Extract, Transform, And Load (ETL) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

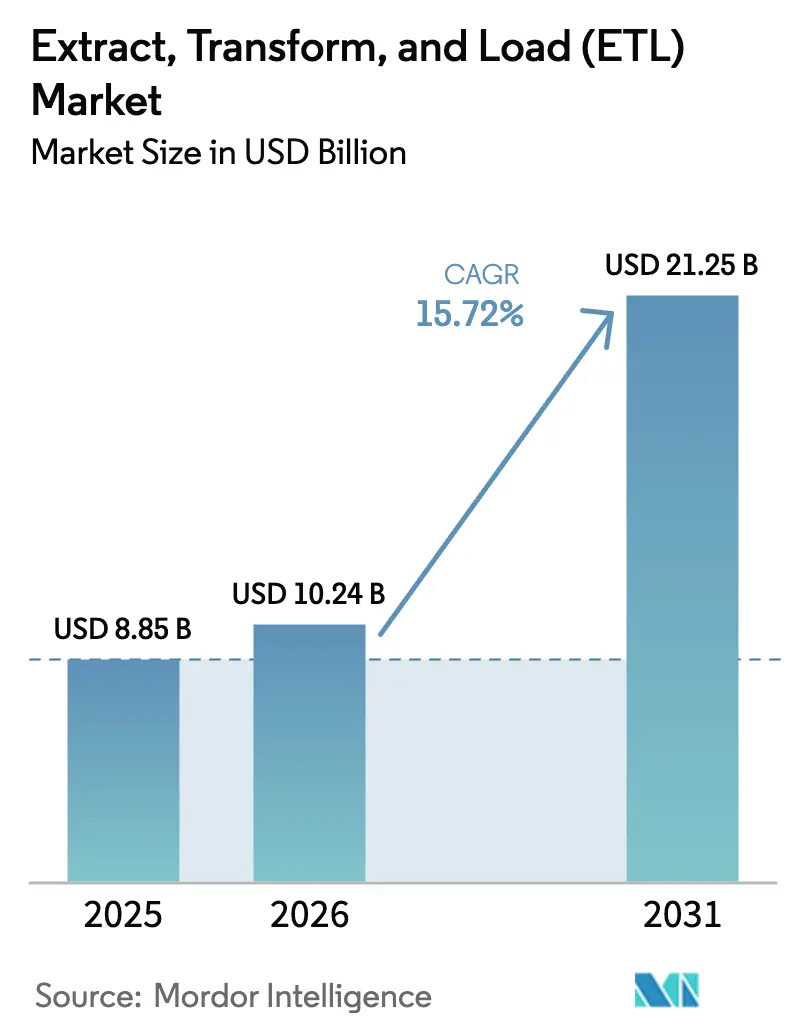

| Market Size (2026) | USD 10.24 Billion |

| Market Size (2031) | USD 21.25 Billion |

| Growth Rate (2026 - 2031) | 15.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Extract, Transform, And Load (ETL) Market Analysis by Mordor Intelligence

The extract, transform, and load (ETL) market size is expected to grow from USD 8.85 billion in 2025 to USD 10.24 billion in 2026 and is forecast to reach USD 21.25 billion by 2031 at 15.72% CAGR over 2026-2031. Cloud-native architectures, surging unstructured data volumes, and no-code integration tools are expanding the addressable customer base. Software components retain dominance as enterprises consolidate around unified data-integration suites, while usage-based pricing and serverless execution models shift cost structures toward operating expenditure. Cloud deployments remain the preferred infrastructure choice because hyperscalers deliver elastic compute, embedded transformation engines, and growing data-governance toolkits. Large enterprises still provide the revenue foundation, but small and medium enterprises (SMEs) now drive incremental growth through democratized tooling. Banks, insurers, and capital-markets firms sustain the largest demand pool, yet healthcare and life-sciences organizations represent the fastest-growing vertical as precision-medicine and electronic health-record initiatives gain momentum.

Key Report Takeaways

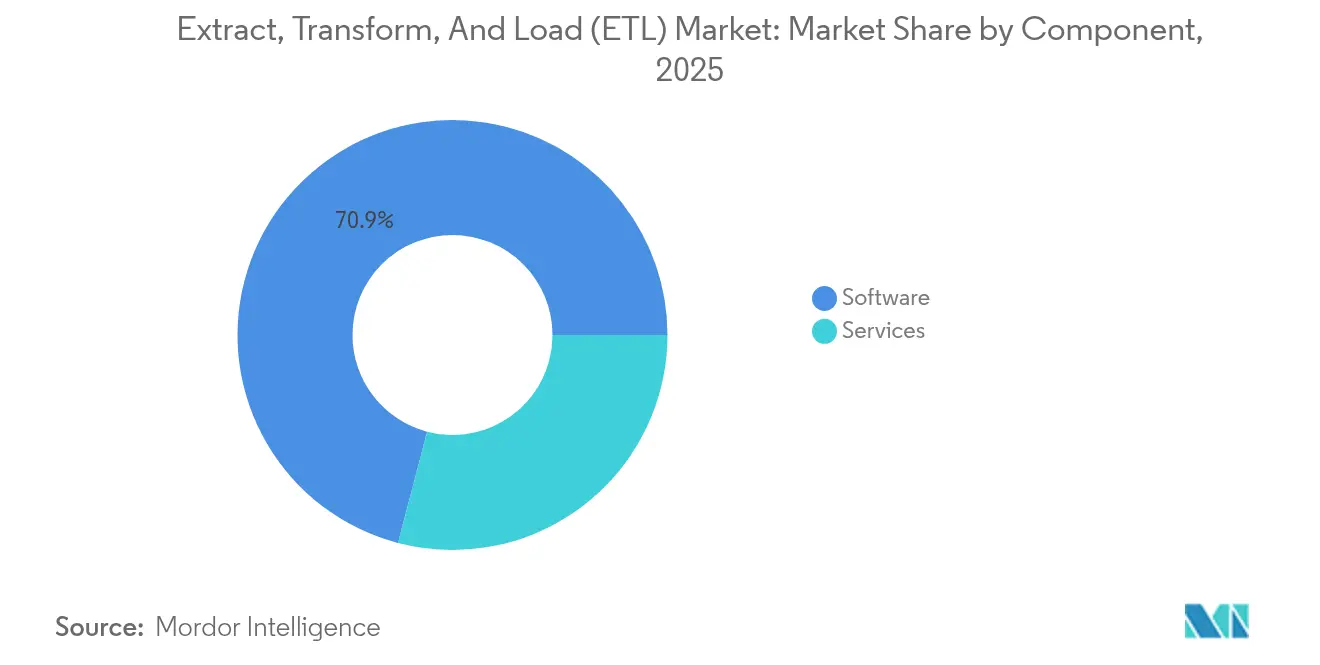

- By component, software captured 70.92% of extract, transform, and load (ETL) market share in 2025; services are projected to expand at a 15.45% CAGR through 2031.

- By deployment model, cloud solutions accounted for 66.35% of the extract, transform, and load (ETL) market size in 2025 and will grow at a 17.42% CAGR to 2031.

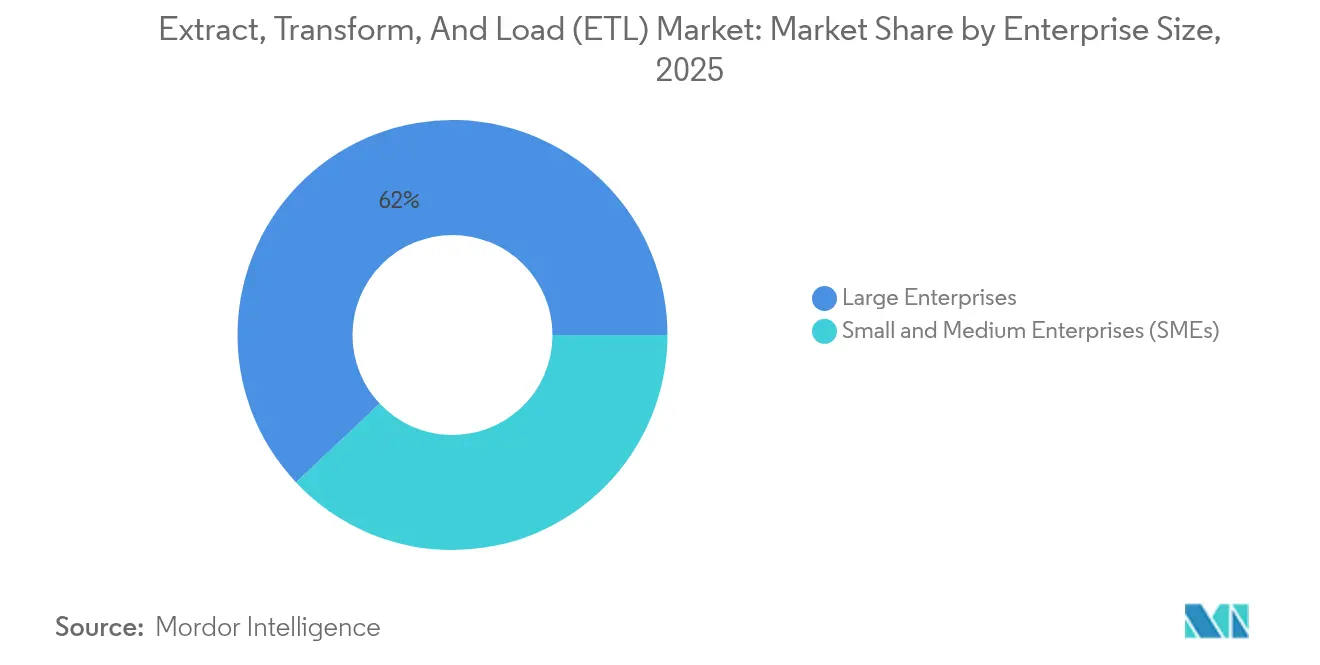

- By enterprise size, SMEs are expected to post the fastest 18.48% CAGR, while large enterprises maintained 62.03% revenue share in 2025.

- By end-user industry, BFSI led with 22.86% revenue in 2025, whereas healthcare and life sciences is forecast to grow at a 17.55% CAGR to 2031.

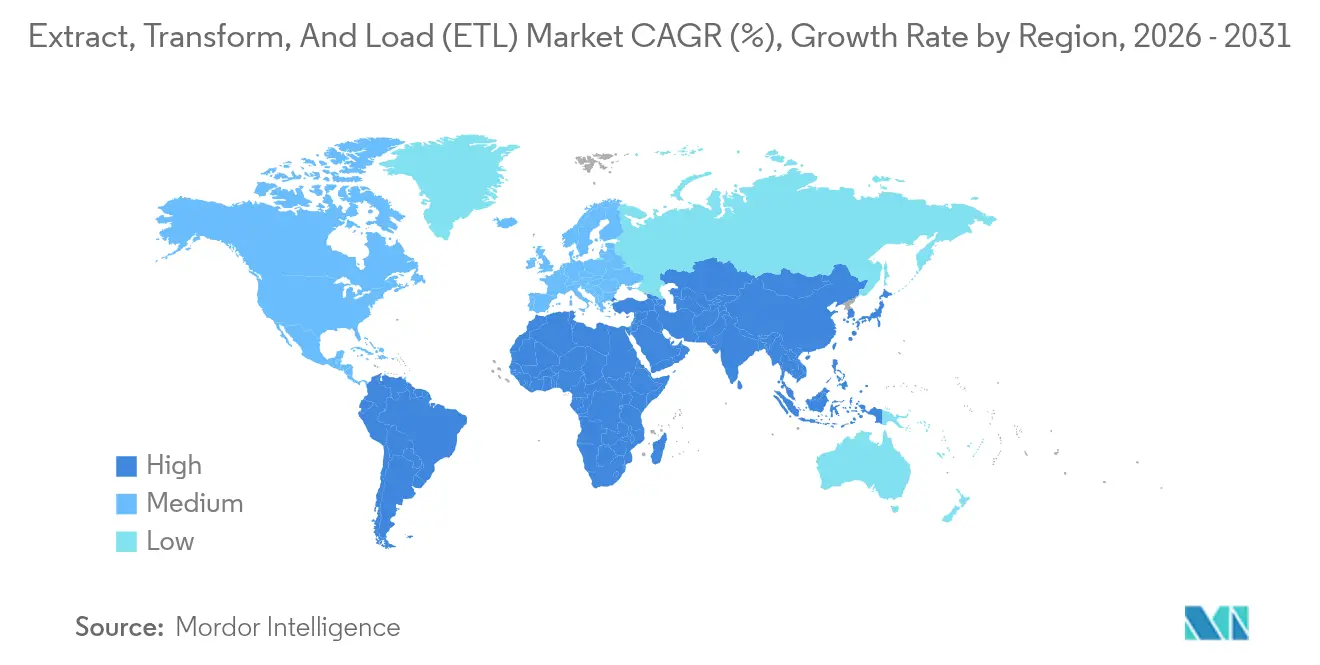

- By geography, North America commanded 39.32% extract, transform, and load (ETL) market size in 2025, while Asia-Pacific is on track for a 17.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Extract, Transform, And Load (ETL) Market Trends and Insights

Driver Impact Analyis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated cloud-native application adoption | +3.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| Explosion of unstructured and semi-structured data volumes | +2.8% | Global; core momentum in Asia-Pacific | Long term (≥ 4 years) |

| Democratization of no/low-code data-integration tooling | +2.1% | North America and Europe, expanding in Asia-Pacific | Short term (≤ 2 years) |

| Vendor shift toward usage-based pricing models | +1.9% | Global | Medium term (2-4 years) |

| Sustainability-driven data-estate rationalization | +1.4% | Europe first, North America following | Long term (≥ 4 years) |

| Gen-AI demand for proprietary clean-room datasets | +2.6% | North America and Europe, selected Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Cloud-Native Application Adoption

Enterprises are dismantling monolithic pipelines and embracing microservices so each data-processing step scales independently and recovers faster from failures. Financial institutions that once kept workloads on-premises now pilot serverless ETL jobs inside secure virtual-private-cloud footprints. Amazon Web Services promotes a “zero-ETL” future by embedding transformation directly in Amazon Redshift, reducing latency between ingestion and analytics [1]Amazon Web Services, “Introducing Zero-ETL with Amazon Redshift,” aws.amazon.com. Consumption-based billing aligns cost with data processed, and Informatica’s cloud annual recurring revenue rose 37% after shifting to pay-as-you-go tiers. Multi-cloud compatibility also guides buying decisions so data teams avoid hyperscaler lock-in.

Explosion of Unstructured and Semi-Structured Data Volumes

IoT telemetry, social feeds, and document repositories now eclipse traditional relational data sets. Healthcare providers blend medical imaging, genomics, and wearable telemetry into patient-360 records, demanding sophisticated normalization pipelines. As volumes grow, many firms flip to ELT patterns that exploit cloud-warehouse compute rather than dedicated ETL engines. Vendors answer with push-down SQL transformations, GPU-accelerated parsing, and schema-on-read features that streamline load times. Specialized suppliers emerge for video, log, and graph data, pushing general-purpose platforms to widen connector catalogs.

Democratization of No/Low-Code Data-Integration Tooling

Visual drag-and-drop canvases now let analysts construct pipelines without Python or SQL. SMEs seize this capability to bypass scarce data engineers, helping the segment log an 18.7% CAGR. Matillion and Fivetran ship pre-configured connectors that deploy in minutes, broadening the user population [2]Matillion, “No-Code Data Integration for the Cloud,” matillion.com. Tiered SKUs begin at single-user seats and scale to enterprise unlimited rights, reducing entry barriers. Governance teams, however, warn that unchecked tool proliferation fragments lineage tracking and inflates licensing costs.

Gen-AI Demand for Proprietary Clean-Room Datasets

Generative AI projects require privacy-preserving corpora sourced from internal systems. Firms build clean rooms to tokenize personal identifiers before model training. Banks deploy ETL jobs that synthesize statistically faithful yet anonymized customer records, safeguarding compliance with financial privacy statutes. Informatica’s CLAIRE GPT embeds natural-language data quality rules that detect policy breaches in real time. The shift lifts demand for lineage graphing, masking, and differential-privacy algorithms integrated into ETL workflows.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating hyperscaler egress fees | -2.1% | Global, especially multi-cloud deployments | Short term (≤ 2 years) |

| Data-sovereignty and residency compliance hurdles | -1.8% | Europe leading, expanding globally | Medium term (2-4 years) |

| Acute shortage of data-engineering talent | -1.6% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Tool sprawl causing integration-spend cannibalization | -1.3% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Hyperscaler Egress Fees

Cross-cloud data transfers can consume 15-25% of analytics budgets, forcing architecture teams to localize compute where data resides. Databricks responded with Serverless Egress Control so customers measure and cap costs in near real time. Many organizations now consolidate workloads inside a single cloud, shrinking addressable revenue for independent multi-cloud ETL vendors.

Acute Shortage of Data-Engineering Talent

Global demand for data engineers will rise from 2.0 million to 2.3 million by 2025, yet universities and bootcamps cannot match the pace. Scarcity inflates wages and prolongs project timelines, prompting enterprises to outsource routine pipeline maintenance to managed-service providers. Platform vendors inject AI-driven auto-mapping and template libraries to cut manual coding tasks, easing pressure on limited staff.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Consolidation Reduces Tool Complexity

Software accounted for 70.92% of extract, transform, and load (ETL) market revenue in 2025 and is projected to grow 15.98% annually through 2031. Organizations prefer unified suites that bundle extraction, transformation, data quality, and monitoring because they simplify procurement and lower integration risk. Informatica’s Intelligent Data Management Cloud illustrates how converged tooling removes the need for separate point solutions. Services, which held 29.08%, remain critical during complex regulated deployments but face slower growth as self-service automation matures.

Standardized software workflows also improve governance by centralizing lineage and access policies. Vendors embed pre-built connectors for SaaS, databases, and event streams so teams accelerate project kick-off. Over time, rising feature parity may commoditize basic functions, shifting differentiation toward AI-powered optimization and domain-specific accelerators. Robust partner ecosystems and certification programs will become decisive purchase factors.

By Deployment Model: Cloud Outpaces On-Premises

Cloud deployments represented 66.35% extract, transform, and load (ETL) market size in 2025 and will post the fastest 17.42% CAGR. Elastic compute and serverless jobs eliminate capacity planning headaches and align costs with usage. AWS Glue automatically provisions workers then shuts them down after job completion. On-premises installations still protect sensitive workloads in heavily regulated industries but capture just 33.65% share.

Hybrid patterns are gaining traction as data-sovereignty rules require local processing while analytics teams crave cloud elasticity. Vendors now offer identical runtimes for public cloud and private Kubernetes clusters so customers migrate at their own pace. Long-term competitiveness will hinge on delivering unified monitoring and policy enforcement across environments.

By Enterprise Size: SME Growth Surges

Large enterprises retained 62.03% of 2025 revenue due to complex data estates and higher average contract values. Yet SMEs represent the fastest-rising pool, expanding 18.48% annually thanks to no-code interfaces and subscription pricing. Pre-configured connectors from Fivetran let smaller firms launch pipelines in days rather than months fivetran.com. Vendors increasingly tailor starter bundles with limited compute hours to lower entry barriers.

As SMEs mature, they upgrade to enterprise tiers that offer fine-grained governance and advanced transformations. Community forums and marketplace templates foster self-help, reducing dependence on expensive consultants. For vendors, land-and-expand strategies in this cohort promise durable revenue streams.

By End-User Industry: Healthcare Momentum Builds

BFSI captured 22.86% of 2025 revenue because daily risk calculations and regulatory reporting demand deterministic data lineage. However, healthcare and life sciences are forecast to grow 17.55% through 2031, making them the fastest-advancing vertical. Hospitals integrate imaging, genomics, and wearable data for precision-medicine projects, placing heavy loads on ETL infrastructure. Interoperability mandates such as FHIR further drive adoption.

Retail, telecom, and manufacturing also ramp spending to personalize experiences and enable predictive maintenance. Manufacturing firms stream IoT sensor data into cloud warehouses to optimize equipment uptime, highlighting the breadth of use cases the extract, transform, and load (ETL) market must serve.

Geography Analysis

North America contributed 39.32% of global revenue in 2025, enabled by mature cloud ecosystems, strict governance frameworks, and aggressive AI experimentation. United States enterprises routinely pilot serverless ingestion into Amazon Redshift and Snowflake, while Canada leverages ETL for resource-sector analytics projects. Mexico’s manufacturing digitization under nearshoring initiatives creates fresh demand for mid-market solutions.

Asia-Pacific posts the fastest 17.08% CAGR, propelled by e-commerce in China, IT services scale in India, and Industry 4.0 rollouts in Japan and South Korea. Government incentives for cloud adoption and digital-skills training accelerate uptake. Australia focuses on mining analytics, and emerging ASEAN markets invest in citizen-service portals that need reliable data synchronization .

Europe shows steady expansion anchored by GDPR compliance requirements. German manufacturers deploy real-time ETL for supply-chain visibility, while UK banks integrate open-banking feeds. France and Spain apply ETL to telecom churn-reduction programs. Middle East and Africa remain nascent but Saudi Arabia and United Arab Emirates lead regional pilots tied to smart-city blueprints. South Africa’s financial sector also increases spending. Together, these dynamics ensure the extract, transform, and load (ETL) market gains resilience across geographies.

Competitive Landscape

The market remains moderately consolidated. Informatica, IBM, Microsoft, AWS, Google Cloud, and Oracle are major players, leveraging broad connector libraries and AI-infused automation. Informatica’s CLAIRE engine suggests mappings and optimizes resource allocation, cutting development time. Meanwhile, hyperscalers integrate ETL into native warehouse services, placing price pressure on independents.

Strategic deals reshape positioning. Salesforce’s May 2025 agreement to acquire Informatica merges customer-relationship data with deep integration tooling and may spur rivals to pair analytics and integration capabilities. Fivetran’s takeover of Census adds reverse ETL so operational systems receive fresh insights in near real time. Such moves illustrate how bidirectional data flow defines next-generation architectures.

Emerging vendors attack white spaces: Airbyte commercializes open-source connectors, dbt Labs streamlines in-warehouse transformations, and Databricks unifies lakehouse storage with streaming jobs. Competitive advantage will increasingly hinge on vertical accelerators, governance depth, and the ability to manage data at the edge. Vendors able to bundle ingestion, transformation, quality, and observability in one SKU are best placed to defend share in the extract, transform, and load (ETL) market.

Extract, Transform, And Load (ETL) Industry Leaders

IBM Corporation

Oracle Corporation

Informatica LLC

Microsoft Corporation

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Salesforce signed a definitive agreement to acquire Informatica, combining CRM and data-integration capabilities.

- May 2025: Fivetran acquired Census to add reverse ETL and real-time data synchronization.

- March 2025: Domo introduced SQL Action, Column Search, and undo/redo within Magic ETL for improved developer control.

- December 2024: Algolia launched Data Transmissions, enabling customers to enrich data before search indexing through built-in ETL functions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the extract, transform, and load (ETL) market as all software and managed services that automate the ingestion of structured or semi-structured data from disparate sources, apply business-rule transformations, and load the cleansed datasets into a target store for analytics or machine-learning workloads.

Scope Exclusions: Stand-alone reverse-ETL tools, generic iPaaS suites that never perform in-pipeline transformation, and professional services sold on a time-and-materials basis are not counted.

Segmentation Overview

- By Component

- Software

- ETL Tools

- ELT and Streaming Integration Tools

- Integration Platform as a Service (iPaaS)

- Services

- Managed Services

- Professional Services

- Software

- By Deployment Model

- On-Premises

- Cloud

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-user Industry

- BFSI

- IT and Telecom

- Healthcare and Life Sciences

- Retail and E-commerce

- Manufacturing

- Media and Entertainment

- Government and Public Sector

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews with data engineers, chief data officers, and channel partners across North America, Europe, and Asia-Pacific; we also fielded short surveys to cloud-platform solution architects. These conversations clarified average license volumes, emerging use cases such as Gen-AI training pipelines, and regional compliance hurdles, giving us confidence to adjust desk-derived assumptions.

Desk Research

We began by scraping freely available statistics from tier-1 public sources such as the US Bureau of Labor Statistics, Eurostat ICT indicators, Singapore IMDA digital-economy reports, and OECD cloud-adoption datasets, which reveal enterprise data-engineering spend patterns. Company 10-Ks, S-1s, and investor presentations helped our team approximate average selling prices and contract lengths. To tighten regional shipment splits, customs data accessed via Volza and patent-filing intensity sourced through Questel were layered in. News and financial feeds from Dow Jones Factiva supplied deal flow that signaled real demand inflections. This list is illustrative, not exhaustive, as dozens of additional webpages, journals, and filings were reviewed for cross-checks.

Market-Sizing & Forecasting

A top-down construct starts with global enterprise software outlays, then applies ETL penetration ratios derived from production and trade data before being further filtered through cloud-migration milestones. Select bottom-up roll-ups, sampled vendor bookings multiplied by prevailing ASPs, serve as guardrails that rein in over- or under-estimation. Key variables tracked include migration of data warehouses to cloud, average data-volume growth per company, subscription versus perpetual license mix, regional GDP growth in data-intensive sectors, and regulatory mandates on data residency. Multivariate regression blends these drivers and projects revenues through 2030; gaps in bottom-up coverage are bridged by applying weighted regional analogs vetted with industry experts.

Data Validation & Update Cycle

Each quarter, our model output is matched against external spend trackers, press-released contract values, and patent-filing spikes. Variances above preset thresholds trigger re-checks with original respondents, and a senior analyst signs off only after anomaly resolution. Reports refresh annually, with mid-cycle updates when material events, such as major M&A or regulatory shifts, occur.

Why Mordor's Extract, Transform, and Load Market Baseline Commands Reliability

Published figures often diverge because firms choose differing scopes, mix years, or roll multiple adjacent categories into one headline number. Our disciplined boundary setting and annual refresh cadence minimize such noise, ensuring decision-makers receive a balanced, current baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.85 B (2025) | Mordor Intelligence | - |

| USD 17.58 B (2025) | Global Consultancy A | Counts wider data-integration stack including API, streaming, and data-prep platforms |

| USD 12.09 B (2024) | Trade Journal B | Measures entire data-pipeline tools space; ETL is only one sub-segment |

| USD 6.70 B (2023) | Industry Portal C | Uses older base year and excludes cloud-native subscription revenue uplift |

In short, while rival publications either stretch the scope or rely on outdated baselines, we at Mordor Intelligence keep the lens squarely on true ETL activity, refresh assumptions every year, and reconcile top-down trends with ground-level purchase realities, giving clients a dependable, transparent starting point for strategy.

Key Questions Answered in the Report

What is the current size of the extract, transform, and load (ETL) market?

The market is valued at USD 10.24 billion in 2026.

How fast will the extract, transform, and load (ETL) market grow through 2031?

It is forecast to expand at a 15.72% CAGR, reaching USD 21.25 billion by 2031.

Which component segment leads the extract, transform, and load (ETL) market?

Software dominates with 70.92% revenue share because enterprises prefer integrated platforms.

Why are SMEs the fastest-growing customer group in ETL?

No-code tools and subscription pricing make advanced data-integration capabilities accessible without large technical teams.

How will Salesforce’s acquisition of Informatica influence the competitive landscape?

The deal combines CRM and data-integration capabilities, pressuring standalone vendors to deepen functionality or pursue similar partnerships.

Page last updated on: