ELISpot And FluoroSpot Assay Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

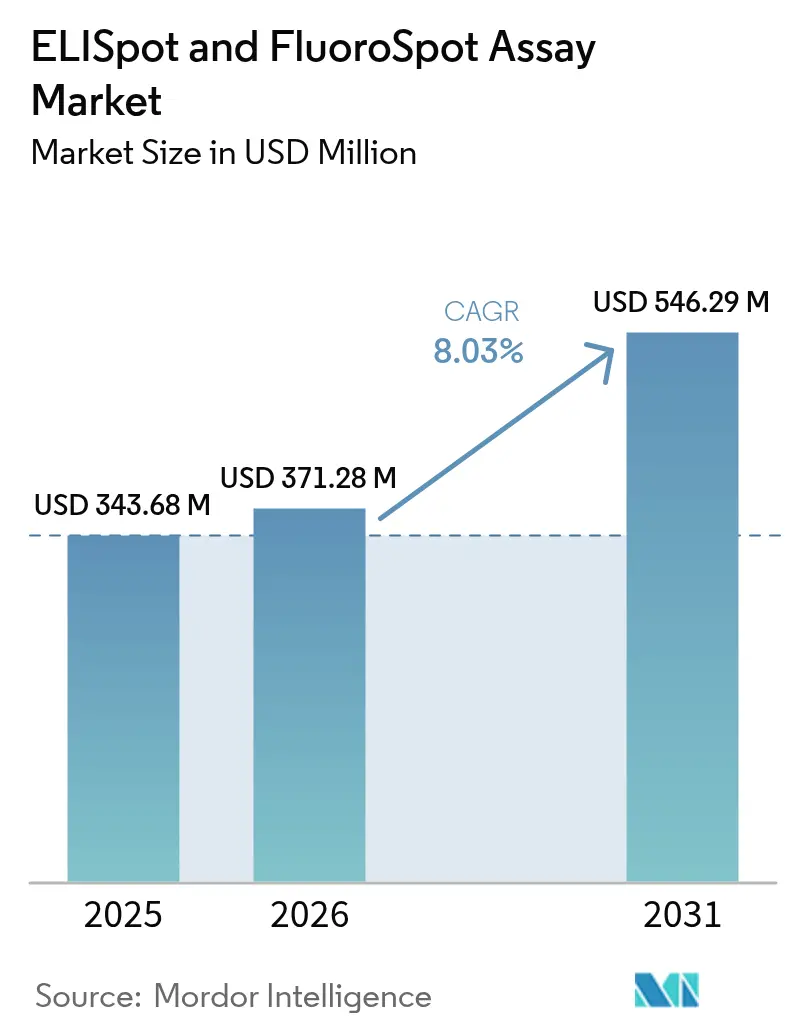

| Market Size (2026) | USD 371.28 Million |

| Market Size (2031) | USD 546.29 Million |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ELISpot And FluoroSpot Assay Market Analysis by Mordor Intelligence

The ELISpot FluoroSpot Assay market size is expected to grow from USD 343.68 million in 2025 to USD 371.28 million in 2026 and is forecast to reach USD 546.29 million by 2031 at 8.03% CAGR over 2026-2031. Intensifying vaccine pipelines after COVID-19, wider clinical adoption of T-cell assays for biologics approval and steady cost declines in open-architecture hardware are combining to keep growth momentum strong. Hospital laboratories are standardizing functional immune-monitoring panels, research organizations are outsourcing large volumes of assay work to specialized CROs and regulators are embedding T-cell functionality metrics in licensure packages for next-generation immunotherapies. Parallel advances in automated image capture, machine-learning-based spot counting and microfluidic chip formats are reshaping laboratory workflows and widening global access. Competitive dynamics remain moderate, with incumbent assay leaders facing new entrants offering AI-enhanced analytics and portable devices that push the ELISpot FluoroSpot Assay market into point-of-care settings.

Key Report Takeaways

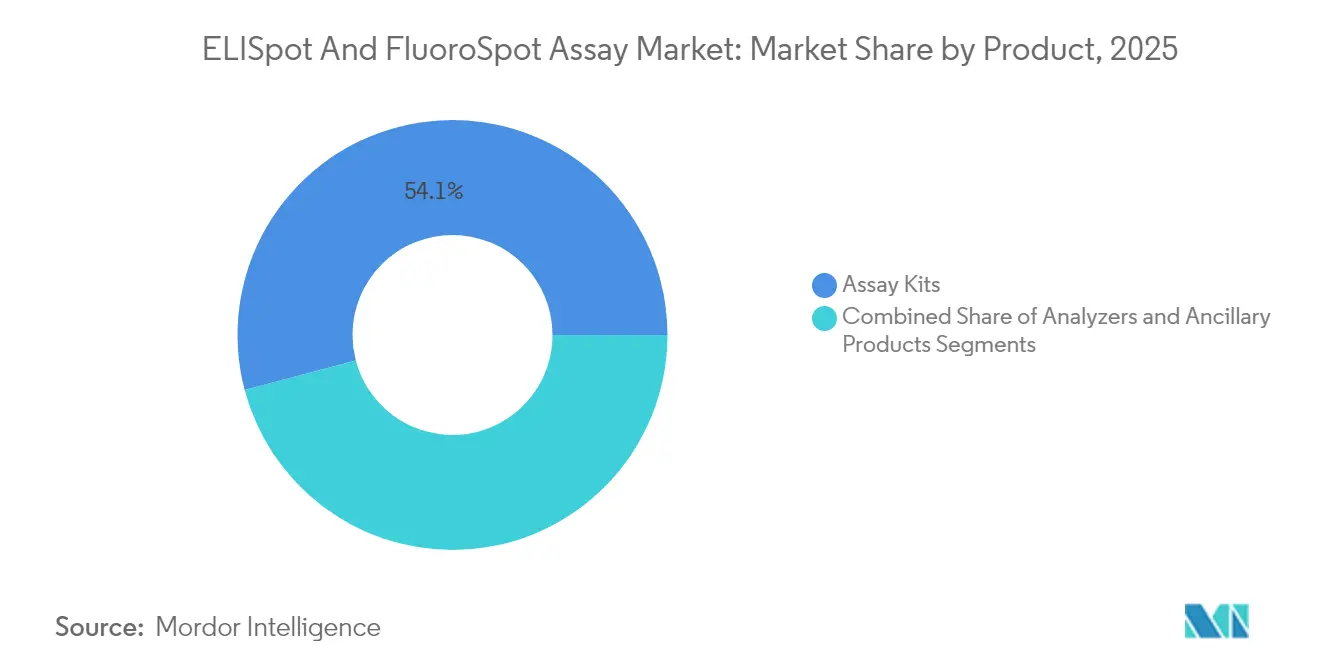

- By product type, Assay Kits led with 54.11% of the ELISpot FluoroSpot Assay market share in 2025, whereas Analyzers are projected to post the fastest 13.89% CAGR through 2031.

- By end-user, Hospitals & Clinical Laboratories captured 64.73% of the ELISpot FluoroSpot Assay market in 2025; Research Institutes & CROs hold the fastest outlook at 15.46% CAGR to 2031.

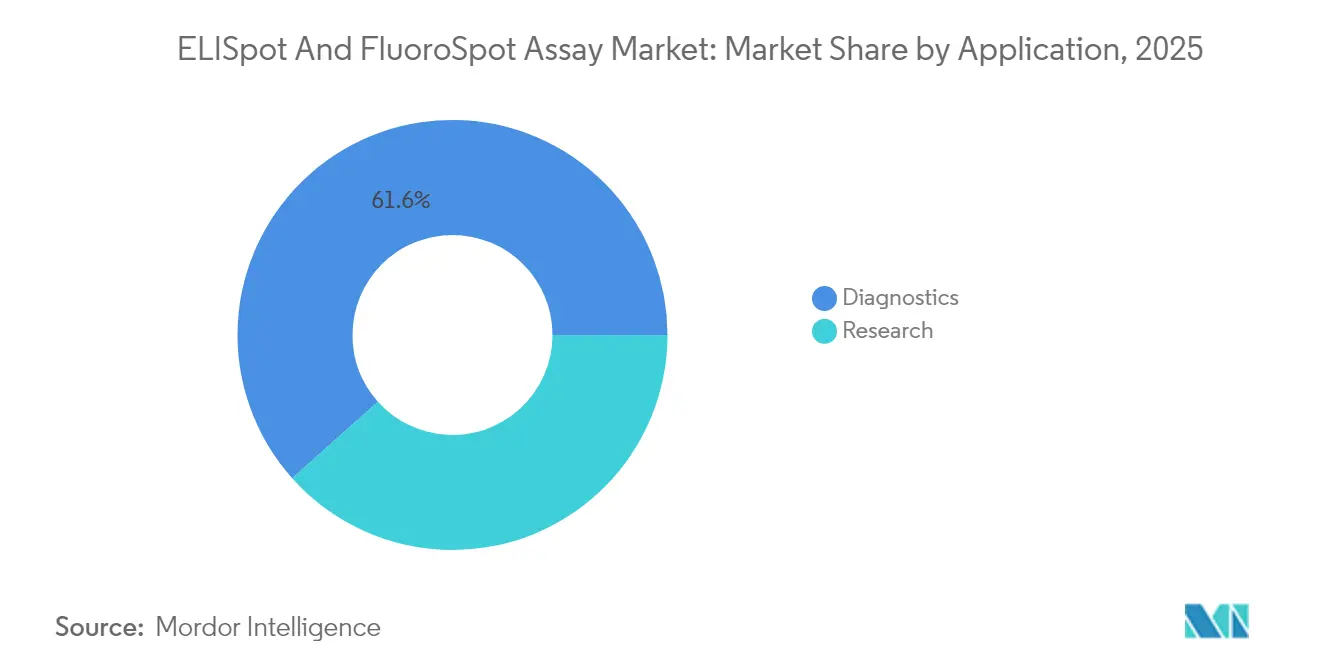

- By application, Diagnostics accounted for 61.61% of demand in 2025, while Research use is expected to record a 13.92% CAGR to 2031.

- By technology, Digital/AI-enhanced platforms are set to advance at 16.33% CAGR, outpacing the mature Colorimetric segment that retained 39.78% revenue in 2025.

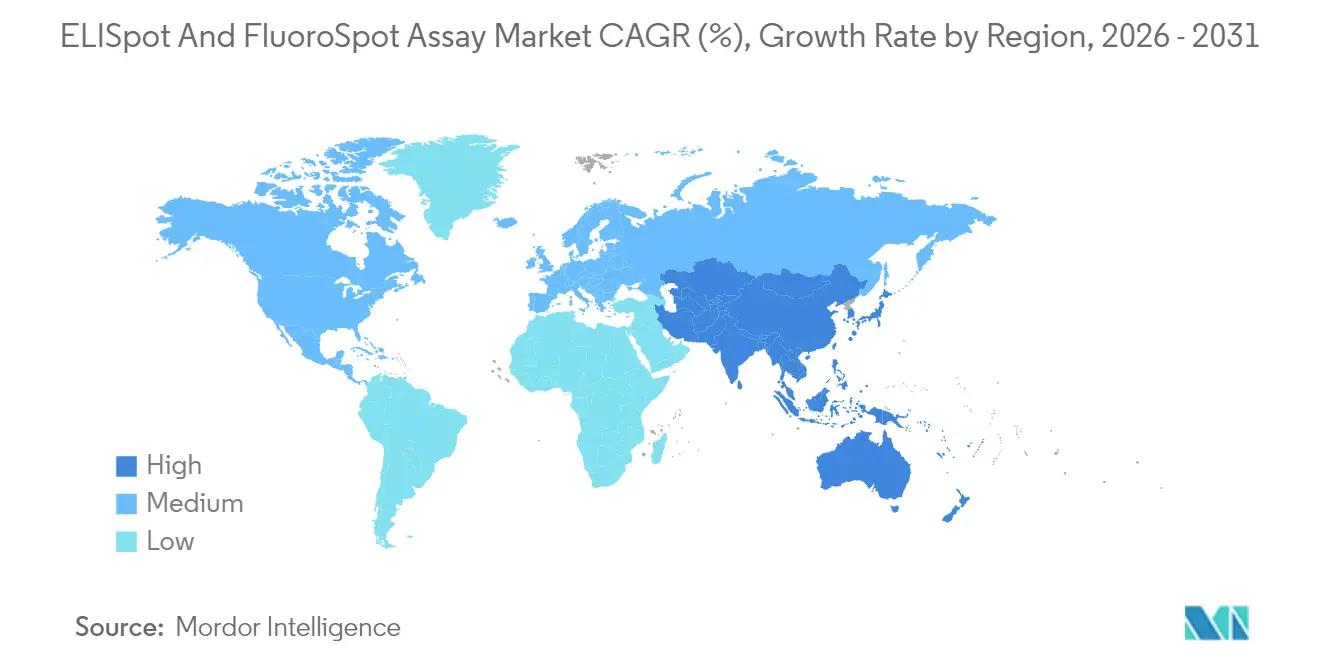

- By geography, North America commanded 38.22% revenue in 2025; Asia-Pacific is on track to deliver a 13.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global ELISpot And FluoroSpot Assay Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence Of Chronic & Infectious Diseases | +1.8% | Global, with highest impact in Asia-Pacific and Sub-Saharan Africa | Medium term (2-4 years) |

| Rapid Vaccine Pipeline Expansion Post-COVID-19 | +2.1% | North America & EU core, expanding to APAC | Short term (≤ 2 years) |

| Technological Breakthroughs In Multiplex Fluorospot Readers | +1.4% | North America & EU, early adoption in Japan and South Korea | Medium term (2-4 years) |

| Regulatory Push For Functional T-Cell Assays In Cell-Therapy QC | +1.6% | North America & EU, with regulatory harmonization spreading globally | Long term (≥ 4 years) |

| Cost Decline Via Open-Source, 3-D-Printed ELISpot Hardware | +0.9% | Global, with highest impact in resource-limited settings | Long term (≥ 4 years) |

| Microfluidic Elispot-On-Chip Enabling PoC Immunomonitoring | +1.2% | Global, with early gains in North America, EU, and urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic & Infectious Diseases

Increasing caseloads of tuberculosis, HIV, viral hepatitis and cancer are boosting demand for precise cellular immune-monitoring. The T-SPOT.TB test now registers 99% sensitivity and 94% specificity, outperforming traditional methods and solidifying ELISpot technology as a frontline diagnostic. FDA clearance of automated T-SPOT-compatible liquid-handling workstations in 2025 further validates clinical use. Oncology centres routinely employ interferon-γ and IL-2 ELISpot panels to track neoantigen-specific responses that guide checkpoint-inhibitor dosing. WHO recommendations calling for broader access to quality diagnostics in high-burden regions align with the ELISpot FluoroSpot Assay market expansion because functional assays detect low-frequency T-cells missed by serological tests. As non-communicable disease prevalence rises alongside infectious threats, broad clinical adoption of standardized ELISpot workflows is likely to remain a durable growth pillar.

Rapid Vaccine Pipeline Expansion Post-COVID-19

Vaccine developers are shifting focus from antibody-centric endpoints toward cellular immunity. BARDA-sponsored phase 2b designs for next-generation COVID-19 vaccines explicitly integrate T-cell assays to demonstrate broader and longer-lasting protection. The same requirement now features in seasonal influenza programs attempting to overcome strain-specific limitations. The Center for Biologics Evaluation and Research reported 17 biologics licenses granted in 2024 that necessitated functional immune data, cementing assay use in regulatory dossiers. In turn, CROs and in-house laboratories are scaling the ELISpot FluoroSpot Assay market by installing multiplex readers that quantify cross-reactive immunity across variant lineages. Universal vaccine research targeting conserved epitopes further strengthens the need to capture polyfunctional T-cell outputs that colorimetric ELISA cannot reveal.

Technological Breakthroughs in Multiplex FluoroSpot Readers

Affordable high-resolution fluorescence optics and embedded AI now allow simultaneous measurement of multiple cytokines released from single T-cells. Open-source microscopes priced below USD 15,000 achieve image quality rivalling commercial units that once cost USD 100,000, driving technology democratization[1]eLife, “An open-source, high-resolution, automated fluorescence microscope,” elifesciences.org. Machine-learning algorithms eliminate operator bias by automating spot detection and classification, delivering inter-laboratory concordance comparable to expert pathologists. Multiplex FluoroSpot readers combining four or more fluorescent filters provide comprehensive data on polyfunctionality, a critical biomarker of vaccine efficacy and CAR-T potency. These innovations widen the ELISpot FluoroSpot Assay market beyond research institutes into mainstream clinical settings, encouraging standardized throughput solutions in mid-volume laboratories.

Regulatory Push for Functional T-Cell Assays in Cell-Therapy QC

Long-term success of CAR-T and other adoptive cell therapies depends on reliable potency assays embedded in GMP workflows. FDA guidance released in 2025 mandates validated functional readouts to confirm lot consistency for living-cell products. ELISpot protocols are becoming critical quality attributes because they measure antigen-specific cytokine secretion directly linked to therapeutic efficacy. International Medical Device Regulators Forum templates are harmonizing submission content, enabling multi-region approvals that rely on the same ELISpot data package[2]IMDRF, “Non-In Vitro Diagnostic Device Regulatory Submission Table of Contents,” imdrf.org. As cell-therapy capacity expands from North America and Europe to Asia-Pacific, demand for turnkey, CFR Part 11-compliant ELISpot systems is expected to sustain a robust order pipeline for instrument makers and kit suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability Of Alternate High-Parameter Flow-Cytometry & CyTOF Platforms | -1.3% | North America & EU, with emerging impact in Asia-Pacific | Medium term (2-4 years) |

| High Capital Cost Of Automated Analyzers & Image-Analysis Software | -0.9% | Global, with highest impact in emerging markets | Short term (≤ 2 years) |

| Data-Analysis Complexity And Lack Of Bio-Informatics Skillsets | -0.7% | Global, with particular challenges in resource-limited settings | Long term (≥ 4 years) |

| Inter-Lab Variability Due To Weak Assay Standardization | -0.8% | Global, with regulatory focus in North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of Alternate High-Parameter Flow-Cytometry & CyTOF Platforms

Forty-five-color full-spectrum cytometry and mass cytometry can delineate complex immune landscapes at single-cell resolution, positioning these platforms as credible substitutes where deep phenotyping outweighs functional readouts. Studies comparing 33-marker CyTOF and spectral flow panels demonstrate high concordance in quantifying immune subsets across clinical samples. Laboratories that already own cytometers may upgrade to ultra-high-parameter configurations instead of purchasing separate ELISpot readers, thereby tempering incremental instrument demand. While ELISpot retains an edge in detecting low-frequency functional responses, technology overlap is likely to intensify procurement deliberations in large reference centres.

High Capital Cost of Automated Analyzers & Image-Analysis Software

Commercial fluorescence readers typically list between USD 150,000 and USD 300,000 and require proprietary algorithms that can add another USD 100,000 in software fees. Full-workflow automation platforms surpass USD 500,000 when robotic liquid handlers and incubators are included. Even though open-hardware designs are emerging, many small laboratories grapple with return-on-investment calculations, particularly in emerging economies. Revenue-share leasing models are appearing, yet high upfront spend remains a headwind that slows adoption even in markets where clinical need is evident.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumable-Driven Dominance with Analyzer Acceleration

At USD 185.97 million revenue in 2025, Assay Kits generated more than half of total spending, echoing the recurring requirement for cytokine-coated wells and detection antibodies. Laboratories reorder these consumables for each run, ensuring steady replenishment streams. Analyzer demand, although forming a smaller base, is projected to outpace kits thanks to a 13.89% CAGR as automation and AI analytics become routine in high-throughput settings. Portable FluoroSpot readers targeting tuberculosis screening programs in community clinics add incremental volume. The ELISpot FluoroSpot Assay market size for analyzers could exceed USD 151.3 million by 2031 under the current replacement cycle, creating a fertile aftermarket for image-analysis upgrades and service contracts. Ancillary items—membrane plates, calibration standards and machine-learning licenses—complement core kit sales, with AI software packages providing premium margin opportunities for vendors.

Assay Kit leadership rests on a robust catalogue that spans single-cytokine IFN-γ kits to multiplex IL-2/Granzyme-B bundles essential for oncology research. Pandemic-era SARS-CoV-2 ELISpot kits still post reorder volumes for booster-shot evaluation, though growth moderates as broader use cases such as tuberculosis and CMV monitoring gain share. Manufacturers are experimenting with universal plate chemistries that cut per-test cost nearly 15%, further expanding global penetration. The rising popularity of open-source 3D-printed plate holders underscores a shift toward cost-sensitive solutions in developing countries, reinforcing consumables’ sustained primacy in the ELISpot FluoroSpot Assay market.

By End-User: Clinical Supremacy alongside CRO Surge

Hospitals and clinical laboratories processed the majority of routine tuberculosis, transplant and primary-immunodeficiency ELISpot panels in 2025, capturing roughly USD 222.46 million in kit and service spending. Regulatory endorsement of automated TB workflows boosts test standardization and throughput, allowing these sites to retain leadership. Nonetheless, Research Institutes and CROs are on pace for a 15.46% CAGR, benefiting from outsourced vaccine and immunotherapy programs that require high-volume, rapid-turnaround cellular assays. Contract organizations bundle ELISpot with flow cytometry and cytokine multiplexing, offering integrated immune-monitoring packages attractive to biopharma sponsors.

Biopharmaceutical and vaccine manufacturers rely on in-house potency testing to meet regulatory timelines, representing a steady mid-single-digit growth niche. Academic centres extend market breadth by pursuing fundamental T-cell biology, often piloting advanced FluoroSpot configurations that later migrate into clinical use. As personalized medicine trials proliferate, CROs will likely assume a larger slice of the ELISpot FluoroSpot Assay market size because their global lab networks can enrol geographically diverse subjects and deliver harmonized data sets for regulatory dossiers.

By Application: Diagnostics Hold Majority while Research Accelerates

Diagnostic use of ELISpot continues to dominate on the back of tuberculosis screening programs where sensitivity and specificity benchmarks eclipse tuberculin skin tests. Growing interest in transplant immunology, autoimmunity panels and latent viral infection monitoring ensures sustained diagnostic revenue. Meanwhile, research applications are climbing swiftly as vaccine, oncology and gene-therapy sponsors employ ELISpot to monitor antigen-specific T-cells in early-phase studies. The ELISpot FluoroSpot Assay market share for research could breach 40% by decade-end if current funding trends persist. Vaccine developers, in particular, favour multiplex FluoroSpot approaches to demonstrate cross-variant T-cell immunity, differentiating candidates in crowded fields.

Cancer centres leverage neoantigen ELISpot assays to stratify patients for checkpoint blockade or dendritic-cell vaccines. In cell-therapy release testing, regulators now expect cytokine-secretion data to verify product potency, embedding research-style assays into commercial manufacturing. This convergence of clinical and investigational workflows blurs traditional application lines and reinforces ELISpot’s relevance across the drug-development continuum.

By Technology: Colorimetric Stability versus Digital Disruption

Colorimetric ELISpot remains ubiquitous due to decades of validation, straightforward reagent handling and low equipment cost. Yet its share is gradually ceding to FluoroSpot and AI-enhanced digital detection, both of which allow simultaneous read-outs of multiple cytokines and objective quantification. Digital platforms incorporating convolutional neural networks deliver reproducible counts across sites, addressing the long-standing inter-laboratory variability restraint on broader adoption. The ELISpot FluoroSpot Assay market size tied to digital/AI formats is projected to grow at 16.33% CAGR, reaching an estimated USD 177.9 million by 2031, aided by cloud-based analytics that fit hybrid working models common in CROs and academic consortia.

Microfluidic ELISpot-on-chip prototypes shrink sample volume and processing time, opening doors to near-patient immune monitoring in oncology clinics and field epidemiology. While still nascent, these devices could lower cost per test by up to 40% once volume manufacturing scales, potentially reshaping technology preferences in emerging economies.

Geography Analysis

North America generated USD 131.35 million revenue in 2025, equivalent to 38.22% of global sales, and benefits from advanced biopharmaceutical clusters, strong reimbursement and FDA guidance that enshrines ELISpot in vaccine and cell-therapy submissions. Large reference laboratories run high-volume tuberculosis and CMV panels, and research hospitals integrate multiplex FluoroSpot into immuno-oncology programs. Canada contributes steady growth through public-health diagnostics and a rising cell-therapy manufacturing footprint, reinforcing regional leadership.

Europe follows with entrenched pharmaceutical R&D ecosystems and EMA frameworks that support functional immune monitoring. Germany, the United Kingdom and the Nordics exhibit high analyzer installations, while cross-border academic consortia spur demand for AI-enhanced digital readers. Adoption also leans on European Union funding lines that underwrite translational immunology and personalized-medicine projects requiring standardized cellular assays. The ELISpot FluoroSpot Assay market size captured in Europe is projected to expand at a mid-single-digit CAGR, aided by regulatory harmonization that lowers validation overheads across member states.

Asia-Pacific is the fastest-growing territory at 13.34% CAGR, underpinned by expanding vaccine manufacturing in China, robust biotechnology investment in South Korea and Japan and emerging contract-research clusters in India. Government programs targeting tuberculosis elimination generate bulk kit orders, while rising CAR-T clinical trials open a high-value analyzer and software market. Public-private partnerships establish reference labs equipped with multiplex FluoroSpot systems, accelerating technology diffusion. Southeast Asian nations leverage microfluidic ELISpot-on-chip pilots to deliver point-of-care diagnostics in remote areas, underscoring the region’s appetite for cost-efficient innovation. Collectively, Asia-Pacific could command nearly one-third of incremental global revenue through 2031, reshaping geographic hierarchy in the ELISpot FluoroSpot Assay market.

Regulatory Landscape

ELISpot and FluoroSpot assays used in diagnostics and regulated clinical trial immunomonitoring generally fall within established medical-device and IVD frameworks, but they still require assay-specific validation packages due to the lack of a single universal regulator-issued standard dedicated to these functional T-cell assays. In the United States, assay platforms and workflow components may enter through FDA pathways such as 510(k) for Class II devices, and the FDA final guidance for potency tests for cellular and gene therapy products (issued in 2025) has reinforced the need for validated functional readouts when ELISpot-style assays are used in lot release or potency strategies for living-cell products.

In Europe, Regulation (EU) 2017/746 (IVDR) continues to raise evidence expectations for IVDs, including performance evaluation and quality management requirements that shape ELISpot-based diagnostic offerings and supporting software. Commission Regulation (EU) 2024/1860, in force from 9 July 2024, extended certain IVDR transition timelines for legacy devices, keeping conformity assessment capacity and notified-body throughput central considerations for suppliers maintaining or expanding CE-marked assay and instrument portfolios. MDCG guidance remains a useful reference layer for interpretation and implementation, particularly where software functions such as spot counting, audit trails, and data integrity intersect with clinical decision support and regulated laboratory workflows.

Competitive Landscape

The ELISpot FluoroSpot Assay market remains moderately fragmented: the top five suppliers together hold a significant revenue, leaving meaningful share for niche innovators. Oxford Immunotec, Cellular Technology Limited and Becton Dickinson anchor portfolios covering kits, analyzers and proprietary software, leveraging established distribution and regulatory expertise. Thermo Fisher Scientific broadened its immuno-assay footprint through the USD 3.1 billion Olink acquisition, signalling convergence between proteomics and cellular immune monitoring[3]Thermo Fisher Scientific Investor Relations, “Thermo Fisher Scientific Completes Acquisition of Olink,” thermofisher.com. BD teamed with Quest Diagnostics to co-develop flow-cytometry-based companion diagnostics that integrate ELISpot data streams, reflecting a shift toward multi-modal test ecosystems.

Emerging players pursue AI-first platforms that bundle cloud analytics, remote calibration and pay-per-sample pricing geared toward CROs and decentralized trials. Open-hardware collectives release validated 3D-print files for plate readers, undercutting incumbents in price-sensitive markets yet spurring service revenues around training and calibration. Competitive focus is tilting toward end-to-end immune-monitoring suites that marry sample prep robotics, multiplex FluoroSpot and AI scoring under a single software license, enabling laboratories to trim hands-on time by up to 40%. Vendors also court cell-therapy developers with CFR Part 11-compliant audit trails and traceability modules that satisfy regulators’ electronic-records mandates, deepening stickiness among GMP users.

Incumbent differentiation increasingly hinges on assay-menu breadth and validation under real-world conditions, not merely hardware specifications. To defend share, leading firms invest in collaborative clinical studies linking ELISpot metrics to patient outcomes, thereby turning data exclusivity into a commercial moat. Mid-tier companies fill white-space opportunities in portable systems targeting outbreak regions, while service-oriented specialists monetise algorithm upgrades through subscription models that add recurring revenue layers over installed bases.

ELISpot And FluoroSpot Assay Industry Leaders

Becton, Dickinson and Company

U-CyTech biosciences

Cellular Technologies Limited (CTL)

Mabtech AB

Abcam plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White-space opportunities cluster around regulated, standardized immune-monitoring workflows where sponsors and public laboratories prioritize method continuity across multi-site programs. One signal of this preference is the UK Health Security Agency awarding a direct 1-year contract in February 2025 to Mabtech AB for ELISpot and FluoroSpot kits and reagents to maintain continuity of test data and compliance in laboratory operations. This procurement behavior supports opportunities for vendors that can lock in validated assay menus, controls, and training bundles, along with CRO-facing services that reduce inter-lab variability and simplify data-analysis burden.

Technology-led expansion is also widening use cases beyond traditional T-cell cytokine secretion panels. In January 2026, published work demonstrated extending ImmunoSpot (ELISpot/FluoroSpot) sensitivity to detect rare antigen-specific B cells at frequencies around 1 in 1 million or lower, which creates further adoption space in vaccine and durability-of-immunity programs that track memory B cell and antibody-secreting cell function. At the same time, multiplex FluoroSpot formats, including multi-cytokine panels, show differentiation value in tuberculosis infection staging compared with single-analyte approaches, creating a pathway for higher-value diagnostic and clinical-trial endpoints when paired with validated analysis software and reproducible workflows.

Recent Industry Developments

- April 2026: VION Biosciences closed its acquisition of Cellular Technology Limited (CTL), bringing CTL's functional immune monitoring analyzers, software, and services under a broader platform portfolio. The deal strengthens vertical integration across instrumentation and assay services, supporting bundled offerings for high-throughput immunomonitoring in vaccine and immunotherapy programs.

- April 2025: Revvity received FDA clearance for its Auto-Pure 2400 liquid-handling platform to automate the T-SPOT.TB workflow, enabling higher throughput and reducing pre-analytical variability. The clearance supports deeper clinical-lab standardization and increases pull-through demand for compatible ELISpot-based TB testing workflows.

- December 2024: Virax Biolabs signed a distribution agreement with Tebubio for its ImmuneSelect portfolio across the European Union, Norway, and Switzerland. The expansion improved regional access for research laboratories and strengthened channel coverage for immune-monitoring assay demand tied to translational studies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is the revenue generated from ELISpot and FluoroSpot assay solutions used to measure antigen specific cellular immune responses, counted across instruments, kits, and supporting consumables sold for research and clinical laboratory use.

Scope exclusions: This sizing does not count broader immunoassays that are not ELISpot or FluoroSpot based, and it also excludes general lab equipment revenue not tied to these assays.

Segmentation Overview

- By Product

- Analyzers

- Automated Plate Readers

- Portable FluoroSpot Readers

- Assay Kits

- Cytokine-specific ELISpot Kits

- Multiplex FluoroSpot Kits

- SARS-CoV-2 T-cell Kits

- Ancillary Products

- Membrane Plates & Reagents

- Image-analysis Software

- Analyzers

- By End-User

- Hospitals & Clinical Laboratories

- Biopharmaceutical & Vaccine Manufacturers

- Research Institutes & Contract Research Organisations

- By Application

- Research

- Vaccine Development

- Clinical Trials Immunomonitoring

- Cancer Immunotherapy Research

- Cell & Gene-Therapy Release Testing

- Diagnostics

- Infectious Disease Diagnostics

- Transplant Immunology

- Autoimmune Disease Panels

- Tuberculosis Diagnostics

- Research

- By Technology

- Colorimetric ELISpot

- FluoroSpot

- Digital/AI-enhanced ELISpot

- Microfluidic ELISpot-on-Chip

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started by mapping where ELISpot and FluoroSpot assays are actually used, then matching those demand points to supply side signals from public materials. We referenced the US FDA databases and related guidance notes for the regulatory context around immunology testing, NIH activity levels, and ClinicalTrials.gov listings for immunology and vaccine study work, and we used World Health Organization updates on infectious disease and immunization priorities to understand demand direction.

To keep the model anchored, we also reviewed peer reviewed immunology journals for assay adoption patterns, and we used trade and customs statistics where available for instrument and reagent movement. Company filings, product brochures, and investor presentations were used to understand pricing ranges, product refresh cycles, and route to market. In a limited way, we used paid subscriptions for company financials and intelligence, news and financials, and patent databases to cross check timelines, product launches, and ownership changes. The sources mentioned here are illustrative, and additional public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on speaking with assay users and supply side participants who influence purchasing decisions, workflow choices, and pricing discussions in routine settings. Responses were checked across major regions so assumptions on kit usage per study, instrument utilization, and the pace of lab adoption could be corrected before the final model build.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | APAC: 50% |

| Mid tier: 53% | Functional/Unit leaders: 37% | EMEA: 31% |

| Smaller Players: 18% | Managers: 49% | Americas: 19% |

Market-Sizing & Forecasting

The core sizing uses a top-down build that starts from the addressable immunology testing and research activity pool, then applies adoption and spending rates specific to ELISpot and FluoroSpot workflows. To keep the total realistic, we corroborate it with selective bottom-up checks, including sampled average selling price ranges for kits and instruments, typical kits consumed per study and per lab, and channel feedback on order patterns.

Key inputs used in the model include vaccine and immuno-oncology trial volumes, the frequency of T-cell monitoring in those studies, average test panels per patient or sample batch, instrument installed base signals in active labs, and pricing progression for assay kits and antibodies as volumes rise. Where direct volume signals were thin for smaller countries, we filled gaps using proxy indicators such as biomedical R&D intensity and the local mix of academic labs versus biopharma activity, followed by a reasonableness check against regional demand patterns.

For forecasting, we used multivariate regression supported by scenario analysis, since the market responds to multiple drivers at the same time, including clinical trial momentum, infectious disease focus, and lab automation readiness. Assumptions were then tuned using expert feedback on how quickly multi-analyte FluoroSpot adoption is replacing single analyte runs in routine programs.

Data Validation & Update Cycle

Outputs are checked in several passes so the final numbers do not depend on a single assumption. We compare the implied spend per study and per lab against independent signals, review year over year jumps for outliers, and then recheck any variance that is not explained by known product launches or policy shifts.

Before sign-off, the model and inputs are reviewed by another analyst, and any weak spots trigger a re-contact with interviewees for clarification. The report is refreshed each year, and interim updates are made when a material event occurs, such as a major regulatory shift, an unusual change in trial activity, or a meaningful pricing move. Right before delivery, we do a final data pass so clients receive the latest updated view.

Mordor Intelligence's Elispot and Fluorospot Assay Market Size Versus Other Published Estimates

Published market numbers for ELISpot and FluoroSpot assays can differ even when multiple parties describe the same overall area, because each study draws the boundary in its own way. The most common differences come from what is counted as part of assay revenue, which year is treated as the starting point, and how pricing and utilization are projected forward.

In this market, gaps usually come from whether analyzers, kits, and ancillary consumables are all counted together, and whether clinical laboratory usage is included alongside research demand. Some estimates also rely on a single base year and apply a flat growth curve, which can miss swings tied to vaccine and immuno-oncology trial activity and to changing kit pricing as volumes expand.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 343.68 M (2025) | |

| Industry Publisher A | USD 311.80 M (2024) | Uses a different base year and growth window, and the published snapshot does not clearly separate instrument revenue versus recurring kit and consumable revenue, which can compress the starting value depending on what is left out. |

| Industry Publisher B | USD 331.59 M (2025) | Keeps the market definition broad, but the public summary provides limited detail on how kit consumption per study and laboratory utilization are validated, which can shift totals when adoption rates are assumed rather than checked. |

Clinical trial volumes and immunology study activity are two of the main evidence checks that keep Mordor Intelligence's estimate tied to a realistic demand pool for ELISpot and FluoroSpot testing. When the scope, pricing logic, and validation steps are made explicit, the remaining spread across published figures becomes easier to explain and easier for buyers to adjust for their own use case.

Key Questions Answered in the Report

What is driving the strong CAGR in the ELISpot FluoroSpot Assay market?

Wider vaccine pipelines, mandatory functional assays in cell-therapy regulations and AI-enabled multiplex FluoroSpot technology together support the projected 8.03% CAGR through 2031.

Which product segment generates the largest revenue today?

Assay Kits lead with 54.11% revenue because laboratories must purchase fresh consumables for every test run.

Why are Research Institutes and CROs growing faster than hospitals?

Biopharma sponsors outsource immuno-monitoring tasks to CROs, and research institutes need high-throughput ELISpot panels for vaccine and immunotherapy trials, pushing this segment at 15.46% CAGR.

How will Asia-Pacific impact future sales?

Asia-Pacific’s 13.34% CAGR stems from expanding vaccine manufacturing, government TB programs and rising cell-therapy trials, positioning the region to capture a sizeable share of incremental global revenue.

Do high-parameter cytometry platforms threaten ELISpot demand?

Yes, flow-cytometry and CyTOF systems offering 30-plus markers can offset new analyzer purchases, but ELISpot retains superiority for functional, low-frequency T-cell detection.

Page last updated on: