Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

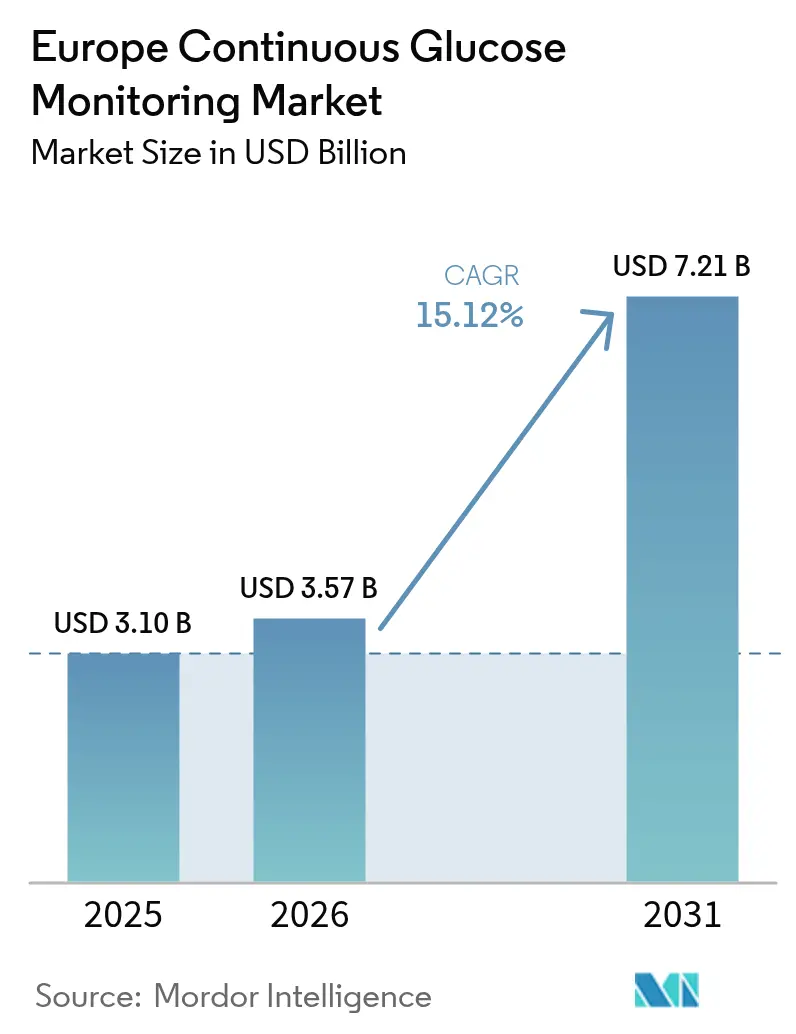

| Base Year Market Size (2025) | USD 3.10 Billion |

| Market Size (2026) | USD 3.57 Billion |

| Market Size (2031) | USD 7.21 Billion |

| Growth Rate (2026 - 2031) | 15.12% CAGR |

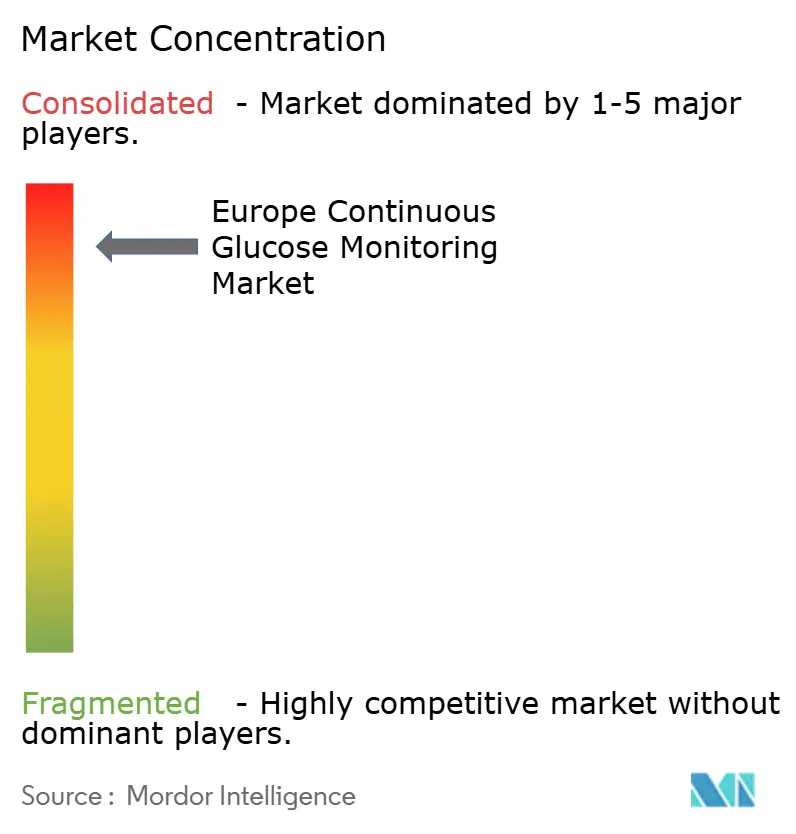

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Continuous Glucose Monitoring Market Analysis by Mordor Intelligence

The Europe continuous glucose monitoring market size is expected to grow from USD 3.10 billion in 2025 to USD 3.57 billion in 2026 and is forecast to reach USD 7.21 billion by 2031 at 15.12% CAGR over 2026-2031. The expansion reflects Europe-wide reimbursement reforms, accelerating telehealth integration, and the EU-MDR rule set that harmonizes device approvals. Germany, France, and the United Kingdom remain the anchor demand centers as statutory insurers broaden coverage across Type 1 and insulin-treated Type 2 diabetes. Manufacturing localization—most notably Dexcom’s EUR 300 million Irish plant and Abbott’s enlarged Dublin hub—reduces import exposure and positions the region as a sensor production base. Competitive intensity is moderate: Abbott, Dexcom, and Medtronic still control close to 70% of revenue, yet Senseonics and i-SENS secure fresh CE Marks that introduce longer-wear and lower-cost options.

Key Report Takeaways

- By component, sensors captured 81.74% of Europe continuous glucose monitoring market share in 2025; transmitters are projected to grow at a 14.40% CAGR through 2031.

- By end user, home/personal use accounted for 71.68% of the Europe continuous glucose monitoring market size in 2025, while hospital/clinic settings are set to expand at a 15.45% CAGR to 2031.

- By demography, adult users represented 62.10% revenue in 2025, whereas pediatric applications are forecast to post the fastest 15.55% CAGR through 2031.

- By geography, Germany led with 22.30% revenue share in 2025; the country is also projected to post the region’s highest 16.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Continuous Glucose Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diabetes Prevalence in Europe | +2.8% | Germany, France, UK (highest impact); rest of Europe | Long term (≥4 years) |

| Expansion of Reimbursement for CGM Devices | +3.2% | Germany, France, UK; spillover to Italy & Spain | Medium term (2-4 years) |

| Advances in User-Friendly Wearable Sensors | +2.1% | EU-wide; R&D hubs in Ireland & Switzerland | Medium term (2-4 years) |

| Telehealth-Driven Demand for Remote Monitoring | +1.9% | EU-wide, supported by post-COVID digital health policies | Short term (≤2 years) |

| National EHR Integration of CGM Data | +1.7% | Germany, France, UK, Netherlands leading adoption | Long term (≥4 years) |

| Manufacturing Automation Lowering Sensor Cost | +1.4% | Production hubs in Ireland, Germany, Switzerland | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes Prevalence in Europe

Europe's continuous glucose monitoring market momentum is anchored by 65.6 million adults currently living with diabetes, a figure projected to climb to 72.4 million by 2050[1]International Diabetes Federation, “IDF Diabetes Atlas 11th Edition,” idf.org . Younger onset of Type 2 diabetes in Eastern Europe widens the addressable patient pool beyond the historical Type 1 focus. German cohort studies show HbA1c improvements to 7.13% among CGM users versus 7.66% for non-users, strengthening physician confidence. Endocrinologists increasingly prescribe CGM at diagnosis rather than after finger-stick failure, embedding the technology as first-line management. This epidemiological tailwind sustains the Europe continuous glucose monitoring market even during economic slowdowns.

Expansion of Reimbursement for CGM Devices

Statutory coverage in Germany since 2016, France’s broadened Assurance Maladie listing in 2024, and NHS England’s FreeStyle Libre program collectively remove upfront cost barriers. Reimbursed users scan glucose 16.3 times per day compared with 4–6 finger-stick tests. Predictable payouts foster manufacturer pipeline investment and scale production. Italy and Spain mirror the policy path through regional tenders, creating a domino effect across Southern Europe. The reimbursement wave underpins double-digit revenue visibility for the Europe continuous glucose monitoring market through 2030.

Advances in User-Friendly Wearable Sensors

Calibration-free designs, smartphone pairing, and AI-powered trend warnings increase adherence. Roche’s machine-learning CGM obtained CE Mark in 2024, offering automated dosing suggestions[2]Roche Holding AG, “Roche Receives CE Mark for New CGM System,” roche.com . Medtronic’s Simplera Sync extends wear to 7 days without finger-stick calibration. Dexcom and Abbott target 100 million annual sensor output from Irish lines by 2027, aiming to cut unit cost by 25-30%. These innovations strengthen patient loyalty and attract first-time adopters, solidifying Europe's continuous glucose monitoring market footprint.

Telehealth-Driven Demand for Remote Monitoring

EU health systems invested EUR 2.3 billion in digital platforms during 2024, embedding CGM feeds into clinician dashboards. German diabetes centers report 40% fewer emergency visits among tele-monitored patients. Remote review saves clinician time and hospitals’ operational budgets, accelerating contract renewals. National EHR programs in Germany, France, and the Netherlands standardize CGM data uploads, reinforcing the Europe continuous glucose monitoring market’s digital-first evolution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device Cost and Partial Reimbursement Gaps | -2.1% | Eastern Europe; Southern Italy & Spain | Medium term (2-4 years) |

| Sensor Accuracy / Calibration Concerns | -1.5% | EU-wide hospitals & clinics | Short term (≤2 years) |

| GLP-1 Drugs Curbing Monitoring Frequency | -1.8% | Germany, France, UK with high GLP-1 adoption | Short term (≤2 years) |

| EU-MDR Uncertainty for Next-Gen Non-Invasive CGM | -1.2% | EU-wide innovation pipeline | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Device Cost and Partial Reimbursement Gaps

Income disparities across Eastern Europe keep patient co-pays high. Some Italian southern regions still reimburse only 70% of sensor cost, stalling uptake. Local advocacy groups lobby for full coverage, but budget constraints prolong negotiations. Manufacturers deploy patient-assistance vouchers yet struggle to close affordability gaps quickly. These pockets temper volume growth within the Europe continuous glucose monitoring market until broader funding parity is secured.

Sensor Accuracy and Calibration Concerns

Hospital adoption lags due to worries about accuracy during rapid glycemic swings. Only 16.7% of UK trusts have formal inpatient CGM guidelines. Clinical teams cite dose-critical decisions and interference risks. Training modules and new algorithms that self-adjust for perfusion changes are entering trials. Until results convince institutional committees, the Europe continuous glucose monitoring market faces speed bumps in the acute-care segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Sensors Drive Market Expansion

Sensors accounted for 81.74% of 2025 revenue within the Europe continuous glucose monitoring market, reflecting their consumable nature and 14-day replacement cycles. Segment growth is forecast at a 15.45% CAGR through 2031 as extended-wear versions such as Senseonics’ 6-month Eversense E3, approved in 2024, gain traction. Automated Irish production lines from Dexcom and Abbott are expected to lift annual capacity to 100 million units by 2027, pushing unit cost below EUR 30 and spurring use in lower-income regions. Receivers and transmitters held 18.26% share but shift toward smartphone apps is gradually eroding dedicated hardware sales. Software subscriptions that interpret CGM data emerge as a fresh margin pool, diversifying revenue beyond physical sensors. Interoperability standards embedded in the EU-MDR encourage app-centered ecosystems and third-party analytics, a trend that deepens platform lock-in for the Europe continuous glucose monitoring market.

By End User: Home Personal Use Dominates

Home/personal users represented 71.68% of the Europe continuous glucose monitoring market share in 2025 and are projected to sustain a 14.95% CAGR through 2031. The shift reflects patient desire for autonomy, real-time smartphone alerts, and telemedicine consults that cut clinic travel. Hospitals and clinics, with 28.32% share, nevertheless show a 15.45% CAGR as infection-control protocols adopted during COVID-19 normalize sensor use in wards. UK data show a 23% reduction in inpatient hypoglycemia where CGM is standard. Capital budgets now favor CGM over intermittent finger-stick monitors because nursing workload drops and length of stay decreases. Workflow integration modules added to electronic medical records mitigate earlier calibration concerns and advance hospital penetration across the Europe continuous glucose monitoring market.

By Demography: Pediatric Segment Shows Fastest Growth

Adults comprise 62.10% of 2025 revenue, but pediatric users—holding 37.90%—clock the fastest 15.55% CAGR through 2031. Updated ISPAD guidelines mandate CGM as standard for children, and reimbursement regimes in Germany cover 95% of pediatric costs. Adoption exceeds 85% among newly diagnosed children, compared with 60% among adults, underscoring the generational tech embrace that will shape long-run demand. Rising adolescent Type 2 incidence in Eastern Europe widens the pool further. Parental demand for remote alerts and school-day oversight adds a use-case advantage that finger-stick meters cannot match. Device makers tailor adhesive strength, app graphics, and tiny gauge wires to safeguard sensitive skin. Pediatric-centric user interfaces encourage self-management earlier in life, anchoring lifetime loyalty within the Europe continuous glucose monitoring market. As these children age into adulthood, replacement cycles lengthen yet unit volumes stay high, ensuring a durable growth pillar for the Europe continuous glucose monitoring market.

Geography Analysis

Germany generated 22.30% of 2025 revenue in the Europe continuous glucose monitoring market and is forecast to post the region’s highest 16.75% CAGR through 2031. The country’s 1,000-plus diabetes centers, generous statutory coverage, and rapid telehealth maturity position it as the innovation proving ground. France followed at 17.42% share and a 16.05% CAGR as Assurance Maladie broadened indications and domestic majors such as Sanofi championed national procurement alliances. The United Kingdom held a 16.10% stake; NHS coverage for FreeStyle Libre offsets Brexit-related regulatory divergence, maintaining steady device volumes.

Italy accounted for 12.52% of Europe's continuous glucose monitoring market size in 2025 and should compound at 14.95% as regional funding gaps shrink. Spain’s 9.95% share and 13.35% CAGR reflect decentralized reimbursement that is gradually synchronizing with national diabetes plans. Russia captured a 9.20% share; sanctions and currency pressure trim growth to 11.40% yet local assembly projects could redirect supply lines.

The rest of Europe comprised 12.51% revenue with a 13.85% CAGR. Poland, the Czech Republic, and Hungary demonstrate outsized momentum as EU cohesion funds underwrite digital health rollouts. Nordic countries, although smaller in population, post near-universal sensor usage due to comprehensive social healthcare and digital record parity. Collectively, rising penetration across Eastern states offsets mature base effects in Western Europe, reinforcing the long-term resilience of the Europe continuous glucose monitoring market.

Regulatory Landscape

Continuous glucose monitoring (CGM) systems marketed across the EU are regulated under the Medical Device Regulation, Regulation (EU) 2017/745 (MDR), in full application since 26 May 2021, with conformity assessment performed by designated Notified Bodies before CE marking. Software elements connected to CGM, such as mobile apps and decision-support that provide insulin dose recommendations or interface with insulin delivery, are assessed under MDCG medical device software qualification guidance (for example, MDCG 2019-11). Depending on function, these can be placed into higher-risk classes, which increases the clinical evidence requirements and post-market obligations.

In June 2026, the European Commission published implementing decisions in the Official Journal updating the lists of harmonised standards for MDR and IVDR. Manufacturers are expected to maintain alignment with these standards to preserve presumption of conformity as the harmonised standards evolve. Compliance operations are also shaped by the phased rollout of EUDAMED modules (including certificates, clinical investigations, and vigilance), with further milestones extending through 2027, which increases the importance of strengthening data submission, vigilance workflows, and traceability to support ongoing access and renewals.

Value Chain Analysis

The Europe CGM value chain runs from specialized raw materials and microelectronics through sensor manufacturing and assembly, then into national reimbursement-driven distribution and patient support. Upstream inputs include enzyme chemistries, membranes, adhesive systems, and ASICs, and the chain remains import-dependent for many critical components. Final assembly and scaling is concentrated in Ireland (notably Abbott and Dexcom), while Germany and Switzerland focus more on precision and stabilization work.

Midstream, MDR (EU 2017/745) compliance, clinical documentation, and Notified Body capacity shape time-to-market and change control for both hardware and software updates. Downstream, the route to patient varies by country: Germany's statutory health insurance pathways favor pharmacy and mail-order fulfillment under defined coverage rules, while other markets rely on mixes of hospital procurement, retail pharmacy, and direct-to-consumer models linked to digital onboarding and cloud monitoring. Regional logistics hubs, including the Netherlands for pan-European distribution, support inventory positioning and rapid dispatch across member states as manufacturers balance lead times, cold-chain or handling requirements, and reimbursement documentation needs.

Competitive Landscape

The Europe continuous glucose monitoring market is moderately consolidated, with Abbott, Dexcom, and Medtronic jointly dominating the market. Abbott leverages first-mover status in flash monitoring and the widest payer listings; its Libre ecosystem dominates pharmacy channels. Medtronic integrates its Simplera Sync sensor with the MiniMed 780G closed-loop, offering end-to-end insulin automation[3]Medtronic plc, “MiniMed 780G Launches in Europe,” medtronic.com .

Roche re-enters with an AI-enabled predictor that differentiates on software rather than hardware, while smaller European startups target non-invasive photonic sensing but face EU-MDR evidence hurdles. As smartphone interoperability standardizes data pipes, profitable differentiation pivots toward analytics subscriptions, predictive alerts, and insurer-linked adherence dashboards. Established leaders invest in cloud platforms to defend their share, yet nimble software players partner with hardware incumbents, spreading value capture. These converging strategies sustain healthy rivalry and product cadence, ensuring the Europe continuous glucose monitoring market remains technologically vibrant and customer-centric.

Europe Continuous Glucose Monitoring Industry Leaders

Medtronic

Dexcom Inc.

Abbott Laboratories

Senseonics Holdings Inc.

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term whitespace in Europe sits at the intersection of reimbursement expansion and health technology assessment pathways for broader Type 2 populations, particularly insulin-dependent Type 2 diabetes outside the most mature coverage markets. In May 2026, Ireland's Health Service Executive requested a HIQA assessment on the cost-effectiveness of expanding CGM access for all insulin-dependent Type 2 patients. The payer and HTA decision process directly gates additional addressable users even when clinical pull exists. In parallel, national EHR integration and telehealth workflows create opportunity for vendors to compete on analytics, clinician dashboards, and adherence programs rather than only on sensor hardware.

Product differentiation and standards alignment also remain tangible opportunity as the EU market absorbs longer-wear and multi-analyte monitoring alongside tighter evidence expectations under MDR. In February 2026, IDF Europe called for harmonized quality and performance standards for CGM devices, and this theme also appeared in 2026 European Parliament scrutiny around transparency of clinical performance data, reflecting demand for clearer, comparable performance disclosures. On the supply side, manufacturing scale-up in Ireland supports availability and cost-down initiatives: Abbott opened a 30,000-square-meter FreeStyle Libre manufacturing facility in Kilkenny in November 2024 and reported plans in January 2026 to pursue an expansion, while Dexcom opened its Athenry, Ireland manufacturing and office facility in April 2026, strengthening regional capacity for faster launches and broader payer tenders.

Recent Industry Developments

- June 2026: Medtronic began the Europe commercial rollout of its Instinct and Instinct Go sensors, manufactured by Abbott, for use with MiniMed systems including MiniMed 780G and MiniMed Go. The sensors broaden Medtronic's options within its insulin-delivery ecosystem, leveraging Abbott's sensor manufacturing scale to support wider availability across European markets.

- May 2026: Abbott secured CE Mark for Libre Duo and Libre Duo 10 Day, positioned as the first dual glucose-ketone sensing sensors for diabetes management. This expansion enables new clinical workflows where ketone awareness matters and supports broader payer and hospital adoption.

- April 2026: Dexcom opened its Athenry, Ireland manufacturing and office facility, expanding regional capacity for CGM device production. The new site accelerates European market access for faster launches and enhanced support across Ireland, the UK, and mainland Europe.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues generated in Europe from continuous glucose monitoring systems used to track glucose levels over time for diabetes management, including the core device set used in routine monitoring.

Scope exclusions: It excludes traditional blood glucose meters and test strips, along with broader diabetes care items such as insulin delivery devices and diabetes drugs.

Segmentation Overview

- By Component

- Sensors

- Transmitters

- Receivers

- By End User

- Hospitals / Clinics

- Home / Personal

- By Demography

- Adult

- Paediatric

- By Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial demand map and pricing guardrails for Europe, before assumptions were pressure-tested in fieldwork. We relied on public health statistics and policy signals such as International Diabetes Federation updates, OECD health indicators, Eurostat datasets, and national health system publications (for example reimbursement bulletins and tender notices). These inputs helped clarify where patient access is expanding.

To keep the model grounded in actual product availability and usage rules, we also reviewed regulatory and safety disclosures such as EMA resources and national competent authority notices, along with peer-reviewed clinical literature on CGM adoption and persistence. Company filings, earnings commentary, and investor presentations were used to sense-check revenue mix and sensor replacement patterns. A paid subscription covering company financials and patent databases supported cross-checks on product pipelines and addressable use cases. These sources are illustrative and not exhaustive, and many other public references were used for data collection, validation, and clarification during the research process.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with stakeholders across the CGM value chain, including device distributors, healthcare providers, payers, and diabetes educators, followed by select follow-ups where assumptions did not align. Since Europe is not a single reimbursement market, we covered major country clusters and then reconciled differences in coverage criteria, sensor supply cadence, and pricing corridors to make the totals comparable.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 21% | |

| Mid tier: 53% | Functional/Unit leaders: 34% | |

| Smaller Players: 21% | Managers: 45% |

Market-Sizing & Forecasting

Sizing started from a top-down build where the treated diabetes pool in Europe was reconstructed by country, and then filtered through CGM eligibility and uptake, before value was computed using typical sensor usage and durable replacement timing. To keep the totals realistic, selective bottom-up approximations were used, such as rolling up a sample of supplier revenues by geography and running channel checks on average selling prices, which were then used to adjust outliers.

Key inputs included diagnosed diabetes prevalence and treated population, reimbursement coverage breadth by country, CGM penetration by diabetes type, sensor change frequency, durable replacement cycles, and price corridors observed across public tenders and interview feedback. When a country had limited public price points, a proxy corridor was applied using nearby markets with similar reimbursement rules, and the gap was flagged for extra expert validation.

For forecasting, scenario analysis was used because policy changes and coverage expansions can shift adoption in steps rather than in a smooth line. Growth drivers such as broader reimbursement, rising CGM use in type 2 diabetes, and product refresh cycles were translated into country-level adoption curves, and then consolidated to the Europe total after consistency checks.

Data Validation & Update Cycle

Model outputs were cross-checked against independent signals such as public reimbursement activity, country-level diabetes burden indicators, and observed pricing bands, and then variances were reviewed in multiple analyst passes before sign-off. If a figure moved outside expected ranges, respondents were re-contacted and assumptions were revisited until the driver could be clearly explained.

The report is refreshed annually, and interim updates are made when material events occur such as a major reimbursement expansion, a regulatory change, or a meaningful pricing shift. Before delivery, a final analyst pass is completed so the numbers reflect the latest available inputs and clarified assumptions.

Mordor Intelligence's Europe Continuous Glucose Monitoring Market Size Compared Against Other Published Estimates

Published estimates for Europe CGM do not always match because the counted items and the timing of the price and adoption inputs are not consistent. Differences also come from how each publisher treats country reimbursement rules, which can change the eligible population and the pace of uptake.

Blood glucose meters and test strips are kept outside Mordor Intelligence's scope, which reduces the total versus estimates that blend CGM with broader glucose monitoring devices. Gaps can also show up when a study uses a single Europe-level ASP or a single penetration rate, since Germany, the United Kingdom, and Southern Europe can move differently based on coverage criteria, tender pricing, and sensor refill cadence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.10 B (2025) | |

| Regional Consultancy A | USD 3.92 B (2024) | Uses an earlier base year and, based on the published scope language, can blend wider glucose testing site frameworks and device definitions that are not always limited to the same CGM-only revenue set. |

| Trade Journal B | USD 3.00 B (2024) | Reports a Europe figure inside a global view with limited detail on country reimbursement filters, which can understate demand in markets where coverage recently expanded and sensor replacement behavior is higher. |

The spread in values mainly tracks back to product inclusion rules and how country-by-country access and pricing are translated into a single Europe number. By tying the model to treated population, eligibility, sensor consumption patterns, and cross-checks from fieldwork, we keep the final estimate easy to explain and repeat when assumptions are updated.

Key Questions Answered in the Report

What revenue level are continuous glucose monitoring devices in Europe expected to reach by 2031?

Sales are forecast to climb to USD 7,211.49 million by 2031, more than doubling the 2026 total.

How quickly is demand for continuous glucose monitoring growing across Europe?

Annual revenue is projected to rise at a 15.12% CAGR between 2026 and 2031, reflecting strong telehealth uptake and wider reimbursement.

Which country currently leads adoption of continuous glucose monitoring devices in Europe?

Germany holds the top position with 22.30% share in 2025 and is set to post the region’s fastest 16.75% CAGR through 2031.

Why are pediatric users the fastest-growing segment for CGM in Europe?

Updated pediatric guidelines, near-universal reimbursement in Germany, and 85% uptake among newly diagnosed children drive a 15.55% CAGR for this group.

How do reimbursement policies influence CGM penetration across European health systems?

Expanded statutory coverage in Germany, France, and the UK removes upfront cost barriers, prompting daily scan rates that far exceed finger-stick testing and fueling sustained device demand.

What effect could widespread GLP-1 therapy adoption have on CGM device sales?

Broader use of GLP-1 receptor agonists may lower monitoring frequency among Type 2 patients, creating a modest headwind that subtracts an estimated 1.8 percentage points from growth.

Page last updated on: