & Loft-Conversion Activities

Renovation has overtaken new-builds as the primary catalyst for the Poland ceramic tiles market. Single-family housing starts dipped 10% in 2024 versus 2023 yet remained above the pre-pandemic baseline, while renovation permits rose thanks to tax incentives and easier planning approvals. Łódź Voivodeship supplies 70% of national output, shortening delivery times to dense Central-Poland metro corridors. Loft conversions, popular in former textile warehouses, depend on ceramic tiles for fire resistance and moisture control, features that vinyl cannot fully match. Continuous upgrades to pre-2000 housing stock keep demand steady even when macro cycles soften[2]Source: Wienerberger AG, “2024 Annual Report,” wienerberger.com..

Government Subsidies for Energy-Efficient Housing Retrofits

The “Czyste Powietrze” program allocates grants covering insulation, window replacement, and efficient heating; ceramic flooring frequently forms part of the required thermal envelope upgrade[3]Source: Gov.pl, “Czyste Powietrze Program Rules 2025,” gov.pl. Eligibility thresholds encourage uptake among households earning under PLN 135,000 annually, stimulating latent demand in lower-income communities. Energy audits bundled into the subsidy process prioritize low-conductivity underlayments and low-porosity floor tiles, nudging consumers toward premium porcelain lines. Subsidies dovetail with EU Fit-for-55 targets, supporting a narrative that ceramic surfaces aid in meeting building-energy quotas.

Developer Shift Toward Large-Format Porcelain Slabs

Architects now specify panels up to 1,500 × 3,000 mm and 3-5 mm thick for retail, hospitality, and office fit-outs. Ceramika Paradyż’s TRI-D sintered stone line (320 × 160 cm) reduces grout lines, accelerates installation, and delivers stone-like looks at lighter weights. Developers value lower lifecycle costs from fewer joints, minimal maintenance, and scratch resistance, qualities that have strengthened porcelain’s grip on the commercial segment and helped the poland ceramic tiles market defend share against laminates. The shift toward large formats also optimizes manufacturing efficiency, as fewer pieces cover equivalent surface areas, reducing handling and logistics costs throughout the value chain.

Growth of E-Commerce DIY Channels for Building Materials

Online sales of home-improvement goods in Poland are rising at a 4.30% CAGR, outpacing brick-and-mortar. Digital marketplaces bundle 3D room visualizers and VR tools, enabling end-users to preview colorways before checkout. Domestic giant Mrówka’s site now lists over 6,000 tile SKUs, while Castorama and Leroy Merlin deploy click-and-collect hubs across 171 combined stores. Direct-to-consumer portals allow manufacturers to bypass wholesaler margins, raising netbacks by up to 12% and improving working-capital turns. Digital channels particularly benefit ceramic tile categories requiring visual selection, as high-resolution imagery and augmented reality tools allow customers to visualize products in their spaces before purchase. This channel evolution also supports customization trends, enabling on-demand production of specialized designs that would be economically unfeasible through traditional retail models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile natural-gas prices | -0.2% | Nationwide manufacturing belts | Short term (≤ 2 years) |

| Intensifying competition from LVT & SPC | -0.2% | Residential renovations | Medium term (2-4 years) |

| EU carbon-border-adjustment costs | -0.1% | Import-dependent niches | Long term (≥ 4 years) |

| Rising supply-chain disruptions | -0.1% | Raw-material logistics corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Natural-Gas Prices Inflating Kiln-Firing Costs

Natural gas covers roughly 70% of firing energy. Spot spikes in 2024 slashed industry capacity utilization from 75% to 57%, prompting temporary kiln shutdowns. ECB econometric models suggest a 1% energy-price uptick can cut fixed investment by 4.1% in energy-intensive sectors[4] Source: European Central Bank, “Energy Shocks and Capital Expenditure,” ecb.europa.eu.. Polish producers hedge with multiyear supply contracts, cogeneration retrofits, and biomass trials yet remain exposed to Russia-Ukraine pipeline risks. Digital printing eliminates traditional screen limitations, enabling unlimited color variations and pattern complexity that respond to individual customer preferences rather than mass-market averages. This technology particularly benefits commercial applications where brand identity and unique design elements justify premium pricing over standard ceramic offerings. On-demand production models also reduce inventory carrying costs while enabling rapid response to design trends and seasonal preferences.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Retains Lead Through Technical Superiority

Porcelain tiles command 48.12% market share in 2025, reflecting their superior technical properties and manufacturing versatility that enable large-format applications and digital printing customization. Mosaic tiles emerge as the fastest-growing segment at 1.05% CAGR through 2031, driven by architectural trends favoring decorative accents and artisanal aesthetics in both residential and commercial applications. Glazed ceramic tiles maintain steady demand through traditional applications, while unglazed varieties serve industrial and high-traffic commercial environments requiring slip resistance and durability over aesthetic considerations.

Thin-tile innovations blur distinctions between wall and floor categories, fostering cross-application products that streamline SKU counts at retail. Unglazed quarry tiles maintain footholds in industrial corridors and public transport hubs where slip coefficients and abrasion ratings trump aesthetics.The shift toward large-format porcelain slabs measuring up to 320×160 cm demonstrates technological advancement in pressing and firing capabilities, with manufacturers like Ceramika Paradyż investing in specialized equipment to serve architectural markets demanding continuous surface applications. Decorative, patterned, and handmade tiles occupy niche segments serving premium residential and boutique commercial projects where customization and artisanal quality justify higher pricing. The product type segmentation reflects broader industry evolution from commodity manufacturing toward specialized, high-value applications that resist competition from synthetic alternatives through unique aesthetic and performance characteristics.

By Application: Floors Dominate as Roofing Gains Momentum

Floor applications dominate with 63.25% market share in 2025, yet face intensifying competition from LVT and SPC alternatives that offer installation advantages and cost benefits in residential markets. Roofing applications represent the fastest-growing segment at 1.72% CAGR, benefiting from architectural trends toward ceramic façade systems that provide fire resistance, thermal performance, and aesthetic durability superior to traditional roofing materials. Wall applications maintain stable demand through bathroom and kitchen renovations, where ceramic tiles' moisture resistance and hygiene properties remain unmatched by alternative materials.

The application segmentation reveals strategic opportunities in non-traditional ceramic tile markets, particularly façade and exterior cladding, where thin-tile panels below 6 mm thickness enable lightweight installations previously impossible with conventional ceramic products. Roofing segment growth reflects building code evolution favoring fire-resistant materials and energy-efficient building envelopes, where ceramic tiles contribute to thermal mass and solar reflectance performance. Floor segment maturity necessitates differentiation through premium positioning, technical innovation, and design leadership rather than price competition with synthetic alternatives that increasingly match ceramic aesthetics at lower installed costs.

By End-User: Commercial Outpaces Residential in Value Terms

The residential segment holds 43.85% market share in 2025, serving renovation projects and new construction where ceramic tiles compete directly with LVT, SPC, and other flooring alternatives on cost and installation convenience. Commercial applications grow at 2.39% CAGR through 2031, driven by hospitality recovery, retail space modernization, and institutional projects requiring durability and maintenance efficiency that justify ceramic tiles' higher initial costs. Healthcare and educational facilities particularly value ceramic tiles' hygiene properties and long-term performance, while transport hubs demand slip resistance and heavy-traffic durability.

Commercial segment growth reflects ceramic tiles' competitive advantages in high-performance applications where synthetic alternatives cannot match durability, fire resistance, and maintenance characteristics essential for institutional and hospitality environments. Office and retail spaces increasingly specify large-format porcelain for design coherence and reduced maintenance requirements, while hospitality projects emphasize custom designs and premium aesthetics that differentiate properties in competitive markets. The end-user segmentation highlights ceramic tiles' evolution from residential commodity toward commercial specialty applications where technical performance and design flexibility command premium pricing despite synthetic alternative availability.

By Construction Type: Renovation Anchors Demand Stability

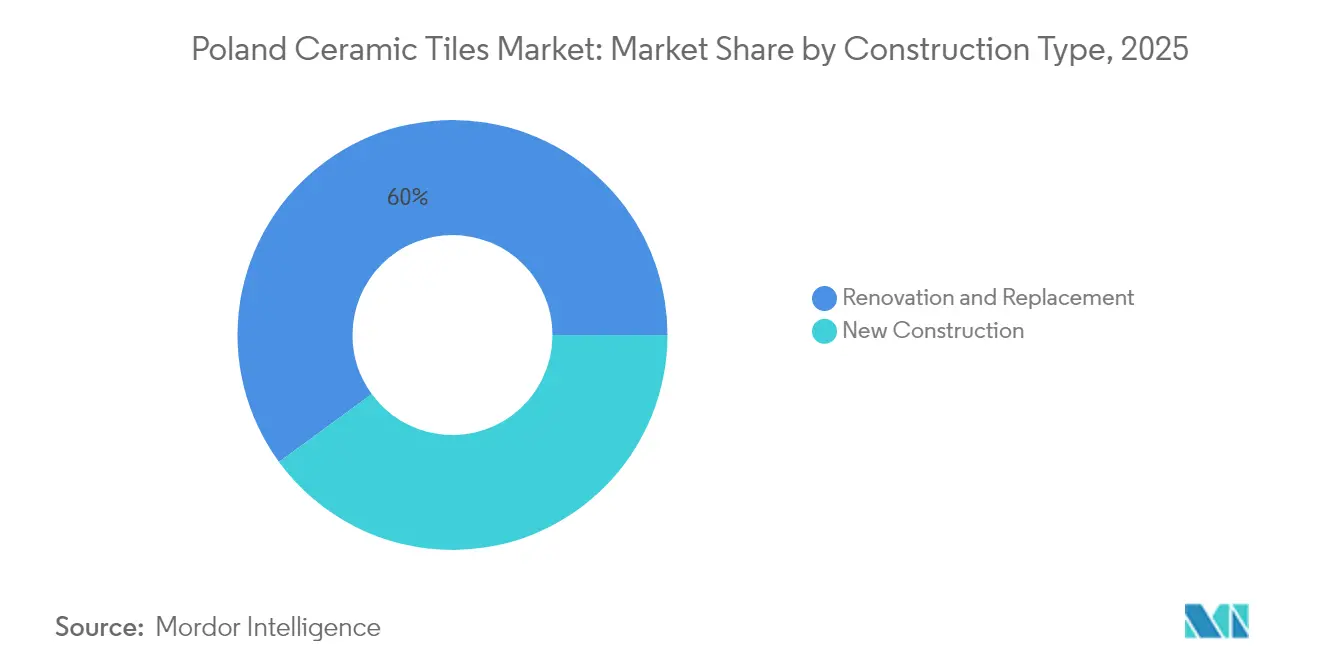

Renovation and replacement activities capture 60.05% market share in 2025, reflecting Poland's construction market maturation, where existing building upgrades generate more sustainable ceramic tile demand than volatile new construction cycles. New construction grows at a 2.06% CAGR through 2031, supported by infrastructure investments and housing shortage pressures, yet remains subject to economic cycles and financing availability that create demand volatility. The construction type segmentation reveals market stability benefits from renovation focus, as building maintenance and upgrade activities continue regardless of new construction fluctuations.

Government programs like "Czyste Powietrze" support renovation activities through energy efficiency subsidies that often include ceramic tile installations as components of comprehensive building upgrades. New construction segment growth benefits from EU infrastructure funding and housing initiatives, yet faces challenges from rising material costs, labor shortages, and interest rate pressures that delay project starts and reduce developer margins. The renovation focus aligns with sustainability trends, emphasizing building lifecycle extension over demolition and reconstruction, positioning ceramic tiles as durable solutions that support circular economy principles through longevity and recyclability.

By Distribution Channel: E-Commerce Rewrites the Go-to-Market Playbook

Home improvement and DIY stores maintain a 42.10% market share in 2025, leveraging established customer relationships and product display capabilities that enable tactile evaluation essential for ceramic tile selection. Online retail emerges as the fastest-growing channel at 4.18% CAGR, driven by digital natives' purchasing preferences and e-commerce platforms' ability to offer broader product selections than physical stores can economically maintain. Specialty tile and stone stores serve premium segments requiring expert consultation and customization services, while direct sales to contractors focus on commercial projects and bulk residential installations.

The distribution channel evolution reflects broader retail transformation, where digital platforms complement rather than replace physical touchpoints, as ceramic tiles require visual and tactile evaluation that online channels struggle to replicate effectively. Poland's DIY landscape encompasses 1,102 stores with domestic chain Mrówka leading at 352 locations, creating opportunities for digital platforms to aggregate fragmented demand while providing installation guidance and design tools that enhance purchase confidence. Online growth particularly benefits manufacturers seeking direct consumer relationships that bypass traditional distributor margins while enabling customization and on-demand production models impossible through conventional retail channels.

Geography Analysis

Central Poland anchors production and consumption, capturing 28.86% of 2025 revenue. Łódź’s dense cluster of kilns shortens last-mile shipping to Warsaw’s 3.2 million metro residents, ensuring 24-hour delivery cycles that big-box DIY chains require. The Poland ceramic tiles market share advantage is reinforced by rail links connecting plants to export terminals in Gdańsk and Gdynia, trimming logistics costs by 11% over truck routes. Western Poland benefits from German border proximity and automotive industry investments that support commercial construction demand, while Eastern Poland relies on EU development funding and agricultural modernization projects.

Southern Poland's market development focuses on industrial and mining region transformation, where ceramic tiles serve facility modernization and environmental remediation projects. The region's raw material availability supports local ceramic production, with building ceramics deposits totaling over 2 million cubic meters of resources across various voivodeships. Geographic market distribution reflects Poland's economic development patterns, where Central region manufacturing concentration creates cost advantages while peripheral regions offer growth opportunities through infrastructure development and EU funding programs. Regional variations in construction activity, income levels, and development priorities create distinct market characteristics requiring tailored product positioning and distribution strategies.

The geographic segmentation also reveals regulatory influence variations, as different voivodeships implement EU environmental standards and building codes at varying paces, affecting ceramic tile specifications and market opportunities. Northern Poland's coastal location creates unique requirements for salt-resistant and weather-durable ceramic solutions, while Southern Poland's industrial heritage demands products suitable for facility upgrades and environmental compliance projects. Eastern Poland's development lag creates opportunities for basic ceramic tile applications, while Western Poland's economic advancement supports premium product demand and architectural innovation adoption.

Competitive Landscape

The Poland ceramic tiles market exhibits moderate concentration, with domestic players maintaining competitive advantages through manufacturing scale, distribution networks, and local market knowledge. Ceramika Paradyż leads through technological innovation, operating 10 Durst digital printers and investing in large-format TRI-D sintered stone production capabilities that differentiate products in premium segments. Cersanit leverages financial resources through EUR 42 million (USD 43.7 million)EBRD financing for large-format tile manufacturing expansion, while Tubądzin Group and Opoczno compete through brand positioning and distribution channel optimization.

International players like RAK Ceramics, Porcelanosa Grupo, and Marazzi Group maintain market presence through premium positioning and specialized applications, yet face cost disadvantages compared to domestic manufacturers, benefiting from local raw material access and logistics efficiencies. Strategic patterns emphasize technological differentiation over price competition, with leading manufacturers investing in digital printing capabilities, large-format production equipment, and customization technologies that create barriers to entry for smaller competitors.

White-space opportunities emerge in thin-tile façade applications, sustainable production using recycled industrial waste, and AI-powered design customization that responds to individual customer preferences rather than mass-market averages. The competitive landscape benefits from EU trade defense measures, including renewed anti-dumping duties on ceramic tile imports from China, India, and Turkey, which protect domestic manufacturers from unfair pricing pressures while maintaining market stability. Technology adoption focuses on energy efficiency improvements and circular economy principles, with research demonstrating 25-35% cost reductions through mining waste utilization in ceramic tile production.

Poland Ceramic Tiles Industry Leaders

Ceramika Paradyż

Cersanit S.A.

Tubądzin Group

Cerrad Sp. z o.o.

Opoczno S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: One Equity Partners acquired Italy’s Gruppo Siti B&T, promising next-gen glazing machinery supply to Polish tile makers.

- March 2024: LB has received a new order from the Polish ceramic tile manufacturer Ceramika Paradyz to supply a new technological tower equipped with an Easy Color Boost colouring system.

- March 2024: Ceramika Paradyż launched a new plant for large-format tile production using Sacmi's Continua+ technology and added two new Sacmi pressing lines at its Tomaszów Mazowiecki facility, expanding manufacturing capacity for premium segment applications.

Poland Ceramic Tiles Market Report Scope

Ceramic Tiles are made up of sand, natural products, and clays, and once it is molded into a shape, then they are fired into a kiln. Ceramic tiles are durable, resistant to water, moisture, and fire, and cheap compared to other flooring products. This report aims to provide a detailed analysis of the Poland Ceramic Tiles market. The report focuses on the market dynamics, emerging trends in the segments, and insights into various product and application types. Also, it analyzes the key players and competitive landscape. Poland Ceramic Tiles Market is segmented by product (Glazed, Porcelain, Scratch Free, and Other Products), by application (Floor Tiles, Wall Tiles, and Other Applications), by construction type (New Construction, and Replacement and Renovation), and by end-user (Residential and Commercial). The report offers market size and values in (USD million) during the forecast years for the above segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Northern Poland |

| Central Poland |

| Eastern Poland |

| Western Poland |

| Southern Poland |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Northern Poland | |

| Central Poland | ||

| Eastern Poland | ||

| Western Poland | ||

| Southern Poland | ||

Key Questions Answered in the Report

What is the projected value of the Poland ceramic tiles market in 2031?

The market is forecast to reach USD 1.18 billion by 2031.

Which segment is growing fastest within Polish tile applications?

Roofing and façade systems are expanding at a 1.72% CAGR thanks to thin-tile adoption for ventilated façades.

How large is porcelain’s share in the Poland ceramic tiles market?

Porcelain captured 48.12% of 2025 revenue, maintaining leadership among product types.

Why are natural-gas prices a concern for Polish tile makers?

Gas supplies up to 70% of firing energy, and recent price spikes cut factory utilization to 57%, pressuring margins.

Which sales channel is seeing the quickest growth?

Online retail is rising at a 4.18% CAGR as digital configurators and direct-to-consumer models gain traction.

Page last updated on: